Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Why your employer’s retirement plan may cost you nearly 30% of your savings (and what to do about it)

It won’t make you wealthy overnight, or even in a decade.

However, a well-funded 401(k) plan can very well get you to work optional status over a career, or even in 20 years or less, as mine did for me.

That is, if fees don’t quietly eat away much of your retirement plan balance along the way.

The “1% Fee Rule”

Retirement researchers often highlight a striking rule of thumb.

A seemingly small difference in annual fees can have enormous long-term consequences.

According to the US Department of Labor (DOL), “…1 percent difference in fees and expenses would reduce your account balance at retirement by 28 percent [over a 35-year career].”

That’s not because the fees are so large in any single year. It’s because they compound.

Each year, fees slightly reduce your account balance. That smaller balance then earns less growth from that point on. Over the decades, that lost growth becomes far larger than the fees themselves.

That’s why even small differences in 401(k) costs deserve close attention.

Do Fees Really Vary By That Much?

Indeed, they do.

According to Cision PRWeb’s 2025 401k Averages Book, smaller plans pay more than larger ones. For example, $5 million plans’ average fees total 1.08%, while $50 million plans’ fees average a much lower 0.76%.

What’s worse, they report that for $1 million plans with 100 participants, fees ranged dramatically, from a low of 0.87% to a high of 3.56%!

Why Does This Happen?

Large employers can pay dramatically lower retirement plan fees because they have negotiating power. With thousands of participants and up to a billion dollars or more in assets, they can access institutional share classes and command lower administrative costs.

Small employers simply can’t do the same. And from the wide disparity in small-plan fee levels, some don’t even do as well by their employees as they could!

How Fees Can Injure Your Retirement Plan

Two workers can earn the same salary, save the same percentage, and even invest in the same asset classes, yet one may retire with hundreds of thousands of dollars more than the other!

Further, this may have nothing to do with their investment skills.

It might simply be because of where they work.

Imagine you and your friend are both 25 years old, and both earn the same $85,400 (roughly the median US household income, scaling Fed 2024 data up 2% per Motio research reported by Seeking Alpha).

You each contribute to your 401(k) enough to max out your respective employers’ dollar-for-dollar match up to 6% of compensation. Both of you pick a low-cost ETF that returns an annual average of 7% above inflation.

Your respective compensations track each other, both rising 1% a year faster than inflation.

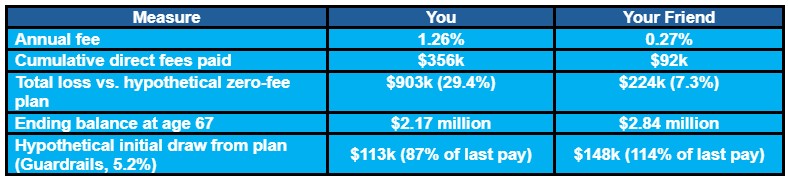

However, your friend works for a much larger employer, whose 401(k) plan manages over $1 billion in assets, so their annual fees are 0.27%, while you work for a small business whose 401(k) plan manages under $1 million, so your annual fees are 1.26%.

That 0.99% difference in annual fees sounds annoying, but surely it doesn’t rise to the level of concern mentioned above, right?

Wrong!

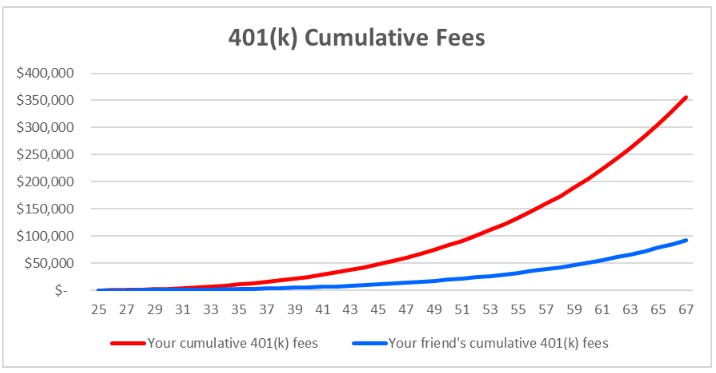

Adjusting for inflation, Figure 1 shows how much each of you would pay in 401(k) fees over your career, assuming you retire at Social Security’s current full retirement age of 67.

By retirement, your friend would pay a sizeable $92k.

You, on the other hand, would be taken to the cleaners, paying nearly four times as much, at $356k!

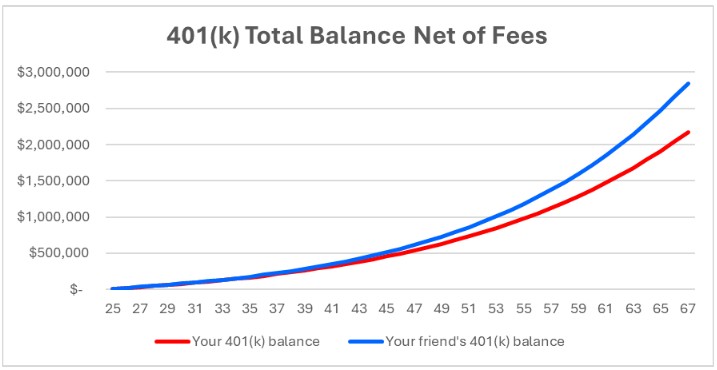

Figure 2 shows your respective 401(k) plan balances over time.

By age 67, your balance would be $2.17 million, while your friend would have $2.85 million!

Those annual fees, less than 1% higher for you, would have eaten $264k more from your account than your friend’s. However, what’s worse is that you’d also lose a good chunk of account growth as a result, for a total loss of over $679k!

That’s because fees reduce your balance each year, leaving less money invested. Over decades, that smaller balance compounds into dramatically lower retirement wealth.

Another way to look at the impact is that you’d need to work to age 67 to end up with the same 401(k) balance that your friend would have around age 63, allowing him to retire nearly four years earlier!

If your friend decided to retire at age 57, with a $1.37 million 401(k) balance, you’d need to keep working to age 60 to reach that same balance.

As Table 1 shows, compared to a hypothetical 401(k) plan with zero fees, your friend loses a total of $224k, or 7% of potential accumulation; while you lose $903k, over 29% of your accumulation. As a result, at age 67, your friend can draw 114% of his last pay, enough for some high-end travel, while you’d need to make do with 87% of yours.

All this becomes far worse if your small employer’s 401(k) plan doesn’t offer solid, low-cost funds like those offered by your friend’s plan. If a similarly performing fund in your plan charges 0.5% more than your friend’s fund, your ending balance would shrink by a further $273k, for a total loss of over 38%!

And all this, because you work for a much smaller employer than your friend!

How Does All This Affect Your Chance of Successful Retirement?

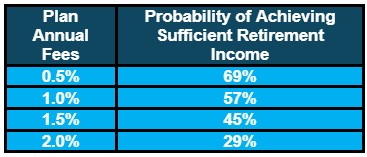

The Center for American Progress carried out simulations to see how 401(k) fee levels affect the probability of achieving sufficient retirement income. Perhaps unsurprisingly, they found that success probability and fee levels are significantly negatively correlated, i.e., the higher the fees, the lower the likelihood of success.

As shown in Table 2, the typical worker can achieve a high enough retirement income 69% of the time if their plan fees are 0.5%, but this drops precipitously to just 29% if fees are 2%.

Is All This Common Knowledge?

You would think that anything that could so massively impact your eventual nest egg size would be common knowledge.

If so, you’d be wrong!

According to the Government Accountability Office (GAO), “GAO found that 45 percent of participants are not able to use the information given in disclosures to determine the cost of their investment fee. Additionally, 41 percent of participants incorrectly believe that they do not pay any 401(k) plan fees.”

So, not only do fees make a huge difference, but more than 4 in 10 participants thought they paid no fees, and even of those who knew there were fees, 45% couldn’t figure out how to translate the fee information plans disclosed to them into practical financial results.

What You Can (and Probably Should) Do

Nobody is suggesting that you quit your job if you work for a smaller employer, just because their 401(k) plan fees are higher.

However, there are steps you should consider:

- Ask HR or your 401(k) plan administrator how much your plan charges in fees, and how much additional fees are charged by each specific fund in the plan. As they say, knowledge is power.

- Next, review your portfolio to see if the funds you picked that charge higher fees achieve better after-fee results. Research shows that, on average, the opposite is true.

- For those funds that charge you higher fees and achieve lower returns, move your money into funds with higher after-fee returns.

- If your plan is so small that it has to charge high management fees, consider contributing each year only enough to max out your employer match, if any. Whatever further amounts you can save should be invested in an IRA with good fund options and much lower fees.

- If your plan has such high fees and you leave that job, roll your 401(k) balance into a lower-cost IRA, as above.

A Counter-Intuitive Exception

Interestingly, despite the negative correlation between plan size and annual fees, the smallest plans in the country aren’t the most expensive.

Individual 401(k) plans for self-employed workers, with just one participant and likely under a $1 million balance, can be among the cheapest.

That’s been my personal experience.

As I alluded to above, I invested heavily in my 401(k) plan for over 15 years. And that plan had exactly one participant – me. As a result, the plan balance has always been very small compared to plans run for employers with multiple employees.

However, my individual 401(k) plan doesn’t charge any management fees, beyond those charged by the mutual funds and/or Exchange Traded Funds (ETFs) in which I invest my plan balance.

There is a $20 service fee per account, but that fee is waived for an individual with a combined balance of at least $50k, which I surpassed many years ago.

This is possible because with just one participant – me, and with me also acting as the plan administrator (minimal effort required), there’s nearly no administrative overhead, and I can pick very low-cost ETFs and relatively low-cost mutual funds.

My per-fund fees vary from 0.03% for index ETFs like Vanguard’s S&P 500 ETF (VOO) to 0.61% for T. Rowe Price Capital Appreciation Fund – I Class (TRAIX). As a result, I end up paying an average fee of just 0.10%!

If you own a solo business, an individual 401(k) can make it much easier to build a nest egg than most employers’ 401(k) plans, even ones that charge relatively low fees.

The Pros Weigh In

I asked professional financial advisors three questions. Here’s what they had to say.

How much do fees really impact retirement outcomes over decades?

Jakhongir “King” Mirtalipov, Founder and Principal Advisor, Dream Life Wealth Management, says, “Considering fees is essential when it comes to employer retirement accounts like 401(k). Administrative fees associated with offering 401(k) plans have come down significantly over the last few years due to high competition, but those fees still could be thousands of dollars per year. For companies with fewer than 100 employees, those fees could be a significant expense annually. One of the ways companies ‘share’ those fees with employees is by ‘offering’ high-cost (high expense ratio) investments (active mutual funds and ETFs) in their 401(k) plans.”

Lucas Fender, CRPS®, Chartered Retirement Plans Specialist at Proper Planning & Wealth Management, agrees, “Fees in the absence of value can be extremely costly when compounded over many years. Some plans offer in-person meetings with experienced, credentialed advisors. Other plans have an unlicensed person come by the office once or twice a year to click through a premade slideshow.”

Dr. Steven Crane, Founder of Financial Legacy Builders, also agrees and expands, “Many people underestimate how much fees matter over time because they look small on paper. If someone sees a 1% fee versus a 0.10% fee, it doesn’t sound like a big deal. But when you stretch that difference over 20 or 30 years of compounding, it can quietly eat away a huge portion of someone’s retirement savings. For middle-class workers, especially, every dollar matters. Losing a big chunk of growth to unnecessary fees can mean the difference between retiring comfortably and constantly worrying about running out of money.”

What should workers look for when evaluating investment options inside their 401(k)?

Mirtalipov again, “If a retirement plan offers ETFs or index funds, I always recommend considering those investments first, as they typically have very low internal costs (expense ratios). Another option, in the absence of low-cost ETFs or index funds, would be to choose a retirement target-date fund.”

Fender says, “Workers should look for a variety of investment options available within their retirement plan, including low-cost passive funds, a stable value option, and perhaps actively managed funds or a self-directed brokerage account (SDBA). Workers should also look for low-cost, highly rated target date funds (TDFs) within their retirement plans.”

Crane advises, “The first thing I usually tell workers is to keep it simple. Look at the expense ratios of the funds. In many plans, low-cost index fund options sit right next to much more expensive actively managed funds. The expensive ones are often marketed as being more sophisticated, but that doesn’t mean they perform better. In many cases, the simpler, lower-cost options end up doing just fine over long periods. Another thing people should pay attention to is how diversified their options are and whether the funds actually match their time horizon. A 30-year-old should not invest the same way as someone who’s 60. But unfortunately, many workers either pick a few funds at random or leave their money in whatever the default option was when they enrolled.”

What can workers do to minimize the impact of fees on their 401(k) balances?

Mirtalipov suggests, “Investment growth takes time and patience. Minimizing frequent changes in the account can help with lowering expenses, as many 401(k) plans charge extra if you make frequent changes in your account. Maximizing contributions and at least receiving the full match from the employer helps offset the cost. You can also roll your 401(k) to your IRA at the age of 59.5 if you’re still employed (the process is called an in-service rollover). Rolling over to your IRA is not a taxable event, and so there are no taxes to be paid (if done correctly). By rolling into a self-directed IRA, you can decrease or eliminate fees associated with employer retirement plans. For example, Schwab doesn’t charge any commissions when you buy the majority of ETFs or individual stocks through their platform.”

Fender offers this advice, “Workers may minimize the impact of fees in their 401(k) balances by choosing lower-cost investments within the plan. Another option is to utilize a self-directed brokerage account to access even lower-cost investments. In some cases, they may want to speak with their benefits department about choosing different investment options or even 401(k) providers.” This last assumes the employer is open to such changes.

Crane’s mostly agrees and adds, “If someone wants to minimize the impact of fees, the biggest lever they have is to choose lower-cost investments when available. Index funds and target-date funds with reasonable expense ratios are often good starting points. If the plan options are limited or unusually expensive, another strategy is to contribute enough to capture the employer match, then invest additional savings in an IRA, where you usually have far more choices and lower-cost options. At the end of the day, a 401(k) is still one of the best tools workers have for building retirement savings, especially if there’s an employer match involved. But it’s worth taking a little time to understand what’s happening under the hood, because small fees that seem harmless today can quietly add up to a very large number over a working lifetime.”

One advisor offered a completely different viewpoint.

Ben Simerly, CFP®, Financial Advisor and Founder, Lakehouse Family Wealth, says this, “Not all employer retirement plans are built alike. In fact, at a high level, last I checked, there were about 27 different types of employer retirement plans, and thousands of permutations. So, the first thing I coach any client on as they job hunt is how to ask for retirement plan and benefits documents from a prospective employer.

“The first thing we all look at is costs, right? And it’s a reasonable starting point for a 401(k). 1% really adds up. But the real cost/benefit is in what you get for it. So, I advise clients to look at plans with me with three ideas in mind:

- “The available investments. Always zoom back out from fees and take a look at the broader plan. The reality is that most plans pick investments based on the likelihood of a lawsuit, not performance or quality. The two are different goals. For example, between some common 401(k) funds with comparable risk and class, there is as much as a 6-8% difference in average annual growth rate over 10 years. I’ll happily pay 1% more for that much more growth.

- “The features in the plan. Better contribution matching, better investments, better Roth and In-Plan rollover options, in-service distributions, and Mega-Back-Door-Roth-IRA options are all potentially worth more than a decrease in cost. The keyword being ‘potentially.’

- “Talk to decision makers. More often than not, these folks have too much on their plate. If you’re willing to do the digging, they may let you help them make a change. I’ve worked with owners of many small and mid-size companies who were happy to make a change if someone was willing to do the legwork for them. Always compare benefits and then maximize them accordingly.”

The Bottom Line

In investing, we often obsess over market returns.

But for many workers, one of the most important determinants of retirement success may be far simpler: how much their 401(k) quietly charges them every year.

High-fee 401(k) plans can dramatically reduce your ending balance and, through that, delay your retirement date and/or reduce your retirement income.

This can be one of many considerations regarding where you choose to work, but even if your other considerations have you pick a small employer, you can minimize the impact on your retirement plans’ total balance by educating yourself about fees and their impacts, checking what each fund in your plan(s) has returned net of fees over the long term, and choosing how much you invest in your 401(k) vs. your IRA.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor