What this article covers

Financial advisors share the moves that actually help new parents reduce stress, protect their family, and build stability during one of life’s most financially and emotionally demanding transitions.

When my then-wife and I brought our first child home from the hospital, both our moms were there to help us settle in.

Then, when evening came, they left.

We looked at each other with matching “deer in headlights” expressions, realizing it was all up to us now.

And as prepared as we thought we were, having a baby bedroom with a crib and a diaper-changing table/dresser, a stroller, a car seat, diapers, 0-3-month-old baby clothes, and so much more, this was the point when it dawned on us that all that wasn’t even “table stakes.”

Because buying all that baby stuff, as crucial as it was, wasn’t the real challenge.

The real challenge was facing all the ways our life changed in that moment.

Before diving in to all that, and how you can navigate those changes, I’d like to make it clear that with all the challenges, if I had it to do over, I’d never give up having kids.

Key Takeaways

The Biggest Financial Risks After a Baby Aren’t the Ones New Parents Expect

Diapers and daycare get all the attention, but the largest financial impacts are often the ones nobody warns you about: needing a larger home, losing one parent’s income, and the career setbacks that follow. Income drops right when expenses spike, and the margin for financial error shrinks dramatically — often to zero.

The First Year Is About Stability, Not Optimization

Financial advisors consistently push back against the pressure to immediately max out 529 plans and optimize every account while running on three hours of sleep. The moves that help most — automating finances, expanding your emergency fund, updating insurance, and handling estate documents — are about reducing fragility and creating breathing room, not squeezing out returns.

Estate Planning and Insurance Coverage Can’t Wait — Even If Everything Else Can

A will, guardian designation, beneficiary updates, and adequate life and disability insurance coverage matter from day one of parenthood — not someday. These documents protect the surviving parent, any future guardian, and your child if the unthinkable happens, and they’re the items most likely to be permanently delayed if not handled early.

Why Bringing a Baby Home Can Feel So Destabilizing

Before you become parents, you had more of a margin when life threw you a curveball. A stressful month at work, an unexpected car repair, or a sudden schedule change could all be annoying, but manageable.

With a baby at home, even relatively small disruptions are harder to deal with.

And even if nothing unexpected happens, your life changes dramatically, as Gottman Institute research reveals.

- No more spontaneous socializing with longtime friends. Indeed, you often find yourself drifting away from friends who have no children.

- Travel is far more complicated.

- Uninterrupted sleep is a distant memory, with all the implications of dealing with life, and each other. Sleep deprivation leads to seemingly constant exhaustion, which turns small irritations into major blowups, and significant decisions into major issues waiting to strike.

- Conversations with your partner shift from shared interests, visions, plans, and goals to everyday logistics.

- Date nights, intimacy, and emotional support often need to be scheduled for after the baby’s asleep.

- Your identity shifts, with many new moms absorbed by caretaking and bonding with the baby, sometimes leaving new dads emotionally adrift.

- Financial margins of error get much thinner, or disappear altogether.

It’s no wonder that financial advisors often say that having a child is one of the biggest life changes. That’s why many new parents seek financial guidance. Because parenthood makes life more complicated and challenging, both financially and emotionally.

As Reggie Fairchild, MBA, CFP®, President, Flip Flops & Pearls, puts it, “Having kids is one of the greatest things you’ll ever do. It will also change literally everything: how you sleep, how you spend your time, how you spend your money, and even what qualifies as date night.”

Dr. Steven Crane, Founder of Financial Legacy Builders, expands, “Having a baby exposes how fragile most people’s financial lives actually are. Everyone talks about diapers, daycare, and college savings, but almost nobody talks about the emotional hit. You’re exhausted, your relationship changes overnight, your routines disappear, and suddenly even basic decisions feel harder.

“Honestly, I think a lot of new parents need less financial optimization and more permission to slow down. The financial industry pushes people to immediately start maxing out 529 plans, buying all the insurance products, and building the ‘perfect’ setup while they’re running on three hours of sleep.”

Many new parents assume their biggest financial challenge will be the direct costs, like baby gear, clothes, diapers, formula, and daycare.

Those costs are all real, but some of the biggest financial impacts are ones you may not have considered.

- Needing a larger home is estimated to drive 30% or more of child-raising costs.

- Losing the income of one parent, in our culture, usually the mom’s.

- The stay-at-home parent’s loss of career advances, raises, and even prospects.

Unsurprisingly, research by a University of California, Berkeley scholar found that many households suffer a significant decline in economic wellbeing around the birth of a child. This is because income drops right when expenses run higher.

The Life Changes New Parents Are Least Prepared For

Your child-free friends are probably still traveling to fun destinations, making spontaneous plans for a night out, staying out late, and taking a quick weekend getaway to recover from an especially stressful week.

With your new baby, you’re stuck coordinating naps, feedings, childcare, pediatric appointments, and have I mentioned exhaustion?

Even when longtime friendships remain strong, the vast difference in your lives makes it hard to stay connected. The resulting sense of isolation, especially for the stay-at-home parent whose career suddenly became secondary to caregiving responsibilities, can take you by surprise.

Before becoming a parent, you had a sense of identity that probably centered on your career, friendships, travel, and relative independence. Now, your identity shifted, to being a mom or a dad.

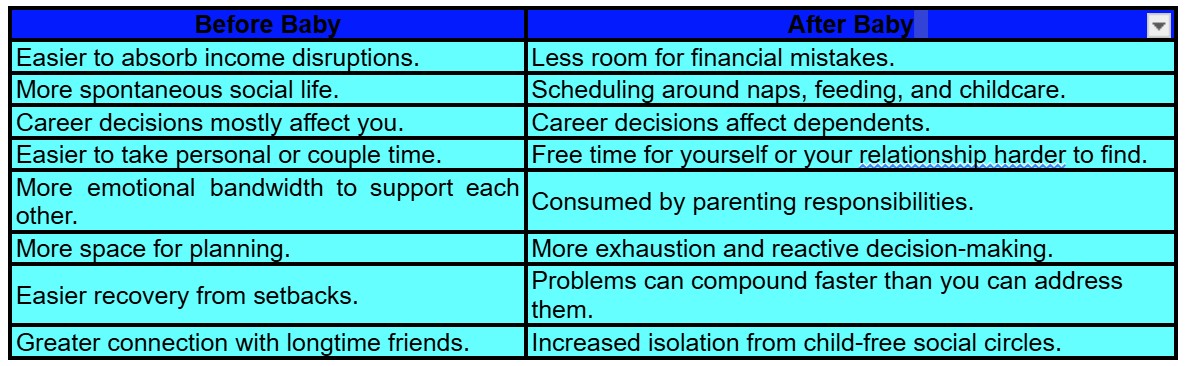

Table 1 summarizes some of the biggest shifts.

The stress is rarely just about finance and numbers. It’s usually tied to exhaustion, uncertainty, unpredictability, changing priorities, and the pressure of trying to hold it all together despite everything.

Why Sleep Deprivation Makes Financial Decisions Harder — Right When the Stakes Are Higher

Before you became parents, your decisions affected just the two of you.

As parents, you’re suddenly responsible for the wellbeing of a helpless infant who’s completely dependent on your making the best decisions possible.

But all the things that support good decision-making come under pressure.

Certain expenses, e.g., healthcare, become less predictable, increasing financial and emotional stress.

Sleep deprivation makes you exhausted, cognitively less capable, and emotionally less stable. The relentless emotional and logistical burden of coordinating daily life makes it hard to take a step back and achieve a broader view. All this makes good decisions harder to reach and implement.

Your childcare arrangements, intended to give you some breathing room, can fall apart with little warning.

The stay-at-home partner may feel resentful, which can make collaborative decisions harder to achieve. This is only made worse if the two of you have different notions on the best ways to parent your child.

The higher stakes of each financial decision make it harder to consider options in a cool, calm, and collected manner.

All this can make even the most financially responsible adults feel off kilter.

Cole Williams, Founder of Vessel Financial Planning, says, “Most new parents expect the money stuff to be hard. What catches them off guard is how much the exhaustion affects their financial decision-making. Judgment gets worse precisely when the stakes get higher, which can affect relationships between partners, family, friends – even colleagues at work or strangers in the grocery store checkout line.”

Your best path forward in this situation isn’t so much about optimizing everything. Instead, reduce your financial fragility and simplify your financial life, which can create the emotional breathing room to handle any emotional, relational, and financial struggles you may face.

Why Many New Parents Delay Important Financial Decisions

It’s understandable.

Important financial decisions get delayed, because new parents are overwhelmed and constantly required to make important and urgent decisions regarding their new day-to-day reality.

When you’re dealing with urgent things like figuring out if baby’s crying because she’s hungry, or colicky, or needs her diaper changed; scheduling your next pediatrician appointment; and even arranging a babysitter so you can have a short breather to remember what it’s like to be a couple, getting to important decisions that simply don’t feel urgent is a challenge.

It’s hard to balance the urgent day-to-day stuff with the important but less-urgent-feeling decisions, such as:

- Starting, or expanding your life insurance coverage.

- Setting up disability insurance.

- Creating and signing a will.

- Reviewing beneficiaries.

- Adjusting your budget including childcare costs.

- Reevaluating career plans, especially for the stay-at-home parent.

- Figuring out how you’re supposed to continue saving for the future when your present seems to “suck all the oxygen” out of your budget.

And you’re supposed to do all this while adapting to your dramatically different life and its challenges.

This combination often leads to decision overload and emotional paralysis.

Fairchild says, “New parents expect the stroller and the diapers. They don’t expect decision fatigue. When you’re running on four hours of sleep, even small financial choices feel enormous.”

Instead of making intentional financial decisions, you may find yourself only able to focus on putting out the (metaphoric) fire that’s right in front of you.

Because when life already feels overwhelming, financial and legal complexity adds even more stress, which makes it harder to make proactive moves.

That’s why the best moves after having a baby are often less about maximizing returns and optimizing allocations, and more about reducing pressure, enhancing flexibility, simplifying decisions, creating breathing room, and making life feel more manageable.

That’s what helps young families successfully traverse one of the biggest transitions of adult life.

The Financial Moves That Help New Parents Most in Year One

The most important thing you can do as new parents is to create for yourselves the emotional and cognitive space to prioritize making important decisions, even when they don’t feel urgent.

You need to identify:

- Which financial decisions matter most right now?

- Which risks are most dangerous?

- Which tasks can safely wait until you can deal with them?

Once you accomplish that, you will feel the relief of knowing that you’re handling the most important and urgent stuff, and that what you’re deferring won’t come back to bite you, at least for a while.

The things that will help you most aren’t necessarily flashy. They just create emotional and financial breathing room, reduce the feeling of chaos, and help make your household more resilient in the face of your unpredictable life.

Fairchild cautions, however, “Even the best systems need revision. Kids will teach you fast that what worked last week might not work this week. Grant yourself some grace and give yourself permission to adjust as you go.”

Simplify Your Financial Systems

New parents often try to keep things as close as possible to how they were pre-children. However, the level of complexity you can handle as a new parent is vastly less than what you were able to manage before.

Optimizing everything to the nth degree is feasible when you’re not constantly exhausted. But that’s not where you are now.

That level of complexity becomes unsustainable in your new life.

The more you simplify your life, the less stressed you’ll feel, and the better you’ll be able to handle the remaining tasks.

- Automate bill payments.

- Consider consolidating accounts.

- Simplify your budget by batching related expenses into fewer line items.

- Cancel unused subscriptions to reduce expenses and the effort to keep track.

- Devise simplified decision rules so you can make each decision once, until something changes.

Every decision you need to make and every action you need to take carries a cognitive cost.

When you’re exhausted, even minor matters contribute to your overwhelm.

Williams advises, “The single most effective thing new parents can do is to automate as much as possible before baby arrives. The goal is to reduce the number of active decisions required of you while you’re running on fumes.”

He then warns that one of the easiest traps for new parents is “death by a thousand small purchases. A DoorDash order here, a subscription service there. Each one feels totally justified when you’re sleep-deprived, but they pile up quickly and are largely invisible until you go to pay the credit card bill.”

The more you simplify and streamline your financial life, the less stress you’ll experience, and the easier it’ll be to get through periods of emotional distress.

Fairchild agrees, “The parents who navigate most easily are the ones who set up systems before the baby arrives: automated savings, auto-pay, and a commitment to paying themselves first by automatically investing in their family’s future every single paycheck, so they’re not making important money decisions while exhausted.”

How Much Emergency Fund Do New Parents Actually Need?

You may not have taken into account the four main factors that drive the size emergency fund you need.

Baseline expenses are higher.

Spending uncertainty is greater.

With one parent staying at home, income stability is lower.

With a young child in the mix, the consequences of financial issues are worse.

If your emergency fund held three months’ worth of your child-free expenses before, it’s worth less than three months’ expenses now, and you should really bump it up to 6, 9, or even 12 months.

This can’t be done overnight, but you need to start the ball rolling on it sooner than later.

Ultimately, your emergency fund offers far more than the financial resources needed to survive unexpected adversity.

It offers emotional breathing room at a time when life feels far less predictable.

Update Insurance Coverage ASAP

Before children, and especially if you both earned decent money, life insurance was important, but it was mostly about getting good term coverage at low prices because you’re young and healthy, and it didn’t feel very urgent.

Similarly, disability insurance is a relatively inexpensive way of ensuring that you can keep paying your bills if your ability to earn is temporarily paused.

But once you have kids, and especially if only one of you is working, both life and disability insurance coverages are critical and urgent.

Just imagine if, heaven forbid, you’re hit by the proverbial bus.

How will your stay-at-home spouse and young dependent child survive financially?

It’s psychologically difficult to consider catastrophic worst-case scenarios and confront our mortality, especially when we’re younger. But once you have a child in the picture, you can’t afford to let that delay you from taking these steps urgently.

And lest we forget, your health insurance also needs to be updated, as Williams points out, “Birth of a baby is a qualifying life event for a change in health insurance. Especially with newborns, you get what you pay for in this arena. The cheapest plans may not offer your preferred pediatrician in network, which could be a make-or-break for you, so it’s worth preparing to spend at least a few hundred bucks more each month to add baby to your plan, or to upgrade your plan’s features overall.”

Why Estate Planning Can’t Wait Until After the Baby Chaos Settles

If you aren’t from a wealthy family, or at least from an upper-middle-class one, you may not have ever dealt with or seen your parents deal with estate planning.

That doesn’t mean you’re off the hook here.

You may not have a lot of wealth built up that needs to be transferred, but an estate plan and will offer stability and clarity, and should you both pass away at the same time, address guardianship for your child and provide support for the guardian(s).

Preparing these documents now is how you can support the surviving parent, the guardian, and your child or children by making clear your desires, and making it easier for financial resources to be given to the right parties, with as little red tape as possible.

Fairchild offers a brief summary, “Year one, get the basics locked in: life insurance if you don’t have it, beneficiary designations updated, an emergency fund that actually covers three to six months of the new normal. A 529 can wait a few months. The estate documents, will, guardian designation, cannot. Those matter from day one.”

Yes, these conversations and preparations are emotionally charged, which is why they often get put off for a future day that somehow never arrives, potentially until it’s too late.

Don’t let that stop you from doing what’s needed, and doing it as soon as you can.

Have a Backup Plan for Childcare Disruptions

Childcare arrangements are crucial, especially once both parents are back to work.

As Williams points out, “One of the biggest financial decisions to get clear on early is what care for the baby will look like during the workweek and healthcare for the family. If both spouses work, daycare through an independent facility may be well worth the expense, but it can still feel like taking on a second mortgage.”

Unfortunately, these arrangements are far from bulletproof.

Daycare closures, sick children, sick caregivers, school schedule changes, weather events, and changes in your work schedules can all throw a wrench into your carefully arranged routine, often with little to no warning.

And when you’re both already stretched to the limit and exhausted, even a temporary problem can feel impossible to deal with.

That’s why it isn’t enough to think about what childcare arrangements you need and how you’ll pay for them.

You need backup plans in case your arrangement suddenly falls through.

- Set up with your employer an option for remote work when needed.

- If you have trusted family or friends who can occasionally help, discuss with them in advance so you can call on them when you need their help.

- If all else fails, make sure your emergency fund will cover the income disruption caused when your childcare solution temporarily breaks down.

Nobody wants to experience such a disruption, but having a backup plan can reduce it from something that can spiral into work problems, financial strain, relationship struggle, and emotional overload into a short-term irritating matter that you’re prepared to handle.

That backup plan creates flexibility, and reduces the number of things that could go wrong at the same time.

Reevaluate Lifestyle Expectations, with Honesty

Parenting comes with enough financial stress as baseline.

Direct costs. Indirect costs like moving to a larger home to have room for the kids. Parental income reduction when one parent stays at home. Greater uncertainty.

Don’t needlessly add to that pressure by trying to meet societal expectations about what “good parenting” is supposed to look like.

Michelle R. Wagner, CFP®, Founder at Wellful Money, cautions that even financially savvy parents can make rushed decisions during the transition to parenthood. “As a financial planner and mom, I’ve made mistakes personally and I’ve seen clients make mistakes. I’ve rushed into buying a nice new SUV and found out after the fact that it won’t work with more than one car seat plus taller adults. I’ve seen families buy a new house but later want a different location for the family-friendly neighborhood, parks, schools, proximity to childcare, etc. For larger purchases like cars and houses, leasing or renting can be helpful so you can see how it truly works with your new lifestyle before fully committing.”

Sure, you need diapers and other baby products, but you don’t have to buy the most expensive brand-name versions.

Do you really need luxury-level clothes that your kid will grow out of in a few months?

As Williams quips, “Your baby won’t care how much you spend on the nursery, on clothes, swings, pack-n-plays, or bassinets. Secondhand items are a strong play here.”

A larger home is often needed, but don’t buy more home than you actually need now and in the coming few years.

Arranging educational and extra-curricular experiences is important to raising a well-rounded human being. But don’t let anyone pressure you into sinking more money than you can sustainably afford just to “keep up” with your friends and neighbors and maintain appearances.

Many families unintentionally inflate the cost of raising children through their choices, trying to maintain high-consumption lifestyles and meet peer expectations.

Raising children isn’t an inexpensive proposition, but don’t make it more expensive than what it takes to meet your desires and means.

Wagner agrees that parents shouldn’t try to do it all in the first year, “The first year is all about survival. Don’t worry about maxing out 529s or 401(k) plans until you have an extra comfortable emergency fund, backup plans for childcare, and a plan if one parent doesn’t return to work or decides to work for themselves for extra flexibility.”

Still, Williams offers important advice regarding opening a 529 plan, “A lot of new parents think the time to start funding a 529 education savings plan is as soon as the baby is born. Opening a 529 plan sponsored in your home state takes just a few minutes and can give friends and family a place to help you save for your kid, but funding with your own money can wait until you’ve gotten your bearings with the newborn and infant stages.”

Crane also feels strongly about the importance of simplifying, taking a beat before rushing to do everything, and accepting and adapting to the new reality. “In reality, the first year is more about creating stability than maximizing efficiency. Simplify your life, lower unnecessary expenses, build breathing room, and stop trying to keep up appearances. The biggest mistake I see is people refusing to accept that becoming a parent fundamentally changes their priorities and capacity. They keep spending like they did before kids, working like they did before kids, and expecting the same energy level.”

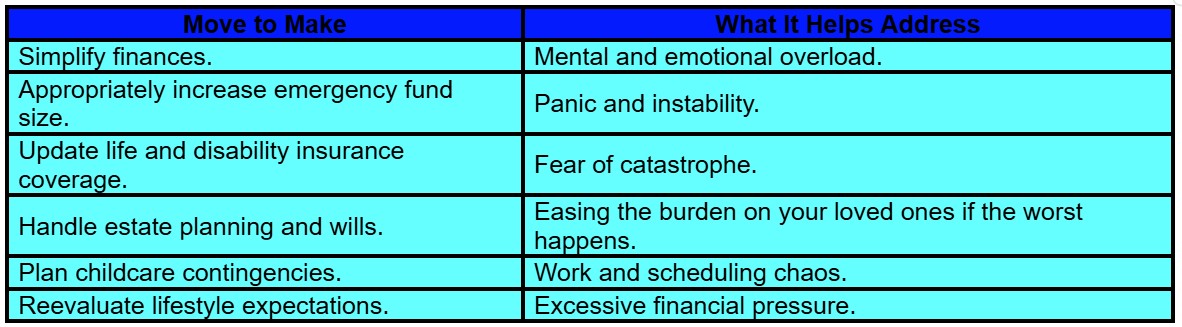

Table 2 summarizes the above moves and how they help.

The Bottom Line: New Parents Don’t Need Financial Perfection — They Need Financial Resilience

Your goal isn’t, and shouldn’t be, to achieve financial perfection.

Nobody adapts to parenthood perfectly, and even what they get right doesn’t happen all at once.

Not emotionally.

Not relationally.

Not financially.

Stress and exhaustion are a normal, expected part of being new parents. So is relational tension. Feeling emotionally and financially overwhelmed and disoriented doesn’t mean you’re failing.

You can’t completely eliminate uncertainty, so don’t even try.

Your goal is to reduce the number of things that can go wrong at once, make each less likely to happen, and come up with ways to mitigate the risks and the consequences of when they turn into reality.

That’s why your best bet after having a baby is to make the changes that reduce your fragility, increase your flexibility and resilience, simplify your decisions, and increase your emotional breathing room.

For many families, this is where outside guidance becomes especially valuable. You haven’t suddenly become less financially savvy, but your emotional and mental bandwidth and your capacity for making calm decisions are all stretched to the max.

A good financial advisor can help you step back from survival mode long enough to prioritize the important things, streamline and simplify decisions that need to be made, and reduce the risk that temporary stress will cause long-term damage.

Crane says, “I think the reason so many families spiral financially after having kids isn’t because they’re irresponsible, it’s because they’re overwhelmed and trying to survive while still pretending life is operating normally. The families who tend to do best are the ones willing to adjust expectations early and build a life that actually matches the reality they’re living in.”

Achieving these things is what separates families who adapt best to their new life from those who struggle through it.

Williams wraps things up nicely, “The key is not to somehow make every right decision. You won’t. No one does. Just avoid making permanent decisions in the middle of the most beautifully chaotic stage of your life.”

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher