If you live in Maryland, you’re already paying some of the highest taxes in the country, but chances are, you’re paying even more than you have to. Most residents only think about taxes when it’s already too late to do anything about them: at filing time, when the decisions are already made and the opportunities are gone. The good news? With the right deductions, credits, and a little proactive planning throughout the year, you could keep thousands more of your hard-earned dollars. Here are 10 strategies to legally reduce your Maryland state and local income taxes, and why starting now matters more than you think.

I’ve been a Marylander for almost 30 years. Although I’ve lived on three continents (four, if you count a couple of months in Antarctica), in three countries, and in two US states, I’ve lived here longer than anywhere else.

There’s a lot to love about Maryland. Just look at the photo below, taken not far from my home, and you’ll start to see why:

However, the tax burden isn’t one of the things I love about my home state.

According to the Tax Foundation, Maryland has the 11th-highest per-capita tax burden in the country, about 13% above the U.S. average (based on 2022 data).

As Ben Simerly, CFP®, Financial Advisor and Founder of Lakehouse Family Wealth and former Marylander, says, “Maryland has literally become famous for unique and destructive taxes. To my knowledge, it’s the first state or territory, or in some cases one of the few, to tax the rain, provide more than a dozen forms of property taxes, and even tax money at the state level both at the time of death and inheritance.

“For some, living in Maryland isn’t optional. Many federal workers and military personnel and their families are required to live and work in the region. If this is you, make the best of the situation. You may not get hazard pay like you would in earlier days of government service in the region, but with some help from pros, you can lessen the ill effects on your finances.

“Here are our top areas of tax concern in Maryland. First, Maryland has its own particularly vindictive capital gains tax, despite gains already being taxed under several other state and federal codes.

“It applies an extra 2% capital gains tax mainly on households with federal Adjusted Gross Income (AGI) above $350,000. Even if your household doesn’t normally make over $350,000, your AGI could get ‘bumped’ over $350k due to, e.g., receiving a large bonus; selling a house that appreciated too much; moving financial assets between account types that causes a taxable event; owning shares in mutual funds that distribute significant capital gains, dividends, and interest; etc. These can all trigger a ‘capital gains’ trap, which happens far more easily than you might think.

“Second is additional death and estate taxes. Maryland levies a 10% tax on inheritance to the beneficiary, even if the money was taxed at the benefactor’s death. That’s right, it taxes the money yet again. And that’s after the also unique state inheritance tax of between 8% and 16% on estates with a gross value of $5 million.

“There are look-back clauses too, meaning you can’t simply move to avoid the tax; you have to move long enough before death or inheritance to avoid the tax. States like Maryland, New York, and California will follow you around the world to collect taxes from you and take you to court or send agents if it goes that far.

“My retirement planning work with Maryland clients over the years shows that most could retire 10 years sooner and have dramatically higher retirement income outside of Maryland, largely due to the benefits of rollovers occurring outside of the state.

“So, for Maryland residents, we often plan out income for even young families the way you normally only would for someone approaching Medicare age or already retired. We do everything we can to keep income under certain thresholds and then get the resident out of Maryland as soon as humanly possible.”

If I had to, I’d bet a nickel (assuming I can still find one in these digital times) that many Marylanders overpay their taxes. Not because they’re careless, but because they start thinking about it too late.

If you’re a higher-income Maryland resident, that can mean paying several thousand dollars in higher taxes per year than you’re legally required to. And once that money is gone, you don’t get it back.

By the time you’re filing your tax return, your tax liability is already set. At that point, your income is already set, your deductions and credits have already been earned (or not), and most opportunities to reduce your tax bill are behind you.

At that point, it’s mostly a question of how well you (or your tax software) identify the deductions and credits you’re eligible for.

That’s why if you want to reduce your Maryland taxes, filing better is a secondary priority. Your top priority should be to focus on better tax planning and strategy.

Three Types of Tax-Reducing Moves for Maryland Residents

There are only three legal ways to pay lower income tax.

- Lower your taxable income, ideally without reducing your standard of living (e.g., by using more and larger deductions).

- Take advantage of all tax credits for which you qualify.

- Make smarter timing and structural decisions.

Many taxpayers focus on the first, but still miss some opportunities, take partial advantage of the second, and almost entirely miss the third.

That’s why, even if they do everything perfectly at tax-filing time, they end up paying more than they could have.

The following are 10 tips for reducing your Maryland state and local income taxes. Some are straightforward. Others require a bit of planning. Most are easier to implement before the tax year is over.

You don’t have to use all 10, but the more you miss, the more of your hard-earned money you’ll leave on the table.

Lower Your Taxable Income

If you ask most people, this is what they’ll identify as a good way to reduce their taxes.

It’s natural. It’s the most straightforward way to reduce taxes.

But there’s a catch.

There’s using this lever, and then there’s USING it.

The former means contributing whatever you feel you can to your traditional retirement plans, using the standard deduction, and letting things flow as they will over the years.

This leaves lots of opportunities on the table, unused.

The latter requires being more proactive and committed.

Here are the top three examples.

1. Maximize Pre-Tax Retirement Contributions

If you can’t afford to maximize your retirement contributions without counting on the tax deduction, and especially if you’re already in a high tax bracket, this may be your best bet.

Not only does it reduce your federal taxable income, but it also reduces your taxable income for Maryland state and local taxes.

Table 1 shows some examples of how much you can lower your 2026 income taxes (federal, state, and local) by contributing an extra $10k to your traditional 401(k) account if you file “married filing jointly” and live in, e.g., Howard County, Maryland.

Clearly, the majority of the tax savings come from the federal portion, but the state and local tax reduction can go as high as $980, or 0.98% (for residents of Dorchester County with a Maryland taxable income above $1.2 million).

If you’re one of those who don’t max their retirement contributions, this is the simplest and most powerful place to start, but only if you make the contributions before the end of the tax year!

And unlike many strategies, this one is (almost) entirely within your control.

2. Use Maryland’s 529 Deduction as Much as Possible

Maryland has a relatively generous deduction for people who set aside money for their dependents’ (or their own) education.

You can deduct contributions to Maryland 529 plans, up to $2500 per contributor, per beneficiary, per year.

That means that, if you’re married and have two kids, you could potentially deduct up to $20k a year ($5k from you and your spouse per beneficiary, for each of your kids, plus for the two of you).

What’s more, you can carry over excess contributions for up to 10 years.

That means that if you, e.g., open a plan for your child when she’s born, and contribute $5k a year from you and your spouse until your daughter goes to college, then contribute $20k in her freshman year and another $50k during her senior year, all of those contributions can ultimately be deducted.

That’s $160k-worth of deductible contributions spread over 32 years.

Even if you can’t afford to set aside money until your kid goes to college, but you do pay $70k in tuition and other eligible educational expenses during his college career, you can deduct those over the four years of college, plus the following decade.

And the most incredible thing about this deduction, in my opinion, is that you can contribute to the plan, then take the money out the very next day to pay the tuition bill, and it’s still deductible!

And lest we forget, if your kid doesn’t go to college or has such large scholarships that there’s a large balance left over, you can change beneficiaries, or you can use a SECURE 2.0 provision to convert up to $35k of the remaining balance into a Roth IRA for the beneficiary.

Few deductions offer this much flexibility with this much impact.

3. Don’t Blindly Use the Standard Deduction

Despite the significant increase in the federal standard deduction over the past several years, if you own a home with a large mortgage, make significant charitable donations, and perhaps have high medical expenses, itemizing can still reduce your taxable income by more than the standard deduction would.

And the larger your federal deduction, the lower your taxable income for Maryland state and local taxes.

The above three tips are the most visible lever and the one that most people focus on.

But if you stop there, you’re likely missing more powerful opportunities.

Take Full Advantage of Tax Credits

Tax deductions are great. They reduce your taxable income, which reduces your taxes.

But there’s something even better.

Tax Credits.

For every $1 of tax deductions, your Maryland state and local taxes drop by about $0.08. But for every $1 of Maryland tax credits, your Maryland state and local taxes drop by a full $1!

If deductions are about trimming around the edges, credits are where meaningful reductions often happen.

The only problem is that, while more valuable from a tax reduction perspective, credits are far more tightly targeted.

Maryland offers quite a few such tax credits. The problem is that most middle-to-high earners assume credits don’t apply to them and never take the time to verify that assumption.

Here are a few credits worth checking carefully.

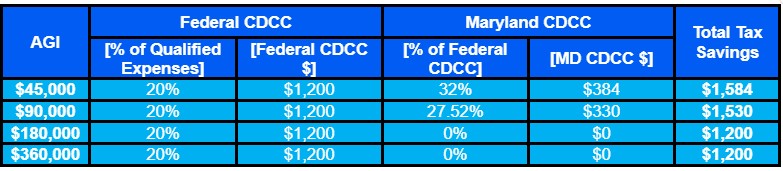

4. Child and Dependent Care Tax Credit

Even if your adjusted gross income is in the 6 figures, Maryland offers a substantial tax credit for child and dependent care expenses.

The Maryland credit amount is figured as a percentage of the federal Child and Dependent Care Credit (CDCC), which can be 20% – 32% of qualified expenses up to $3000 for a single dependent or $6000 for two or more dependents.

That percentage depends on your filing status and your federal AGI. Table 2 shows some examples for couples who file jointly, have two dependents, and paid $6k or more in qualified care expenses.

5. Senior Tax Credit

Maryland offers a tax credit for seniors, even if their federal AGI is up to $150k if married filing jointly or up to $100k if single.

The credit takes up to $1750 off your Maryland tax bill if both spouses are 65 before the end of the tax year. If it’s a single taxpayer, or a couple where only one is 65 by the end of the tax year, the senior tax credit is $1000.

6. First-Time Homebuyer Subtraction

If you and your spouse (if any) are Maryland residents, haven’t owned or purchased a home in the past seven years, and contributed money to a first-time home buyer savings account, you can subtract from your taxes the lower of $5000 or the amount you contributed in the tax year, plus earnings from the account for the tax year.

You can do this for up to 10 years.

The earnings subtracted cannot exceed $50k over the 10 years.

There are caveats.

First, by the end of 15 years from when you open the account, you must use the account balance toward a down payment and/or eligible closing costs for buying a home in Maryland. Any amount not so used counts as taxable income in the following year.

Second, amounts withdrawn from the account for purposes other than eligible first-time home buying expenses count as taxable income for the tax year of the withdrawal and are also subject to a 10% penalty. Three exceptions are rollovers, bankruptcy, and administrative costs charged by the financial institution for the savings account.

Some other possible credits to investigate include:

- Student Loan Debt Relief Tax Credit

- Maryland Earned Income Credit

- Credit for Taxes Paid to Another State

- Long-term Care Insurance Credit

- Independent Living Tax Credit

- Oyster Aquaculture Credit

- Historic Revitalization Credit

- Conservation Easements Credit, and many more.

As mentioned above, don’t simply assume that you make too much to qualify. That just increases your risk of leaving easy money on the table, paying higher taxes than you owe.

Also, you may qualify for certain income-limited credits you wouldn’t normally qualify for in years when your income is lower than usual. This could be due to, e.g.:

- Being unemployed or underemployed for part of the year (or, hopefully not, all of it).

- Living off withdrawals from a Roth account, taxable portfolio, and/or savings accounts.

- Living off untaxable proceeds from the sale of a home or other property.

There’s no doubt that tax credits can be a powerful tool in reducing your Maryland state and local income tax.

But even these aren’t necessarily your biggest tax-cutting opportunity.

That will often result from planning and making optimal timing and strategic decisions.

Strategic Decisions and Timing – Where Planning Shines

As helpful as tax deductions may be, and as powerful as tax credits are, there’s someplace else where the biggest savings often are, and where many people leave the most money on the table.

Some because they prefer not to make the changes that would reduce their state and local taxes by the largest amount, but many others just don’t make the right moves in time.

This is the only category where decisions made months or even years earlier can completely change your tax outcome.

Simerly says, “While most of the available tax credits or deductions for Maryland are automatically asked about or applied by tax software and or accountants, some areas require more advanced planning.”

7. Time Income and Deductions Proactively

You don’t want the tax tail to wag your income dog, but the progressive nature of our tax system lets you reduce your long-term total taxes by avoiding spikes in taxable income that would push you into higher tax brackets.

This is true for federal taxes, but also for Maryland state and local taxes.

For example, if you have an especially high income in a specific year, you can:

- Ask to defer at least part of your bonus (if any) to the following tax year.

- Avoid realizing capital gains that year, holding off on selling appreciated assets until the following year.

- Harvest tax losses by selling assets whose current value is lower than your basis in them.

- Bunch charitable contributions into that year from the previous and/or next year.

The crucial thing is to be intentional and make the necessary decisions proactively, when you still have the flexibility to make them.

8. Coordinate Federal and State/Local Tax Decisions Intelligently

A Roth conversion is a plausible long-term tax-reduction and estate-planning strategy.

However, it’s important to consider your short-term taxes, including your Maryland state and local income taxes.

If you’ve decided on a Roth conversion, carry it out during years when you’re in a lower tax bracket.

Similarly, if you’re retired, you may benefit from drawing more out of your tax-deferred retirement accounts in years when your taxable income is otherwise lower than typical.

9. Where You Live Matters

Your Maryland state and local income tax could vary by up to 13% simply because you live in one jurisdiction vs. another.

For example, the local income taxes in Worcester County and Talbott County are relatively low, at 2.25% and 2.40%, respectively. Local tax in Dorchester County is the highest, at 3.30%.

All other counties fall between those extremes, with Anne Arundel and Frederic Counties charging progressive taxes, per taxable income.

In this age of remote work, all other things being equal, you could shave over 1/8 of your Maryland state and local tax by moving from a high-local-tax-rate county to the lowest one.

Crucially, if for some reason the Comptroller of Maryland can’t identify your county of residence, you will be taxed at the highest local tax rate, of 3.30%. So if you live in a county that charges a lower rate, make sure you identify it correctly on your state tax return.

10. Treat Tax Planning as a Year-Round Process

Most people only think about how they can reduce their taxes when it’s mostly too late.

At tax filing.

By then, your income is already earned, your decisions are already implemented, and your tax-reduction opportunities are mostly gone.

If you want to minimize your state and local taxes, you need to do more than file better. You need to plan, decide, and execute earlier.

This means you need to:

- Review your situation before year-end (preferably far before that point).

- Identify opportunities.

- Make adjustments while they can still affect your taxes.

Dr. Steven Crane, Founder of Financial Legacy Builders, shares, “In my experience, the biggest state tax wins usually come from decisions around income timing and where income shows up. Maryland has relatively high state and local taxes, so things like Roth conversions, retirement withdrawals, and even where assets are held can make a noticeable difference. I’ve worked with clients who didn’t realize that simply shifting how and when they recognize income could save them thousands over time.

“One of the biggest mistakes I see is people treating state taxes as an afterthought. They focus on federal planning but ignore how state and local taxes stack on top of that. Another common issue is not coordinating decisions; someone might take a large distribution, sell assets, or exercise stock options without realizing the full state tax impact until it’s too late.”

The Bottom Line for Maryland Residents

If you’re a Maryland resident, especially one paying relatively high state and local income taxes, your biggest-impact tax-reduction strategy isn’t to find a single large tax break you somehow missed all these years.

It’s to identify and take advantage of all the deductions you’re legally allowed to take, claim all the tax credits you’re eligible for, and most crucially, make proactive choices before the end of the tax year, when they can still reduce your taxes.

The goal isn’t to find one big tax break. It’s to avoid small inefficiencies that add up over time.

Crane agrees, “The biggest thing I wish people understood is that tax planning isn’t something you do in April. By then, most of the decisions are already locked in. The real opportunities happen during the year, when you still have flexibility to control income, deductions, and timing. At the end of the day, reducing state taxes isn’t about finding one big trick. It’s about being intentional with how your financial life is structured and making small decisions that add up over time.”

You may already be implementing some of the above tips.

But it’s a good bet that you’re missing one or more and overpaying your taxes, year after year, as a result.

To reduce your Maryland state and local taxes as much as legally possible, identify the tips you’re missing and implement them as soon as possible.

The earlier you start, the more options you’ll have.

And the more options you identify and take advantage of, the more control you’ll have over how much of your money you’ll get to keep.

If you consider yourself financially disciplined, this is one area where that discipline can pay off directly. Because when it comes to taxes, the difference between ‘good enough’ and ‘well planned’ can mean thousands of dollars a year back in your pocket.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher