California’s top state income tax rate of 13.3% doesn’t discriminate — it applies to wages, bonuses, investment gains, and business sale proceeds alike. But while every high earner in California faces the same tax code, not all of them pay the same amount. The ones who keep more aren’t doing anything illegal, and they don’t have access to secret strategies unavailable to others. What they do have is a deliberate, multi-year approach built around three core levers: controlling when income is recognized, structuring investments for state-level tax efficiency, and making coordinated financial decisions with long-term tax consequences in mind. Here’s how it works and why waiting until tax season to think about any of this is one of the most expensive habits a high earner in California can have.

California taxes are high. In fact, according to the Tax Foundation, Fiscal Year 2022 data show they’re second only to New York. Overall, California tax collections per capita were about $10,319, compared to a US average of $7,109.

But if you’re a high earner there, doubtless you already know this.

You may be less aware that even within the same tax system, people earning similar amounts can pay different amounts of taxes. Some even make more than others while paying less in state taxes, sometimes significantly so.

This isn’t about tax evasion, which is illegal, nor do these people try to avoid California taxes altogether, which is next to impossible for California residents. Instead, they focus on optimizing when and where income shows up, and on how different financial decisions interact and affect outcomes.

Implementing these strategies won’t let you eliminate your taxes, but it can make a big difference in how much you get to keep over a lifetime.

Key Takeaways

California taxes long-term capital gains the same as ordinary income — making federal tax strategies unreliable at the state level.

Unlike the federal tax code, California offers no preferential rate for long-term capital gains, which means strategies specifically designed to minimize federal taxes can fall flat — or even backfire — for California residents. High earners need a California-specific tax framework, not a one-size-fits-all approach borrowed from federal planning.

Stacking income events in a single tax year is one of the most expensive mistakes high earners in California make.

Bonuses, stock option exercises, RSU sales, and business sale proceeds hitting in the same calendar year can push high earners into California’s steepest marginal tax brackets — a self-inflicted tax problem that proactive income timing can often prevent. Spreading these events across multiple years, when feasible, can meaningfully reduce the effective rate paid on that income.

The highest-impact California tax strategies — including direct indexing, municipal bonds, and multi-year deferral planning — require ongoing coordination, not a once-a-year tax filing mindset.

Tools like direct indexing (which harvests losses even in up markets), California municipal bonds (exempt from both federal and state taxes), and long-term deferral vehicles such as cash balance plans and deferred compensation can dramatically reduce lifetime tax drag — but only when implemented consistently and coordinated across your financial advisor and CPA well before year-end.

Why California Tax Strategies Are Different and Why That Matters for High Earners

Not only are California taxes higher than almost any other state’s, but they’re also broader than most. For example, there are no preferential tax rates for long-term capital gains (LTCG).

When

- marginal rates are high,

- income is broadly taxed, and

- there’s limited preferential treatment,

many common tax-reduction strategies stop working. In fact, some can even backfire. This is why the gap between managing and optimizing taxes vs. just paying them tends to be wider in California than in most other states.

The Most Common California Tax Mistakes High Earners Make

So, if it isn’t about tax evasion, generic tax tips, or access to some secret tools, how do certain high earners optimize their taxes better than others?

First, most high earners don’t ignore taxes, but they do tend to focus mostly on maximizing their earnings. They evaluate compensation, bonuses, and business-sale windfalls based on how large they are.

They think of taxes, but often as a secondary consideration.

In California, as in other high-tax states, income timing can be crucial. Having multiple one-time income spikes in a single year can push you into higher tax brackets.

That makes your taxes more expensive.

Second, many assume that the same strategies they use to optimize federal taxes work equally well for state taxes.

In California, some, but not all, do.

Here’s one example that doesn’t.

If you’re a high earner, concentrating long-term capital gains in a taxable portfolio lets you pay significantly lower federal income tax on them than placing them in a tax-deferred account, such as a traditional IRA.

California, however, taxes long-term capital gains the same as wage income, so strategies built around long-term holding periods for federal purposes don’t carry the same state-level benefit.

Third, people only think about taxes when it’s time to file, when it’s already too late to do much optimizing. Or, at best, they think about them one year at a time.

That’s understandable, since that’s how we report our income and pay our taxes.

But this is far less powerful than multi-year tax planning. If you have an especially high income in a single year, you’ll get pushed into the higher tax brackets of California’s progressive tax system, which would extract much higher taxes than if you could spread the excess income over two or more years.

While these patterns are understandable, not evidence of carelessness, they won’t let you achieve the optimal results you want.

You need a different approach for that.

3 Proven Strategies High Earners Use to Reduce California State Taxes

In California, there are 3 main ways you can optimize your lifetime taxes.

- Time Your Income to Avoid California’s Highest Tax Brackets

- Build State Tax Efficiency Into Your Investment Portfolio

- Plan Taxes Across Years, Not Just Tax Seasons

Here’s how they work.

1. Time Your Income to Avoid California’s Highest Tax Brackets

Here, your power move is combining two ideas, income timing and the resulting tax rates.

In a high-tax state like California, this is connected even more tightly than in other states.

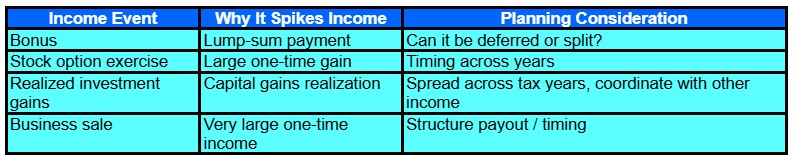

Beyond “base” income, high earners often have other large compensation sources (Table 1).

- Bonuses.

- Exercised stock options.

- Significant realized investment gains, e.g., when selling Restricted Stock Units (RSUs) at highly appreciated prices.

- Selling (part or all of) a business.

When several of these get stacked in a single tax year, you may get pushed into higher marginal tax brackets, forcing you to pay a larger fraction of your income in taxes.

Dr. Steven Crane, Founder of Financial Legacy Builders, agrees, “The biggest mistake I see is people focusing only on how much they make, not when and where it’s taxed. California is aggressive, and if you stack income in one year, bonuses, stock sales, and business income, you can get hit far harder than expected. A lot of high earners don’t realize they’re creating their own tax problem just through timing.

“The people who plan ahead keep more. The ones who react usually pay more. California taxes success aggressively, but it doesn’t mean you’re stuck. The key is realizing that taxes aren’t just something that happens to you; they’re something you can plan around. Most of the damage I see isn’t from bad investments, it’s from unplanned tax events that could have been managed with a little foresight.”

That’s why smart high earners try, when they can, to spread these events across multiple years. This doesn’t let them avoid the tax, but it does let them pay at least somewhat lower taxes on the same income.

A similar notion shows up in picking what retirement accounts to contribute to.

Roth accounts, both IRA and 401(k), are attractive because they let you pay taxes now on your contributions, but avoid paying any taxes on withdrawals, even when the majority of the withdrawn money is investment gains.

That makes sense in some situations.

But when your current marginal tax rates are very high, that’s an expensive choice. One that doesn’t usually optimize your long-term results.

As Joe Stabile, Founder at Coast Financial, explains, “A common mistake I see many high earners in California make is blindly choosing to fund Roth retirement accounts. While Roth accounts have their benefits, it’s important to realize that your top marginal tax rate in California, between federal and state, can be 50.3%, which means any income you can defer at this level to future years, where your effective rate is lower, is extremely powerful. Deferral strategies can include 401(k) plans, HSAs, deferred compensation plans, cash balance plans for business owners, and more.”

The key here is that by contributing to a tax-deferred account, rather than a tax-now account like a Roth, you can pay taxes later, when your marginal tax bracket may be lower.

This will often reduce your lifetime taxes, even with the same lifetime income.

If, like me, you’ve put most of your long-term savings into such tax-deferred accounts, you may be unhappy that all withdrawals, including money that originated from long-term capital gains, get taxed at regular income tax rates, rather than at preferential LTCG rates.

In states like California, where LTCG is taxed the same as regular income, the negative impact of this is smaller than in states that treat LTCG preferentially, as do federal taxes.

Tushar Kumar, Founder, Twin Peaks Wealth Advisors, has a different perspective, “The number one mistake I see high taxpayers in California making is not maxing out all of the tax-advantaged buckets at their disposal. Most of my clients max out their 401(k) contributions, but many overlook the Mega Back Door Roth 401(k) option. Most of my clients make some contributions to 529 accounts, but many don’t max them out or don’t take advantage of the super-funding rules. Most people don’t understand how much money they are leaving on the table by not maxing out these accounts.”

How California treats the 529 college savings plan is different from many other states. There is no state tax deduction for contributions made to these plans, but qualified withdrawals are tax-free.

Ajay Vadukul, CFP®, EA, Vice President of Endeavor Advisors, also sees Roth accounts as a useful tool, “Roth conversions are a conversation we start early, too, since California offers no special treatment for retirement distributions. Converting in lower-income years before Required Minimum Distributions (RMDs) kick in reduces your long-term burden at both levels.”

2. Build State Tax Efficiency Into Your Investment Portfolio

Next up is how you structure your investments.

Not all income sources get taxed the same, which you can use to your benefit.

For example, as Ray Prospero, Partner Advisor, AdvicePeriod, details, “My practice is geared toward the high-net-worth space, and two of the tax-mitigation strategies I like to explore for my high-income California clients are municipal bond ladders and direct indexing.

“Municipal bond ladders can generate consistent, tax-advantaged income while managing interest rate risk by holding individual bonds with staggered maturities. On the equity side, direct indexing gives us more control. By owning the individual stocks within an index, we’re able to harvest losses throughout the year, even in up markets, while staying broadly aligned with overall market performance. Those losses can then be used to offset capital gains and potentially reduce a portion of taxable income.

“When combined, it can be an effective way to potentially enhance tax efficiency while maintaining a disciplined, long-term investment strategy.”

Kumar agrees, “I see many California residents sitting on cash in high-yield savings accounts or money market funds when they could be considering California muni bonds for tax-free yield. Of course, there is a risk trade-off there.”

As this demonstrates, you can and should build tax efficiency, especially at the state level, into your portfolio structure.

Income from municipal bonds is exempt from federal and, for bonds issued by California public agencies, state taxes.

Direct indexing lets you harvest losses even when the index is up. That’s because there are almost always some companies in the index with depressed prices, even in a bull market. This means you can sell those shares to capture a loss, without selling the entire index, which may be at a higher price point than when you bought in.

Then, when enough time has gone by so it isn’t a wash sale, you can buy back those shares to reestablish the full index.

Doing this consistently, not as a once-and-done exercise, provides long-term tax benefits. That’s why you should make a point of it, even if you’re busy.

3. Plan Taxes Across Years, Not Just Tax Seasons

Yes, income is reported, and taxes are paid on an annual basis.

But that doesn’t mean that’s the optimal way to plan. The most effective tax strategies play out over years or even decades and help guide and coordinate decisions across multiple aspects of your financial life.

As James Selu, CFP®, CEPA®, CBDA®, President & Founder of Palm Coast Wealth Management, says, “One of the biggest mistakes high earners make is waiting until tax season to think about taxes. By the time you’re preparing a return in March or April, the tax year is already over, and many of the best planning opportunities are gone. At that point, you’re often limited to reporting what happened rather than improving it.”

This is where long-term planning becomes critical.

Advanced tax planning for higher-net-worth households looks five, ten, twenty, or even more years into the future, rather than focusing on the next Tax Day.

These strategies include various trusts, permanent insurance, annuities, charitable giving vehicles, and more, with each family’s situation calling for a different set of tools, implemented in a tailored way.

Selu again, “Depending on the client’s situation, strategies may include maximizing retirement plan contributions, Roth conversions in lower-income years, tax-loss harvesting, charitable giving, municipal bond strategies, deferred compensation planning, or repositioning assets into more tax-efficient investments. The right strategy depends on how someone earns income: W-2 wages, business income, stock compensation, real estate, or investments.”

Vadukul expands, “The biggest mistake high-earning Californians make is treating state taxes as a fixed cost instead of a planning opportunity. With California’s 13.3% top rate, there’s real leverage available. You just have to use it.

“For clients who are charitably inclined and over 70½, qualified charitable distributions from your IRA are one of the cleanest tools available, reducing your Adjusted Gross Income (AGI) at both the federal and state level in one move. If you’re sitting on appreciated stock, gifting shares to children in a lower bracket rather than selling yourself can dramatically cut the capital gains bill.

“On the deferral side, maxing your 401(k) is table stakes, but self-employed clients and business owners should be looking at solo 401(k) plans or cash balance plans, which can shelter hundreds of thousands annually. An S-corp election is also worth revisiting for the right business owner. And for clients facing a large capital gains event, Qualified Opportunity Zone investments can defer and potentially reduce that exposure in ways most people haven’t considered.”

None of this implies that you, or even a financial advisor, can predict the future with any guaranteed accuracy.

However, planning over the long term gives you a better chance of success than focusing on the current tax year, or worse, on the previous one.

Taken together, these three levers don’t eliminate state taxes, but they do let you optimize how you position yourself, which determines how efficiently you can maximize your lifetime take-home money.

The Bottom Line: California Taxes Are High, But Your Lifetime Tax Bill Isn’t Fixed

Whatever you think or feel about California’s high state income taxes, if you live there and earn a high income, they’re a major, unavoidable factor in your financial picture.

Some people suggest moving out of California because of this.

Moving to a lower-tax state can indeed reduce your tax burden, but you should only consider it if it makes sense for your overall life. And even then, California’s residency rules mean the timing and structure of that move matter. If it looks temporary or primarily tax-driven, you may not achieve the outcome you expect.

Vadukul agrees, “Something I only half-joke about with clients: one of the most effective California tax strategies is leaving California. Texas, Nevada, Florida, Arizona. The savings can be $50,000 a year or more for a high earner. But there are things money can’t buy. Family, community, California’s business ecosystem. I’ve had clients look at that number and say, ‘still worth it to stay,’ and that’s a completely legitimate answer. The goal is to make sure the decision is informed, not to let the tax tail wag the life dog.”

For most people, you can get the results you want from planning, without needing to relocate. From not treating taxes as something you deal with once a year for a few weeks, but rather planning and managing them continuously, even if you’re busy with your career and family.

As Selu puts it, “Successful professionals are so busy building careers or businesses that tax planning gets pushed aside. Unfortunately, California’s high state tax rates can make procrastination expensive. Without proactive planning, people often miss opportunities to manage income timing, harvest losses, maximize retirement contributions, or structure investments more efficiently.

“Tax planning should be ongoing, not seasonal. The earlier you plan, the more options you tend to have. The most valuable habit a high earner can have in this regard is scheduling a coordinated year-end tax planning meeting with both their financial advisor and CPA before December 31. That gives you time to evaluate what happened during the year and make adjustments while there’s still time to act.

“California taxes may be high, but with proactive planning, coordination, and discipline, you can often reduce unnecessary tax drag and keep more of what you earn.”

Crane sums it up, “The most effective strategies usually come down to control. Control when income hits, diversify how it’s taxed, and be intentional about where you live and work. That might mean spreading income across years, using tax-deferred and tax-free buckets, or even thinking seriously about residency if it aligns with your life.”

It’s simple, but not necessarily easy to implement:

Taxes aren’t just something you file. They’re something you manage.

Ongoingly.

And in a high-tax state like California, small, consistent improvements in how you manage them can add up to a noticeable difference in what you keep over a lifetime.

Are You Ready to Hire a Financial Advisor?

You’ll find a growing number of financial advisors featured on Wealthtender. You can search based on the areas of specialization most important to you and where they’re located, or browse our financial advisor directory for more search options to find advisors who may be a good fit for you.

Find Your Next Financial Advisor on Wealthtender

📍 Click on a pin in the map view below for a preview of financial advisors who can help you reach your money goals with a personalized plan. Or choose the grid view to search our directory of financial advisors with additional filtering options.

📍Double-click or pinch pins to view more.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher