If you live in a high-tax state like California, New York, or Maryland, the idea of moving somewhere with no state income tax like Florida or Texas probably sounds like an obvious financial win. And for some people, it genuinely is. But the mistake most people make isn’t moving to a no-income-tax state, it’s treating a complex, life-altering decision as if it has a simple, single-variable answer. Because when you factor in what actually changes — property taxes, insurance costs, public services, infrastructure, and the less-quantifiable things like proximity to family — the math gets a lot more complicated than your last state tax return suggests.

Key Takeaways

Moving to a no income tax state saves money on one line item — but often raises costs on others.

States without income tax still need revenue, so they typically offset it through higher property taxes, sales taxes, and fees. According to Tax Foundation data, Florida and Texas have lower overall per-capita tax burdens than the national average — but the gap may be smaller than your income tax bill alone suggests, especially once housing, insurance, and daily living costs are factored in.

This is a full-life tradeoff decision, not a tax decision.

Moving to a lower-tax state means accepting a different mix of public services, infrastructure quality, insurance costs, and distance from family — none of which show up in a tax calculator. Financial advisors consistently report that lifestyle factors, proximity to family, and day-to-day quality of life matter more to their clients than tax savings once the move is made.

The move makes the most sense when your tax savings are large, your lifestyle tradeoffs are acceptable, and you’ve pressure-tested your assumptions.

High earners in high-tax states like California or New York can see the largest absolute savings — potentially tens of thousands of dollars annually — which can justify the move when the non-financial tradeoffs are acceptable. The people most likely to be satisfied after moving are those who evaluated the full picture first, not just the headline tax rate.

Many people look at states with no income tax, like Texas and Florida, with more than a little envy. Especially high earners in high-tax states like California and New York think, “No state income tax? Sign me up!” And it makes a good bit of sense.

If you can legally stop paying tens of thousands of dollars in state taxes, why wouldn’t you?

As a Maryland resident paying the fourth-highest state-income-tax rates and fifth-highest overall taxes in the nation, I get the appeal. I pay much more in taxes than someone in a similar financial situation living in Florida (5th-ranked overall tax competitiveness index in the nation) or Texas (7th-ranked). But I know what this buys me, and the tradeoff works for me.

That’s the part that’s critical to think all the way through, but that not many do.

Yes, moving to a no-income-tax state can absolutely lower your tax bill. But that doesn’t necessarily translate into an overall improvement of your life, or even of your financial picture. In many cases, the costs just shift to different budget line items.

Moving to a no-income-tax state isn’t necessarily a mistake in all cases. The mistake is to use a single variable, like state income taxes or even the overall state tax burden, to make a life-altering decision that depends on far more than just taxes.

To make this decision wisely, you have to recognize that it isn’t really a tax decision. It’s a full-life tradeoff. And if you miss this critical point, you risk experiencing a major disappointment, as your expected savings from taxes, after accounting for how other expenses change, may be far smaller than you expected.

Worse, you may find that there are other, non-financial impacts that you wouldn’t have chosen to live with.

You’re already working hard to improve your situation, so the last thing you want is to shortcut the assessment phase and make a move that seems like a no-brainer on its surface, but that ends up providing smaller benefits alongside unexpected, unwelcome side effects.

Because your goal isn’t just to pay lower taxes. It’s to actually be better off, which requires making a solid, fully thought-out decision, not a reckless one.

Benjamin Simerly, CFP®, Founder & Wealth Advisor, Lakehouse Family Wealth, observes that financial gain is the least important aspect of deciding on a move, “I truly believe the biggest factor that should determine where you live is lifestyle. No matter the politics or taxes, good, bad, left, right, of any area, things like traffic, proximity to desired friends and activities, ease of lifestyle, length of time at the grocery store with level of business, etc., become the real decision makers.

“The kicker is that I’ve seen lifestyle be the reason younger folks move to the city, and older folks (with more emphasis on day-to-day ease) move to lower-tax areas.

“Ironically, the more retirement communities pop up for truly active lifestyles, especially closer to where grandchildren might live, the less I imagine people might move because of taxation. So, moving to be close to grandchildren for healthy reasons can be great. With planning, taking advantage of time with family is the number 1 win we see.”

The Tax Savings Are Real, But Incomplete

This is the simple part that most people get right. States like Texas and Florida don’t just have no income taxes. They have a lower overall per-capita tax burden than most states.

According to 2022 data from the Tax Foundation, the average combined per-capita state tax burden in the US is $7,109. Florida comes in at $4,914 (4th lowest), and Texas comes in at $5,469 (17th lowest).

That’s significant. This is why, especially for high earners from high-tax states like California or New York, moving to a no-income-tax state like Florida or Texas can lead to real tax savings. That’s why I’m not arguing that making such a move is a bad idea.

The mistake is assessing such a multi-factor decision through just that single factor. Because when you’re trying to improve your situation without unnecessary risk, it’s easy to latch onto something that looks like a clear win.

But while lower taxes can absolutely help, they don’t guarantee a better outcome. If you don’t consider all the tradeoffs that come with it, you can’t tell if you’ll actually be better off and happier after moving.

When something feels like an obvious win, especially in a complex decision, it’s usually worth slowing down and asking what you might be missing.

What Actually Changes When State Income Tax Goes Away

Obviously, as you’d expect in a no income tax state, the state income tax budget line-item goes to zero.

Win!

But is it truly that simple?

Not really.

All states levy taxes to fund government operations like public safety, courts, water systems, roads, bridges, and other core services. And states also differ in the services and programs they choose to fund.

When a state chooses not to tax income, it still has to fund whatever functions that state’s government takes responsibility for.

So, the question is not whether they’ll collect taxes. It’s what they’ll tax, who will pay those taxes, and what level of services they will fund.

And that’s something you need to evaluate before you move, not after.

If you stop your analysis at, “No state income tax? Win!” it’s easy to think you’ve found a simple way to reduce your costs without much downside.

John Davis, CFP®, EA, founder of JKD Financial, agrees, “The biggest thing people overlook is the total tax impact. States with no income tax still have funding needs (roads, schools, etc.); they just use other revenue sources to meet those needs. This comes in the form of higher property taxes, sales tax, and overall higher fees for normal government programs. These taxes add up and often create a similar out-of-pocket expense as income taxes.

“One of the biggest things I see with my clients, who are mostly near or at retirement, is the additional travel costs. Many of my clients move away from family to no-tax states. Because of that, they end up spending more to either go back to visit family or pay for children and grandchildren to come visit them. This takes away from their travel budget elsewhere, as well as time available to do other trips. I often call the cost of flights and hotels to maintain those family connections the ‘grandkids tax.’

“My recommendation is to start with your desired lifestyle, then do the math. You should look at your income as it currently stands, what you project in retirement, and how that’s taxed in your current state. Many people don’t realize their current state may already exempt their biggest income sources, like Social Security, pensions, or capital gains. These are common income sources for retirees. If your effective tax rate is already low, the friction and cost of moving might be greater than your actual tax savings.”

In reality, you may find a move to a no-tax state has unexpected consequences you won’t be as happy about, such as:

- High property taxes that increase the burden on homeowners.

- High sales or consumption taxes that increase the burden on consumers.

- High state fees that increase the burden on, e.g., drivers.

- Leaner government services that push many expenses onto individuals and families.

- More travel expenses to maintain family relationships.

Thus, real income-tax savings aren’t free.

You may pay nothing through one channel – state income tax, but more through others. Some costs will be obvious. Others show up in different ways, like weaker infrastructure, fewer public services, or higher out-of-pocket spending.

That’s why moving to a no-tax state may be riskier than it appears if you don’t look beyond the headline tax savings.

People who make this move often don’t realize they’re not just reducing taxes. They’re stepping into a different system with different tradeoffs. You may think it’s a straightforward tax decision, but in reality, whether you realize it in the moment or only much later, you’re choosing a different mix of taxes, expenses, services, and tradeoffs.

That means the real question isn’t whether you’ll pay less in taxes. It’s whether you’ll actually be better off living in that new system.

And that’s something you need to evaluate before you move, not after.

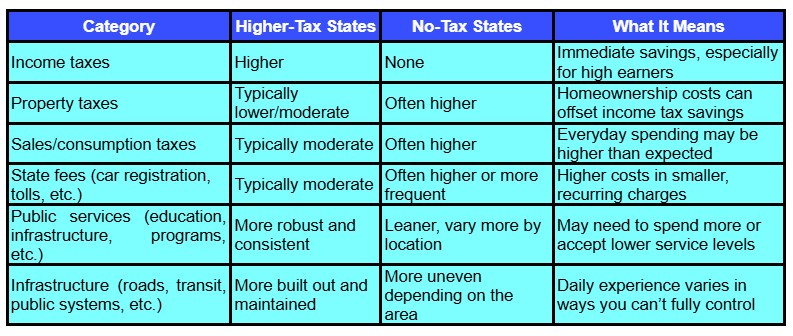

The Tradeoff: You Pay Less, and You Often Get Less

No question, paying lower taxes is helpful.

But it isn’t a standalone outcome. It comes with a tradeoff. You aren’t just lowering taxes. You’re changing the wider picture of how you pay and what you get, as we see in Table 1.

This gives you a practical way to assess whether the move actually improves your situation, instead of assuming it will be based on a single factor – state income tax. Rather than “Is paying lower taxes worth the hassle of an interstate move?” your real decision should thus be “Is this overall tradeoff worth it to me?”

Instead of a pure reduction in expenses due to lower taxes, you need to realize that you’re moving to a completely different mix of costs, services, and experience.

You may be happy with some parts of the change and unhappy with others. Unfortunately, if you don’t consider everything carefully beforehand and do your due diligence, you may get blindsided by some of the changes, especially non-financial ones like the consistency and quality of the infrastructure and environment you’ll have to live with.

That’s a much broader decision than most realize when they consider moving to a state where their income tax burden will be lower.

When Moving to a No Income Tax State Makes Financial Sense

In some cases, moving to a no-tax state is exactly the right decision.

For that to be true, certain conditions need to be met that tilt the above-mentioned tradeoff strongly in your favor. First and foremost, you need to be ok with the change in community, moving away from friends and (possibly) family, and the change in your professional environment.

Beyond that, here are some specific cases.

1. Your Tax Savings Are Large Relative to Your Lifestyle Changes

If you’re a high earner living in a high-tax state, your tax savings could amount to many tens of thousands of dollars a year.

For example, a single filer making $500k a year in California, taking the standard deduction, and maxing out their 401(k) contribution would pay about $41k in state income taxes alone.

Moving to, e.g., Texas, even assuming no change in salary, saves that large tax payment.

That can justify the move, especially if:

- You’re happy with your expected housing situation.

- Your day-to-day spending doesn’t increase too much.

- You don’t rely too much on any services that are reduced or less consistent in the place to which you move.

If that’s your situation, the tradeoff is simple and highly beneficial. You give up little and have a big financial win.

2. You’re Not Heavily Dependent on State-Provided Services

Not everyone relies on public services to the same extent.

If you have no school-age kids, you aren’t directly affected by the level of state investment in K-12 education.

If you prefer to drive everywhere, public transport, or lack thereof, is of little concern (though you may want to consider possible impacts on traffic congestion and air quality).

If you don’t use local support systems, having a leaner state government doesn’t affect your quality of life too much.

If the above are all true for you, the tradeoff is, again, a net plus.

3. You’re Willing and Able to Replace What the State Doesn’t Provide

This is a trickier one.

If you do use state-provided services where you live now, and those won’t be provided for you in your new state, you’ll need to replace them or do without.

This can include:

- Education options and quality for your school-age kids – private schools are notoriously expensive.

- Healthcare access and quality – especially if you’re not in great health, high-quality hospitals that get less state funding are more expensive.

- If your new location suffers from poorly maintained infrastructure, that poses inconveniences and even safety concerns that can’t be addressed privately.

- If you move to, e.g., Florida, homeowner insurance will likely be more expensive and even hard to obtain in some locations.

If, after considering all these and similar factors, the net savings is still large enough, a move can make sense.

4. Your Values and Lifestyle Preferences Align with the Tradeoff

Some people simply prefer lower taxes, a leaner government that’s less intrusive, and different regional priorities and values.

If these, as they are in your target state, are better aligned with your values and preferences than what you experience now, a move can make sense even if the financial factor isn’t a strict win.

What Does This Mean for Your Decision?

Moving to a no-tax state isn’t overall “right” or “wrong.”

It can be a net positive or a net negative, depending on your personal situation and preferences, and how well the tradeoffs match them.

As long as:

- The savings are large enough to be an important factor for you,

- The tradeoffs are acceptable to you, and

- You’re prepared for the changes you’ll experience.

As long as those conditions are true, the move can work very well.

But if even one of them doesn’t hold, the outcome becomes much less predictable.

That’s when what looks like a clear financial win can turn into a frustrating tradeoff, where the savings are smaller than expected, and the downsides are harder to live with, if not outright unacceptable.

When Moving to a No-Tax State Can Fall Short or Even Backfire

It’s a big decision, and if you’re not careful, things can fall apart.

Yes, it may save you tens of thousands of dollars on paper, but once you consider all the other financial implications, the outcome may not be as favorable as it looks on the surface.

Even more importantly, your new life may fall far short of your expectations, or even short of your current situation, sometimes in ways that aren’t obvious until after the move.

Here are some possible scenarios where this could happen.

1. Your Costs Shift More Than Expected

After the move, you may face higher insurance costs, higher day-to-day expenses due to higher sales tax, and major out-of-pocket expenses for things you don’t want to give up and that are state-funded or state-subsidized in your current state but not in your target state.

If these increases are large enough, they’ll offset much of your state income tax savings.

This may make the benefit of the move too small to justify the non-financial impacts.

2. The Non-Financial Impacts Matter More Than You Thought

Knowing your state income tax is as simple as looking at last year’s state tax return, or possibly asking your accountant for their estimate for the current tax year.

That’s how easy it is to figure out the likely maximum financial benefit.

What isn’t as easy is quantifying and assessing the impacts of:

- Lower infrastructure quality.

- Healthcare access, quality, and consistency.

- Public school quality.

- Environmental factors.

- General day-to-day convenience.

- Connection to family.

These don’t show up in your budget.

But they can have a massive impact on how enjoyable you may find living in your new location. In ways that are hard to ignore once you’re experiencing them daily.

If these things matter to you enough, they can make the move feel like a big mistake, even if the financial impact is positive.

As Simerly says, “The biggest tradeoff that surprises people after they move to a lower-tax state is lifestyle. Tax changes tend to come with lifestyle changes, more or less traffic, more or less time for fun, and more or fewer friends. And my clients who moved to lower-tax areas appreciate lifestyle improvements most. I saw the tax numbers change, but clients saw both their disposable income and the time available to spend it increase. These lifestyle factors tend to be far more important to them than the lower tax.

“If you’re considering moving, my top recommendation is to talk with your children! I’ve met more than a few couples who made a big move, only to have a new grandchild born five states away 6 months later. Family can be the biggest driver of a potential move, no matter the tax changes. The things you can’t replace aren’t things; they’re family.

“If you’ve saved money and have enough to retire comfortably, you can likely afford the extra taxes. The fun you have in retirement, and the time you spend with people and hobbies you care about, these will be far more important.”

3. Your Situation Changes After You Move

Your move may make perfect sense today, even considering the non-financial factors.

But life changes.

- Your health could deteriorate.

- You may not have kids now, but that could change, and they need to attend school.

- Your preferences may evolve.

If this happens, a move that made sense under one set of assumptions may become less attractive.

It isn’t that this would necessarily mean the move was a mistake, but it does imply that you should try to have a wider margin to accommodate such potential changes.

What Does This Mean for Your Decision?

The core mistake people make when making a move that turns out badly is making a multi-factor decision based on single-factor thinking.

When you do this, it’s too easy to:

- Make a shallow assessment.

- Overestimate the value of the benefit.

- Underestimate, or even ignore, the tradeoffs.

This is how what should have been a deep dive into a complex life-changing decision gets inappropriately seen as a slam-dunk no-brainer.

This isn’t to say you shouldn’t move.

It’s to make sure that you don’t short-change your decision-making process.

Because when you broaden your lens, the decision becomes less obvious, but once made, it’s more likely to work out well.

As Dr. Steven Crane, Founder of Financial Legacy Builders, says, “The biggest thing many people miss is that taxes don’t exist in a vacuum. They fixate on state income tax and ignore everything else, property taxes, insurance, cost of living, and even how income is sourced. I’ve seen people move, thinking they’re saving money, only to realize the total picture didn’t change much.

“A lot of people are surprised that life doesn’t automatically get cheaper just because income taxes go away. Housing, insurance, and everyday costs can offset a big chunk of the savings. And beyond money, you’re also dealing with lifestyle changes, being further from family, different services, and a different pace of life. That stuff matters more than people expect.

“I tell clients to run the full picture, not just the headline tax rate. Look at your actual spending, your income sources, and how everything changes in the new state. Then stress-test it. If the move only works on paper but not in real life, it’s probably not the right move. Taxes are important, but they shouldn’t be the only reason to pick where you live.”

How to Actually Evaluate This Decision

Now that you recognize this isn’t a simple tax-reduction decision, here’s a simple, structured way to assess it broadly enough to make a better-informed choice.

Step 1: Quantify the Real Financial Benefit

First, obviously, figure out your expected state income tax savings (accounting for the federal deduction, if you itemize). Then, adjust for other financial impacts:

- How will your housing costs change, including property taxes?

- How will your daily cost of living change, including sales taxes?

- How will your homeowner’s insurance and other policy premiums change?

- What things will you need to pay for, which are currently free through state funding, and how much will they cost?

Absolute precision isn’t possible or necessary here.

But directionally, will you save a lot? Enough?

As Simerly says, “In our experience with clients, the most overlooked factor, with the biggest budget impact, lies in everyday expenses, not the primary income tax itself. Gas costs, contractor rates, commodities, goods and services, etc., tend to make the biggest differences in our clients’ budgets, especially in the major categories of transportation and housing-related concerns. Of course, you should always do your own math. If you travel a lot and don’t spend much money at home, these expenses may not be a real concern for you.”

Step 2: Identify What Will Change in Your Day-to-Day Life

Next, look beyond the numbers:

- What services and infrastructure do you rely on today?

- How will these be different in your new state?

- Which of these changes matter to you, and to what extent?

These things can’t be captured in a spreadsheet, but they can make your overall daily experience positive or, conversely, an emotional drag.

Step 3: Pressure-Test Your Assumptions

This is a critical step that many people miss.

Rather than simply assuming everything will work out just fine, start with an assumption that it won’t, and figure out what could cause that negative outcome.

Ask yourself:

- What would have to go wrong to make this move feel like a big mistake?

- How likely is it for these things to happen?

- How confident am I that I’m not missing other risks?

If you’re struggling to answer these questions clearly and with confidence, you’re not done assessing the move.

Step 4: Decide if the Tradeoff Is Worth It for You

There isn’t a universal answer for this question.

But that’s ok, because you don’t need to answer it for everyone, just for you.

If:

- your expected net financial benefit is meaningful,

- the tradeoffs are acceptable (or even appealing), and

- you’re comfortable with the risks,

Then the move makes sense for you.

If not, even with a heavier tax burden, staying put is the better choice.

The Bottom Line

Moving to a no-income-tax state can be very good for your finances.

But that alone isn’t enough to make a solid, well-informed decision.

For that, you need to consider and accept the tradeoffs. The people who are most likely to benefit from such a move aren’t necessarily the ones who pay the most in state income taxes.

They’re the ones who take the time to fully explore and understand all the consequences and tradeoffs of such a major life-changing choice and make a decision that leaves them truly better off, not just paying lower taxes.

Are You Ready to Hire a Financial Advisor?

You’ll find a growing number of financial advisors featured on Wealthtender. You can search based on the areas of specialization most important to you and where they’re located, or browse our financial advisor directory for more search options to find advisors who may be a good fit for you.

Find Your Next Financial Advisor on Wealthtender

📍 Click on a pin in the map view below for a preview of financial advisors who can help you reach your money goals with a personalized plan. Or choose the grid view to search our directory of financial advisors with additional filtering options.

📍Double-click or pinch pins to view more.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher