Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Traditional, Roth, HSA, or taxable account – which maximizes after-tax income and legacy?

Now that I’m mostly retired and have most of our nest egg in traditional tax-deferred accounts, I find myself wondering if I made a mistake.

With Required Minimum Distributions (RMDs) looming, will those decades of tax deferral come back to haunt me?

We did maximize our Health Savings Account (HSA), but should I have put less into tax-deferred accounts and more into Roth or taxable instead?

Let’s compare four account types so you can decide which one really wins for you.

What Does Winning Mean Here?

For pre-retirees, here are the criteria I find most important:

- Flexibility before retirement (e.g., convertibility)

- After-tax retirement income

- Maximum amount allowed to be invested, including income limits (if any)

- Limitations on penalty-free and/or tax-free withdrawals

- Tax treatment for spousal and non-spousal heirs

As we’ll see below, every account is a trade between tax timing, flexibility, and legacy efficiency. Thus, different account types “win” in different circumstances and by different criteria.

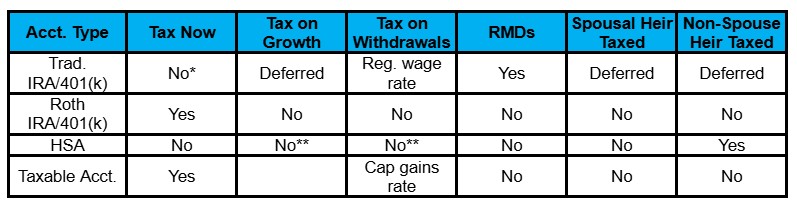

Meeting Our Contenders and Their Tax Characteristics

Here’s a quick reference guide for the tax characteristics of the different account types.

Next, let’s dig a little deeper into each account type.

Traditional IRAs and 401(k) Plans

Both of these are tax-deferred retirement accounts. The IRA is an individual plan available to anyone with earned income, while the 401(k), along with its cousins, the 403(b) and 457 plans, are employer plans to the benefit of employees.

Since the 403(b) and 457 are limited to employees of state and local governments, religious organizations, public schools, and non-profit organizations, we’ll ignore them here.

Annual Contribution Caps (for 2026)

- IRAs: $7,500, plus $1,100 catch-up for people over age 50.

- 401(k) plans: $24,500 elective salary deferral, plus $8,000 catch-up for employees over age 50. Employers are allowed, but not required to, match employee contributions. However, the overall contribution may not exceed the lower of 100% of the employee’s compensation or $72,000 ($80,000 if over age 50 and $83,250 if aged 60-63).

- Note that these limits are shared with the Roth versions of the same account types.

Income Limit to Contribute

None.

Deductibility Limits (for 2026)

- For IRAs, there is a complex set of deductibility limits, depending on your filing status and whether or not you and/or your spouse have access to an employer retirement plan. For example, if married and filing jointly, and you have access to an employer plan, you can fully deduct up to a Modified Adjusted Gross Income (MAGI) of $129,000. For MAGI above $149,000, none of your contributions are tax-deductible. For MAGI between the two numbers, you can deduct a prorated fraction of the contribution. If neither you nor your spouse (if married) can access an employer plan, the deductibility of your contributions isn’t subject to income limits.

- There are no deductibility limits for employee contributions to 401(k) plans (up to the contribution limit). Employer contributions are deductible to the employer, up to 25% of employee compensation.

Withdrawal Rules

- Taxed as ordinary income in the year of the withdrawal.

- With limited exceptions, withdrawals before age 59½ are subject to a 10% penalty in addition to taxes.

- RMDs apply (if not already subject to RMDs, RMDs begin at age 73 for those who turn 73 before 2033; those who turn 73 in 2033 or later will be subject to RMDs from age 75).

Heir Rules

Inheritance rules are different for spouses and non-spouse heirs.

- Spouses:

- If the original account holder had already started RMDs, their widow(er) can (a) keep the account as an inherited account and delay their distributions until the original account holder would have turned 72; (b) take distributions based on their own life expectancy; or (c) follow the 10-year rule, wherein they must drain the account within 10 years of the original account holder’s death. Alternatively, the widow(er) can roll the account over into their own IRA.

- If RMDs had not been started, the widow(er) can keep the account as an inherited account and take distributions based on their own life expectancy, or roll it over into their own IRA.

- Non-spousal heirs:

- If an “eligible designated beneficiary” (for non-spouse, this is a minor child of the original account holder, disabled or chronically ill, or someone who is no more than 10 years younger than the original account holder), can (a) take distributions over the longer of their own life expectancy or the original account holder’s remaining life expectancy, or (b) follow the 10-year rule.

- If not an eligible designated beneficiary, must follow the 10-year rule.

Pro for Pre-Retirees

Get tax deductions during peak earning years.

Cons for Pre-Retirees

- RMDs apply.

- Withdrawals get stacked as taxable income on top of wage income and realized short-term capital gains, all subject to the high rates of taxes on regular wages. This may push you high enough to be subject to Medicare Income-Related Monthly Adjustment Amount (IRMAA).

- Non-spousal heirs must drain the account within 10 years and pay regular wage tax rates on the resulting withdrawals.

Roth IRAs and 401(k) Plans

These are similar to the traditional accounts mentioned above, but instead of getting a tax deduction now and paying taxes later, you contribute after-tax dollars, and withdrawals are tax-free (once the account has been open for five years).

Annual Contribution Caps (for 2026)

- IRAs: Share limit with traditional IRAs.

- 401(k) plans: Share limits with traditional 401(k) plans.

Income Limit to Contribute

- Complex income limits for Roth IRAs – for example, if married and filing jointly, MAGI up to $236,000 allows Roth contributions. MAGI above $246,000 disallows it. MAGI between those allows a prorated reduction in contribution limits.

- Can convert from traditional to Roth. Note that the IRS uses a pro-rata rule for the total balance of after-tax vs. pre-tax balances across all IRAs when calculating what part of the conversion is not taxable.

- Can make “back-door” contributions by making an after-tax contribution to a traditional IRA, then converting to a Roth. The pro-rata rule applies here too.

- None for 401(k).

Deductibility Limits

Not deductible.

Withdrawal Rules

- Tax-free withdrawals.

- Withdrawal of contributions is allowed, but you cannot later reverse it.

- With limited exceptions, withdrawals of earnings before age 59½ and/or before the account is five years old are subject to a 10% penalty.

- RMDs don’t apply.

Heir Rules

Generally, the same rules as for non-Roth accounts, except that withdrawals are tax-free, However, withdrawals of earnings from accounts that are less than five years old may be subject to income tax. Since the 10-year rule doesn’t require withdrawals in any specific year, the heir can hold off on withdrawals until the Roth account is five years old, and thus avoid such taxation.

Note that heirs’ RMDs from an inherited Roth account are separate from RMDs from Roth accounts not inherited from the same person.

For qualified employer plans, such as a 401(k), there are further rules.

Pros for Pre-Retirees

- Tax-free retirement income.

- Heirs receive tax-free.

- If tax rates are lower now than later, can pay lower tax now to avoid higher tax later.

- No RMD

Cons for Pre-Retirees

- No current tax deduction, potentially at a high tax bracket.

- Higher taxes now may mean current cash flow doesn’t allow maxing the contribution limits.

- Conversions cause a taxable income spike, possibly causing IRMAA.

HSAs

These are intended to provide a way to cover qualified healthcare expenses with pre-tax dollars. These accounts enjoy a triple tax benefit:

- Tax deduction for contributions.

- Tax-free growth.

- Tax-free withdrawals (for qualified health-related expenses).

As a result, these can be used as a long-term way to maximize healthcare dollars for retirement.

Annual Contribution Caps (for 2026)

Assuming you have an HSA-compliant high-deductible health plan (HDHP), you can contribute up to $4,400 for an individual or $8,750 for a couple or family.

Income Limit to Contribute

None.

Deductibility Limits

Fully deductible (assuming HSA-compliant health plan).

Withdrawal Rules

- Tax-free withdrawals for qualified health-related expenses.

- After age 65, can use like a traditional IRA for non-health expenses.

- RMDs don’t apply.

Heir Rules

- Spouses: inherit as HSA.

- Non-spousal heirs: taxed for full market value in the year of inheritance. This means, for example, an inherited $200,000 HSA could add $200,000 of taxable income to your child in a single year, potentially pushing them up into an extremely high tax bracket.

Pros for Pre-Retirees

- Current tax deduction.

- Tax-free way to fund healthcare expenses in retirement.

- No RMD

Cons for Pre-Retirees

- Must be enrolled in HDHP.

- Penalties apply for withdrawals not used to cover eligible health-related expenses before age 65.

- Worst tax setup for non-spousal heirs.

Taxable Portfolio

This is the least tax-efficient for you, but more tax-efficient for your heirs than a traditional retirement account, and especially compared to an HSA.

Annual Contribution Caps

None.

Income Limit to Contribute

None.

Deductibility Limits

Not deductible.

Withdrawal Rules

None.

Heir Rules

Heirs enjoy a step-up in basis, which means no taxes are ever due on gains that were unrealized as of the death of the original account owner.

Pros for Pre-Retirees

- When used for retirement income, (long-term) realized capital gains are taxed at the preferred long-term capital gains rates (0%, 15%, or 20%, depending on your taxable income).

- Greatest flexibility.

- Heirs receive with step-up basis.

- No RMD

Cons for Pre-Retirees

- No current tax deduction, potentially at a high tax bracket.

- Dividends and interest are taxed in the current year.

- Mutual funds distribute capital gains annually, increasing current-year taxes.

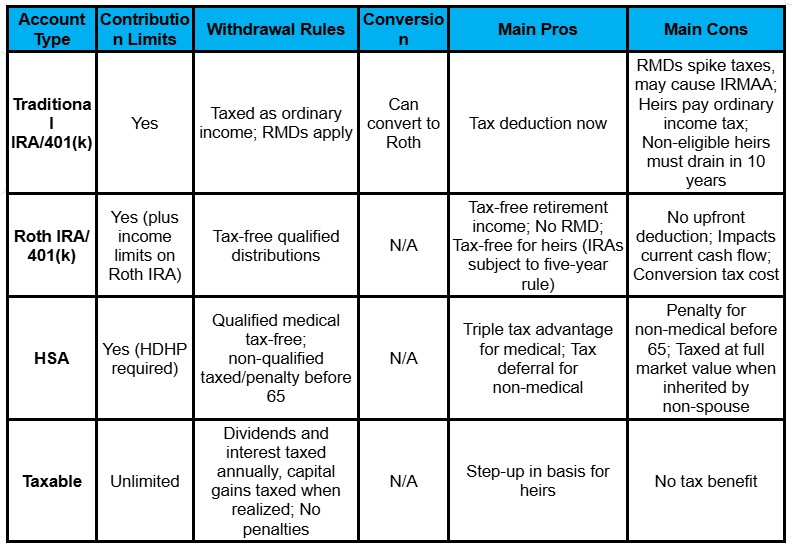

Head-to-Head Comparisons

Here’s a quick summary of the four account types with their pros and cons.

My Personal Math

Numbers clarify trade-offs better than theory. Here’s how the math worked in our case.

Whenever I had an HDHP, I maxed out our HSA contributions.

Beyond that, I maxed out our traditional, tax-deferred contributions to the best of our ability, given our cash flow each year.

Let’s see how that math works when your contribution is limited by cash flow. Say you can set aside $3,350 a year and pay a total marginal tax rate of 30%. That translates to contributing $5000 into your HSA or traditional retirement account and getting a tax deduction worth $1,500, or putting $3,500 into a Roth or into your taxable account.

- Putting $5,000 in an HSA: Fits within your after-tax cash flow, grows tax-free, and allows tax-free withdrawals for qualified health expenses. Assuming 7% real (inflation-adjusted) return, you’ll have about $10,000 in 10 years, all of which is accessible for use.

- Putting $5,000 into a traditional retirement account: Fits within your after-tax cash flow, grows tax-deferred, and allows penalty-free withdrawals after age 59½ (some exceptions allow earlier penalty-free withdrawals). Assuming 7% real (inflation-adjusted) return, you’ll have about $10,000 in 10 years, but if you’re still paying 30% marginal tax rate, only $7,000 is accessible for use.

- Putting $3,500 into a Roth account: Fits within your after-tax cash flow, grows tax-free, and allows tax-free withdrawals once the account is at least five years old and you’re 59½ (contributions can be withdrawn earlier). Assuming 7% real (inflation-adjusted) return, you’ll also have about $7,000 in 10 years, all of which is accessible for use.

- Putting $3,500 into a taxable account: Fits within your after-tax cash flow, dividends and interest are taxed annually, and capital gains are taxed when realized. Realized long-term capital gains are taxed at preferred rates (0%, 15%, or 20%, depending on your taxable income). Assuming 7% real (inflation-adjusted) return, you’ll have less than $7,000 in 10 years (if you had to pay annual income taxes from dividends and interest income), and the accessible amount is even lower due to taxes on realized capital gains.

Had we not been limited by cash flow, maxing out Roth contributions would have provided more retirement income than traditional retirement accounts. Had we made the contributions to a traditional account and used the tax benefit to fund a taxable investment, the difference would shrink, but not disappear.

From the perspective of eventual heirs, we need to drain our HSA before touching our Roth accounts, and preferably before draining our tax-deferred accounts. Once the HSA is drained, we should drain as much as possible of our tax-deferred accounts before draining our taxable portfolio.

However, I don’t plan to let the bequest tail wag the retirement-income/tax dog. Accordingly, we will use our HSA in years when our taxable income is higher, and when we have little taxable income, we’ll “fill” the 12% federal tax bracket by converting a portion of our tax-deferred balance into a Roth account.

More General Math

Pre-retirees need to balance their priorities and risks. These include:

- Current marginal tax rate (federal, state, and local).

- Expected marginal tax rate in retirement, especially once RMDs hit.

- IRMAA risk, especially once RMDs start growing.

- Estate goals.

- Current liquidity needs.

Your winning option depends on your priorities and which risks most concern you.

If your top priority is maximizing after-tax retirement income, your winning strategy is maximizing HSA contributions, if you’re eligible, up to the point where your balance is more than you’re likely to spend on qualified healthcare expenses during your lifetime.

Next, if your tax rate in retirement is likely to be equal to or higher than your current rate, Roth accounts win. If not, traditional retirement accounts are better.

If your top priority is managing RMD risk and/or funding healthcare costs, HSAs are once again your top winner, followed by Roth accounts and a taxable portfolio.

For the greatest flexibility, a taxable portfolio is your best bet.

If your priority is ensuring your heirs get the biggest benefit, Roth accounts are the clear winners, followed by traditional retirement accounts.

In short, If all else is equal and used optimally:

- HSA wins for healthcare dollars.

- Roth wins for legacy (e.g., $1 million inherited by non-spouse taxed at a total 33% rate in a traditional IRA is worth $670k vs. $1 million in a Roth is worth $1 million) and RMD control.

- Traditional wins if current tax rate > retirement tax rate.

- Taxable wins for flexibility.

Interesting Takes from the Pros

I asked several financial advisors for how they advise their clients, and the biggest mistakes they see people making when saving for retirement. Here’s what they had to say.

Alex Bridges, CFP®, ChFC®, RICP®, Wealth Advisor, Tiverton Wealth, says, “Because every financial plan is as unique as a fingerprint, account selection is never a generic exercise; it requires balancing current tax liabilities with future flexibility. I frame this decision for clients through the lens of Tax Diversification.

“For young professionals just starting, we aggressively favor the Roth side of the equation, Roth IRAs, Roth 401(k)s, and Roth 403(b)s. In lower early-career tax brackets, the upfront tax deduction of a traditional account is less valuable, whereas decades of tax-free compounding growth are incredibly powerful. However, as clients enter their peak earning years, the strategy shifts. We start balancing the need for immediate tax relief via pre-tax deferrals with the necessity of future tax flexibility.

“For our small-business-owner clients, this often involves layering bespoke retirement plans, like pairing a Safe Harbor 401(k) with a Cash Balance Plan, to maximize their personal tax deductions while simultaneously structuring beneficial retention incentives for their employees. Ultimately, my goal is to ensure a client never reaches retirement with all their eggs in one tax basket.

“We aim to build a ‘three bucket’ strategy: tax-deferred via traditional 401(k)/IRA, tax-free via Roth accounts, and after-tax in taxable brokerage accounts. A perfect real-world example of this synergy is an employee who contributes their own money to a Roth 401(k), receives their employer’s matching funds in a pre-tax bucket, and systematically funds a taxable brokerage account on the side. This triangulation gives us ultimate control over their tax destiny in retirement.

“The single most pervasive mistake I see is tax concentration, which is arriving at retirement with entirely one type of tax asset. I often work with highly successful professionals, such as retired attorneys, who accumulated massive wealth. Often, they own their homes outright and have multi-million-dollar balances sitting entirely in pre-tax IRAs.

“On paper, they are wealthy, but functionally, they are trapped, because every single dollar they withdraw is taxed as ordinary income, so they have zero control over their retirement tax bracket. This lack of tax diversification can trigger a ‘tax torpedo,’ exposing them to massive RMDs, higher taxes on their Social Security benefits, and steep Medicare IRMAA surcharges.

“Conversely, while many advisors preach that ‘all Roth is perfect,’ overconcentration in Roth accounts presents its own set of challenges, particularly for early retirees. If you want to retire at 50, having 100% of your assets tied up in pre-tax or Roth accounts usually means navigating restrictive IRS rules and potential 10% penalties to access earnings before age 59½.

“This leads to what I consider the most underrated retirement vehicle: the after-tax taxable brokerage account. There is a lot of noise in the industry dismissing taxable accounts for retirement savings, but I view them as the ultimate ‘bridge account.’

“If you have a healthy after-tax portfolio, you can retire at whatever age you choose. There are no age restrictions, no early withdrawal penalties, and the funds are subject to highly favorable long-term capital gains tax rates rather than ordinary income rates. Failing to build this after-tax bridge is the biggest missed opportunity for anyone dreaming of financial independence before age 60.”

Anthony Ferraiolo, CFP®, Partner Advisor at AdvicePeriod, agrees and expands, “As pointed out above, the best account type is really a combination of many. It’s not uncommon for clients to tell me they wish they had more money in their Roth IRAs or HSAs, but Roth IRAs debuted in 1998 and HSAs in 2003. I tell them that if all their money was in Roth accounts, they probably would have missed some tax-arbitrage opportunities during their working years.

“However, I think HSAs provide some good mental accounting benefits in addition to their tax benefits. It’s a lot easier to stomach a $5K dental bill in retirement when you have a tax-free bucket to tap.

“During all these conversations, I often feel that the plain old regular taxable account gets the least love but is one of the most flexible tools for your accumulation and retirement years. There are really only two cons to the taxable account: no tax benefit, and taxes on interest and dividends along the way.

“However, the latter is an overblown concern, and there is a minor tax benefit that may come into place. I say the latter is overblown because with a proper account structure, with the inclusion of municipal bonds or municipal bond funds, most of your bond allocation’s income can be tax-exempt, so there’s little to no carrying cost for bonds. This is important because in most people’s retirement, if they retire before they can claim Social Security benefits, they may tap their taxable portfolio’s bonds for more stable distributions.

“Next, you have tax-efficient ETFs. Nowadays, you can even find low-to-no-dividend ETFs for your favorite indices or prioritize growth stocks or US stocks, which could have lower yields than their international counterparts. These accounts have the most flexibility, no contribution limits, age limits, penalties, etc., so when ‘life happens’ you don’t need to worry about the tax hit too.

“The hidden tax benefit is twofold when you invest cash during a high-yield environment vs. keeping it in a high-yield savings account, you can reduce the tax hit from your assets.

“Similarly, if you need $50k from your portfolio, you may only need to pay capital gains on a fraction of that amount, and in some cases, that can be at the 0% tax bracket. It always depends, but I don’t think the regular taxable account gets enough credit for its Swiss-Army-Knife-like character.

“The biggest challenge with the taxable account is that it doesn’t, by default, have automations connected to your paycheck, like your 401(k) or HSA, which means it takes intention to build up this account. So, while the tax benefits are attractive compared to the other accounts, the regular taxable account remains a bit underrated in my view.”

Ben Simerly, CFP®, Founder and Financial Advisor of Lakehouse Family Wealth, rounds out the conversation, “First, adding to the 401(k) discussion above, there are technically annual compensation limits to 401k accounts, including pre-tax dollars. This does not factually change the outcome because of the contribution limits themselves, but I have seen it impact those with unique plan contribution percentage rules and higher incomes.

“Also, since these conversations often affect families looking into trusts, you should note that the above-mentioned rules can be significantly affected by the use of trusts, both for the owner of the assets, and those inheriting them.

“Account type questions are some of the most common ones we receive. There are two sets of answers. The first is technical: what fits the client according to the math? The second set of answers addresses the emotional aspect. What helps the client feel most comfortable?

“More often than not, it’s the client’s comfort level with a given path that helps find the answer that’s best for them. From a math perspective, the biggest mistake we see is looking at the account-type choice based on current tax return savings. Choosing a pre-tax 401(k), for example, may reduce current taxable income. But what’s the effect of choosing a pre-tax 401(k) vs. a Roth or after-tax 401k sub-account on lifetime taxation and lifetime income from investments?

“Often, a significant decrease in current taxes can create a significant decrease in retirement income. The other major factor on the math side is legacy. If an account type being considered will be primarily used for legacy to children or non-profit donations, it can completely change the math of the situation.

“From the emotional perspective, the number one question is this: would you rather pay taxes later when you are unsure of your ability to work or make up the difference? Or would you rather pay the taxes now while you’re able to work, likely have more control over your life and ability to work, and a choice over your investments?

“Once someone nears retirement, choices decrease. Once someone retires, they decrease further. Whether it’s from IRMAA bracket considerations, RMDs, or a potential future disability, we may not always have the same choices in the future that we have now.

“More often than not, our clients choose to focus on Roth, or after-tax, contributions to pay more of the taxes now while they have more control. We love the benefits of Roth accounts and the after-tax growth. Especially with the length of modern retirements. But taxation relative to ability to work decides more cases than any other single factor we’ve encountered.”

The Bottom Line

So, did I make a mistake that will come back to haunt me?

Tentatively, my answer is that I didn’t.

True, having such a concentrated bet on tax-deferred accounts does reduce our flexibility in any specific year. For example, anytime we have an especially high spend in retirement, we’ll need to account for the higher taxes we’ll be hit with.

However, while I didn’t dig in deeply enough ahead of time to make the most informed choices, overall, I don’t regret what we did because it ended up allowing us to make the most of what our cash flow allowed us to set aside.

More generally, what I learned is that there is no perfect account type. There is only a tax structure that fits your stage of life, and managing your tax brackets over time. And the earlier you understand the trade-offs, the fewer regrets you’ll suffer.

However, always keep in mind that the US tax code changes often, sometimes dramatically, and all the above assumes things will mostly stay as they currently are. But that’s the best we can do without a functioning crystal ball.

In the end, the real winner isn’t one account type, but rather tax diversification across the account types that fit your priorities.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor