Managing money as a couple is one of the most important things you can do for your relationship and your financial future. Yet most couples rarely sit down together to actually talk about it in a structured way. Life gets busy, conversations get avoided, and before long, financial stress starts to quietly build beneath the surface.

That’s where the money date comes in.

A money date is a scheduled, intentional time you set aside with your partner to review your finances together. It doesn’t have to be long or complicated. In fact, the simpler you keep it, the more likely you are to actually do it. Once a month is a good rhythm for most couples, though some prefer every two weeks, especially when working toward a specific goal.

Couples who regularly discuss money report higher relationship satisfaction and better financial health. This is why regular money dates can be so valuable for your relationship.

The goal isn’t to audit each other or assign blame. It’s to stay connected to your shared financial picture so you can make decisions together, reduce surprises, and work toward the things that actually matter to you as a team.

Here’s a checklist you can work through together at every money date.

Your Monthly Money Date Checklist

Review Last Month’s Spending Together

Start by pulling up your spending from the past month. This could be your budgeting app, a spreadsheet, your bank account, or your credit card statements. The format doesn’t matter as much as actually looking at the numbers together.

The point here isn’t to critique every purchase. It’s to get an honest picture of where your money went. Did spending align with what you both value? Were there any surprises? Did any categories run higher than expected?

This is also a good time to notice patterns. If dining out keeps coming in over budget, that’s useful information. Maybe the budget needs to be adjusted, or maybe it’s a signal to be more intentional. Either way, you’re making that decision together instead of one person silently stewing about it.

Keep this part of the conversation neutral and curious, not accusatory. You’re reviewing data, not assigning fault.

Check Progress on Shared Savings Goals

Whether you’re saving for a vacation, a home down payment, a new car, or an emergency fund, your money date is the time to check in on how those goals are progressing.

Pull up the balance in whatever account you’re using for each goal. Compare it to where you expected to be by now. If you’re on track, great. If you’ve fallen behind, you can talk about why and decide if you want to adjust your contribution or your timeline.

Having a visual tracker for savings goals can make this part of the conversation more motivating. Watching a number grow, even slowly, reinforces that your efforts are adding up.

If you don’t have shared savings goals yet, this is also a good time to start defining them. What are the two or three things you’re both most excited to save toward in the next year? Getting specific about goals makes it much easier to stay committed to them.

Identify Upcoming Big Expenses for Next Month

Take a few minutes to think through what’s coming up financially in the next 30 days. Are there any irregular or larger-than-usual expenses on the horizon?

This might include things like:

A car registration or annual insurance premium

A birthday or anniversary gift

Planned home maintenance or a repair

A school event or activity fee

Travel or a hotel for a trip you’ve already booked

Flagging these ahead of time helps you plan for them rather than getting caught off guard. It also gives you a chance to decide together how you’ll cover them, whether that’s from a sinking fund, from discretionary spending, or by temporarily cutting back somewhere else.

This step alone can eliminate a significant amount of financial stress. Most financial surprises aren’t truly surprises. They’re just expenses that weren’t planned for in advance.

Discuss One Financial Win Each Person Had Since the Last Date

This one might feel a little uncomfortable at first, especially if you’re not used to celebrating financial progress. But it matters.

Each person shares one thing they feel good about financially from the past month. It doesn’t have to be dramatic. Maybe you resisted an impulse purchase, automated a savings transfer, increased your 401(k) contribution, negotiated a lower rate on a subscription, or finally called to dispute a charge you’d been putting off.

Acknowledging progress, even small progress, builds positive momentum. It also helps reinforce that both people in the relationship are making an effort, which strengthens trust and keeps the financial conversation from feeling like it’s only about problems.

This part of the money date sets a constructive tone and reminds you both that you’re on the same team.

Confirm All Bills Are Paid or Scheduled

This is the unsexy but important housekeeping portion of the money date.

Go through your regular monthly bills and confirm that everything is either paid or scheduled. This includes utilities, rent or mortgage, subscriptions, loan payments, insurance premiums, and anything else that hits your accounts regularly.

If you have bills set to autopay, verify that the payment amounts look right and that there’s enough in the account to cover them. Autopay is convenient, but it can also lead to surprises if a rate changes or a payment processes at an unexpected time.

This step only takes a few minutes, but catching a missed payment or an unexpected charge during your money date is a lot less stressful than catching it after a late fee or an overdraft.

Review Debt Payoff Progress

If you’re currently paying down debt, whether that’s credit cards, student loans, a car loan, or anything else, your money date is a good time to check in on where things stand.

Look at the current balances and compare them to last month. Are they going down? Is the payoff strategy still the one you both agreed on? Are there any opportunities to accelerate payoff, like applying a bonus, a tax refund, or some extra cash flow toward a balance?

Watching debt balances decrease can be genuinely motivating, and celebrating that progress together makes the effort feel worth it.

If debt isn’t currently part of your picture, you can skip this step or use the time to talk about your strategy for staying debt-free going forward.

Ask: “Is There Anything Money-Related Causing You Stress Right Now?”

This is arguably the most important item on the list, and the one most couples skip.

Financial stress rarely announces itself clearly. More often, it shows up as irritability, avoidance, or tension that seems unrelated to money but usually isn’t. Giving each person a direct, low-pressure opportunity to name what’s worrying them can prevent a lot of that from building up.

The question is simple: Is there anything money-related causing you stress right now?

Maybe one person is anxious about job security. Maybe there’s a financial decision coming up that feels overwhelming. Maybe someone has been avoiding opening a certain account because they’re afraid of what they’ll see. Whatever it is, this question creates a safe opening to bring it into the conversation instead of carrying it alone.

You don’t have to solve everything in the money date. Sometimes just naming a concern out loud to your partner is enough to take the edge off it. And sometimes, it opens a conversation that leads to a plan.

A Few Tips for Making Your Money Date Work

You don’t need to make this elaborate. Some couples do their money date over brunch on a Sunday morning. Others do it over dinner on a weeknight. Some keep it to 20 minutes, others go longer. The format is flexible.

What matters is that it’s consistent and intentional. Put it on the calendar like any other commitment. Protect the time. And agree in advance to keep the conversation constructive.

If you and your partner are just getting started with money dates, it’s okay if the first few feel a little awkward. That’s normal. Financial conversations can carry a lot of emotional weight, especially if you’ve had conflict around money in the past. The structure of a checklist actually helps here because it gives you something concrete to focus on instead of letting the conversation drift into old patterns.

Over time, the money date becomes something most couples genuinely appreciate. It removes the guesswork from your finances, reduces conflict, and helps you feel like a real team when it comes to building the life you want together.

Financial stress in relationships often comes not from lack of money but from lack of communication. The money date is a practical way to change that.

By setting aside a small amount of time each month to review your spending, track your goals, look ahead, celebrate progress, and check in emotionally, you build the kind of financial partnership that makes everything else easier.

You don’t have to be perfect at it. You just have to show up.

Frequently Asked Questions About Money Dates

How long should a money date actually take?

For most couples, 15 to 30 minutes is a reasonable target. If you’re just starting out, your first few sessions might run longer as you set up systems and get comfortable with the format. Once you’ve established a rhythm and your finances are organized, many couples find they can get through the checklist in 10 to 15 minutes. The goal isn’t to spend hours on it. It’s to be consistent.

What if one partner is more interested in finances than the other?

This is extremely common. One person in most relationships tends to be the “money person,” and the other is less engaged. The money date helps bridge that gap because it creates a regular, low-stakes opportunity for the less financially engaged partner to stay informed without having to manage everything day to day.

Keep the conversation accessible. Avoid jargon. And remember that engagement usually grows over time once the less interested partner starts to see the value in staying connected to the financial picture.

Should we combine our finances before starting money dates?

That said, if you’re not sure what approach to take with your accounts, a money date is actually a great time to have that conversation.

What if our money date turns into an argument?

It happens, especially in the beginning. Money is emotional, and old tensions can surface when you start talking about it openly. A few things that help: agree on ground rules before you start, such as no blame and no bringing up past mistakes. Stick to the checklist so the conversation stays focused on information rather than grievances. And if things get heated, it’s okay to pause and come back to it later.

The goal is progress, not perfection. If financial conflict is a recurring and serious issue in your relationship, working with a couples therapist or a financial therapist can be genuinely helpful.

Do we need a budgeting app or special software to do this?

No. A shared spreadsheet, a notes app, or even paper works fine. What matters is that you both have access to the same information during your money date. If you don’t already have a system for tracking spending, a money date is a good time to decide together what tool you want to use going forward. But don’t let the lack of a perfect system stop you from starting. You can always refine your tools as you go.

How do we handle it if one partner earns significantly more than the other?

Income differences can create subtle power imbalances in financial conversations if you’re not careful. The key is to approach the money date as a conversation between equals regardless of who earns what. Both people’s perspectives, concerns, and goals deserve equal weight. If income disparity is creating real tension around spending, saving, or decision-making authority, that’s worth addressing directly, either in your money dates or with the help of a financial advisor or therapist who can help you build a structure that feels fair to both of you.

What if we have very different financial personalities?

One person might be a natural saver, while the other tends to spend more freely. One might be comfortable with financial risk while the other prefers security. These differences are common and don’t have to be a problem. In fact, they can balance each other out.

The money date creates a regular space to acknowledge those differences, understand where the other person is coming from, and find a middle ground that works for both of you. The structure of the checklist helps keep the conversation grounded in shared goals rather than personal habits.

When is a good time to start doing money dates?

Now. There’s no financial milestone you need to hit first. You don’t need to be debt-free, fully employed, or have a certain amount saved. Money dates are useful at every stage of a financial journey, whether you’re just starting out, actively building wealth, or navigating a financial challenge.

The earlier you establish the habit, the more natural it becomes. And if you’ve been together for years without ever having a structured financial conversation, it’s still not too late. Starting now is always better than waiting for the perfect moment.

Find financial advisors in Biloxi, Mississippi ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Biloxi for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Biloxi featured on Wealthtender you may want to add to your shortlist.

Featured Biloxi Financial Advisors

As you prepare to interview financial advisors in Biloxi who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Biloxi

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Biloxi.

The Benefits of Hiring a Financial Advisor in Biloxi

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Biloxi, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Biloxi? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Biloxi Financial Advisor

Before hiring a financial advisor in Biloxi, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

If you live in Maryland, you’re already paying some of the highest taxes in the country, but chances are, you’re paying even more than you have to. Most residents only think about taxes when it’s already too late to do anything about them: at filing time, when the decisions are already made and the opportunities are gone. The good news? With the right deductions, credits, and a little proactive planning throughout the year, you could keep thousands more of your hard-earned dollars. Here are 10 strategies to legally reduce your Maryland state and local income taxes, and why starting now matters more than you think.

I’ve been a Marylander for almost 30 years. Although I’ve lived on three continents (four, if you count a couple of months in Antarctica), in three countries, and in two US states, I’ve lived here longer than anywhere else.

There’s a lot to love about Maryland. Just look at the photo below, taken not far from my home, and you’ll start to see why:

Maryland autumn, 2022. Photo by the author.

However, the tax burden isn’t one of the things I love about my home state.

According to the Tax Foundation, Maryland has the 11th-highest per-capita tax burden in the country, about 13% above the U.S. average (based on 2022 data).

As Ben Simerly, CFP®, Financial Advisor and Founder of Lakehouse Family Wealth and former Marylander, says, “Maryland has literally become famous for unique and destructive taxes. To my knowledge, it’s the first state or territory, or in some cases one of the few, to tax the rain, provide more than a dozen forms of property taxes, and even tax money at the state level both at the time of death and inheritance.

“For some, living in Maryland isn’t optional. Many federal workers and military personnel and their families are required to live and work in the region. If this is you, make the best of the situation. You may not get hazard pay like you would in earlier days of government service in the region, but with some help from pros, you can lessen the ill effects on your finances.

“Here are our top areas of tax concern in Maryland. First, Maryland has its own particularly vindictive capital gains tax, despite gains already being taxed under several other state and federal codes.

“It applies an extra 2% capital gains tax mainly on households with federal Adjusted Gross Income (AGI) above $350,000.Even if your household doesn’t normally make over $350,000, your AGI could get ‘bumped’ over $350k due to, e.g., receiving a large bonus; selling a house that appreciated too much; moving financial assets between account types that causes a taxable event; owning shares in mutual funds that distribute significant capital gains, dividends, and interest; etc. These can all trigger a ‘capital gains’ trap, which happens far more easily than you might think.

“Second is additional death and estate taxes. Maryland levies a 10% tax on inheritance to the beneficiary, even if the money was taxed at the benefactor’s death. That’s right, it taxes the money yet again. And that’s after the also unique state inheritance tax of between 8% and 16% on estates with a gross value of $5 million.

“There are look-back clauses too, meaning you can’t simply move to avoid the tax; you have to move long enough before death or inheritance to avoid the tax. States like Maryland, New York, and California will follow you around the world to collect taxes from you and take you to court or send agents if it goes that far.

“My retirement planning work with Maryland clients over the years shows that most could retire 10 years sooner and have dramatically higher retirement income outside of Maryland, largely due to the benefits of rollovers occurring outside of the state.

“So, for Maryland residents, we often plan out income for even young families the way you normally only would for someone approaching Medicare age or already retired. We do everything we can to keep income under certain thresholds and then get the resident out of Maryland as soon as humanly possible.”

If I had to, I’d bet a nickel (assuming I can still find one in these digital times) that many Marylanders overpay their taxes. Not because they’re careless, but because they start thinking about it too late.

If you’re a higher-income Maryland resident, that can mean paying several thousand dollars in higher taxes per year than you’re legally required to. And once that money is gone, you don’t get it back.

By the time you’re filing your tax return, your tax liability is already set. At that point, your income is already set, your deductions and credits have already been earned (or not), and most opportunities to reduce your tax bill are behind you.

At that point, it’s mostly a question of how well you (or your tax software) identify the deductions and credits you’re eligible for.

That’s why if you want to reduce your Maryland taxes, filing better is a secondary priority. Your top priority should be to focus on better tax planning and strategy.

Three Types of Tax-Reducing Moves for Maryland Residents

There are only three legal ways to pay lower income tax.

Lower your taxable income, ideally without reducing your standard of living (e.g., by using more and larger deductions).

Take advantage of all tax credits for which you qualify.

Make smarter timing and structural decisions.

Many taxpayers focus on the first, but still miss some opportunities, take partial advantage of the second, and almost entirely miss the third.

That’s why, even if they do everything perfectly at tax-filing time, they end up paying more than they could have.

The following are 10 tips for reducing your Maryland state and local income taxes. Some are straightforward. Others require a bit of planning. Most are easier to implement before the tax year is over.

You don’t have to use all 10, but the more you miss, the more of your hard-earned money you’ll leave on the table.

Lower Your Taxable Income

If you ask most people, this is what they’ll identify as a good way to reduce their taxes.

It’s natural. It’s the most straightforward way to reduce taxes.

But there’s a catch.

There’s using this lever, and then there’s USING it.

The former means contributing whatever you feel you can to your traditional retirement plans, using the standard deduction, and letting things flow as they will over the years.

This leaves lots of opportunities on the table, unused.

The latter requires being more proactive and committed.

Here are the top three examples.

1. Maximize Pre-Tax Retirement Contributions

If you can’t afford to maximize your retirement contributions without counting on the tax deduction, and especially if you’re already in a high tax bracket, this may be your best bet.

Not only does it reduce your federal taxable income, but it also reduces your taxable income for Maryland state and local taxes.

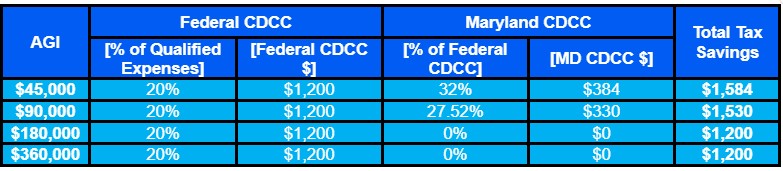

Table 1 shows some examples of how much you can lower your 2026 income taxes (federal, state, and local) by contributing an extra $10k to your traditional 401(k) account if you file “married filing jointly” and live in, e.g., Howard County, Maryland.

Table 1. Example 2026 tax savings (federal, state, and local) for a married couple living in Howard County, Maryland, by increasing traditional 401(k) contributions by $10k.

Clearly, the majority of the tax savings come from the federal portion, but the state and local tax reduction can go as high as $980, or 0.98% (for residents of Dorchester County with a Maryland taxable income above $1.2 million).

If you’re one of those who don’t max their retirement contributions, this is the simplest and most powerful place to start, but only if you make the contributions before the end of the tax year!

And unlike many strategies, this one is (almost) entirely within your control.

2. Use Maryland’s 529 Deduction as Much as Possible

Maryland has a relatively generous deduction for people who set aside money for their dependents’ (or their own) education.

You can deduct contributions to Maryland 529 plans, up to $2500 per contributor, per beneficiary, per year.

That means that, if you’re married and have two kids, you could potentially deduct up to $20k a year ($5k from you and your spouse per beneficiary, for each of your kids, plus for the two of you).

What’s more, you can carry over excess contributions for up to 10 years.

That means that if you, e.g., open a plan for your child when she’s born, and contribute $5k a year from you and your spouse until your daughter goes to college, then contribute $20k in her freshman year and another $50k during her senior year, all of those contributions can ultimately be deducted.

That’s $160k-worth of deductible contributions spread over 32 years.

Even if you can’t afford to set aside money until your kid goes to college, but you do pay $70k in tuition and other eligible educational expenses during his college career, you can deduct those over the four years of college, plus the following decade.

And the most incredible thing about this deduction, in my opinion, is that you can contribute to the plan, then take the money out the very next day to pay the tuition bill, and it’s still deductible!

And lest we forget, if your kid doesn’t go to college or has such large scholarships that there’s a large balance left over, you can change beneficiaries, or you can use a SECURE 2.0 provision to convert up to $35k of the remaining balance into a Roth IRA for the beneficiary.

Few deductions offer this much flexibility with this much impact.

3. Don’t Blindly Use the Standard Deduction

Despite the significant increase in the federal standard deduction over the past several years, if you own a home with a large mortgage, make significant charitable donations, and perhaps have high medical expenses, itemizing can still reduce your taxable income by more than the standard deduction would.

And the larger your federal deduction, the lower your taxable income for Maryland state and local taxes.

The above three tips are the most visible lever and the one that most people focus on.

But if you stop there, you’re likely missing more powerful opportunities.

Take Full Advantage of Tax Credits

Tax deductions are great. They reduce your taxable income, which reduces your taxes.

But there’s something even better.

Tax Credits.

For every $1 of tax deductions, your Maryland state and local taxes drop by about $0.08. But for every $1 of Maryland tax credits, your Maryland state and local taxes drop by a full $1!

If deductions are about trimming around the edges, credits are where meaningful reductions often happen.

The only problem is that, while more valuable from a tax reduction perspective, credits are far more tightly targeted.

Maryland offers quite a few such tax credits. The problem is that most middle-to-high earners assume credits don’t apply to them and never take the time to verify that assumption.

Here are a few credits worth checking carefully.

4. Child and Dependent Care Tax Credit

Even if your adjusted gross income is in the 6 figures, Maryland offers a substantial tax credit for child and dependent care expenses.

The Maryland credit amount is figured as a percentage of the federal Child and Dependent Care Credit (CDCC), which can be 20% – 32% of qualified expenses up to $3000 for a single dependent or $6000 for two or more dependents.

That percentage depends on your filing status and your federal AGI. Table 2 shows some examples for couples who file jointly, have two dependents, and paid $6k or more in qualified care expenses.

Table 2. Example 2026 tax savings (federal, state, and local) for a married couple living in Maryland, claiming the CDCC for $6k or more in qualified expenses for two kids.

5. Senior Tax Credit

Maryland offers a tax credit for seniors, even if their federal AGI is up to $150k if married filing jointly or up to $100k if single.

The credit takes up to $1750 off your Maryland tax bill if both spouses are 65 before the end of the tax year. If it’s a single taxpayer, or a couple where only one is 65 by the end of the tax year, the senior tax credit is $1000.

6. First-Time Homebuyer Subtraction

If you and your spouse (if any) are Maryland residents, haven’t owned or purchased a home in the past seven years, and contributed money to a first-time home buyer savings account, you can subtract from your taxes the lower of $5000 or the amount you contributed in the tax year, plus earnings from the account for the tax year.

You can do this for up to 10 years.

The earnings subtracted cannot exceed $50k over the 10 years.

There are caveats.

First, by the end of 15 years from when you open the account, you must use the account balance toward a down payment and/or eligible closing costs for buying a home in Maryland. Any amount not so used counts as taxable income in the following year.

Second, amounts withdrawn from the account for purposes other than eligible first-time home buying expenses count as taxable income for the tax year of the withdrawal and are also subject to a 10% penalty. Three exceptions are rollovers, bankruptcy, and administrative costs charged by the financial institution for the savings account.

Some other possible credits to investigate include:

As mentioned above, don’t simply assume that you make too much to qualify. That just increases your risk of leaving easy money on the table, paying higher taxes than you owe.

Also, you may qualify for certain income-limited credits you wouldn’t normally qualify for in years when your income is lower than usual. This could be due to, e.g.:

Being unemployed or underemployed for part of the year (or, hopefully not, all of it).

Living off withdrawals from a Roth account, taxable portfolio, and/or savings accounts.

Living off untaxable proceeds from the sale of a home or other property.

There’s no doubt that tax credits can be a powerful tool in reducing your Maryland state and local income tax.

But even these aren’t necessarily your biggest tax-cutting opportunity.

That will often result from planning and making optimal timing and strategic decisions.

Strategic Decisions and Timing – Where Planning Shines

As helpful as tax deductions may be, and as powerful as tax credits are, there’s someplace else where the biggest savings often are, and where many people leave the most money on the table.

Some because they prefer not to make the changes that would reduce their state and local taxes by the largest amount, but many others just don’t make the right moves in time.

This is the only category where decisions made months or even years earlier can completely change your tax outcome.

Simerly says, “While most of the available tax credits or deductions for Maryland are automatically asked about or applied by tax software and or accountants, some areas require more advanced planning.”

7. Time Income and Deductions Proactively

You don’t want the tax tail to wag your income dog, but the progressive nature of our tax system lets you reduce your long-term total taxes by avoiding spikes in taxable income that would push you into higher tax brackets.

This is true for federal taxes, but also for Maryland state and local taxes.

For example, if you have an especially high income in a specific year, you can:

Ask to defer at least part of your bonus (if any) to the following tax year.

Avoid realizing capital gains that year, holding off on selling appreciated assets until the following year.

Harvest tax losses by selling assets whose current value is lower than your basis in them.

Bunch charitable contributions into that year from the previous and/or next year.

The crucial thing is to be intentional and make the necessary decisions proactively, when you still have the flexibility to make them.

8. Coordinate Federal and State/Local Tax Decisions Intelligently

A Roth conversion is a plausible long-term tax-reduction and estate-planning strategy.

However, it’s important to consider your short-term taxes, including your Maryland state and local income taxes.

If you’ve decided on a Roth conversion, carry it out during years when you’re in a lower tax bracket.

Similarly, if you’re retired, you may benefit from drawing more out of your tax-deferred retirement accounts in years when your taxable income is otherwise lower than typical.

9. Where You Live Matters

Your Maryland state and local income tax could vary by up to 13% simply because you live in one jurisdiction vs. another.

For example, the local income taxes in Worcester County and Talbott County are relatively low, at 2.25% and 2.40%, respectively. Local tax in Dorchester County is the highest, at 3.30%.

All other counties fall between those extremes, with Anne Arundel and Frederic Counties charging progressive taxes, per taxable income.

In this age of remote work, all other things being equal, you could shave over 1/8 of your Maryland state and local tax by moving from a high-local-tax-rate county to the lowest one.

Crucially, if for some reason the Comptroller of Maryland can’t identify your county of residence, you will be taxed at the highest local tax rate, of 3.30%. So if you live in a county that charges a lower rate, make sure you identify it correctly on your state tax return.

10. Treat Tax Planning as a Year-Round Process

Most people only think about how they can reduce their taxes when it’s mostly too late.

At tax filing.

By then, your income is already earned, your decisions are already implemented, and your tax-reduction opportunities are mostly gone.

If you want to minimize your state and local taxes, you need to do more than file better. You need to plan, decide, and execute earlier.

This means you need to:

Review your situation before year-end (preferably far before that point).

Identify opportunities.

Make adjustments while they can still affect your taxes.

Dr. Steven Crane, Founder of Financial Legacy Builders, shares, “In my experience, the biggest state tax wins usually come from decisions around income timing and where income shows up. Maryland has relatively high state and local taxes, so things like Roth conversions, retirement withdrawals, and even where assets are held can make a noticeable difference. I’ve worked with clients who didn’t realize that simply shifting how and when they recognize income could save them thousands over time.

“One of the biggest mistakes I see is people treating state taxes as an afterthought. They focus on federal planning but ignore how state and local taxes stack on top of that. Another common issue is not coordinating decisions; someone might take a large distribution, sell assets, or exercise stock options without realizing the full state tax impact until it’s too late.”

The Bottom Line for Maryland Residents

If you’re a Maryland resident, especially one paying relatively high state and local income taxes, your biggest-impact tax-reduction strategy isn’t to find a single large tax break you somehow missed all these years.

It’s to identify and take advantage of all the deductions you’re legally allowed to take, claim all the tax credits you’re eligible for, and most crucially, make proactive choices before the end of the tax year, when they can still reduce your taxes.

The goal isn’t to find one big tax break. It’s to avoid small inefficiencies that add up over time.

Crane agrees, “The biggest thing I wish people understood is that tax planning isn’t something you do in April. By then, most of the decisions are already locked in. The real opportunities happen during the year, when you still have flexibility to control income, deductions, and timing. At the end of the day, reducing state taxes isn’t about finding one big trick. It’s about being intentional with how your financial life is structured and making small decisions that add up over time.”

You may already be implementing some of the above tips.

But it’s a good bet that you’re missing one or more and overpaying your taxes, year after year, as a result.

To reduce your Maryland state and local taxes as much as legally possible, identify the tips you’re missing and implement them as soon as possible.

The earlier you start, the more options you’ll have.

And the more options you identify and take advantage of, the more control you’ll have over how much of your money you’ll get to keep.

If you consider yourself financially disciplined, this is one area where that discipline can pay off directly. Because when it comes to taxes, the difference between ‘good enough’ and ‘well planned’ can mean thousands of dollars a year back in your pocket.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

You’ve hit $1 million… now what? That milestone puts you ahead of most Americans your age, but it also changes the game in ways you might not expect. The biggest risk is no longer saving too little; it’s making less-than-optimal decisions with what you’ve built. So should you stick with the DIY approach that got you here, or is it time to bring in professional help? The answer isn’t as simple as your net worth. Here are nine signs you’d benefit from a financial advisor, and five signs you’re doing just fine on your own.

Hitting $1 million is a big milestone, and one worth celebrating. You’re ahead of roughly three out of four Americans your age. But unless you’re comfortable with a modest retirement budget, think around the median U.S. household income, you need to keep building.

But now that you’re “worth” seven figures, the game changes in ways you may not expect. At this point, the biggest risk is no longer saving too little. You’ve already proven you can save and invest. It’s making less-than-optimal decisions with what you’ve built and will keep building, and, without realizing it, giving up hundreds of thousands of dollars over time. Money that could let you retire earlier and/or live better once you do.

That’s why it’s worth stepping back and asking the question differently:

Is your best move to stay the DIY course, or would you do even better with professional support?

Things That Could Be Costing You Sleep

If you’ve crossed the $1 million mark, you might be asking yourself:

I’ve done well, but will staying solo get me to the finish line, or am I at the point where DIY stops being enough? In other words, isn’t this a case of “if it ain’t broke, don’t fix it”?

Am I leaving money on the table by not using an advisor? Am I being penny-wise and pound-foolish?

I don’t want to pay 1% unless it’s actually worth it. Is it?

What does a good advisor actually do that I can’t do, or do as well, on my own?

I don’t want to get sold things I don’t need. How do I avoid being pitched products and investments that benefit the advisor more than me?

These are all excellent questions. And not the kind you want to leave unanswered.

That’s exactly what we’ll walk through here.

The Core Question Isn’t What You Think It Is

Now that you’ve saved $1 million, do you really need a financial advisor?

It seems like a simple yes/no kind of question, right?

Unfortunately, it runs afoul of something Albert Einstein warned us: “Every problem should be simplified as far as possible, but no further!”

Posing this as a “Do you or don’t you?” question oversimplifies the issue to the point that it sets you up to get it wrong.

Because the answer isn’t based on a single number, even if it’s relatively large, like $1 million. Lots of people with more than $1 million manage just fine on their own. I did, for many years. At the same time, many people, even with less than $1 million, would benefit from professional advice.

The question isn’t if you could do it on your own. You’ve already proven that you can.

The better question is this: Would hiring the right financial pro help you do better than you could on your own?

In other words, which approach gives you the best fee-adjusted outcome, financially and behaviorally?

A Quick Way to Think About It

Before we go deeper, here’s a simple way to frame it.

You’re more likely to benefit from working with a financial advisor if:

Your financial life is getting more complicated, especially around taxes (hello 150-page tax return! Am I being tax efficient?), retirement planning (I need to plan to what age?! Is the 4% rule the best strategy?), or other major decisions (think providing for special-needs kids, negotiating a compensation package, etc.).

You’re not certain you’re optimizing what you’ve built.

You’d rather not manage every detail yourself or worry about missing something important, and worse, setting your spouse up for an unmanageable scenario if you die first.

You’re more likely to be fine on your own if:

Your finances are relatively straightforward (think W2 wages, renting, investing in low-cost index funds, etc.) , and you may be single with no kids.

You follow a disciplined, low-cost investment approach (e.g., a basket of Exchange-Traded Funds, or ETFs, charging sub-0.1% annual management fees).

You enjoy managing your money and can consistently stay on top of it.

Most people don’t fall cleanly on one side or the other. And even if they do today, they may find themselves changing sides in the future.

And that’s the point.

How to Use What Follows

This isn’t about checking off a bunch of boxes on a checklist and calling it a day.

Most people who can benefit from professional financial advisors don’t have just one reason for it. They typically see themselves in several of the “yes-side” items we’ll cover below.

So, as you keep reading, rather than asking yourself if you match all of them perfectly, ask yourself if you’re closer to “yes” than “no” for enough of them.

That will make your personal answer clearer.

With that in mind, we’ll walk through the signs that suggest you might benefit from professional advice, starting with those that tend to have the biggest long-term impact.

Nine Signs You Might Benefit from Working with a Financial Advisor

There are several common scenarios where professional advice can make the biggest difference, where things gradually become more complex, and mistakes become more costly.

1. Complicated tax situations

Early on, your tax situation was likely simple.

You had W2 income, took the standard deduction, and perhaps funded a traditional IRA and/or a pre-tax 401(k) account.

But now, with over $1 million in net worth and the income that helped build it, things stopped being so simple. Most likely, more than one of the following describes your current tax situation:

You own a business (or five) that brings in enough money that self-employment taxes are uncomfortably high.

Your taxable brokerage account generates qualified and unqualified dividends, and both short-term and long-term capital gains.

You have a mix of pre-tax and Roth IRAs and 401(k) accounts, and tapping them each has different tax implications.

You’re starting to hit income phase-outs for Roth contributions and certain deductions (or have long ago passed that marker).

You’re facing a Required Minimum Distribution (RMD) cliff in a couple of decades, so you want to do Roth conversions, but are not sure how much to convert and when.

You’re receiving multiple K-1 forms from different states and/or own properties in more than one state.

You’re thinking of moving to a different state.

Individually, these aren’t too complicated, at least not beyond tax season. But taken together, you have a system where a change in one place affects everything else, and where even small inefficiencies could be costing you thousands or tens of thousands of dollars each year.

For example, it took a while until I learned that electing to have my consulting practice, a sole-member LLC, taxed as an S-corp would save me tens of thousands in self-employment taxes.

It took changing accountants to teach me that.

And if I had had a good financial advisor back then, he or she would likely have suggested making the change a few years earlier.

It may not be flashy like identifying the next Amazon or Nvidia when they’re still small, but a good advisor adds value by coordinating decisions across your entire financial picture.

2. Approaching or entering retirement

I won’t lie.

I’ve been a dyed-in-the-wool personal-finance DIYer for decades.

I reached “work-optional” status and reduced my workload by 90%. I describe myself now as “mostly retired.”

I put together a monster spreadsheet that tracks and projects our finances, revenues, business expenses, personal expenses, estimated taxes, and investment outcomes for the past 12 years and almost forty years into the future. Call me weird, but I enjoy it.

But one thing I’ve never done before is to retire and live off a portfolio. So, I started wondering, how many things are out there that “I don’t know that I don’t know” and that could end up biting me on the rear end?

I tried two flat-fee advisory companies. Both were epic failures.

Then, I found a sort of “family office light” service, where I work with an experienced advisor rather than a different fresh-out advisor each call.

We just kicked things off, so I’ll report on my experience with him in the future. But thus far it’s promising. I especially appreciated his plausibly pushing back on some of the assumptions in my projections spreadsheet that put me at risk of retirement failure in a few decades.

When you’re in the accumulation phase, things are relatively simple. Save (a large enough fraction of your income) consistently, invest for growth, and stay the course. But when the flow reverses? When, instead of feeding your portfolio, you now need it to feed you?

Now you need to figure out:

How much can you safely withdraw each year?

From which accounts should you withdraw money, in what order, and in what proportions, to minimize taxes and maximize your long-term results?

How do you mitigate sequence-of-returns risk? I.e., how do you prevent an early-retirement market crash from eviscerating your retirement plan?

And the real problem is that there isn’t a single “right” answer for everyone.

Your personal answer depends on:

Your mix of taxable, pre-tax, and Roth accounts, and how that mix evolves throughout your retirement.

Your Social Security claim timing.

Your spending needs and how those evolve, especially with any large unplanned expenses that may crop up.

Your legacy desires, and how those might change.

Market conditions for equities, bonds, and other asset classes you may invest in.

Getting things right in all these domains can add to your discretionary spending in retirement, reduce the risk of running out, leave more for heirs and/or charities, and even let you accomplish all these with fewer years of full-time work.

Getting things wrong, or even less optimally, will likely not immediately show up on your radar, but you’ll face a less friendly outcome when it’s too late to do much about it.

3. Dealing with a major life transition or financial event

Every once in a while, something comes up that raises the stakes and/or reduces your margin of error. Things like selling a business, going through a divorce, having to support aging parents or adult children, or, on the more positive side, receiving a major bonus, stock option award, or inheritance.

These aren’t everyday things.

They come with considerations for tax impacts, timing, and hard-to-reverse tradeoffs, and you’re likely dealing with a lot emotionally. Having an experienced, objective advisor can help make decisions that will more likely turn out to your satisfaction.

4. Estate and legacy planning

You’ve hit and exceeded $1 million. That means your financial plan isn’t just about you anymore.

What if something happens to you (and possibly your spouse, too)?

How do you want your assets to be passed on? How can you set that up to minimize your heirs’ red tape nightmare?

You need estate planning, including wills and trusts, designating primary and secondary beneficiaries (I just revisited mine), coordinating accounts, ensuring legal documents are easily found by your heirs, and optimizing taxes on assets you leave behind.

And all this has to be done in a way that will work in real life, not just on paper.

This is where a good financial advisor can help, crafting a comprehensive, coordinated plan that addresses and minimizes complexity and reduces risk.

Having addressed complexity, we move on to how you react when life happens. How do you make the best decisions possible when things go wrong?

And even if you make good decisions, do you lose sleep because you’re not sure they’re the best possible ones?

5. You struggle with market volatility

When the markets keep climbing, everyone’s a genius, long-term investor. But about once every four years, the bear strikes. When it does, it isn’t as easy to stay unemotional and disciplined. The headlines are screaming that the sky is falling, and recency bias makes it look like the red ink will keep flowing indefinitely, so you’re wondering if you shouldn’t cut your losses and sit out the rest of the drop.

When this happens, even if you know a crash is just an opportunity to buy stocks at a discount, it’s beyond difficult to do the right thing, and buy the dip, or at least follow the saying, “Don’t just do something! Stand there!”

Because knowing the right thing to do (or not do) and being emotionally capable of executing it are two completely separate things.

Even smart investors get caught up in the drama and sell at the wrong time, sit on the sidelines in cash way too long because they’re afraid the most recent move back up is a “dead cat bounce,” and even when they do move back in, they chase what’s worked for others recently, which is more than likely no longer the best bet.

This is where a financial advisor’s value can be huge. Not just helping you manage your portfolio, but more importantly, managing your emotional response to what’s happening to it.

6. You stress over your decisions

In today’s financial environment, if your net worth broke through seven figures, there are a lot of decisions to be made, sometimes a few a year, but other times several a day. So you decide and act. But then, you start wondering:

“Does my Roth conversion plan optimize taxes for my heirs and me?”

“Is my portfolio allocation too aggressive, too conservative, or just right?”

“Can I really retire at age X?”

“Does it make sense to buy that vacation home my spouse wants?”

“How much can I donate to our congregation?”

“How much can I give my kid to help with buying a first home?”

“Am I missing something obvious?”

These are all financial decisions, but they’re also deeply emotional.

In extreme cases, you may be losing sleep. I’ll confess, this has happened to me more than once, especially around the decision to mostly retire at age 63.

But even in less extreme cases, you may feel stressed, which isn’t good for your next decision, and even more so for your physical health.

A financial pro can add a pair of knowledgeable eyes, helping you validate your decisions when you pick the best option, catch things you may have missed, and give you confidence in moving forward.

Having a neutral third party can also help keep things calm and constructive when you need to negotiate these decisions with your spouse or kids.

7. You don’t have the time or, frankly, the interest in managing everything

It’s not (just) about picking investments. You’ve done enough of that to reach a net worth higher than most.

But you still need to:

Monitor your investment allocations and rebalance when appropriate.

Manage and optimize taxes, including harvesting tax losses.

Review accounts for unexplained charges or withdrawals.

Make sure your spending aligns with your priorities and stays within your budget.

Stay current with changes in law, rules, and regulations, and how they impact your plan.

You can do all of this, especially if you keep up with financial and tax changes.

However, doing all of it takes time, attention, and emotional bandwidth. You may miss something important. And even if you don’t, it still takes time and energy away from the rest of your life. What’s more, you may simply not enjoy doing it.

I mean, I enjoy reading about the markets, optimizing our portfolio, and especially running multi-decade projections (I told you, I’m weird!)

But I very much doubt you’re that weird.

And if you don’t enjoy it, having to do it adds to your everyday stress, and adds to your “to-do list” things that feel like nagging chores. And if you’re like me, things that feel like that get put off until you can’t put them off anymore.

And by the time you get to them, they’re no longer just important. They’re urgent too. And you may not have enough time to address them well.

And you may also miss something from time to time, and over time, small missed actions can compound into major missed opportunities.

If this sounds like you, wouldn’t outsourcing these things improve not just your outcomes, but also your quality of life?

Would you rather spend the time and energy on tracking everything and optimizing your finances, or delegate as much as possible to a professional advisor so you can concentrate on work/business, family, friends, health and fitness, hobbies, and travel?

8. You’ve become a single point of financial failure

Even if you have everything down to a science, with systems in place to keep everything humming along, what happens if, heavens forbid, you get hit by the proverbial bus?

Could your spouse step in without missing a beat? Could even your kids step in and help your spouse without anything important being dropped?

This is something I’ve been pondering a lot, especially in recent years, after hitting age 60.

And my answer is still, “Not really.”

Frankly, that’s scary. And it’s another reason to have a financial advisor’s support. Our advisor can help by providing continuity of decision-making, serving as a resource to negotiate a painful time, and helping ensure my plan continues providing for my wife.

9. You want to do better than just “fine”

You’ve already shown you can do just fine as a DIYer.

But what if “fine” isn’t enough?

What if you want things optimized so you aren’t leaving money on the proverbial table?

A good advisor can help you optimize, structure things more efficiently, find smarter and easier ways of reaching your goals, and have all that happen without increasing the load on you.

Things like optimal tax efficiency, safe withdrawal strategies that let you spend more in retirement without increased risk of running out, and allocating assets so your returns can cover your expenses, inflation, and a bit extra for growth.

These are all signs that hiring a financial advisor may benefit you.

But that’s not the case for everyone.

Next, let’s look at who, having hit $1 million, would do just as well without paying an advisor.

Five Signs You’re Likely Fine on Your Own

The above 9 signals all point in the same direction – getting an advisor can be helpful and very much worth it.

But in many cases, the opposite may be true.

Plenty of people have reached seven figures and are perfectly capable of continuing the DIY path, saving significant money in fees that aren’t worth it for them.

Here are the 5 most common signs.

1. Despite being “worth” $1 million, your financial life is still simple

If, despite your net worth milestone, you still have just W2 income, a 401(k), some IRAs, and a couple of checking and savings accounts, and especially if you’re single with no kids, your financial situation is simple enough that you don’t need a financial pro’s help.

2. Your investment strategy is simple, low-cost, and adequately diversified

You have money in a basket of low-cost, broad-market index ETFs, and enough money in low-risk, liquid accounts to cover an emergency. You understand how asset allocation works, and your allocation makes sense given your age and net worth. When the market crashes, you stay the course or even take advantage to buy temporarily discounted assets.

If that’s you, you aren’t paying high fees (this was one of my portfolio’s weak points for a long time, paying about 0.8% annual mutual fund management fees, rather than sub-0.1% index ETF management fees).

You also don’t constantly tweak things, and don’t chase yesterday’s hot assets, which by now are likely overpriced and ready to revert to the mean anyway (i.e., drop in price right after you pile in). This means there’s less of a difference for a financial advisor to make for you.

3. You actually enjoy managing your finances and follow through consistently

This was me, in spades, for decades. I enjoyed knowing where every dollar we spend goes; projecting our revenues, business expenses, personal expenses, taxes, and investment results; optimizing our strategy; and continuously reading, learning, and writing about personal finance.

Plus, I consistently followed through on our plan. That consistency compounded into long-term results that got us to where we are. If that describes you, too, then managing your finances isn’t a burden. It’s fun (crazy, right?)!

All this means that you’re less likely to miss anything important or simply neglect it until it’s too late, without needing a financial pro to look over your shoulder and keep cluing you in.

4. You’re comfortable making decisions without constant validation

If you can make important decisions regularly, without stressing and second-guessing, and if you can make these decisions thoughtfully, accepting that there’s rarely a “perfect answer,” you can move forward without losing sleep and without getting paralyzed.

If that’s you, a financial advisor’s value for you is far less than for most mere mortals.

5. The math just doesn’t justify the fees

Financial advisors aren’t set up as a charity. They’re professionals who need to be compensated for their knowledge, expertise, experience, and time.

And different advisors use different fee structures. For example:

Assets Under Management (AUM) fees, e.g., 1% a year to manage a $1 million portfolio. The AUM rate usually drops as your assets increase.

If you’re looking at paying 1% of $1 million, that’s $10k a year. The table below shows how this may evolve over a 20-year period.

The table assumes a median tiered AUM fee schedule, where you’re charged 1.0% for the first $1 million, 0.8% for the portion from $1 million to $2.5 million, 0.65% for the portion from $2.5 million to $5 million, and 0.5% above that.

It also assumes 7.5% annual portfolio growth.

Projected fees are adjusted for a presumed 3.5% annual inflation.

The benefit/(loss) columns assume The benefit/(loss) columns assume that without advice, your annual return would be lower by 0.5% or 1%. With the former, fees exceed the pure financial return. With the latter, they don’t.

Table 1. Projected cost and benefit of (AUM-based) financial advice. The Benefit (Loss) columns show the net impact of fees after assuming 0.5% or 1% lower investment returns for DIY.

You have to ask yourself if the value you’d likely get from hiring an advisor would be much greater than the cost. In the table, we assume your annual DIY returns would be lower than your advised returns by 1%, which results in a win for hiring an advisor.

If we assume just a 0.5% performance penalty, the picture flips (but note that we’re only looking at investment returns, ignoring all other possible benefits). If your situation is so simple and well-organized that the value simply isn’t there, an advisor is likely not a good fit for you.

At least not yet. It may still be worth considering a flat fee, one-time, full financial plan, but you may not even need that yet.

Where Does All This Leave You, and Why Is It a Harder Decision Now?

Some of the first 9 signals probably resonated, at least somewhat.

Some of the last 5 may also feel right.

That’s to be expected.

This isn’t a binary decision. And at this stage of your financial life, the right answer is about what will give you the best outcome, with the least stress, over time. Unfortunately, that decision tends to get harder, not easier, once you’re in “seven-figure land.”

You’d think you’ve already done the hard part, right? You saved, invested, stayed disciplined, and crossed into seven-figure territory. Can’t you just “rinse and repeat?”

In some ways, yes.

Building wealth from nothing was relatively simple, if not easy.

Spend less than you earn.

Build an emergency fund so you don’t get easily derailed.

Consistently invest the difference between your income and your spending in a low-cost, diversified portfolio.

Even if you aren’t perfect, time and discipline do the heavy lifting. But as your net worth grew, things quietly became more complicated, and the margin for error shrank.

Now, at seven figures, you can’t continue just investing. You need to manage your taxes strategically, use different account types appropriately, and avoid excessive risk.

Unlike before, in case of massive losses, you’d have a longer road and less time to recover.

At higher income levels, being a bit less efficient in your tax strategy could eat up thousands or tens of thousands of dollars a year.

Too-aggressive an allocation could set you back years.

Too conservative a one will compound your returns far more slowly than they could.

The wrong withdrawals can lead to large penalties.

Individually, none of these feels critical. But repeated over time, they can quietly reduce what your portfolio can ultimately support.

Not overnight. Not in an obvious way. But slowly, quietly compounding in a way that only becomes visible years later, when your options are more limited.

And whether you want it or not, over time, as assets grow and as you use debt strategically, your financial life gets more complicated.

More accounts.

More tax implications.

More people who count on you to get things right.

Which makes coordination more important than ever.

So, what should you do next?

At this stage, the better question to ask isn’t, “Can I keep doing this myself?”

It’s, “Now that I’ve made it this far, what gives me the highest likelihood of achieving the best outcomes with the least stress?”

For some, continuing the DIY route is the better answer. For others, it’s engaging the right professional help.

What Does a Good Advisor Actually Do?

At this point, if you’re seriously considering hiring a financial advisor, it’s important to be clear on what you’d be paying for. Here are some of the main things.

Investment management (or advice if you prefer to keep your own finger on the trigger), but that’s the least differentiated part of an advisor’s job, the tip of the proverbial iceberg.

Help navigate complicated, interconnected, emotionally driven decisions. E.g., when to retire; how much you can safely spend; if, when, and how much to convert into Roth accounts; when to claim Social Security benefits; how to handle major, unexpected expenses, or large windfalls. These aren’t always one-off questions. You often need to revisit them as the years go by.

Tax strategy around investments, charitable giving, etc. When to draw, from what account, how much to give, and when, etc. You can’t (legally) avoid taxes, but the right setup and the right choices can help you minimize your tax liability over a lifetime.

Coordinate your entire financial situation, including different account types with different tax treatments, different asset classes that bring in returns that get taxed differently, competing goals, and interconnected insurance decisions (e.g., how big an umbrella policy makes sense, what type and how large a life insurance policy you should buy, and which carriers’ policies are your best fits). A good advisor can even help you find the best offer and negotiate the best deal on a car purchase from a dealer.

Provide emotional ballast when markets crash and/or your spending spikes. This is crucial to prevent short-term thinking and emotional reactions from derailing your long-term plan. The value of this behavioral support can’t be quantified ahead of time, but over a lifetime, it can be one of the biggest drivers of optimal outcomes.

Reduce complexity and mental and emotional load. Yes, you can probably do it all yourself. But a good advisor can take many tasks off your plate so you don’t have to. Things like tracking market conditions, insurance assessment, finding the best providers for, e.g., concierge services, etc. This not only improves financial outcomes but also reduces stress and improves your quality of life.

As mentioned above, if you’re a single financial point of failure for your family, a good advisor can provide a critical backup system.

It Isn’t All or Nothing!

It’s a common misconception. Hiring a financial advisor isn’t all or nothing. It isn’t a choice between doing everything yourself or handing everything over. Certainly not from Day One.

You could hire a full-service advisor, especially if your situation is especially complicated and you prefer to delegate everything to a pro.

Or, you could pay a flat fee for a financial plan or advice around a specific decision, then implement it yourself. This is best if you’re capable, engaged, like doing things yourself, and just want a second opinion or a better-structured overall plan.

Another option is as-needed advice, paid by the hour. This is best when you don’t need ongoing support, but want to have someone you can call on for advice whenever you need it.

Or, finally, you can go for a hybrid approach. This could be getting an initial plan including asset allocation, followed by occasional check-ins when needed, or using a robo-advisor for portfolio management, and paying for as-needed human advice when you need more.

What the Pros Say

I asked several financial advisors some questions regarding both sides of the “do they/don’t they” divide regarding millionaires needing professional support.

Here’s what they have to say.

Q. In your experience, what’s the clearest sign that someone who has built a significant portfolio on their own would benefit from working with a financial advisor?

A. Ben Simerly, CFP®, Financial Advisor and Founder of Lakehouse Family Wealth, kicks things off for us, “The clearest sign that someone who has built a significant portfolio on their own would benefit from working with a financial advisor is if they think they don’t need an advisor.

“For this one, talk to any business owner or leader in human history. The best will tell you that the #1 thing they look for in finding a ‘smart’ person is the combination of mental state and passion for learning more about what they don’t know, and an understanding that they actually know so little that they will always need help.

“One of the best compliments to any hungry mind is _”that guy/gal really knows what they don’t know…’And if I manage to die knowing even a hint of what I do not know, it will be a life well learned.’ The smartest people in the room always ask for help, across all of history, in every profession, in every scenario. The only real question is how much help, in what ways, and who will be in charge of the team. And this dictum bears out.

“Often, the prospective clients who believe they need an advisor the most have done a far better job than those who are convinced they don’t need an advisor, but want some free ideas.”

Steven Crane, Founder of Financial Legacy Builders, adds, “The clearest sign someone with a million-dollar portfolio needs an advisor is when the decisions start getting more complex than the investments themselves. Building wealth is one skill. Turning that wealth into sustainable income, managing taxes, and making smart decisions under pressure is a completely different skill set. I’ve seen plenty of people do a great job accumulating assets, but then struggle when it’s time to actually use the money.”

Jeffrey J. Smith, Founder and Managing Partner of OWL Private Wealth Advisors, offers a nuanced view, “In my experience, having a $1 million portfolio doesn’t automatically mean you should have a financial advisor. Some people are delegators and like the idea of partnering with a professional in order to keep them on the right path when it comes to their asset allocation, asset location, tax planning, estate and charitable planning goals, along with their income planning needs. For others, they are just fine as a DIY investor with $1 million or even more. There needs to be a fit between the two parties, and in many cases, that partnership can be better than going at it alone.”

Scot Johnson, CFA, Principal & Chief Investment Officer at Adell, Harriman & Carpenter, Inc., offers some observations: “There doesn’t appear to be any rhyme or reason to how the portfolio was constructed. Advisors build portfolios to target client goals and aspirations, not to accommodate a collection of stock-of-the-week picks. We will also often find that portfolios are concentrated in the market sector where the prospective client works and feels knowledgeable. Advisors build portfolios that are diversified across sectors. Each of those sectors will at some point have its proverbial day in the sun, and advisors will want to make sure clients have exposure when that day comes, even if we don’t know when it will arrive.”

Don Rudolph, Fixed Fee Fiduciary at FlatFeeCIO, shares how financial advice, these days, can be far less expensive, and thus far more approachable for many. He says, “Experienced advice is far more accessible today than even 5 or 10 years ago. We are in a new era of efficient wealth management where far lower fixed annual fees are transforming financial outcomes for affluent investors by unlocking the potential for tens of thousands of dollars in savings each year versus legacy level percentage on asset fees.

“Today, the full-service wealth suite that includes ongoing wealth management and tax and estate planning is available for a far lower single fixed annual fee based on complexity and curated for the exact services needed, versus a one-size-fits-all decades-old percentage on asset fee. The current AI disruption is rapidly accelerating this efficient wealth services wave toward fixed-fee fiduciaries as a preferred engagement alternative for affluent families.”

Q.How can a good financial advisor add value for a millionaire in ways that most people don’t fully appreciate?

A. Simerly points out the difference a financial advisor’s team can make, “For many clients aged 55 with $1 million in investable assets, we can often add 2-4% to returns, and cut taxes in retirement by 75% to 95%. That often translates to a retirement income that is 1.5 to 3 times what it would have been before they came to us.