Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

What if I could show you a way you could make your kid wealthy.

For real.

No get-rich-quick schemes. No summer jobs. No complicated financial shenanigans.

All it takes is small gifts.

What Do I Mean by Wealthy?

If you’re expecting me to teach you how your kid can become as wealthy as Bezos, Gates, or Buffet, sorry but no.

But how about enough money to buy a house without a mortgage before she’s 30? According to the St. Louis Fed, as of the end of June 2020 that would take $313,200.

How about enough money to be able to retire by 67 with a portfolio throwing off more than the median income in the U.S. ($75,500 as of the fiscal year 2019 according to the U.S. Department of Housing and Urban Development)?

Would that be interesting?

How It Works

Your kid is born.

Congratulations!

Open a taxable investment account in your own name (so you retain control over it until it’s ready for prime time).

Set up an automatic transfer of $250 per month from your checking account to the new investment account and have it automatically invested in a tax-efficient diversified investment. This could be an exchange-traded fund (ETF) mimicking the S&P 500 or another diversified index.

It’s important to make sure it’s not an actively traded mutual fund, so you don’t have to keep paying income taxes each year as the mutual fund is required to distribute its gains to you.

Each year, increase the monthly gift to account for inflation. If inflation is 2% for example, increase the gift from $250 to $255.

Rinse and repeat until your kid turns 30.

That’s it.

How It Turns Out

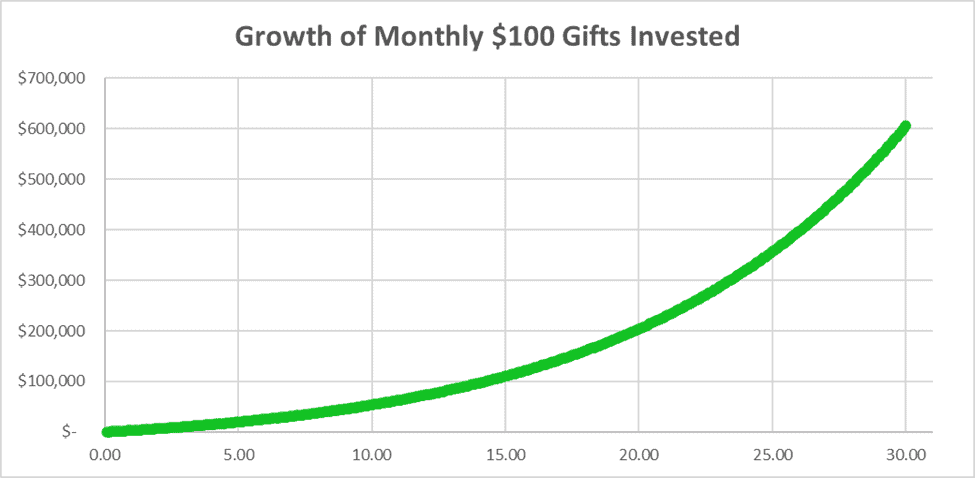

Let’s assume a 9.5% annual return on your investment (depending on how far back you start, the long-term historical return of the U.S. stock market was around 9.5% to $10%).

The figure below shows the growth of your gift balance including returns.

Spectacular, right?

By the time your kid is 30, the account is worth over $600,000!

Not so fast my friend.

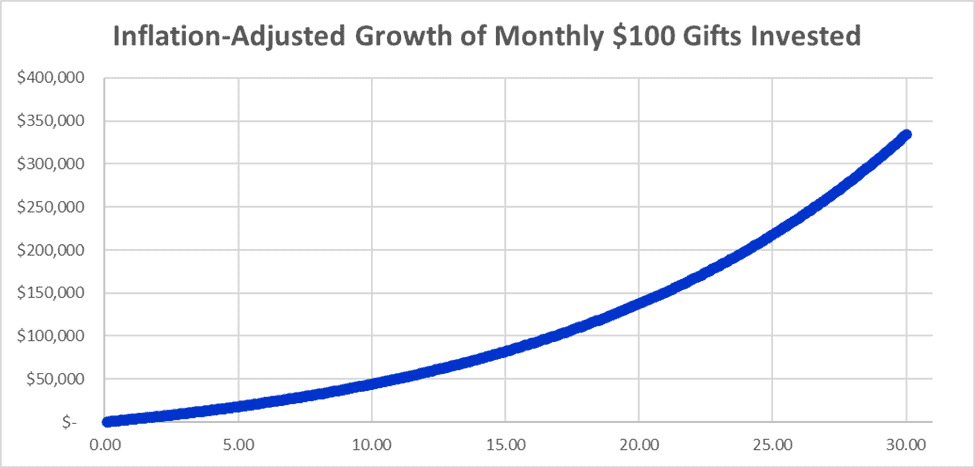

During these 30 years, inflation has been nibbling away at the value of the dollar. The next figure shows your results after adjusting for an assumed 2% annual inflation.

Still pretty impressive, wouldn’t you agree?

Whether your kid would want to do it or not, this would let her buy a $340,000 home with no need for a mortgage!

Alternatively, she could hold off on using the money and set it aside until she turns 60.

By then, with the same assumed annual investment returns, she’d have a cool $9.2 million! Even after inflation, that would be over $2.8 million!

If she stuck with a 3.5% safe withdrawal rate, she’d have over $98k inflation-adjusted dollars to live on for the rest of her life!

How’s that for wealthy?

Caveats

Yes, caveats. Those always have to be acknowledged, right?

Here they are:

- Not everyone can afford to set aside $250 a month for their kid (let alone that much for each of several kids).

- It takes commitment to keep going even when it’s hard to never raid the account for other things and to actually hand it over when it’s time even though the account is in your name so your kid has no legally binding rights to it.

- The stock market may have higher returns than 9.5% a year, but it may also have a lower long-term return. As they say, past results are no guarantee of future ones.

- When it’s time to give the money over, you’ll need to work with financial pros to make sure you don’t have to pay gift tax. This may require transferring the money over the course of several years or using up some of your lifetime gift tax exemption.

The Bottom Line

Even if you can’t afford to gift $250 a month to your kid(s), making regular gifts, even small ones, over the first several decades of their lives can build up into a very significant chunk of money.

As long as you do it smartly, you can maximize the ultimate impact of your gifts, while minimizing taxes.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor