Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

One of the scariest questions you may have to ask yourself is: “Do I have enough money to retire?” It’s about more than just the numbers. Your retirement lifestyle and the money to make it happen require long-term planning.

To have a smooth retirement, you’ll need to address retirement savings and manage ongoing risks like market downturns and inflation. Having a game plan is essential, but it doesn’t have to be difficult. With attention to some key areas, you can transition into retirement with confidence.

Understand Your Retirement Lifestyle Goals

Retirement goals can feel like an imaginary concept. In many cases, we might’ve been so busy we forgot to ask, “What do I really want?” Also, goals can shift over time. Costs may have changed, your interests change (what’s this pickleball thing?), and let’s be honest, life can throw unforeseen wrenches in our plans.

Regardless, it’s important to have the most accurate idea of what you want. You’ll want to account for family activities, travel, and hobbies you want to get (back) into. You might also want a hybrid of working part-time while adding in more personal interests. In the end, you might just want the ability to choose what you will and won’t do each day.

Dare to Dream

All these goals have a number tied to them, but we’ll get to the financial aspects in a moment. Right now, we’re dreaming a bit and deciding what ideal looks like. What’s your perfect day, week, or month look like?

Let yourself get wild for a moment, and then we’ll see what you can realistically achieve. It’s also possible to complete lots of “little” achievements (five new states each year) versus one large goal (visit all 50 states in one massive trip). Remember, this is your canvas, so paint in your style.

Estimate Your Annual Retirement Expenses

Once you’ve dreamed up your ideal retirement, it’s time to get honest about how much everything will cost. You’ll need to sort by category so we can align your income sources later. It’s best to break expenses into two categories: essentials (housing, food, healthcare) and non-essential (vacations, hobbies).

Be as realistic as possible. If you have friends who took a similar trip, ask them for a ballpark estimate of what it cost them. If you’re already living where you plan to retire, you might know precisely what your housing costs are. We don’t want to underestimate here.

It’s easiest to estimate on an annual or monthly basis.

Accounting for Inflation

Next, you’ll need to account for inflation during retirement. There’s nothing more annoying than feeling your buying power slowly erode with the continual rise of inflation. This can be especially painful for increased healthcare costs or other expenses rising faster than inflation.

We use advanced software to adjust for inflation. However, you can use online tools and apps to get ballpark estimates. Adjusting for inflation ensures you have all the money you need in the future.

Calculate Your Income Sources

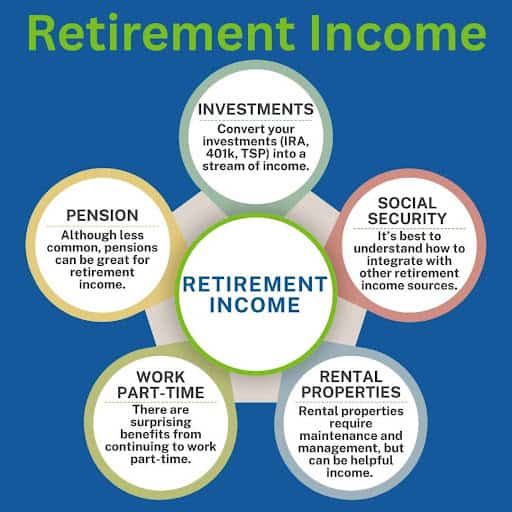

You’ve probably heard the benefits of having a diversified portfolio of stocks and bonds. However, it’s equally important to have a diverse set of retirement income streams. These include investment income, Social Security, pension income, annuities, rental income, and part-time work.

Investment Income

Investment withdrawals from IRAs, 401(k), and taxable accounts can be great sources of income in retirement. However, investing does have risk. Returns may fluctuate over time, so you’ll need a solid investment strategy tailored for your needs.

Social Security

The nice thing about Social Security is the annual adjustment for inflation. It’s a great source of safe income for many Americans. Carefully consider when to start drawing Social Security to maximize your benefits.

Pension Income

Although pensions may not be as common today, they’re still a significant retirement asset for many retirees. If you have a pension, you’ll want to maximize your payout and coordinate pension income alongside other income sources. In many cases, a pension comes with other benefits too.

It may be possible to have all your basic needs met with the combination of Social Security and a pension.

Annuities

Annuities are an insurance product, but they’re insuring against you living longer than planned. These can be great if you don’t have much guaranteed retirement income. However, they can be expensive (lots of fees), and typically don’t have high returns.

There’s always a tradeoff. In this case, your annuity income gives some added peace of mind, but comes at a cost.

Rental Income

Rental properties can be a great source of retirement income. You don’t have to own a huge rental empire either. Even renting a vacation home on Airbnb or VRBO can give you a nice secondary income stream.

Of course, you’ll need to manage the properties or hire a property manager. In most cases, a well-maintained rental property or two can be worth the hassle. If you’re not interested in continual management and upkeep, you might not want to be a landlord.

Part-Time Work

Although working part-time might not be your first choice, it could be a benefit in more ways than one. You might be able to take on part-time coaching, consulting, or teaching just a few hours a week. The extra income is nice, and your expertise can be valuable to employers.

Surprisingly, continuing to work part-time might be good for your health. Only you can decide what’s best for your mind, body, and spirit.

Bringing it All Together

Once you understand all your income streams, you can form a cohesive retirement income plan. There are many considerations, such as safe withdrawal rates (4% rule, dynamic withdrawal strategies), timing of Social Security, tax-saving strategy implementation, and estate planning considerations.

There’s no one-size-fits-all retirement plan. You’ll want to take a comprehensive approach to bringing everything together. It’s like pulling on a shoelace; each adjustment on one side has an equal pull on the other side.

Run the Numbers: Do You Have Enough?

Once you’ve brought everything together, you can answer the biggest question: “Can I afford to retire?” Once you add up all your income, you can subtract your expenses. If you’ve got money left over, you’re good to go. If not, you’ll need to figure out how to make more or spend less.

However, retirement income risk factors are the final pieces of the puzzle.

Watch Out for Retirement Risk Factors

You’ll still have to navigate real risks such as longevity risk (outliving your money), healthcare and long-term care costs, market volatility (recessions), inflation, tax changes (SECURE Act and SECURE 2.0), and sequence of returns risk (bad timing of market corrections).

All of these can be overcome, but it’s a lot easier when you’ve planned for them. We can’t prevent problems from happening, but we can make sure we’re protected when things don’t go according to plan.

Tools and Resources to Help You Decide

Luckily, there are many tools available to help plan your retirement. From financial planning software and calculators to professional advice, you’ve got options. You might even be pleasantly surprised at how prepared you are for retirement.

We’re slightly biased but highly suggest working with a financial planner for a personalized retirement plan. It’s hard to describe the peace of mind from knowing you’ve got all your “ducks in a row” for retirement.

Know the Number, But Plan Beyond It

The numbers are only part of the equation. You may also be surprised how small shifts can go a long way. It’s never too late to create a retirement strategy to get you where you need to go.

Lean on experts like accountants and financial planners to help guide you. The best decisions come from wise counsel, accurate numbers, and a healthy understanding of what’s most important to you in life. You can create the right retirement plan, but you have to get started.

This article reflects the insights and opinions of its author and is not a recommendation or endorsement of their views or services.

About the Author

Clint Haynes, CFP® | NextGen Wealth

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor