Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

If you’ve ever pulled up a college savings calculator and felt an immediate knot in your stomach, you’re not alone — and you’re probably not as far behind as you think. The benchmarks that investment firms publish are useful planning tools, but they’re built on assumptions that rarely match any real family’s situation, and they say nothing about what actually determines whether families reach a good outcome. What financial advisors consistently find is that the decisions you make about funding, school choice, and trade-offs matter far more than the balance in a 529 account. Here’s how to stop measuring yourself against a hypothetical family and start focusing on the factors you can actually control.

If you have kids under 18, you’ve probably looked up college savings numbers.

According to T. Rowe Price (TRP), for example, the full cost of attendance for a four-year degree is $103k at a public university for in-state students and $183k for out-of-state students. At a private non-profit school, that cost grows to $244k.

TRP expects parents to save up enough to pay about half of that, considering likely grants, scholarships, loans, and income from current employment during school years.

If you’re anything like my family was while our kids were growing up, it can seem like an impossible task, especially given all the competing priorities, like putting food on the table, keeping a roof over your head, and hopefully saving at least some money for retirement.

Key Takeaways

College savings benchmarks measure a hypothetical family, not yours.

Benchmarks from firms like T. Rowe Price assume you started saving at birth, contributed consistently, and knew years in advance which type of school your child would attend. Most families don’t fit that profile. Being behind on paper reflects those mismatched assumptions — not a verdict on whether your child can afford college.

Deciding how much you’re willing to pay matters more than how much you’ve saved.

Defining your funding commitment — whether that’s full cost of attendance, in-state tuition only, a fixed dollar amount, or a percentage of total cost — drives every other decision: school choice, loan strategy, scholarship goals, and how realistic your path forward actually is. Two families with identical savings balances can reach completely different outcomes based on this one conversation.

Retirement savings should take priority over college savings when you can’t fully fund both.

Your child has decades of options — loans, scholarships, work-study, and school choice — to fund their education. You have far fewer levers to fund retirement, and every year you delay makes the challenge steeper. Financial advisors consistently remind clients that not becoming a financial burden to your children later in life is itself one of the most meaningful things you can do for them.

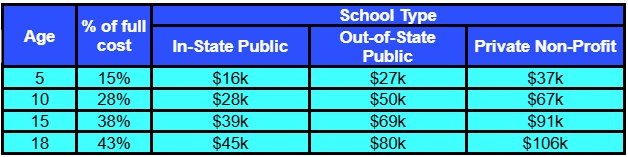

When our kids were growing up, we never managed to save a single dollar toward their college costs, let alone meet TRP’s benchmarks, shown in Table 1.

In practical terms, that means being expected to have tens of thousands saved well before high school. Those are big numbers, especially if you’re starting late.

Say you have a 15-year-old who has her heart set on attending a private university. Do you already have $91k in her college fund?

If you’re not on track with these guidelines, the gap can feel increasingly uncomfortable. You may be asking yourself, “Are we behind?”

And if the answer is yes, you may be thinking, “Are we failing our daughter?”

That’s a feeling I know well from firsthand experience.

Since we didn’t have a college fund, we had to figure out ways to cover those costs as we went, using current income, with trade-offs and uncertainty as our constant companions.

When our son was accepted to our state university’s flagship campus, the University of Maryland, College Park (UMCP), and to a prestigious private school he preferred, we sat him down to discuss what each choice would mean.

We could cover the full costs of a degree at UMCP without taking out loans, but the private school would have left him with many tens of thousands of dollars in student-loan debt by graduation, even considering their offer to reduce his tuition by 50%.

Conversations like this, and the decisions they led to, shaped how we paid for our kids’ degrees, how they approached school and work, and, ultimately, their careers.

All this forced us to face something that benchmarks and guidelines don’t usually address. Those numbers were never intended to be treated as a scorecard.

They’re a useful planning tool, based on specific assumptions, defined savings goals, and the ability to contribute consistently from birth to college graduation. If you’re anything like we were, your life simply doesn’t look like that.

Some families start late.

Some can’t save consistently, or at all.

Even if you saved from your kid’s birth, they may start out willing to attend their state school, only to decide later that they really want to attend a highly selective, super expensive private school. And when that happens, say when they’re 15, even in the unlikely case that you were “on track” up to that point, you’re suddenly less than halfway to where you’re “supposed” to be.

And yet, many of those families still find a way to make it work.

Not by hitting all the benchmarks on time, but by making informed decisions about what they’ll pay for, what they won’t, and how they expect their children to support the process.

Unless you’re uber-wealthy, you can’t avoid all trade-offs. But you can and should make smart choices about the trade-offs you face.

What that looks like is what we’ll cover below.

What College Savings Benchmarks Actually Measure And What They Don’t

The biggest pitfall of benchmarks like TRP’s is if you believe they’re something they’re not, which may then lead you to despair or make unsustainable decisions.

First, what they aren’t.

They’re not requirements, predictions, or guarantees.

They’re just intended to give you a sanity check. And even that’s limited, because they’re trying to give you a plausible path to successfully funding your kid’s college career, without knowing anything about your situation.

- How old is your child?

- What’s the full cost of attendance at the college your child will attend, and how will that cost change by the time your child graduates?

- How many college years will your child need to graduate (4 is the minimum, not a maximum or even the median*)?

- How many other children do you have, for whom you need to save in parallel?

- How much, if anything, do you already have saved up for their college expenses?

- How much can you afford to put into their college fund, and how consistently?

- How will you invest that college fund, and what returns will you achieve?

* According to the National Center for Education Statistics (NCES), “In 2020, the overall 6-year graduation rate for first-time, full-time undergraduate students who began seeking a bachelor’s degree at 4-year degree-granting institutions in fall 2014 was 64 percent.” This means that more than one in three students took longer than 6 years to graduate! The median time to graduate was 52 months, and only 44.1% graduated in 4 years.

So, not knowing any of those things, they make assumptions:

- You have one child (or the following is true for each of your children).

- You started saving from your child’s birth and contribute a consistent amount each month.

- You aim to cover 50% of the full cost from your college fund.

- Your college fund is invested and will compound at a “reasonable” long-term rate.

- You know the cost level of your child’s college (between the three levels they show).

With all these hypotheticals in place, they generate a plausible trajectory that helps you see if you’re ahead, on track, or behind.

But there’s a problem.

You live in the real world, not in their hypothetical “typical” scenario.

- You may have started saving later than ideal.

- You face competing priorities and may have had months (or years) when you couldn’t contribute as much, or at all, to the college fund.

- College costs are unlikely to stay the same over the 20+ years from when your kid is born until they graduate from college.

- You may think you’ll send your kid to your state’s school, but they may choose to go to a far more expensive private school.

As Cole Williams, Founder, Vessel Financial Planning, says, “Benchmarks are hard to trust because the true out-of-pocket cost varies so much from family to family. There are too many variables on the front end to know whether you’re ahead or behind.”

Using the benchmarks as gospel is like playing on a tilted playing field with moving goalposts.

Stressful and not very helpful.

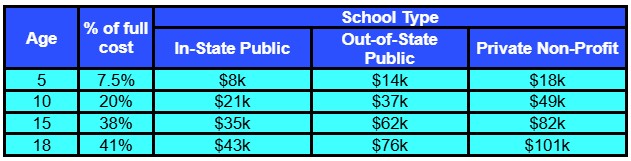

TRP recognizes this and provides a secondary set of benchmarks for parents who can’t save as much as their main model assumes, starting from their child’s birth. This secondary model assumes lower contributions early on, with contributions increasing gradually, as seen in Table 2.

This seems much more practical because many families face higher expenses in the early years, especially for childcare, and their earnings are usually lower than in later years. As these factors reverse, it becomes easier to allocate money for college savings.

This shows that TRP realized their benchmarks need flexibility, though even this “ramp-up strategy” doesn’t necessarily account for your specific situation and how it will evolve over 20+ years.

As you can tell, these benchmarks should be viewed as one reference point, not a judgment or verdict on how successful you are.

They help answer the question: If everything went according to the specific assumptions of these benchmarks, where should I be at this point?

They don’t answer any of these questions:

- Am I doing this right?

- Have I already failed?

- Will my child end up unable to go to college because I haven’t saved enough?

They also don’t tell you what to do next, given your specific situation, which is really the only thing that would make a difference.

Things like:

- Discuss school choice with your kid and make clear what you can and likely cannot afford.

- Adjust your aim to a smaller portion of the full cost of a degree, with grants, scholarships, and loans covering the remainder.

- Have your kid work part-time through college to help pay tuition.

Two families can have identical college-fund balances for kids at the same age but have completely different likelihoods of success, depending on how they address potential shortfalls.

That’s why financial advisors tend to treat such benchmarks as a starting point rather than a plan. They use them to surface potential gaps, then shift to defining realistic goals, prioritizing competing needs and goals, and proposing ways of making the plan work by increasing income, decreasing spending, or a combination of the two.

As Joe Stabile, founder of Coast Financial, explains, “Most families I speak with would like to fund their kid’s college 100% if they could, but also understand it may not be realistic. I’ve found that the best way to give them confidence in their decision is to show them different scenarios on what it would take to fund different levels of college tuition. For example, showing them the monthly savings required to fund 100%, 75%, 50%, and 25% of projected college tuition at different tuition rates. Once they see these numbers and we have a conversation about their family values, they feel much more confident in their approach.”

This kind of scenario planning helps make trade-offs concrete and easier to evaluate.

In other words, benchmarks can tell you how close you are to a plausible trajectory, but don’t tell you what to do about it.

That’s our next focus.

The College Planning Decision That Matters More Than Your Savings Balance

Since benchmarks don’t tell you what to do next, what does?

The answer is both simpler and more uncomfortable than you might expect.

You need to decide how much you’re actually willing and able to pay toward your child’s college.

As Mike Hunsberger, ChFC®, CFP®, CCFC, Owner, Next Mission Financial Planning, puts it, “I find that most families are behind in saving for college and don’t understand what they’re likely to be expected to pay at different schools. While saving for college is important, choosing the best school you can actually afford has far more impact.”

That single decision drives everything else:

- What type of school can your child realistically attend, cost-wise?

- Will they need to take out student loans, and if so, how large?

- Will they need to bring in scholarships and grants?

- Will they need to work during college to help cover costs?

- How much “catching up” do you have to do?

Without such clarity, you risk defaulting to “We should cover the full cost of attendance at whatever school she chooses.”

Steve Witter, CFP®, CSLP®, Founder of Student Loan Steve, warns, “The biggest mistake I see with parents is telling their kid that ‘if you get into your dream college, we will figure it out.’ With the new student loan borrowing limits and the loss of parents’ ability to repay Parent Plus loans based on income, it’s more important than ever to have a college budget and stick to it.”

Hunsberger agrees, “The most dangerous words in college planning are ‘If you get in, we’ll figure it out.’ Families need a plan and a budget for college. You don’t shop for Ferraris if all you can afford is a Honda. College shouldn’t be any different.”

Doing that could cause you to:

- Stretch beyond what you can sustain.

- Underfund your retirement nest egg.

- Suffer long-term financial stress that lasts long after your kid graduates.

This is why a good financial advisor won’t ask, “How far behind are you?”

Instead, your advisor is more likely to ask, “What role do you want to play in paying for your child’s college?”

Your answer could be, “All costs related to getting the degree at whatever college he chooses.” And if you can afford that, without shortchanging your other priorities, your advisor will work that into your plan.

However, you could instead say, “Full cost of attendance for 4 years at the in-state tuition level,” or a fixed dollar amount, or a set percentage of total cost.

There’s no universally right answer here.

There’s just an answer that’s right for you, your situation, and your priorities.

Williams explains, “School choice still matters, but it’s not as clean as ‘public = affordable, private = expensive.’ There are exceptions on both sides. What matters more is getting clear early on whose shoulders the funding will fall. Are the parents and student willing to take on loans? Is the student prepared to do the work required to get merit-based aid, such as scholarships or grants? How much? These answers matter a lot.”

He then addresses what often happens when there are several children, “I commonly see spouses who aren’t aligned on what college funding should look like, especially with multiple kids, when ‘being fair’ becomes the goal. Fairness is our instinct as parents, but life doesn’t sit still. One spouse loses a job, or bonuses dry up, or, on the flip side, income increases. The financial picture that existed when your oldest started school often looks different by the time your youngest gets there.”

Should You Prioritize College Savings or Retirement Savings?

Except for the wealthiest among us, we all face financial trade-offs.

The biggest such trade-off regarding funding college is how it interacts, not to say interferes, with saving and investing for retirement.

Hunsberger shares how he illustrates this to clients, “I like to frame the savings choice between college and retirement in terms of how much longer the parents will need to work if they decide that funding college is the priority. If their after-tax income is $120,000 and they have 2 kids that they expect will cost $240,000 to get through undergrad, I make sure they’re willing to work for an additional 2 years.”

Williams agrees, “Every family is different, but my general coaching is to put your own oxygen mask on before helping others with theirs. Some parents commit to covering every dollar of their kid’s education without realizing that choice might require them to work three more years before they can retire comfortably. I want them to see that tradeoff clearly before they share any funding expectations with their students.”

I’m sure you’ve heard the common saying, “You can borrow for college, but not for retirement.”

And while it’s not completely accurate, since you can take out a reverse mortgage to help fund retirement, it is directionally true, since those options tend to be expensive, reduce flexibility, and leave you with a smaller cushion later in retirement.

Student loans, on the other hand, are a $1.8 trillion (and growing) industry that includes both federal and private options.

This doesn’t mean that student loans are appropriate in all cases, nor that students don’t often over-extend themselves and then struggle with years or decades of debt repayment.

But it is a broader and more readily available resource.

Peter Bo Rappmund, Principal at Counterpoint, explains, “Regarding how to balance college savings with retirement savings, especially when you can’t fully fund both, the priority is clear: retirement comes first. You put on your oxygen mask, then help your kids. Your child has decades of options to pay for college, including loans, scholarships, part-time work, and school choice. You have far fewer options to fund retirement, and they all diminish the longer you wait. I remind clients that a loving and thoughtful thing you can do for your kids is not to become their financial burden in 20 years. So, we protect retirement at the level we need to commit to, then direct what’s left toward college, and we have an honest conversation with the child about what that means for school choice.”

A Real-World Example: Starting College With $0 Saved

In our situation with my two older kids, this wasn’t a theoretical trade-off.

We barely managed to put something away for retirement. We certainly couldn’t save anything for their college expenses, so we had to figure out what we could and would do.

Their mother and I, seeing our trajectory early on, told them both, from when they were tweens, that we would cover their full cost of attendance for 4 years at UMCP in-state levels.

If they wanted to attend a more expensive school and/or if they took longer than 4 years, it would be up to them to cover the difference. This could be from grants and scholarships, or student loans.

That was the context of our later conversation with our son, which led him to decline his acceptance to the private school he initially preferred and to attend UMCP.

While this wasn’t an easy conversation to have, it was clear.

And it was that clarity that led him to make that choice, because he understood that (a) managers at the private school had a higher regard for UMCP graduates in his field than their own, all other things being equal; (b) it would be far better for him financially to avoid the crushing student debt he’d incur; and (c) his career outcome was unlikely to be affected by school choice in the long term, based on research that shows long-term earnings are often similar regardless of school selectivity.

As a result, he graduated in 4 years with a degree in his chosen field from a highly regarded school and went on to a successful career, all from a starting point of $0 in college savings when he started school.

Rappmund says such conversations are critical, “The biggest mistake I see parents make when trying to fund their child’s college education is when they avoid the conversation. Parents will save diligently for 18 years and then never sit their kid down to say, ‘Here’s what we can pay for, here’s what we can’t, and here’s what we expect you to bring or compromise on.’ That straightforwardness and clarity are worth more than another $20,000 in the 529 plan. The mistake isn’t so much that too little was saved. It’s hoping the numbers will perfectly work themselves out by the finish line.”

This illustrates the limitations of college savings benchmarks.

They focus only on the savings balance and the child’s age. Understandably, they can’t account for the things you can do to address any “paper shortfalls.” Things like setting expectations and deciding what trade-offs you’re willing to make.

Two families can have identical college-fund balances, be equally behind (or on track) on paper, and end up with vastly different ultimate outcomes. Had we encouraged our son to go to the private school, his results would likely have been far worse.

In other words, while how much you’ve saved matters, the decisions you make about funding, school choice, and trade-offs matter far more.

That’s what ultimately determines whether a family ends up with a workable outcome or one that creates long-term financial stress.

As Rappmund puts it, “Benchmarks can be a good sanity check, but shouldn’t be a scorecard. The savings balance tells me where a family stands on a hypothetical track. It tells me almost nothing about whether they’ll reach a good outcome, though. The decisions matter far more. I’ve seen families who were ‘behind’ on paper end up just fine because they had those conversations early. And I’ve seen families who were ‘on track’ get into real trouble because they never did.”

The most important takeaway here isn’t that you shouldn’t try to set aside money for your kids’ college education.

It’s that your goal can’t be to avoid every trade-off; it should be to make the trade-off choices that are right for you and your family.

Articulate and share with your kids what you’re willing and able to pay towards their college expenses. Once you do that, even if you’re far behind on paper, your path forward becomes much clearer.

What to Do If You’re Behind on College Savings

If you made it this far and still feel behind, you’re not alone.

But remember, what matters most isn’t where you are relative to benchmarks based on “typical” assumptions.

It’s what you’ll do next.

TRP acknowledges this and offers more nuanced guidance based on your child’s age.

- If your kid is young, they suggest trying to redirect money spent on childcare to college savings. The point isn’t to fix everything immediately by magically making up any savings shortfall, but to concentrate on changing the trajectory.

- If your kid is about halfway to college age, they suggest asking family and friends to make college-funding contributions as holiday and birthday gifts, and using income increases, and budget cutting to increase college savings. Here, the point is to make serious changes that make it at least plausible that you’ll hit your goal.

- When there’s little or no time left, their guidance is to try to get scholarships, student loans, and paid internships or part-time work while in school. At this point, you’re in the situation we were in. It’s too late to save for college, but you still have options for getting to a good outcome, especially if your kid is willing to attend your state school.

In our case, we did what we needed to do:

- Set clear boundaries.

- Made trade-offs explicit for our kids.

- Set expectations that they’d work while in school and contribute some of their earnings toward their college expenses.

We also took (legal) advantage of our state’s 529 plan rules.

In Maryland, contributions to a 529 plan may qualify for a state income tax deduction, even if the funds are used shortly after you contribute. Thus, when we needed to make a tuition payment, we first put the money into a 529 plan, then withdrew it the next day and sent it to the school.

We couldn’t benefit from the tax-free growth of investing over time in such plans, but we did get the state income tax deduction for the 529 contributions, which helped make those college expenses somewhat more affordable.

The details of 529 plan rules vary by state, so you may or may not be able to do something similar. But the broader point stands. Even late in the process, there are probably ways you can improve your situation.

The Bottom Line on College Savings Benchmarks

Benchmarks are useful tools. But they’re not a guilty verdict when you’re behind on paper.

Instead of stressing over how far behind you may be, focus on what you can still control.

- Evaluate and adjust your strategy and the trade-offs you’re willing to accept.

- Decide what you’re willing and able to pay.

- Make adjustments where you can.

What you’ve saved so far gives you options you wouldn’t have otherwise. But it doesn’t determine your outcome.

The most important factors in determining your results are the trade-offs you choose and the actions you take from this point forward.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor