What this article covers

Financial advisors explain why recession-proofing your finances has little to do with predicting markets — and everything to do with reducing fragility, building margin, and making good decisions before economic stress arrives.

Every once in a while, recession fears dominate headlines.

And many people obsess over this kind of doomsday-peddling.

However, as CNN’s David Goldman wrote recently, “Economists have been predicting or warning about a recession every single year for the past eight years, and they were only right once – kinda.”

Even the famous yield-curve-inversion recession signal, which correctly signaled 8 out of 8 recessions since 1968, has been signaling a recession for nearly four years now, falsely, so far.

That’s because recessions are impossible to predict reliably.

What we do know is that there will be another recession, and another after that, and more after that one. That’s because, since the end of World War II, the US has experienced 12 recessions. Once every 6.75 years.

Most lasted less than a year, and the longest was 18 months. But if you make the wrong moves as a result of a recession, or because you fear one, that can impact you for years or decades.

If you’re like most people, you probably bought into the fallacy that preparing for a recession means you have to predict the economy, so you can time the market and make a major “protective” change in your investments before everyone else starts running for the doors and crashing the market.

That’s because the standard recession-prep advice isn’t very helpful.

As professional financial advisors point out, the real issue isn’t forecasting the economy or the market.

It’s addressing financial fragility.

Dr. Steven Crane, Founder of Financial Legacy Builders, says, “I think most recession advice is worthless because it assumes the average person’s biggest problem is their portfolio. It’s usually not. The real issue is fragility. People build lives that only work if everything keeps going perfectly: stable income, rising markets, low stress, no layoffs, no health issues. A recession just exposes the cracks that were already there.”

You can appear to be financially successful on paper, but still be one layoff, one medical emergency, or one business slowdown away from making panic-driven decisions.

That’s financial fragility.

Depending on a single paycheck (or both paychecks in a dual-income household), having minimal liquidity, over-concentrated investments, a budget overwhelmed by non-discretionary expenses, and a lifestyle with almost no resilience to disruption.

As Crane says, “One of the most overlooked recession-prep moves has nothing to do with investing. It’s reducing dependency. Dependency on one paycheck, one client, one stock position, one inflated lifestyle, one economic outcome.”

This is why financial experts recommend a completely different recession-prep framework. One that focuses less on recession predictions and headlines, and more on building resilience into your financial life, so that it can absorb stress without crumbling.

That means you need to build up your liquidity, flexibility, and emotional discipline so that you avoid panic and forced decisions.

Key Takeaways

The Real Recession Risk Is Financial Fragility, Not Your Portfolio

Most recession-prep advice focuses on investments, but financial advisors say the greater danger is a life built to work only when everything goes perfectly — one income stream, minimal liquidity, and fixed expenses that leave no margin for disruption. Recessions don’t create fragility; they expose it.

Building Financial Margin Is the Most Effective Recession Preparation

Financial margin — the sum of savings and discretionary expenses as a share of after-tax income — is the buffer that lets you absorb job loss, take advantage of down-market opportunities, and make decisions from clarity rather than panic. Advisors target 35–40% for clients who want genuine resilience.

Your Recession Risk Depends on Your Life Stage and Income Type

W-2 employees, business owners, RSU holders, near-retirees, and retirees each face different recession vulnerabilities — and generic advice rarely addresses the right one. The goal isn’t to predict the next downturn; it’s to identify your specific concentration risks and reduce them before economic stress forces the decision.

The Biggest Recession Risk Usually Isn’t Your Portfolio

When reading recession-fear headlines, many people react as if their biggest risk is how their portfolio is positioned.

Financial advisors argue the real risks are usually elsewhere.

Crane explains, “Honestly, I think emotional decision-making matters more than investment strategy during recessions. Most people already have decent investments. What they don’t have is psychological preparedness. They’ve never stress-tested their lifestyle, marriage, business, or emotions under financial pressure. Recessions are behavioral events disguised as economic events. The real problem is that they don’t have a system for handling fear. A recession exposes behavior, relationships, debt problems, overspending, and unrealistic lifestyles all at once. That’s why resilience matters more than prediction.”

He continues, “The most common mistake I see is people trying to predict the economy instead of preparing for uncertainty, trying to ‘outsmart’ recessions instead of outlasting them. They panic sell, move everything to cash, freeze up, stop investing, or make huge financial changes based on headlines and fear. Then, six months later, the world hasn’t ended, and the market recovers without them, but the damage from their reaction is permanent. I’ve seen people sit out rallies for years because they emotionally froze during a downturn. What felt ‘safe’ in the moment destroyed long-term wealth. Fear makes people feel productive while they’re sabotaging themselves.”

The real damage from recessions is caused by:

- Losing your job and being unable to find a new job with a similar income.

- Being over-concentrated, e.g., when a large part of your portfolio is tied to your employer, so if that employer suffers, you could lose your salary and much of your net worth at the same time.

- Making panic-driven decisions, or on the flip side, suffering emotional paralysis that prevents you from making rational decisions.

- Lacking liquidity, which can force you to sell assets at a loss in a bear market.

Crane identifies the things that help survive recessions intact: “The people who survive downturns best are usually the people with margin. Multiple income streams, lower fixed expenses, manageable debt, and cash reserves that buy them time to think clearly, as well as adaptable skills, strong relationships, and the emotional ability to pivot when things get ugly. Everyone focuses on investments, but most financial stress during downturns comes from a lack of flexibility. If your lifestyle requires every dollar of income to survive, even a small disruption feels catastrophic.”

The lesson may be uncomfortable, but it’s critical if you want to be in that group Crane describes.

Before anything else, you need to figure out if your financial safety requires everything to work perfectly.

Because recessions expose people’s fragility far more often than they create it.

Stress-Test Your Financial Life Before the Economy Does It for You

Far too often, we take financial success for granted.

We’re so used to our current spending levels and lifestyle that we don’t realize how financially rigid and vulnerable we’ve become.

Until something happens that shakes apart your financial life.

Ryan Veldhuizen, MS, CFP, Founding Principal of Catalyze Wealth Management, advises, “If you want to become more financially resilient over the next 6 to 12 months without making drastic changes or trying to predict the market, the most useful thing you can do is build margin. I define financial margin as the sum of savings and discretionary expenses divided by net after-tax income, and I target 35–40% for my clients.

“While that may initially seem far too big in percentage terms, it actually looks quite reasonable since it only affects the edges of our lives. But it has a huge impact on how cluttered and stressful, or how organized and flexible our lives are. Much like standard one-inch document margins don’t look very large, despite using 37% of the page, and without this margin, the document would be cluttered and overwhelming.”

If most of your income is “spoken for” before the month even starts, you’ve painted yourself into a corner, where even a short-term income drop can become a major problem.

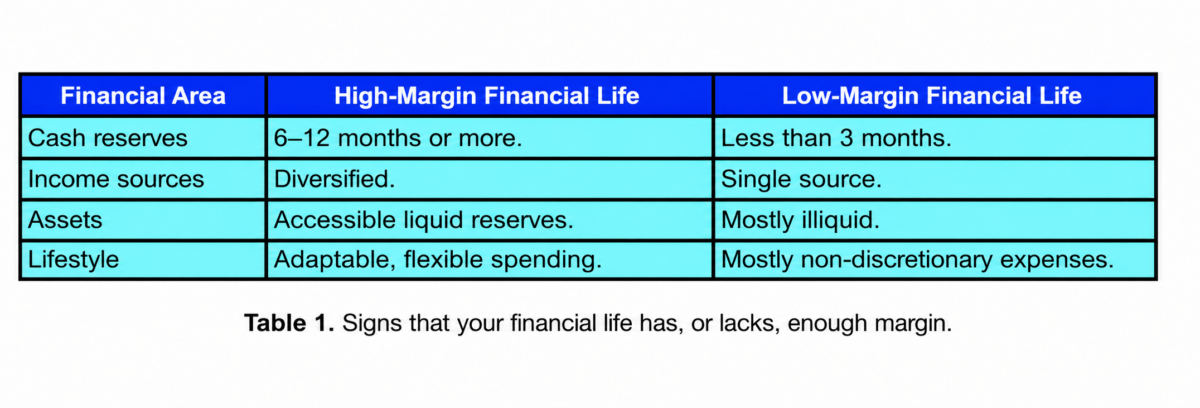

If you want to know how vulnerable your financial life is, ask yourself:

- How concentrated are your income sources? Could you survive six months or longer if you lost a paycheck?

- How much of your spending is non-discretionary (think mortgage or rent, utilities, health insurance, auto loan payments, and groceries) vs. discretionary (e.g., travel, gifts, donations, etc.)

- Can you raise money in a hurry, or are your assets mostly illiquid (e.g., home equity)?

The answers to those three questions will tell you if you’d likely be forced into major financial decisions quickly if conditions worsen (see Table 1).

Take paying down debt.

Even with no recession in sight, paying off high-interest debt as quickly as possible should be one of your highest financial priorities.

As Veldhuizen says, “Debt matters more than most people realize, not primarily for the interest savings, but because every liability you eliminate lowers the floor your income has to cover.”

However, while paying down debt and lowering your required “income floor” improves resilience, draining your cash reserves to eliminate debt also reduces your liquidity and flexibility, which can be critical if you lose your job before rebuilding your reserves.

Veldhuizen reiterates the importance of having enough margin, saying, “A family with 35% margin can absorb extended unemployment without selling the house, invest opportunistically when others are fearful, and make a career change or weather an emergency without the most important expenses ever being in question. Those who are intentional about building margin in their finances will benefit during economic growth and during economic downturns.”

He then adds, “Margin is built in three ways: controlling fixed expenses, maintaining meaningful cash, and diversifying away from your own income concentration.”

Once you build that margin, you have more breathing room, adaptability, and space for emotional clarity.

Personally, I never consciously “prepared for a recession.” In fact, I probably leaned harder into long-term investing and less into liquidity than I should have.

Yet looking back, the things that protected me during downturns had nothing to do with predicting the economy or timing the market. They had more to do with maintaining my employability, preserving professional relationships, and building adaptable skills, all of which helped when my consulting business suffered an 80% loss of revenue for a year, and avoiding the sort of poor financial decisions, such as high-interest debt, that would have trapped me when my income suddenly changed.

Build an Opportunity Fund Before You Need One

Having a solid emergency fund is a well-known tenet of financial preparedness.

Conventional financial advice says we should have at least 3 months’ worth of expenses in a liquid and low-risk asset, such as a high-yield savings account.

Depending on how stable your situation is, how strong a safety net you have, and how many responsibilities you carry, that recommendation can grow to 12 months’ worth of expenses or even more.

Yet, the National Association of State Credit Union Supervisors (NASCUS) reports that fewer than half of Americans (47%) can cover a $1000 emergency expense.

As Deb Meyer, Founder of WorthyNest®, says, “Whether a recession is on the horizon or not, cash is king. Most people have an emergency fund of, at best, a few thousand dollars tucked away for unexpected expenses like car repairs, home appliances, or medical bills.”

However, she then points out that having greater liquidity results in greater optionality and more freedom. She says, “Yet very few people have a sizable opportunity fund. An opportunity fund allows you to take a mini-sabbatical between jobs, helps you start the business you’ve always dreamed of pursuing, or provides ample breathing room for the home project you’ve been meaning to do for years.”

Meyer then expands on the importance of building such an opportunity fund, and the sooner the better: “There will always be items outside of our control. Political unrest, life-threatening weather events, and stock market movements are just a few examples of things we cannot control. However, you do have the power to control your decisions around how much money to save, spend, or give. You can also control how you will react if a recession arrives: either calm or panicked. Having a substantial cash opportunity fund provides peace during a very uncertain time. To improve your financial resilience in 2026, start an opportunity fund.”

Indeed, having greater optionality preserves and opens up choices, and it can even help you build wealth.

As T. Casey Loper, CFP®, Wealth Advisor at Cornerstone Wealth Management, points out, “It’s not a matter of if a recession or a market drop comes, it’s a matter of when. We teach all of our clients to expect them to come often and be prepared to take advantage when they come. Having some money in fixed accounts to buy when bargains are available will always help one go from surviving to thriving in the next downturn or recession.”

A higher net worth doesn’t automatically provide rapid-response optionality.

For example, if much of your net worth is trapped in your home equity, you’re caught in “cash-poor” vulnerability.

Real estate investments can be very profitable, but they are illiquid, which can pose a challenge in difficult times.

Meyer explains, “Many clients who achieve a certain level of financial success inevitably ask if real estate is a wise investment. And usually, my answer is no. It’s an illiquid asset that can be extremely difficult to sell, especially in a recession. One exception? If it consistently generates income and is an asset that will be passed down to the next generation.”

“For retired clients or those nearing retirement,” Meyer adds, “I’d much rather see a diversified mix of liquid assets that can be sold at a moment’s notice if necessary. Real Estate Investment Trusts (REITs) provide a similar experience to tangible real estate ownership with greater liquidity.”

Other risk factors that make you vulnerable in a downturn include:

- Concentrated stock compensation that isn’t diversified as quickly as possible.

- Highly leveraged investments that can result in a dreaded “margin call.”

- Private business ownership, when the business is in a recession-sensitive industry.

- A lifestyle built around a permanently high income.

Crane warns against acting on recession fearmongering, “Recession preparation should not feel like hiding in a bunker waiting for collapse. It should feel like building a life that can absorb stress without completely falling apart.”

He then suggests a more positive way to prepare: “If you want to become more resilient over the next year, stop obsessing over predictions and start improving adaptability. One thing I strongly encourage people to do over the next 6–12 months is to build optionality into their lives. Build cash flow flexibility. Lower unnecessary stress. Increase liquidity. Reduce unnecessary financial obligations. Improve skills or income streams. Tighten weak areas of your financial life before the economy forces you to.”

How Recession Risk Differs for Employees, Business Owners, and Retirees

If you read most recession-prep advice, I’m sure you’ve noticed how generic it all sounds.

It rarely discusses how your strategy should depend on your life stage, your income type, and your existing liquidity and flexibility.

Different people face different risks in a recession, and they often don’t even look at the right ones.

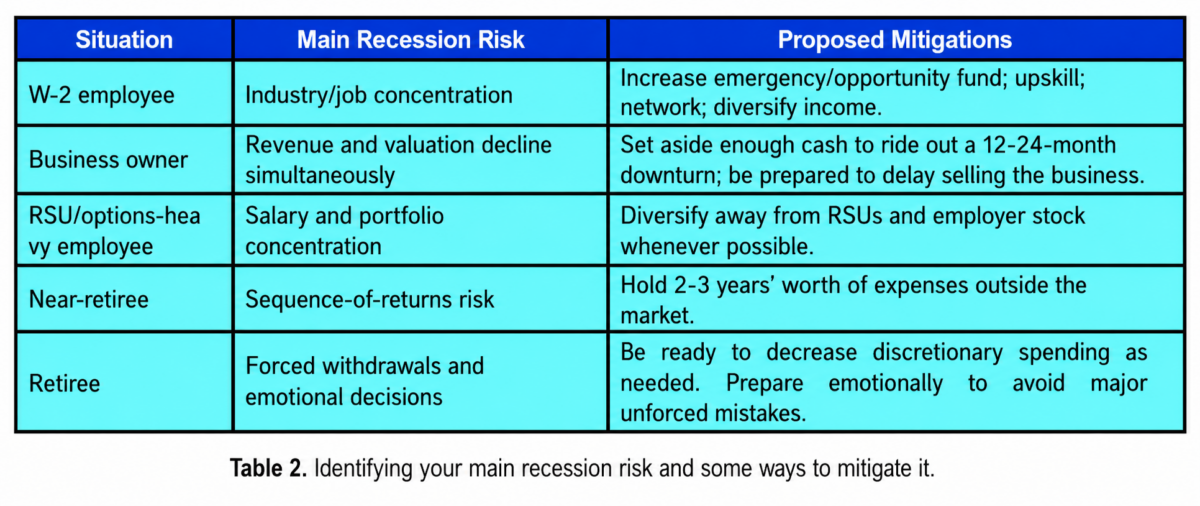

As Jim Crider, CFP®, Founder of Intentional Living FP, says, “Most recession worry is misdirected. The W-2 employee fretting about the S&P 500 is usually overexposed to their employer’s industry, not the overall market. The business owner watching the news is concentrated in an asset that’s both their income and their nest egg. The near-retiree fixated on returns is actually exposed to sequence risk. Good prep starts by naming the real concentration, not the one that’s loudest in the headlines.”

He then elaborates on the different risks and how to mitigate them, “Here’s how that plays out in specific situations:

- “Business owners: Recession hits twice. Revenue drops at the same time as the business is worth less if you try to sell. The real prep isn’t trimming portfolio risk. It’s building personal liquidity outside the business so you can ride out 12 to 24 months without forced distributions or panic decisions about staffing, pricing, or your own compensation. If a 2027 sale was your retirement plan, a downturn can push it out three years and cut the price 30%. Plan to be patient by being liquid.

- “High earners with Restricted Stock Units (RSUs) or stock options: The mistake is treating vested shares as diversified wealth. They aren’t. You’re double-concentrated in one company that also pays your salary. Recessions reveal that. The fix isn’t to predict the next downturn; it’s building a disciplined sell-at-vest schedule and a real cash bucket before you need it, so a layoff doesn’t force you to sell vested shares at a five-year low.

- “Near-retirees: Sequence-of-returns risk is the actual enemy, not recession. Two to three years of living expenses outside the market (not just an emergency fund, actual spending cash) keeps you from being a forced seller in Year 1 of retirement. Bonus: a real downturn opens a window for Roth conversions at depressed account values, which is one of the few tax moves that gets better in a bad market.

- “Already retired: Spending flexibility matters more than nailing the withdrawal rate. Clients who can dial back the discretionary line, the travel year, and the truck upgrade recover faster than those running a rigid budget. Build the flex in before you need it.”

Crane agrees, “The specific advice changes dramatically depending on the person. A W-2 employee may need greater cash reserves and skill flexibility. A business owner may need to focus on reducing operational fragility and personal lifestyle creep. High earners living off RSUs and stock options often think they’re diversified when they’re actually massively concentrated, so they need to sell during liquidity events. Near-retirees need to focus heavily on sequence risk and income structure, while fully retired people usually need emotional guardrails more than aggressive portfolio changes.”

Table 2 captures these different situations, their real recession risks, and ways to mitigate those risks.

As Veldhuizen puts it, “Every client’s situation is unique, and clients are quick to remind me of this, which always makes for a great discussion during our meetings. Rules of thumb too often assume everyone has the same thumbprint. Targeting a 35–40% margin is a starting point, not a final answer. Its value is in forcing the question: where is the actual flexibility in my financial life? The answer looks different for a retiring professor than for a Series B founder, but the process of intentionally thinking it through and identifying areas to improve your financial margin will build greater financial resilience.”

He then explains how his above-mentioned margin formula, “… sum of savings and discretionary expenses divided by net after-tax income…” applies differently in different situations:

- “The framework applies cleanly to W2 employees.

- “The framework applies to business owners, too. When distributions are strong, discretionary spending tends to rise, and using the formula might calculate an 80% margin in a good year. That number isn’t the point. The point is that the margin should be calculated on income that is repeatable and spendable, not enterprise value that hasn’t been realized, not a distribution year that tripled because the business had an exceptional quarter. If distributions compress and there’s no personal cushion, the business risk fully transfers to the household. If anything, business owners need either higher margin targets or sufficiently realistic estimates of the durability of their income during a slow year or an economic downturn.

- “Even in cases where the formula might seem inapplicable, the principle still applies. For example, a physician finishing residency with a reasonable expectation of a 5× salary increase in two years is making the most valuable investment available to them, themselves. Maxing out qualified retirement savings on a resident’s salary would be the wrong advice. Even so, I find that discretionary expenses in this phase tend to be proportionally larger, which preserves the spirit of the framework even when one of the variables, savings rate, is likely zero.

- “For retirees in the distribution phase, savings drop to zero, and the formula becomes discretionary expenses divided by after-tax sustainable portfolio withdrawals. Two adjustments are made to get there: savings disappear from the numerator, and the focus is on non-guaranteed income sources, which don’t include Social Security and pensions. It’s a small tweak, but a retiree drawing from their retirement portfolio can still quickly calculate their financial margin using this framework.”

How to Improve Your Financial Resilience in the Next 12 Months

As the financial experts quoted throughout this article repeatedly emphasize, the best recession prep is reducing fragility, increasing adaptability, and preparing yourself to make good decisions before economic stress fractures your life.

Here are some specific ideas for each of these.

Steps to Reduce Financial Fragility Before a Recession

- Reduce fixed obligations and recurring expenses as much as you can, before loss of income makes them hard to cover.

- Reduce discretionary spending before you need to and use the money that’s freed up to bulk up your emergency and opportunity funds.

- Diversify over-concentrated investments and compensation.

- Keep high enough liquid reserves (i.e., the above emergency and opportunity funds).

- Pay down high-interest debt, but not to the point that you become cash-poor.

- Take on responsibilities that directly support your supervisor’s priorities, making it less likely that your job will be among the first to be axed.

How to Increase Your Financial Adaptability

- Update your resume now, before you need it.

- Network to strengthen professional relationships, especially ones outside your current employer.

- Build marketable skills to increase your employment flexibility.

- Consider starting a side gig to diversify your income.

How to Make Better Financial Decisions During a Recession

- Create financial rules and emotional guardrails for yourself, and practice them before panic arrives.

- Avoid doomscrolling and headline-driven financial decisions. Remember that the media publishes what they think will get your attention, which is not necessarily what helps you. They also drive attention by sensationalizing and catastrophizing.

- Recognize that fear often creates urgency that feels rational in the moment, especially when it isn’t.

- Focus on outlasting downturns rather than trying to outsmart them.

What to Do If Income Drops

Mike Tyson is often (though not accurately) quoted as saying, “Everyone has a plan, until they get punched in the face.”

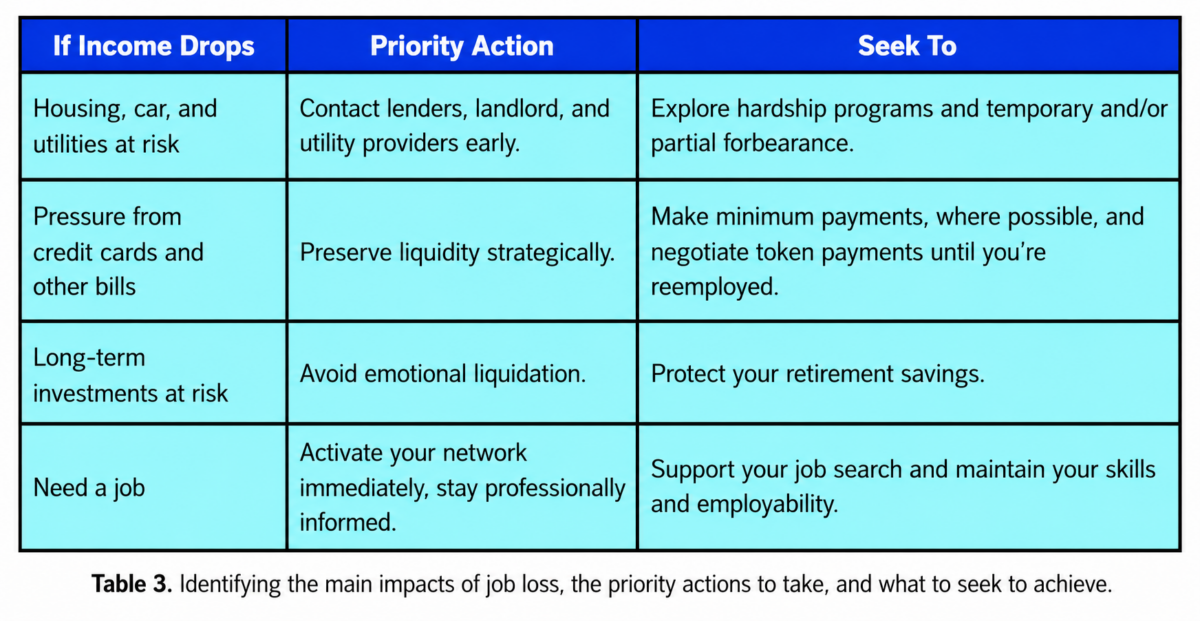

In that spirit, let’s assume that despite all your planning and preparing, a recession causes the worst to happen to you, and you lose your job. The more you did beforehand along the lines of the above recommendations, the better you’re positioned to survive this. Still, there are things you can do after losing income that can help.

- Prioritize essential obligations, like your mortgage, rent, auto loan payments, and utilities. However, contact lenders (or your landlord) and your utility providers early to explore hardship programs or temporary and/or partial forbearance.

- To preserve liquidity, consider making minimum payments where possible and putting off payments of bills that are less likely to damage your credit. For example, if you have medical bills, reach out to the provider(s), explain the situation, and offer to make token payments until you’re employed again. Interest is expensive, but it may be the lesser evil if it’s temporary and helps maintain liquidity as a survival tool.

- Avoid liquidating long-term investments, especially during a market crash, until and unless it becomes unavoidable. Replacing long-term investments after panic-selling them during a downturn can take years.

- Avoid isolating yourself professionally. If anything, hard times are a reason to network more actively, not less, and staying on top of developments in your field will make it easier to get your next job (or start your own business).

Table 3 summarizes what’s at risk due to job loss, what priority actions to take, and what to pursue as mitigation and/or solution.

The Bottom Line: Outlast, Don’t Outsmart

Recessions are a normal part of the economic cycle. That’s why it isn’t a matter of if there will be a recession, just when.

And that “when” is impossible to predict accurately.

As Physics Nobel laureate Nils Bohr once quipped, “It’s very hard to make accurate predictions, especially about the future.”

Given that, our job isn’t to predict the next recession. It’s to reduce our financial fragility and build enough resilience to survive it with as little damage as possible.

And the fact that recessions are usually shorter than a year makes that doable.

Margins and resilience have to be built ahead of time, not when the downturn already hits. At that point, what you built, or failed to build, gets revealed.

And if you managed to build enough resilience into your finances and emotional preparedness, you’ll do well.

As Crane puts it, “The people who usually come out strongest after difficult economic periods are not the ones who predicted everything perfectly. They’re the ones who stayed adaptable, disciplined, and emotionally steady while everyone else reacted impulsively.”

Your goal can’t be to outsmart recessions.

It has to be building a financial life resilient enough to outlast them.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher