Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

So I get some version of this question in almost every meeting with parents. “How do we even start financial planning for a child’s college?” And honestly, it usually comes with a little bit of tension in the voice, because college costs feel like this enormous, moving target. Keep in mind, though, that this is one of those goals where a little structure goes a long way. You don’t need a perfect plan. You need a reasonable one that you can adjust as you go.

Let’s Define What We’re Actually Planning For

The way I think about it is that “college planning” really means three separate things happening at once: saving money in the right kind of account, understanding roughly what you’ll need, and deciding how much of the cost is actually yours to cover. Those are three different conversations, and a lot of the anxiety I see comes from trying to solve all three at the same time.

For example, a family I worked with a while back kept putting off opening a savings account because they hadn’t figured out whether their child would go to a state school or a private one, or whether there’d be scholarships involved. That’s an understandable instinct, but it’s also backwards. You don’t need the destination locked in before you start saving. You just need to start.

Here’s What the Research Actually Suggests

Research suggests that time in the market matters more than timing the market, and that principle applies just as much to college savings as it does to retirement.¹ A 529 plan, which is a tax-advantaged account designed specifically for education expenses, tends to be the most commonly used tool for this. Generally speaking, the money grows tax-free, and withdrawals aren’t taxed either as long as they’re used for qualified education expenses. If you want a deeper walkthrough of how these accounts work, Saving for College’s guide to 529 plans is a solid, unbiased resource.

That said, a 529 isn’t the only option, and it’s not automatically the right one for every family. Some parents prefer more flexibility, since 529 funds are meant for education specifically. Others like the structure it provides, because it keeps the money separate from everyday accounts and harder to dip into for something else. There’s no universally correct answer here. It really depends on your goals, your income, and how disciplined you are with separate savings. If you’re weighing a 529 against other investment vehicles, our piece on target date funds covers some of that same “how much do I need to manage myself” tradeoff.

What This Means in Plain English

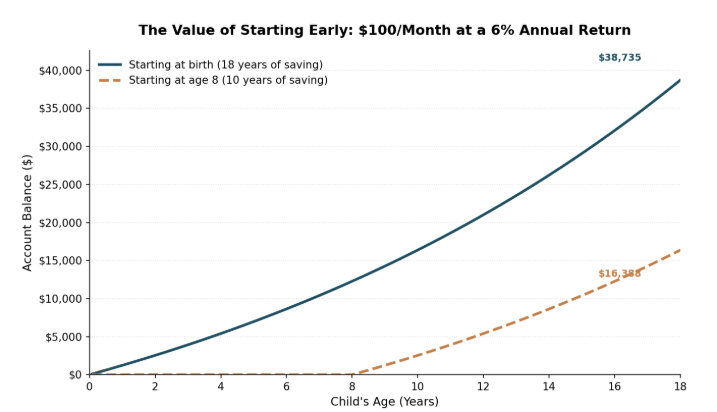

What this means in practice is pretty simple: open an account, even a small one, and set up an automatic contribution. It doesn’t need to be dramatic. Fifty dollars a month started early tends to matter more than five hundred dollars a month started late, simply because of how compounding works over time. The earlier you begin, the more time your contributions have to grow on their own, without you having to do anything extra.

Here’s what that looks like in practice. The chart below compares two families contributing the same $100 a month, at the same 6% hypothetical return, but starting at different points.

One thing to consider is that the goal was never to cover every dollar. It’s to reduce how much your child has to borrow later, and to give them real options when the time comes. Falling short of “the whole thing” isn’t the same as falling short of the goal.

The Behavioral Side of This, Which Matters More Than People Expect

One thing to consider is that money decisions are emotional before they’re mathematical, and college savings is a great example of that. Parents often carry some guilt around this topic, especially if they started late or if life got in the way of consistent saving. I’d gently push back on that feeling. Behavior matters more than any single decision you made or didn’t make five years ago. What matters now is the pattern you build going forward.

Another thing to consider is your child’s own relationship with money as they get closer to college age. Involving them in the conversation, even in a small way, tends to help. That doesn’t mean handing over spreadsheets to a twelve-year-old. It means talking openly about tradeoffs, so that by the time they’re choosing a school, they understand that cost is part of the decision, not something that magically works itself out. This is really an extension of the broader idea we wrote about in Family Finance: Building Savvy Money Skills Together, where money conversations across generations tend to go better the earlier and more naturally they start.

A Practical Framework for Financial Planning for a Child’s College

So, what does this look like in practice? Generally, I’d suggest starting with three questions rather than trying to build a full financial model right away.

First, how much can you comfortably contribute each month without straining your other goals, like retirement or an emergency fund? That second part matters. Retirement savings should almost always come before college savings, because your child has other ways to pay for school, like loans or scholarships, but there’s no loan for retirement.

Second, what account makes sense given your state’s tax rules and your comfort with flexibility? A 529 plan is worth researching, and many states offer a tax deduction or credit for contributions, which can make it even more attractive. You may want to read What College Savings Plan is the Best, to further refine which account makes sense for your family.

Third, how will you talk about cost expectations with your child as they get older? This one gets skipped a lot, but it’s arguably the most important. A family conversation in ninth or tenth grade about what’s realistic can prevent a lot of stress during senior year, when college choices start to feel very real and very final.

On the Other Hand, Don’t Let Perfect Get in the Way

That said, I’d caution against over-optimizing this. I’ve seen families spend so much energy trying to find the perfect savings vehicle or the perfect projected cost that they delay actually starting. The reason for that is understandable. College costs feel unpredictable, and it’s uncomfortable to commit money toward something with an uncertain price tag years in the future. But waiting for certainty usually means losing time, and time is the one resource you can’t get back in this particular goal.

Where This Leaves You

Ultimately, financial planning for a child’s college is less about hitting a specific number and more about building a habit that grows alongside your child. Some years you’ll contribute more, some years less, and that’s normal. What matters is consistency over the long run, paired with a plan you actually revisit rather than one that sits in a drawer.

Keep in mind, there’s no single “right” amount to save or a magic age to start. What matters most is that the plan reflects your actual life, your income, and your other goals, not just an abstract target you saw somewhere online. You don’t have to figure all of this out today. You just have to take the first step, and then keep showing up for it.

If you’re not sure where to start, that’s a completely normal place to be. At BlackBird Finance, we can walk through the numbers together and figure out what makes sense for your specific situation.

Source

1. J.P. Morgan Asset Management, “Back to School: 3 Principles for Your Portfolio,” analysis of S&P 500 returns and the impact of missing the market’s best trading days over a 20-year period.

This article reflects the insights and opinions of its author and is not a recommendation or endorsement of their views or services.

About the Author

Nathan Mueller, MBA, CFP® | Blackbird Finance

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor