Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Have you started thinking about retirement and begun to worry about what life in retirement will be like if you don’t build a whopping big nest egg?

Experts estimate a comfortable retirement requires $1.04 million dollars saved up. Factor in even a few years of high inflation and a couple of decades of average inflation, and that million could easily quadruple!

That’s a tall order, but if you’re smart about it and avoid major investing mistakes, it’s very doable.

In this article, we’ll detail several of the worst investing mistakes that could derail your retirement dreams and how to overcome them to achieve your savings goals.

Too Little Too Late

Compound interest has been called “the 8th wonder of the world,” “mankind’s greatest invention,” and “the strongest force in the universe.”

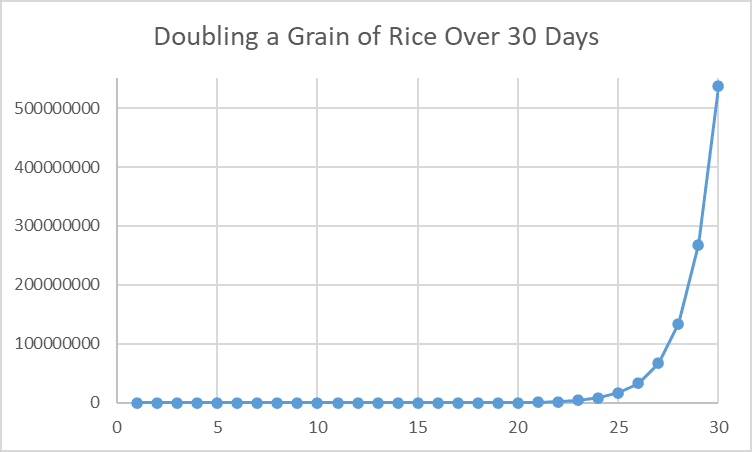

Possibly the most famous story about compounding is the fable of a grain of rice.

Briefly, a clever young girl outsmarts a miserly raja. When he offers her a reward for a good deed, she asks for just a single grain of rice, and then each day for 29 more days, double the previous day’s rice.

On Day 2, she got 2 grains.

Day 3, 4 grains.

Day 4, 8 grains.

Day 5, 16 grains.

…

On Day 30…

… the young girl received over 500 million grains, for a total of over a billion.

Adapting the story to more modern times by changing the grain of rice to starting with a single penny, by the end of a month, the total is over $10 million!

Of course, doubling your money every day, or even every year, is pure fantasy. Still, the story demonstrates how compound interest can turn small sums into a major fortune.

The flip side is that if you delay investing for retirement by 10 years, starting at age 32 instead of 22, you need to nearly double your annual investment to reach the same amount. Delay to age 42, and the required annual investment more than doubles again.

That’s why starting “Too Late” is a major mistake. The “Too Little” part is self-explanatory.

Playing It Safe

Many people look at the stock market with fear. They hear about (or experienced first-hand) losses of 50% or more in a single year.

As a result, they play it “safe” with their retirement savings, keeping them in cash or bonds.

The problem is that over a 45-year investing career, assuming the 3.5% long-term average annual inflation, your investment would lose nearly half its value. Set aside $1000 each year for 45 years for a total of $45,000 saved, and keep it in cash, and you’d end up with less than $23,000.

Bonds are a bit better, with a 1.9% average inflation-adjusted annual return. Here, $45,000 invested over a 45-year period would get you over $70,000.

Not bad, right?

Compare it to stocks though, with a historic average inflation-adjusted return of 6.6%. Here, your $45,000 turns into over a quarter-million dollars!

This means that if you don’t want to have to set aside 3.6x more each year (if you even could), keeping your money “safe” in bonds would cut your retirement income by more than 70% compared to stocks!

Ignoring the Nickel-and-Diming of Fees

Erroneously attributed to Mark Twain, an often-repeated quip says the surest way to get rich during a gold rush isn’t to prospect for gold but to sell overpriced picks and shovels to those pursuing unsure fortunes.

This is what some financial institutions, wealth managers, and investment advisors do. They provide investment advice to people seeking an uncertain fortune through investments and charge a fee for that service. While there’s absolutely nothing wrong with doing so (in effect, selling shovels at a fair price), some charge unjustifiably high fees that come out of your pocket, whether their advice adds value or not.

For example, many mutual funds charge a sales fee, or “load,” to pay commissions to financial advisors who bring them investors. Say you pay an advisor to choose a fund for you to invest in. Given two similar funds to choose from, one which pays him $5 for every $100 you invest, and another that pays him nothing (a “no-load fund”), the advisor invests your money in the former. As a result, if you invested $10,000, you own $9500 worth of shares, and the advisor pockets $500 of your money.

If load funds tended to outperform no-load funds by a wide enough margin, this would be acceptable. However, as finweb.com says, there is no evidence for such outperformance. Indeed, there’s ample evidence to the contrary.

Letting Emotions Rule You

A humorous, but highly instructive story was reported in 2014 by Business Insider. In a Bloomberg Radio show, a guest related the following:

“Fidelity had done a study as to which accounts had done the best at Fidelity. And what they found was…“

“They were dead,” interjected the interviewer.

“…No, that’s close though!” responds the guest. “They were the accounts of people who forgot they had an account at Fidelity.“

Numerous studies show time and time again that mutual fund investors underperform the very funds in which they invest.

How is this possible?

Simple.

Investors act on fear, panic selling when they should hold on. They then act on greed, buying a “hot fund” after it’s run up a lot and is poised for losses. That’s how emotion-driven trading can hurt your long-term results.

David Berns, Financial Planner, Truadvice Wealth Management, points out, “Behavioral finance shows us how emotions drive decisions. We all watch the news, but once you realize they’re selling ad revenue, your perspective changes. Gone are the days of ‘only reporting the news’ without anyone’s opinions. Understanding your own risk tolerance and how it aligns with your retirement goals are key.”

Putting All Your Eggs in the Same Basket

Twenty years ago, energy trader Enron, then the nation’s 7th-largest company, became an object lesson in the folly of putting all your eggs in the same basket.

The company loaded its employee’s pensions with Enron stock.

When the company’s accounting tricks couldn’t hide massive losses anymore, shares dropped from $80 to pennies. As NPR reported, “All told, Enron employees [were] out more than $1 billion in pension holdings.”

On top of that, 14 thousand employees lost their job as the company imploded.

Most money managers will tell you to avoid holding more than 10% of your portfolio in a single company (if it’s your own company, things may be different). How much more so, when your portfolio is invested 20%, 30%, or more in your employer’s stock?

There, if the company goes under, your portfolio suffers a massive “haircut,” your pension, if any, may become worthless, and you lose your job, all at the same time.

David Barfield, CFP®, Founder / Financial Planner, Datapoint Financial Planning, LLC shares, “My financial planning practice primarily serves tech professionals, and the most common mistake I see is over-concentration in technology stocks. I was guilty of this mistake myself early in my prior career in technology. In the late 90s I loaded up on all the hot tech names and watched many of them go to zero in the dotcom bust. Fortunately, I learned this lesson early enough that, while painful at the time, it helped me in the long run. When I see clients making this same mistake today, I use my experience to help them see the dangers, but it doesn’t always work.”

Jorey Bernstein, Executive Director, Wealth Manager and Founder, Bernstein Investment Consultants shares, “This reminds me of something one of my Johns Hopkins economics professors, Dr. Hanke, told me in 1984. He said, ‘Jorey, they say there’s no free lunch on Wall Street, but that’s not true. There is a free lunch. It’s called diversification.’ Dr. Hanke and I are still friends to this day, and I think of that quote every time I forget to diversify enough.”

Following the Herd

In John Bogle’s Little Book of Common Sense Investing, Warren Buffet is quoted as saying, “A low-cost fund is the most sensible equity investment for the great majority of investors. My mentor, Ben Graham, took this position many years ago, and everything I have seen since convinces me of its truth.”

Indeed, if you have no idea about investing, following the herd by investing in the entire market will have you beat many, if not most, active investors.

However, you’re guaranteed to slightly underperform the market (due to management fees).

If you educate yourself on investing, you can find a system that works for you and lets you outperform the market for a very long time, allowing a richer, more comfortable retirement.

Similarly, conventional wisdom suggests you gradually become more conservative with your investments as you grow older and near retirement. Common options of “glide paths” would have you keep your stock allocation at 100 minus your age (so you’d have only 33% in stocks at age 67), or 110 minus your age, or 120 minus your age.

So-called “target-date funds” follow different glide paths, but all reduce your stock allocation as their target date draws near, and some even continue reducing their stock allocation after that, when you’re presumably already retired.

CNBC reports that these funds account for $1.8 trillion invested for retirement!

While these funds give you a simple investing solution, their “one size fits all” approach fits many very poorly indeed. Depending on what else you invest in, and what other mitigations you may have in place for a market crash as you near retirement, a target date fund may be too aggressive for you, or the opportunity cost may be higher than it needs to be.

Leaving Money on the Table

Most American workers have access to an employer 401(k) or 403(b) plan, and most employers offer a match for employee contributions. Some are very generous (when I worked at the University of Maryland, we got 7.25% of our pay added to our 403(b) plans, even if we contributed nothing).

Others offer a $0.50 on the dollar match up to a 6% employee contribution. There, if you earn $50,000 a year, and contribute $3000, your employer throws in an extra $1500. This gives you $1500/year of free money, immediately giving you a 50% return on your investment.

Despite this, studies show that on average, employees leave $1300/year of this free money on the table by not contributing enough to maximize their employer’s match.

Stealing from Yourself

Many 401(k) plans allow you to borrow from yourself at lower interest than you’d pay the bank. Indeed, the interest you pay goes back into your 401(k), since that’s where the money comes from.

However, if the interest is lower than the returns on your 401(k) investments, you just stole money from yourself through opportunity cost.

Worse, if you lose your job before you paid back the loan, or you’re simply unable to pay it back, your retirement funds just took a big hit, and to add insult to injury, the IRS will charge you a 10% penalty and taxes on what has become in effect an early withdrawal.

Similarly, many workers raid their old 401(k) funds when they leave a job, rather than rolling them over. Again, this robs their future selves, and they have to pay penalties and taxes on top of it.

Inflating Your Lifestyle

Most workers’ income grows over their careers. This is because they become more skilled and experienced and/or because they’re able to move to better-paying jobs.

If you start off making $40,000 a year and manage to score a $10,000 increase through a promotion or moving to a different employer, you have a choice.

You could use the extra income to increase your standard of living, what’s known as “lifestyle inflation,” or you could divert part or all of the extra income to increase your savings and investing rate.

For many years now, I’ve tried to divert 2/3 of each income increase to my investments, to great effect. By letting myself spend at least some of the increase, I balance this with enjoying some of the fruits of my labor in the present, making this sustainable.

Grabbing the Money Too Early

As another example of leaving money on the table, many Americans claim Social Security benefits as early as they can, at age 62. According to the Social Security Administration (SSA), this can cost them nearly a third of their monthly benefits for life. On the flip side, says the SSA, delaying benefits to age 70 increases monthly benefits by at least 24% for life.

Many people are forced to claim early due to forced early retirement, and many others benefit from early claiming as their ill health makes it likely they won’t survive long enough to make late claiming viable. However, many others who claim early are simply eager to start getting money earlier, at a great eventual cost to their financial health.

Ignoring the Tax Man

While many rail against taxation as an unjust seizure of our money, I firmly hold that taxes (at reasonable levels) are a necessary evil. That’s how we fund things like our national defense, federal and state responses to emergencies, the highway system, etc.

Of course, there’s plenty of waste, and many cases where lawmakers stuff unnecessary “earmarks,” also known as “pork,” into legislation. However, that’s a small part of the federal budget.

Regardless of whether you agree with me or not, you have to pay your taxes if you want to avoid going to jail (e.g., mobster Al Capone famously evaded conviction on countless cases of murder and mayhem, but was ultimately undone on tax evasion charges).

While tax evasion is illegal and will drop you in hot water, tax avoidance is perfectly legal. The International Tax Blog offers two relevant quotes from rulings by Judge Learned Hand.

“Any one may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury; there is not even a patriotic duty to increase one’s taxes.” Gregory v. Helvering, 69 F.2d 809, 810 (2d Cir. 1934)

“Over and over again courts have said that there is nothing sinister in so arranging one’s affairs as to keep taxes as low as possible. Everybody does so, rich or poor; and all do right, for nobody owes any public duty to pay more than the law demands: taxes are enforced exactions, not voluntary contributions. To demand more in the name of morals is mere cant.” Commissioner v. Newman, 159 F.2d 848, 851 (2d Cir. 1947) – dissenting opinion

There are multiple tax-advantaged ways of saving and investing for retirement, and if you don’t take advantage, your retirement will be far less comfortable.

These include Roth IRAs and Roth 401(k) plans, where you contribute after-tax money, but both the contributions and every penny they make are all tax-free. They also include traditional IRAs, SEP IRAs, SIMPLE plans, and 401(k) plans, where you contribute pre-tax dollars and don’t have to pay any taxes until you withdraw money, and even then, only on those withdrawals.

Best of the lot are Health Savings Accounts (HSAs), where you contribute pre-tax dollars, they grow tax-free, and withdrawals are tax-free as well, so long as they’re used to pay for medical expenses. Given how the average retired couple can expect to pay over $300,000 in medical expenses, it’s a good bet that HSA money can all be spent tax-free.

Ask the Experts: Financial Advisors Suggest Investing Mistakes to Avoid

For additional insights, we invited financial advisors in the Wealthtender community to share investing mistakes they sometimes hear among people not yet working with a financial advisor. Here’s what they said:

“Target-date retirement funds are a great innovation and make sense for many 401(k) participants, but one mistake I see is people remaining in them as they approach and enter retirement.

“Target-date funds are indeed well-diversified, but they have a single net asset value (a single price). So when you need a withdrawal you have to sell a bit of everything, instead of being strategic and selling the things that are either up most or down least. The riskiest day of your investing life is the day you go from accumulating assets to living off of them. As soon as some of your money becomes short-term money you need to adjust your investment allocation strategy.”

– Stephanie McCullough, Founder, Sofia Financial | Wealthtender Profile

“I have seen investors in or approaching retirement, clutch onto a holding in their portfolio that doesn’t match their objectives or that may never perform how they had hoped, because they are holding out for that “Hail Mary,” that highly unlikely possibility that they see as the only way they won’t outlive their money.

“Some hold an investment for sentimental reasons, or because of pride, even if they continue to lose money as opposed to accepting the new reality and moving forward. In cases like this, where investors are anchoring, they aren’t listening and adjusting to the moment at hand.”

– Michael Raimondi, Wealth Manager, Clarus Group | Wealthtender Profile

“One of the biggest investing mistakes I see people make is to invest based on the “noise” from those around them. Everyone has an opinion on stocks, crypto, etc. But the most successful investing plans are often very boring. There’s nothing sexy about investing every month into a mutual fund for 20 years it’s often the most reliable way to get the results you want.”

– Michael Reynolds, CSRIC®, AIF®, CFT-I™ | Elevation Financial | Wealthtender Profile

Trying to Time the Market

Possibly the greatest investor of all time, Warren Buffet credits Graham’s teachings for his incredible success. Among other things, Buffet quoted Ben Graham as having said, “In the short run, the market is a voting machine but in the long run it is a weighing machine.”

Since it’s impossible to know everything about an investment (short of illegal insider trading), timing the market requires you to guess correctly the market’s lows (to buy in), and its highs (to sell).

Jesse Carlucci, PhD, CFP®, Chief Investment Officer, Arrow Investment Management agrees, “One of the most common mistakes I see investors make is trying to time the market during periods of volatility in the stock market. There’s a lot of evidence showing that missing just a handful of the best-performing days in a year can significantly erode your investment performance and hurt the compounding in your portfolio. So, sticking to your long-term plan is even more important during periods of high volatility because you might never be able to get the return back on the big performance days you missed.”

According to a Business Insider article, Fidelity Investments conducted a study to find out what their investors with the best investing results had in common. The result, according to BI, was that they were the ones who had forgotten they had a Fidelity account!

What does forgetting you have an account mean? It means you stop trading. This means that just holding for the long haul resulted in better outcomes than trying to optimize your results by timing the market.

Nathan Mueller, MBA, Financial Planner and Financial Coach at Blackbird Financial Planning says of people trying to time investments down to days or even hours, “Day trading can be fun. You can learn a lot, you can make money, and you can lose money. I often see millennials trying to day trade in the wrong type of account. The odds are usually stacked against them outperforming the market, and most of the time, they’d be better off sticking to a long-term strategy. The issue isn’t that they’re day trading but that they’re doing it in their retirement accounts. Sure, play around with extra cash in a non-retirement account. But messing up your retirement account could significantly affect your lifestyle later in life.”

Trying to Beat the Market

Many claim (with some basis, according to research) that beating the market over the long term is impossible. I disagree. In my opinion, backed with data from many of the funds I invest in, it’s not impossible, merely difficult.

Either way, what matters is how you invest to get the best long-term results. If you bet the farm on high-risk strategies, you may get very lucky and go from a few thousand dollars to a few million. However, doing that makes you a speculator (= gambler) rather than an investor, and you’re far more likely to lose it all.

Investing is about achieving your personal financial goals, not beating the market. Would you rather get great returns but fail to achieve your goals (e.g., because you invested too little, too late), or achieve your goals with mediocre returns (because you invested early, often, and consistently)?

In short, if you consistently follow a plausible system for picking good solid investments, you should do well over the long haul. If you keep taking high-risk bets in the hope of knocking it out of the park, you’re setting yourself up for big losses.

Trying to Beat the Pros

When I sold my first home and bought my next one, I ended up with a nice chunk of change beyond what I needed for the new purchase. I decided to split it between my 403(b) retirement plan and a taxable account with TD Ameritrade.

The money in the latter I split five ways between stocks I thought would do well. One of those was Bank of America, which at the time paid a very high dividend. For a while, the stock climbed slowly. Then, it started falling, and continued falling until it was worth pennies on the dollar.

My other picks did better, some doing quite well. But overall, the S&P 500 left me behind, as did my mutual fund investments.

The lesson I learned from that was that I don’t have the expertise and experience to beat the pros, nor the time to gain such expertise and experience, nor the analyst support they all enjoy. Do you?

Staying in an Investment Too Long, Trying to Break Even

Holding on to a losing investment until you break even can burn you badly. Some stocks never come back. Buy and hold can work out well for some stocks, but for others, you’re just throwing good money after bad.

Even companies that don’t go bust may take a very long time to recover their stock price (if they ever do). That’s why you should consider whether there are other investments that offer better prospects than the ones you’re holding that have dropped.

Of course, running for the exits after you lost a big chunk of your investment and buying a new market darling is a “great” way to sell low and buy high – not the optimal investing strategy. This is why you have to craft your investment system when you’re not stressed by losses, and then stick with it through the inevitable market gyrations.

Staying in an Investment Due to the Time and Effort You Put into Picking It

Doing due diligence when choosing investments is crucial. But there are no extra points for effort in investing. How hard you worked on your analysis matters far less than how good a job you did.

If you picked an investment due to fundamentals (or technical analysis), and market, industry, or specific investment conditions have changed, be ready to pivot and move your funds to what is now a better investment.

A great way of expressing it is that investing requires you to have strong opinions, weakly held. Strong enough to act on, but weakly enough held that you don’t hesitate to act appropriately on new information.

The Bottom Line

Personal finance, as I often point out, is exactly that – personal. What’s right for me could be completely wrong for you.

However, as the well-known quip goes, “The race isn’t always to the swift, nor the battle to the bold. But that’s the way to bet.”

You may choose to go against any or all of the above recommendations, and may even be better off for it. However, in my experience, the odds will be against you.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals.

Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Find a Financial Advisor

Do you have questions about your financial future? Find a financial advisor who can help you enjoy life with less money stress by visiting Wealthtender’s free advisor directory.

Whether you’re looking for a specialist advisor who can meet with you online, or you prefer to find a nearby financial planner, you deserve to work with a professional who understands your unique circumstances.

Have a question to ask a financial advisor? Submit your question and it may be answered by a Wealthtender community financial advisor in an upcoming article.

–

Do you already work with a financial advisor? You could earn a $50 Amazon Gift Card in less than 5 minutes. Learn more and view terms.

This article originally appeared on Wealthtender. To make Wealthtender free for our readers, we earn money from advertisers, including financial professionals and firms that pay to be featured. This creates a natural conflict of interest when we favor their promotion over others. Wealthtender is not a client of these financial services providers.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor