Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

I’ve been investing in (mostly stock) mutual funds since 1994.

As I wrote elsewhere, after a rocky start, I developed a method for picking mutual funds that’s worked pretty well for me.

2 Pieces of Accepted Investing Wisdom I Rarely Follow

There are two commonly accepted pieces of investing wisdom that I mostly reject.

First, Warren Buffet’s assertion that investing in low-cost index funds is the best way to invest. I’ve invested almost every dollar in actively managed funds, and my picks beat the S&P 500 (including dividends) by 1% per year.

Second, that using past results to pick investments is like “driving while looking in the rear-view mirror.”

Let’s look at that second assertion a bit more closely, and see if it’s really crazy, or actually smart (or as I prefer to say, crazy like a fox :)).

The Case Against Using Past Results to Pick Investments

A Yale study reported that a 1997 analysis by Mark M. Carhart, titled “On Persistence in Mutual Fund Performance,“ which concluded that a fund’s prior-year performance does help predict how well the fund will perform in the year ahead, was outdated.

This new study stated, “If anything, over the past two decades, you seem to do a little bit worse if you chase past returns on mutual funds… For the last 40 years, the Carhart persistence phenomenon hasn’t existed, but nobody had examined whether the Carhart findings are relevant for our investment choices today.”

The Case for Using Past Results to Pick Investments

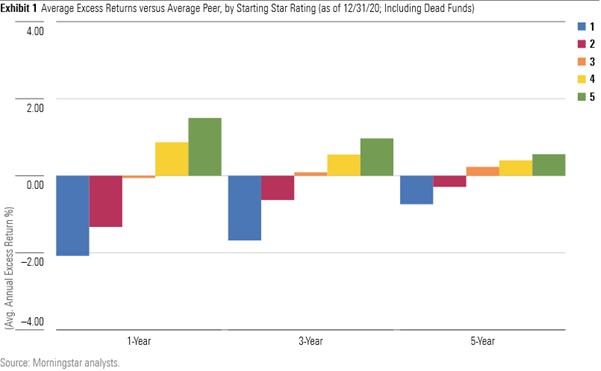

However, according to a study by Morningstar investment research and management company, “Which funds have tended to outperform in recent years? The past winners. And which have lagged? The past losers. You heard that right: Past performance has been predictive lately.”

Morningstar uses risk-adjusted performance to rate funds from 1 to 5 stars in their category. Here’s what their research shows, looking at funds’ average 1-year, 3-year, and 5-year excess returns vs. their average peer as a function of their star rating (including dead funds).

Clearly, the data show that the higher the star rating, the higher the fund’s average excess returns. Interestingly, the excess returns appear to diminish somewhat over time.

The author of this study considered that outperformance might be the result of a fund manager taking on too much risk, and getting lucky. Here’s what he reports about the results when he tested that hypothesis: “Past winners—that is, funds with 5-star ratings–earned a 4- or 5-star rating over the subsequent five-year period about five times more often than past losers–that is, funds with 1-star ratings. What’s more, past losers subsequently earned a 1- or 2-star rating, or died, about three times more often than 5-star funds. Thus, risk doesn’t seem to explain the performance pattern.”

My Personal Experience with Using Past Experience to Pick Winning Funds

After bad experience with one fund early on, having to do with poor governance, I decided to stick with T. Rowe Price funds, since I’ve found them to be extremely trustworthy. Importantly, this fund family offers dozens of no-load funds charging below-average management fees, many of which have a long track record of outperformance.

When picking funds, I look at their Morningstar star ratings, how long the management team has been in place, and how well they’ve performed compared to the indexes over the very long term. Using this method, I’ve outperformed the S&P 500 by 0.7%/year over 18 years in my personal portfolio, and 3.9%/year over 9 years in my 401(k).

Clearly, my anecdotal experience agrees with the Morningstar study results, and not with that of the Yale Study. It is possible that the Yale study looked at returns without adjusting for the risk fund managers took on to achieve those returns.

An Important Note on When I Use Past Performance to Trim My Holdings in a Fund

Having said all the above, when a fund massively outperforms in a specific year, I prefer to take some of those excess profits “off the table,” and move them to another fund that has a great track record.

This because extreme overperformance may be the result of the fund manager making a large bet on a trend s/he identified. In such situations, I’m not confident that the next (or same) concentrated bet will work out as well (or at all) the following year, so I don’t just stick with it.

3 cases in point are T. Rowe Price Global Technology Fund (PRGTX), Health Sciences Fund (PRHSX), and Communications & Tech Fund (PRMTX), as seen in the following table.

| Fund/Index | 2020 Performance | YTD Performance |

| S&P 500 | 18.2% | 17.0% |

| PRGTX | 75.6% | 14.0% |

| PRHSX | 30.1% | 9.8% |

| PRMTX | 53.7% | 12.1% |

These three funds outperformed the S&P 500 by anywhere from 2/3 to more than 4-fold (!) in 2020, but as of this writing are underperforming the index by anywhere from 1/5 to 2/5.

My Bottom Line

The above describes my anecdotal experience and compares it to competing studies. In short, I’ve found that if an active fund is managed well, charges low fees, and beats the index over the long haul, it’s a better investment than otherwise.

However, if any of my funds trounces the index in a particular year, I consider the downside risk as likely to be higher the following year than the upside. In this situation, I often trim my holdings in the extreme overperformers and reallocate those excess profits to other long-term winners that didn’t have an outlier of a year.

As an important disclaimer, none of the above should be viewed as investment advice, nor as an endorsement of any specific fund or fund family for anyone else to invest in. When choosing investments, do your own due diligence, or consult with a licensed investment advisor, preferably a fiduciary, who must put your interests above his or her own.

About the Author

Opher Ganel

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals.

Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor