What this article covers

Financial advisors weigh the real pros, cons, and emotional complexities of reverse mortgages — and offer a practical framework for deciding whether tapping home equity is the right move for your retirement.

It can be a financial lifeline for struggling retirees.

Or it can turn out to be an expensive trap.

“It” is the reverse mortgage, first issued more than six decades ago in a bid to help a Maine widow stay in her home, and subject to periodic tinkering by Congress ever since.

If you’re a near-retiree or in your early retirement years, you may be caught in an uncomfortable situation.

Key Takeaways

For Many Retirees, Home Equity Is Their Largest Untapped Financial Resource

When primary residence equity is excluded, the median net worth of Americans aged 65–69 drops from roughly $394,000 to just $132,000 — enough to generate only about $5,000 annually under the 4% rule. For retirees with a significant income gap but substantial home equity, a reverse mortgage can convert an illiquid asset into usable retirement income without requiring a monthly payment.

A Reverse Mortgage Works Best as a Strategic Tool, Not a Distress Solution

Advisors who support reverse mortgages emphasize using them proactively — to reduce portfolio withdrawals during market downturns, delay Social Security, or create a healthcare buffer — rather than grabbing them as a last resort under financial pressure. Reactive use, when options are already limited, typically produces worse outcomes and leaves less room to weigh the tradeoffs carefully.

High Fees, Maintenance Requirements, and Reduced Flexibility Are the Biggest Risks

Reverse mortgages carry origination fees, closing costs, mortgage insurance premiums, and higher interest rates than standard loans. You remain responsible for property taxes, insurance, and maintenance — and failure to keep up can trigger foreclosure. If you move sooner than planned, or life circumstances change, the income stream ends and the high upfront costs will have bought you little in return.

The Retirement Income Gap That Makes Home Equity So Attractive

Here’s an illustrative example for how retirement math can work.

The average combined Social Security retirement benefit for couples where both worked is $50k. That’s about 60% of the median US household income of $84k.

Using the common estimate that retirement income can be 20% lower than pre-retirement income, the median target retirement income should be around $67k, so if you get $50k from Social Security, you’re looking for another $17k annual income from your portfolio.

According to DQYDJ.com, the median American aged 65-69 has a net worth of $394k. Hypothetically, the 4% rule says this should translate into a $16k annual portfolio income.

Great, right? That puts you at $66k, within touching distance of the $67k “target.”

However, when you exclude primary residence equity, the median net worth drops to just $132k, dropping the estimated portfolio income to just $5k, which with the average Social Security check is still nearly 20% short of the target.

Your home may be worth far more than it was a decade ago, but that growth is trapped in your home equity, an illiquid asset that doesn’t typically provide any income.

Worse, with the increase in home values, property taxes have also risen. According to the St. Louis Fed, property taxes have nearly tripled since 2000, of which 31% was in the last five years. Homeowner insurance has also gone up significantly, 2.6× since 2000, and nearly 30% in the last five years.

Along with these housing-related costs, inflation has pushed up the cost of food, healthcare, energy, and much more. The Consumer Price Index for all Urban consumers (CPI-U) has nearly doubled since 2000 and gone up 25% in the past five years alone.

Combine all these with ever-longer retirements, and it’s clear that coming up with sufficient retirement income is a major concern for many American seniors.

A big enough concern to make tapping home equity an attractive option, since, for some retirees, home equity may represent their largest remaining source of financial flexibility.

Why Tapping Home Equity Feels Different from Spending Other Assets

You may technically have a healthy net worth while still struggling with monthly cash flow. You may feel reluctant to withdraw heavily from investment accounts during market downturns. You may want to stay in your home for emotional and practical reasons. Yet much of your financial flexibility may be trapped in an illiquid asset.

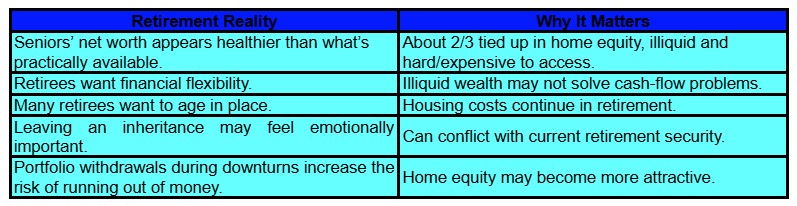

Table 1 summarizes some of the important realities of Americans’ retirement considerations.

With home equity comprising two thirds of the median near- and early-retiree net worth, tapping that most significant resource for retirement income can seem like a lifeline tossed to a drowning man.

This, and increased guardrails put in place by Congress, is why reverse mortgages are receiving renewed attention.

But… if one of your financial goals is to leave a legacy for your kids, tapping home equity can be emotionally difficult.

After my father passed away, I helped my mother manage her finances because Dad had always handled them. Her biggest fear wasn’t stock market volatility or inflation. It was “spending the inheritance” she hoped to leave to my sisters and me.

This, to the point that she hesitated to buy new panties until I reassured her that the money was hers, and was there for her to use.

That emotional conflict may help explain why reverse mortgages are so controversial. It isn’t just a numerical financial decision.

It’s a deeply emotional one.

So, “Is a reverse mortgage good or bad?” isn’t the right question to ask. The better question is, “Is a reverse mortgage right for me, given my individual situation, priorities, and goals?”

What Is a Reverse Mortgage and What Does It Do?

A reverse mortgage lets senior homeowners borrow against their home equity without making monthly mortgage payments.

The most common reverse mortgage is the federally insured Home Equity Conversion Mortgage (HECM), which is regulated by the U.S. Department of Housing and Urban Development (HUD), and available only through lenders approved by the Federal Housing Administration (FHA).

FHA-insured HECMs are subject to annual lending limits. For 2026, the national lending limit is $1,249,125, while some proprietary “jumbo” reverse mortgages, not insured by the federal government, may allow borrowers to access more equity, particularly in expensive housing markets, up to several million dollars for high-value homes.

How much equity you can access through a reverse mortgage depends on several factors, including your home’s value, interest rates, available equity, and the age of the youngest borrower. In general, if both you and your spouse are older, you’ll likely qualify for larger amounts.

With regular mortgages, you make monthly payments, where each payment covers the interest that accrued since the previous payment, plus some of the loan principal, which reduces your owed balance.

Reverse mortgages, no pun intended, are (mostly) the reverse.

You make no monthly mortgage payments, so the interest keeps accruing, gradually increasing the balance of the loan. The loan gets paid off when:

- You sell the home.

- You move out permanently.

- Or all borrowers pass away.

However, just as with a regular mortgage, you still own your home, and can, e.g., make any changes to it that you want, without needing lender approval.

As alluded to above, there are age and other requirements for taking out a reverse mortgage. Specifically:

- All borrowers must be at least 62 years old.

- The property must be your primary residence, i.e., where you live most of the year.

- If you have any outstanding balance secured by your home, including a mortgage, a Home Equity Line of Credit (HELOC), or a home equity loan, these must be paid off no later than when you close the reverse mortgage, and the amount you can take from the reverse mortgage will be reduced by the payoff balance of these previous debts.

- If you have any federal debt, e.g., federal income taxes owed and/or federal student loan debt, those must be paid off similar to your previous mortgage. Again, you can use part of the reverse mortgage money to pay off these federal debts.

- If your home isn’t in acceptable shape, the lender will tell you what repairs you must make before you can get the reverse mortgage.

- You need to have enough money, possibly using part of the reverse mortgage, to pay for property taxes, homeowner insurance, and ongoing maintenance and repair costs.

- You must take mandatory counseling from a HUD-approved reverse mortgage counseling agency. This counseling covers your eligibility, the financial implications of the reverse mortgage, and other alternatives you may prefer.

Modern HECMs include safeguards beyond the mandatory counseling. Specifically, they’re federally insured, and there are “non-recourse protections” that generally protect you and your heirs from owing more than the home’s value when the reverse mortgage is paid off.

Reverse mortgages offer much more flexibility than a standard mortgage. You can structure them to receive:

- A lump sum.

- A monthly payment.

- A line of credit.

- A combination of the above.

Beyond not having to make a monthly mortgage payment, there’s another crucial benefit. Because the money you receive is borrowed, rather than income, it isn’t taxable.

What Costs You Still Owe with a Reverse Mortgage

Also as with a regular mortgage, you must still keep paying:

- Your property taxes.

- Homeowners insurance.

- Maintenance and repairs.

- Homeowner Association (HOA) fees, if any.

- Any other housing-related expenses, such as utilities.

Thus, although you have no mortgage payment, you may still have significant housing costs.

Why Reverse Mortgages Have a Bad Rep

With all their benefits, reverse mortgages are best viewed with caution. Some of the bad reputation may be outdated, given newer protections, but it still pays to be cautious.

As Mike Hunsberger, ChFC®, CFP®, CCFC, Owner, Next Mission Financial Planning, says, “I find that many people still have negative views of reverse mortgage even though the industry has changed significantly. The reverse mortgage industry is fully regulated now by the Department of Housing and Urban Development. I find that most people don’t know enough about the changes and protections that are in place. While reverse mortgages aren’t right for everyone, they can be a useful tool in the right situation.”

Reverse mortgages have much higher fees than standard mortgage loans. Partially due to these higher fees, they’ve historically been marketed aggressively, even for borrowers for whom they weren’t a good fit. Also, the terms can be confusing, resulting in many borrowers not fully understanding all the implications.

This is where the mandatory counseling comes in.

If the counseling boils down to this being a good fit, and especially if your financial advisor says it’s a useful part of your overall financial plan, you can set aside the bad rep. However, you still need to consider how well the reverse mortgage, with its high cost and complexity, works in your particular situation.

The Emotional Conflict Involved in the Reverse Mortgage Decision

If you think of reverse mortgages in purely mathematical terms, you’re missing a major factor.

The deep emotional impact.

Especially for older homeowners, who may have lived in their home for decades, the home represents far more than simply a roof over their head. It may also represent:

- Security.

- Independence.

- Stability.

- Family history and memories.

- And perhaps more importantly than many financial discussions acknowledge, a way to leave behind something meaningful to their kids.

If leaving a legacy to your kids is important to you, spending down your home equity can feel very different from spending investment returns. It can feel like you’re dismantling part of the legacy you hoped to leave your kids, which can cause major emotional distress and resistance.

From the kids’ perspective, many want their aging parents to have a comfortable retirement, even if it means less will be left behind for them once their parents pass away. However, especially for kids who struggle financially, seeing their parents “spend their inheritance” brings up negative emotions like fear and resentment.

This can shape family dynamics, even if nobody discusses it out loud.

As a result, many seniors end up reluctant to spend their own money, especially the equity in their homes, even to cover very legitimate needs, let alone to enjoy their late years. They may delay needed home repairs, avoid travel, and in general live with financial anxiety that’s beyond what their true situation warrants.

This doesn’t mean that a reverse mortgage is necessarily the right answer in all cases. However, retirees who struggle with cash flow problems should ask themselves, and their financial advisors, if protecting their home equity for their eventual heirs aligns with how they want to live in their retirement.

Where Financial Advisors See Strategic Value for Some Retirees

Even financial advisors who support reverse mortgages don’t generally see them as universally valid solutions.

Instead, they may frame them as one of many retirement income tools. And, as with all tools, they fit certain situations better than others. Ideally, they should be used strategically, as part of an overall plan, and only when they’re a good fit to the specific individual’s needs.

And preferably not reactively, when they have to be grabbed like that “lifeline” to avoid sinking.

Ben Simerly, CFP®, Founder and Financial Advisor at Lakehouse Family Wealth, cautions, “While reverse mortgages can be a Godsend for some retirees, they come with a significant set of drawbacks. Clients often get in touch with advisors to see if they are the ‘magic wand’ described by so many mortgage brokers. In reality, we only use reverse mortgages as a last-ditch resort.”

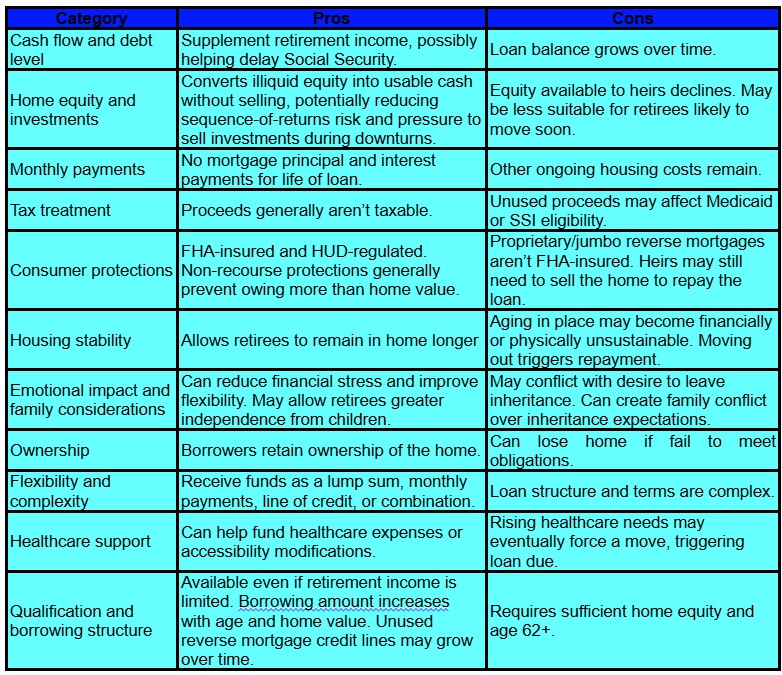

Table 2 contrasts strategic vs. distress-driven uses for reverse mortgages.

A reverse mortgage tends to work better when you still have other options, but there are valid reasons to prefer the reverse mortgage.

You may tap your home equity strategically to, e.g.:

- Reduce withdrawals from your investment portfolio during market downturns.

- Improve your retirement cash flow.

- Delay claiming Social Security benefits, allowing them to grow 8% a year up to age 70.

- Create a financial buffer for your healthcare expenses.

- Allow you to remain in your home without mortgage payments, if you plan to stay there for the long term.

For near- and early retirees, sequence-of-returns risk means that a market crash in the early years of your retirement may force you to sell depressed assets, which makes it hard or even impossible for your portfolio to recover.

Having a non-portfolio source of retirement income can ease the pressure on your portfolio, significantly reducing this risk and improving your portfolio’s longevity.

If you take a portion or all of the reverse mortgage in the form of a line of credit, you have far greater flexibility, and unused portions of the credit lines can continue growing over time, potentially increasing flexibility later in retirement.

As stated before, none of this makes a reverse mortgage intrinsically “good” in all cases. It’s just that in the right circumstances, treating it as a smart part of an overall financial plan is better than treating your home equity as “untouchable.”

When Reverse Mortgages Can Become Risky

Having said all that, taking out a reverse mortgage in the wrong circumstances can be a costly mistake.

As mentioned above, even though you won’t have any mortgage payments, you’re still on the hook for property taxes, homeowners’ insurance, maintenance and repair costs, utilities, HOA dues if any, etc.

And if you can’t afford to pay these expenses, your lender can foreclose on your home.

Since reverse mortgage fees are high, ideally you want to be sure to get the benefit of the loan for as many years as possible. If you end up moving out of the house early, you’ll have paid high fees for little return.

Simerly emphasizes how changing life circumstances can create problems for retirees who expected to remain in their homes long term. “Retirement is about choice,” he noted. “When retirement gets unfriendly, it’s typically because people are out of choices. Narrowing your plan with a reverse mortgage removes choice. If you move, or life changes, or maintenance is neglected due to illness, the income stream ends, and you have little if any recourse.

“Seniors often have a difficult time completing maintenance on homes, especially older homes. Strict maintenance requirements mean that missed maintenance can end the income stream, and you may be forced into a months-long or even years-long process of fighting the reverse mortgage company for resolution.”

The high fees involved in a reverse mortgage include high origination fees and closing costs, as well as mortgage insurance premiums and servicing fees. In addition, reverse mortgage interest rates tend to be higher than those of regular mortgages, something that affects your payoff costs.

Some reasons for moving early are harder to anticipate.

For example, health changes, mobility limitations, or changes in family circumstances (e.g., grandchildren being born a few states away).

Other reasons are more likely to be known ahead of time.

These include downsizing plans, or feeling like your home is becoming too big for you to manage.

Because the loan balance of a reverse mortgage grows instead of shrinking, over time, what’s left for your heirs will decline. Especially if you stay in your home for decades of retirement, there may be nothing left of the home’s value for your heirs after the loan is paid off.

Reverse mortgages may also affect eligibility for certain government programs, e.g., Medicaid or Supplemental Security Income (SSI) if unused funds push assets above eligibility thresholds.

Table 3 summarizes the pros and cons of reverse mortgages.

As you can see in the table, there are many pros, but just as many cons.

The thing to be most careful of is waiting until financial stress pushes you to make a hurried decision, without having the time and emotional bandwidth to fully understand these pros and cons and how they play out in your specific situation.

Alternatives to a Reverse Mortgage Worth Comparing First

If you need to tap your home equity, there are other ways than a reverse mortgage, and any of these may be more appropriate for your personal situation.

These alternatives include:

- Downsizing, which may be emotionally difficult and stressful.

- Opening a HELOC or taking out a home equity loan, however, both require monthly payments.

- Doing a cash-out refinance, which may require income qualification, and could increase your monthly costs, especially when rates are high.

- Taking early Social Security benefits (at the cost of permanently reducing the benefits).

- Reducing discretionary spending.

- Taking on part-time work.

- Investing your portfolio somewhat more aggressively, which increases the risk of loss.

As is the case with most such decisions, each option comes with its own set of pros and cons, and these play out differently for different people. That’s why financial advisors work with each client to compare multiple scenarios to find the one that best fits the needs and desires of the specific client.

Simerly doesn’t see reverse mortgages as the appropriate solution in the overwhelming majority of cases. He says, “The number one goal in retirement planning, from a broad perspective, is to build flexibility into the plan. A reverse mortgage removes much of your flexibility. When plans change, the reverse mortgage often cannot.

“So, what to do instead? Moving, if it’s possible, can be the biggest win. One of the common themes we hear is that retirees do not want to move. Unfortunately, that’s often plan A. The reality is that when a home doesn’t fit the family, it ends retirement.

“Even if a reverse mortgage feels like it’s the last possible option, selling the home to pay the down payment on a Medicaid-friendly retirement community often ends up being the better option.

“For a retirement to be a retirement, the key pieces must fit. That means functional housing for both lifestyle and budget, a healthy community around you, being close to family, functional transportation, access to helpers nearby, etc. And the home is at the heart of this.

“So, we always advise clients to focus on retirement life, over retirement belongings. Community is more important than the state or town you’re in. And lifestyle is more important than the physical house. Going into retirement with a lifestyle-focused mindset is one of the most important things a retiree can do, and reverse mortgages tend to result in the opposite.”

Questions to Ask If You’re Considering a Reverse Mortgage

There are multiple questions you should ask if you’re considering taking out a reverse mortgage. For example:

- What problem is this trying to solve, and is there no better solution?

- Do I plan to remain in this home long term?

- How important is preserving home equity for heirs?

- Would greater cash-flow flexibility improve my retirement enough to make this desirable?

- Can I comfortably keep paying taxes, insurance, utilities, upkeep, etc.?

Your answers to these questions are far more important than any general statement about whether reverse mortgages are good or bad. Working with a fiduciary financial advisor may help improve clarity around these and other important considerations.

The Bottom Line: A Reverse Mortgage Is a Tool, Not a Trap or a Magic Wand

Reverse mortgages are neither universally good solutions nor universally costly traps.

For some retirees, they may create flexibility, reduce financial stress, and support aging in place. For others, they may be a needlessly expensive and complex solution for a problem that’s better solved in a different way.

The main point is how you think about your home equity.

Many people spend decades building equity in their homes, then struggle emotionally with the idea of ever using it. For some, preserving that equity may align perfectly with their goals and financial situation. For others, protecting inheritance at all costs can come at the expense of retirement security and peace of mind.

Sometimes the hardest retirement decisions aren’t just about money. They’re about what that money represents.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher