Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

When people think of financial professionals, a local financial advisor most often comes to mind. And with approximately 300,000 financial advisors in the U.S., the role they play helping millions of Americans invest and improve their financial health is considerable.

Beyond financial advisors, there are other types of financial professionals to consider as well, including financial coaches, counselors and therapists. And today, many personal finance blogs, podcasts, video channels and online courses created by a growing community of personal finance enthusiasts have become integral sources of education and advice, primarily built upon the life experience of their owners.

What has also changed is the way people work with financial professionals. If you’re ordering a pizza, it’s important to choose a place that’s close to home. But when it comes to working with a financial professional, it’s more important to choose someone who can offer personalized insights and service based on your unique needs than to hire someone near your where you live. Many financial professionals offer virtual services to people across the country while maintaining the very important human and personal touch through video calls, live chats and help on demand.

Then there’s the question of cost and timing. Can I afford to hire a financial professional? When should I hire a professional? Fortunately, there are more pricing options today than ever before with a range of costs for every budget, including free help available for the people who need it.

We prepared this guide to help you learn more about your options for choosing a financial professional, including the services they provide, when you might need one, how much they cost and how to find the right financial professionals for your individual needs.

Understanding the Types of Financial Professionals

It can be confusing and overwhelming for most people (including those in the finance industry!) to keep track of countless titles and financial certifications held by financial professionals. Many financial professionals offer similar services, though their areas of specialization can differ significantly. And some charge upfront for their services or by the hour, while others work on commission or take a percentage fee, and others offer their services with no cost for people who can’t afford to pay.

To simplify things, we’ve organized this guide into five broad categories of financial professionals that each offers a more in-depth discussion of the different titles and designations often associated with the category. (It should be noted that this guide is not exhaustive as we don’t discuss accountants, insurance agents, lawyers, and other professionals who may offer financial services.)

Read on to learn more about these different types of financial professionals you might need to consult, titles they may use, what they do, and exactly when you should consider hiring them.

Financial Advisors (including Financial Planners)

Titles and Regulations

Financial advisors are also commonly known as financial planners, investment advisors, financial consultants, or investment consultants. Common professional designations include Certified Financial Planner (CFP) and Chartered Financial Analyst (CFA).

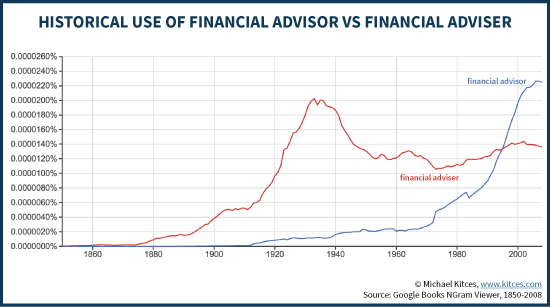

You may also see these professionals referred to as either financial advisors or advisers. This is not a spelling error. It’s due to the fact that some professionals still use the original old English spelling used in the Investment Advisers Act of 1940, as shown in the chart below and explained further in this article written by industry expert Michael Kitces on his blog, Nerd’s Eye View.

There is often crossover in the services offered by financial advisors and financial planners (as we explain further below) making it hard to ascertain exactly how many there are in the US. But according to Kitces.com citing research from Cerulli Associates, the number has been estimated at a little over 300,000 (though as Kitces suggests in his article, this number may be overstated).

Financial advisors in the US are commonly regulated by the US Financial Industry Regulatory Authority (FINRA) and those with more than $100 million in regulatory assets under management must also be registered with the US Securities and Exchange Commission (SEC), as a Registered Investment Adviser (RIA).

A financial planner is often known as a Certified Financial Planner (CFP) if they have earned this financial certification common among financial professionals. CFP.net claims there are now more than 80,000 Certified Financial Planners in the United States.

You will find there is a lot of crossover between financial advisors and financial planners, with some professionals offering both types of assistance. Financial planners may be registered with the National Association of Personal Finance Advisors (NAPFA) and/or the Financial Industry Regulatory Authority (FINRA). Financial planners must also be registered with the US Securities and Exchange Commission (SEC) or the appropriate state securities regulator.

It is also important to note that the Securities and Exchange Commission (SEC) established a new regulation known as Regulation Best Interest (Reg BI) effective June 30, 2020. This rule establishes a standard of conduct for financial advisors affiliated with broker-dealers to act in the best interest of their clients. While it may sound odd that this hasn’t always been the case, the previous suitability standard only required that a product recommendation be suitable based on a client’s personal situation, not necessarily determined by the financial advisor to be the best option for a client.

What Do Financial Advisors and Financial Planners Do?

The services offered today by most financial advisors have evolved from acting as a broker selling financial products and services for a commission, to receiving a percentage fee on the assets they manage for clients. While financial advisors continue to spend significant time helping clients select and understand investment products like mutual funds and exchange-traded funds (ETFs), their role increasingly focuses on understanding their clients’ complete financial picture.

Good financial advisors listen to learn your investment goals, how comfortable you are with risk and take your personal circumstances into account to then advise you on the best investment options, products, and services offered by their firm based on your financial resources, needs, and requirements.

Much like a financial advisor, a financial planner will help you make investment decisions, but, as the name implies, your financial planner will generally help you take a longer-term view of finances and look at the bigger picture. They will help you plan your entire life, from a financial perspective, advising you on things such as investing your wealth, minimizing tax liability, estate planning, insurance, and planning for long-term goals such as saving for your kids’ college education or planning for retirement.

When Do You Need a Financial Advisor or Financial Planner?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer, or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

How Much Does a Financial Advisor or Financial Planner Cost?

Some financial advisors charge a fee, which means you pay them directly, either an hourly fee or, more commonly, a small percentage of the value of the assets they are managing for you known as an advisory fee that is deducted from your account. Generally speaking, you can expect to pay an advisory fee ranging from around 1% to 1.5% of the value of your assets under management each year. It is worth noting that this fee does not include the cost of investment products like mutual funds or ETFs that may be held in your account.

Other financial advisors are compensated by the companies whose products they sell, based on the sales they make, and some use a mixed model, charging lower fees, but also taking a commission on sales made.

Before you hire an advisor, you should be sure you understand how they are paid and they should be comfortable telling you when you ask the question.

Before you hire an advisor, you should be sure you understand how they are paid and they should be comfortable telling you when you ask the question.

Financial planners are often paid by the hour, although some work for a monthly retainer. Depending on your circumstances, you may also pay a one-off fee for a consultation on a specific issue, or to have a comprehensive financial plan put together for you. This may be necessary, for example, if you’ve just sold a business for a large sum and want your future finances planned out in detail.

You can expect to pay hourly fees in the region of $150 to $400, and around $1,000 to $3,000 for the creation of a financial plan. For ongoing financial planning, you will generally be charged an annual retainer of $2,000 to $7,500 (or $167 to $625 per month), depending on your needs and your financial situation. Financial planning is a complex process with a complex fee structure, so make sure you know exactly what fees you will be charged and when.

How Do You Find a Financial Advisor or Financial Planner?

You’ll find a growing number of financial advisors and financial planners in the Wealthtender Financial Advisor Directory. You can search based on the financial certifications they hold and the services they offer to find those who may be a good fit for you.

Another useful resource is the National Association of Personal Finance Advisors (NAPFA.) website Financial advisors and financial planners registered with NAPFA are legally bound to act as fiduciaries, and must always put their clients’ interests first. This means you will always be advised based on which is the best product for you, and not based on which provides the highest commission for the advisor.

There are also a few networks that list financial advisors and planners, including Garrett Planning Network and the XY Planning Network. Financial Advisors who are part of the XY Planning Network have no minimum asset requirements and all offer their services online so you’re not limited by location.

You should always check the credentials and registration of any financial advisor or planner you’re planning to work with, and you can use free tools from FINRA and the SEC to do so. BrokerCheck is a free tool offered by FINRA to research the background and experience of financial advisors associated with securities firms. For a more comprehensive search, you can use the SEC’s Investment Adviser Public Disclosure database that includes results from BrokerCheck as well.

Since there is a lot of crossover in what a financial advisor and a financial planner will do, make sure any professional you engage knows exactly what you are looking for before entering a long-term arrangement.

Financial Coaches (and Financial Counselors)

Titles and Regulations

A financial coach may also go by the title money coach, personal finance coach, financial life coach among other names. A financial counselor is another common title among financial professionals who offer coaching and counseling services.

Unlike financial advisors and planners, financial coaches and counselors are not generally registered or regulated by an outside authority, as this area is not as tightly controlled as most financial services. This means it is impossible to say how many money coaches there are in the US, but it has been estimated that there are around 17,500 personal coaches across the US, specializing in different areas.

Common certifications held by financial coaches and counselors include the Accredited Financial Counselor (AFC), Certified Personal Finance Consultant (CPFC), and Certified Financial Planner (CFP) designations.

What Do Financial Coaches Do?

As you would expect, financial coaches and counselors offer coaching and counseling to help you manage your own personal finances better. This includes things like setting financial goals, improving spending and saving habits, developing a budget, making a plan to get out of debt, improving your mindset around money, and making sound financial decisions. They may also refer you to other financial professionals or recommend digital apps and other online tools to help you with your finances.

Financial coaches and counselors do not sell you financial products or give specific investment advice.

When Do You Need a Financial Coach?

You may want to hire a financial coach or counselor if you feel you need to get your finances in order and learn to manage your money better. You’re not looking for specific investment advice, but rather to develop a skill set that will let you excel in the area of personal finance and money management. You may also feel you need the accountability that comes with hiring a financial coach or counselor, or that you need to change your mindset when it comes to money and wealth.

How Much Does a Financial Coach Cost?

Financial coaches and counselors usually charge by the hour, or sometimes put together a package, such as six one-hour coaching calls in six months, with email support in between, or offer a membership arrangement, like the Financial Gym., or offer a membership arrangement, like the Financial Gym.. The Financial Educators Council states that hourly rates for financial coaches tend to vary between $75 and $600, with an average of $257 per hour. When it comes to annual coaching programs, you may pay anything from a few hundred dollars to almost $6,000.

Most financial coaches and counselors will offer you a free initial consultation or ‘discovery call’ to see if you are a good fit for each other.

How Do You Find a Financial Coach?

You’ll find a diverse group of financial coaches and counselors featured in the Wealthtender Financial Coach Directory. You can search based on the financial certifications they hold and the money topics most important to you.

The directory includes financial coaches with a broad range of education, experience, and specializations who are ready to help you enjoy life more with less money stress.

Financial Therapists

Titles and Regulations

Financial therapists represent a fairly new, but rapidly growing niche in the financial services industry. The Financial Therapy Association (FTA) offers training and certification, leading to the designation Certified Financial Therapist-I (CFT-I). This is a professional certification offered by the FTA, covering financial and mental health professionals. In order to hold this designation, financial therapists must also adhere to the FTA Standards of Practice and Code of Ethics.

What Do Financial Therapists Do?

Financial therapists aim to help people improve their finances by changing the way they think and feel about money. This can then impact their behaviors when it comes to earning, saving, spending, and managing money.

It has long been acknowledged that the way people manage money is strongly associated with emotions and attitudes, rather than just financial knowledge, and financial therapy uses evidence-based practices and interventions to improve both financial and emotional well-being.

Good financial therapists help clients develop healthy attitudes and boundaries around money, which can in turn help with issues such as overspending, financial enabling, and financial dependence. While financial therapists may sometimes offer insights on specific strategies or investments, they are primarily focused on mindset and developing a sense of control and well-being around personal finances.

When Do You Need a Financial Therapist?

You may need a financial therapist if your attitude towards money is causing you stress and impacting your well-being. It is often hard to distinguish between situations where it’s your attitude that is the problem, or your finances themselves.

As examples, financial therapists can help you if money is causing major issues between you and a partner or family member, if you have limiting beliefs around money that prevent you from becoming financially stable, or if you have an attitude towards money that results in inappropriate spending patterns (whether that’s overspending or extreme frugality).

How Much Does a Financial Therapist Cost?

Financial therapists tend to charge by the hour, as other types of therapists do. Unsurprisingly, they also charge roughly the same hourly rates as any other therapist, which can vary greatly, but is never cheap. According to Good Therapy, most therapists in the USA charge anywhere from $65 to $250 an hour. Prices will usually depend on various factors, such as the therapist’s training, reputation, and location.

As financial therapy falls under the broad concept of mental health, you may find your health insurance at least partially covers it, which certainly won’t be the case with other financial services. For example, New York-based therapists TriBeCa Therapy, who offer financial therapy among their services, claim that many patients receive at least partial reimbursement from their health insurance providers if they have out-of-network coverage.

However, there may be several hoops to jump through, including things like getting a mental health diagnosis or a referral for treatment from another professional.

How Do You Find a Financial Therapist?

The FTA maintains a list of financial therapists across the USA, with details of their qualifications, number of years in practice, fee structure, and practice approach. They also specify whether they offer therapy at a distance (usually through Skype, Zoom, or similar).

You’ll also find a growing list of financial therapists on Wealthtender, along with members of the Financial Therapy Association interested in financial therapy, but who may not yet hold the CFT-I certification offered by FTA.

Remember that many traditional therapists may include money matters among the things they are willing and able to help you with. This is especially true of couples therapists, given how commonly money becomes an issue of conflict between partners. However not all therapists have a financial background or a thorough understanding of the emotional aspect of dealing with finances, so choosing to hire a financial therapist can be worth it if money matters are a major issue for you.

Credit Counselors (and Debt Counselors)

Titles and Regulations

Credit counselors go by a few other titles including, perhaps confusingly, debt counselors (as they help you reduce your debt and improve your credit). You may also hear a credit counselor referred to as a Certified Consumer Debt Specialist (CCDS). This is a professional certification held by some financial counselors, awarded by the Center for Financial Certifications (Fincert).

Credit counselors generally work within agencies that may be accredited by the National Foundation for Credit Counselling (NFCC) or the Financial Counseling Association of America (FCAA). The NFCC has approved 57 non-profit agencies across the US, but with so many organizations offering both non-profit services and for-profit counseling, it’s hard to estimate how many credit counselors there are working across the US, in various capacities.

What Do Credit Counselors Do?

As in other areas of life, a counselor tends to help you with something you are struggling with. You might hire a financial coach to help improve your finances (even if there’s nothing drastically wrong with them), but you will usually hire a credit counselor to help you put right something that has gone wrong.

Credit counselors typically help people get debt under control and improve their credit score. They will help you put together a plan to pay off your debt, which might include better budgeting, refinancing, or debt consolidation strategies. Some credit counselors will help you set up a debt management plan, and act as an intermediary between you and your creditors.

When Do You Need a Credit Counselor?

It’s worth considering a credit counselor if you have financial problems that you can’t solve yourself, such as out of control debt or a very poor credit score. Even then, you only need counseling if you don’t know how to get back on track yourself.

People generally seek credit counseling when something goes wrong that will seriously impact their finances, such as unemployment, divorce or a serious health issue. They may also seek help if credit card and other consumer debt has grown to a level they can no longer manage.

How Much Does a Credit Counselor Cost?

Understandably, you won’t want to spend a lot of money on credit counseling if you’re in debt, but you may not have to. Various non-profits, credit unions, and religious organizations provide credit counseling for free to people in need, so tell the agency if you’re in a position where you need help but simply can’t afford to pay for it, which will usually be the case if you’re seeking credit counseling.

If you don’t qualify for free counseling, you will find that many non-profit agencies are very affordable. At the very least, you may find you can get a free initial consultation.

You will, however, have to pay a fee for setting up a debt management plan, though this can be very reasonable. Credit agency, Green Path, for example, currently charges $50 to set up a debt management plan, and $36 a month for ongoing management of it.

Depending on how much debt you have, you may find you save a lot more than that each month by the time the agency has negotiated your repayments and helped you consolidate your debts. Fees for credit counseling can vary greatly, so shop around and ask your potential credit counselor to let you know in advance exactly how much you’ll be charged.

How Do You Find a Credit Counselor?

It’s always a good idea to start with a non-profit credit counseling agency and see if you can get help without paying a fee. Look for an agency that is accredited by the National Foundation for Credit Counselling (NFCC)or the Financial Counseling Association of America (FCAA). You may prefer a local agency where you can talk to someone face-to-face, but many agencies offer phone counseling, which can be just as effective, and very convenient.

You’ll also find a growing list of organizations and financial professionals in the Wealthtender Directory of Free and Low-Cost Services.

Personal Finance Blogs, Podcasts and Online Courses

Titles and Regulations

A growing area of importance for people seeking help with personal finances comes from blogs, podcasts, online courses, and other resources (e.g. YouTube video channels) offered by financial professionals and personal finance enthusiasts. These individuals are often collectively referred to as the personal finance community.

While many people in this area may have a background or qualification in finance or a related field, there is no requirement regarding this, and many people in the personal finance community simply write from their own experience.

What Does the Personal Finance Community Do?

Members of the personal finance community offer education, insights, and guidance regarding common money matters, such as overcoming financial challenges, paying off debt, managing money effectively, saving for retirement, or building wealth. Often they write, speak or teach based on their own personal experience, backed up with evidence from other sources and opinions they have formed throughout their lives and careers.

There are many blogs, podcasts, and courses that focus on a particular topic like getting out of debt or investing, while others are oriented to a demographic niche (e.g. recent graduates, real estate investors, women, or retirees). While many blogs prominently feature the writing of their owner, podcasts usually include interviews with a diverse range of people offering varied perspectives.

When Do You Need a Blog, Podcast or Online Course?

Most of us can benefit from learning more about personal finance. It isn’t often taught in school, therefore many of us will find it helpful to read, listen and tune in to what members of the personal finance community have to say to better educate ourselves in the principles of good money management.

You should be aware, however, that the personal finance community is generally writing or speaking to a broad audience. While some may connect with their audience individually in forums, you should usually consult a financial professional like a financial advisor or coach for personalized advice.

With this said, an increasing number of financial advisors, planners, coaches, and other professionals also have blogs, podcasts, and courses, so make sure you do your homework on who’s behind your favorite blog, podcast, or course as they may be able to offer individualized services.

How Much Do Blogs, Podcasts and Online Courses Cost?

The good news is that you can access most personal finance blogs and podcasts for free. Online courses may offer a free preview, but usually charge users for completing the course with costs that range from a few to several hundred dollars.

Be aware that owners of personal finance blogs and podcasts primarily make money from advertising or recommending specific services and tools to their readers. A good personal finance website will clearly disclose how they make money and if they are compensated for recommending financial products and services.

How Do You Find Personal Finance Blogs, Podcasts and Online Courses?

You’ll find hundreds of personal finance blogs, podcasts, and online courses on Wealthtender. You can easily search based on the money topics most important to you in each of these directories:

- Wealthtender Personal Finance Blog Directory

- Wealthtender Financial Podcasts Directory

- Wealthtender Online Courses Directory

Once you have found a few you like, it’s worth subscribing so you don’t miss future articles or episodes on the topics that are of interest to you.

Final Thoughts

Money is a complex and emotional topic, and you don’t have to always face difficult decisions about your finances on your own. You may not need to consult all of the above professionals, even over the course of a lifetime, and certainly not all at the same time. However, you may find that knowing what type of help is out there and how to find the help you need can increase your confidence and give you peace of mind about your personal finances.

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

About Wealthtender

At Wealthtender, we believe personal finance is an emotional and human subject. We enjoy using online tools and apps that help automate and simplify our finances, but when it comes to financial education, guidance, and advice, we believe there’s no substitute for human wisdom and life experience.

We coined the term wealthtender to describe a person who is a resource you can trust for help with money matters. This includes a broad range of financial professionals and semi-professionals who offer their insights and services in person and online.

Our mission at Wealthtender is to help people discover the most trusted and authentic financial professionals no matter their income or stage of life. We believe everyone deserves a wealthtender and we want to help you find yours.

About the Author

Brian Thorp

Brian is CEO and founder of Wealthtender. He and his wife live in Texas, enjoying the diversity of Houston and the vibrancy of Austin.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor