Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Ask ten financial advisors whether you should pay off your mortgage before retiring, and you’re likely to get ten different answers — and all of them might be right, depending on your situation. The conventional wisdom that responsible retirees enter retirement debt-free has real merit for some people, but for others it’s a rule that delays retirement unnecessarily, drains liquidity at the worst possible time, and trades a manageable fixed payment for a portfolio too small to weather a market downturn. The real question isn’t whether carrying a mortgage into retirement is good or bad. It’s whether you’re evaluating the right factors — interest rate, tax consequences, guaranteed income, liquidity, and emotional tolerance — to make the decision that’s actually right for you.

Until last year, my wife and I were paying three mortgages. One on our old house, which we kept as a residential rental. Another for an office suite we both use and partially lease to others. The third for our current home.

When we’d had enough of being residential landlords, we sold the rental property, leaving us with two active mortgages. Then I reached a personal and professional decision point: should I mostly retire, or keep running my consulting business full-time?

I chose retirement.

If you were advising me then, you might have asked, “But what about the mortgages? Are you planning to pay them off?” That would have been a fair question. For many people, being debt-free feels like a requirement for retiring responsibly.

In our case, the math didn’t force the issue. We could pay off the mortgage without draining our savings, but both loans carry low fixed rates, so the payments are manageable.

Still, we’ve long planned to downsize. As empty nesters who live close to our kids, we love our home, but it’s more house than we need. But now, things aren’t so simple.

Even if we move to a home costing half as much as our current home and put 20% down, the new mortgage payment would be higher than our current one because today’s rates are so much higher. Downsizing would still reduce our cash-flow needs by lowering utilities, property taxes, maintenance costs, and insurance premiums, so it’ll likely be the right decision in the short to medium term.

But then, we’d face a familiar dilemma: should we buy the next place in cash, or take out a new mortgage and invest the difference? This isn’t a simple “pay it off or don’t” decision.

Even financial advisors don’t all agree. Some say retirees should do everything they can to enter retirement debt-free and stay that way. Others argue that tying up so much net worth in home equity reduces your retirement income and flexibility.

The real issue isn’t whether a mortgage is good or bad, even in retirement. It’s whether you’re evaluating the right factors so you can make the decision that’s right for you.

Key Takeaways

Paying off your mortgage before retirement isn’t always the safer choice.

Eliminating a mortgage reduces fixed expenses and provides peace of mind, but it also converts liquid, income-generating assets into illiquid home equity. For retirees with low-rate mortgages or limited portfolio size, paying off the loan can actually increase financial risk by reducing flexibility exactly when you need it most.

The mortgage payoff decision must be evaluated as part of your full retirement plan — not in isolation.

Key factors include your mortgage interest rate, the tax consequences of liquidating assets to pay it off, how much of your fixed expenses are covered by guaranteed income sources, and how much liquidity you’ll retain afterward. A large IRA withdrawal to clear a mortgage, for example, can trigger bracket creep, IRMAA surcharges, and a permanently smaller tax-deferred base.

A third option — partial paydown with a dedicated mortgage reserve — often beats paying off or keeping the loan outright.

Recasting the mortgage after a partial paydown, or setting aside short-duration Treasuries or a laddered CD portfolio to cover remaining payments, can capture most of the psychological benefit of debt elimination while avoiding a one-time tax event and preserving liquidity. Most retirees don’t realize this middle path exists until a financial advisor models it alongside the two obvious alternatives.

Why the “Pay Off Your Mortgage Before Retiring” Rule Can Backfire

For many people, the idea of keeping a mortgage into retirement feels not just suboptimal, but outright wrong, maybe even irresponsible.

Blame decades of conventional advice that said the only way to retire responsibly is to pay off your mortgage and any other debt you may have.

That doesn’t mean this view has no merit. If you do this:

- Your retirement expenses are lower, making your lifestyle easier to sustain.

- No lender can come in and take away your home for missing a few payments.

- As a result, there’s the very real emotional comfort of owning your home outright.

That’s why it feels so obvious that if you can pay off your mortgage before you retire, you should absolutely do that.

However, this approach treats your mortgage as a standalone problem you need to solve, rather than as one piece of your larger financial puzzle.

And that’s the pitfall.

Because once you choose to accept that you must pay off your mortgage before retiring, it can dramatically delay your retirement age, just because you haven’t yet “checked that box.”

This, even if your overall financial picture can support it,

The result is that you aren’t optimizing for the life you want to live in retirement. Instead, you’re optimizing for following conventional wisdom that may not be wise for you.

Why Financial Advisors Disagree on Paying Off Your Mortgage in Retirement

Some advisors argue passionately that paying off your mortgage as early as possible, especially if you’re about to retire, or already in retirement, is one of the best moves you can make.

Others make just as strong a case for keeping that mortgage in place, especially if the interest rate is fixed and low.

Both sides’ reasoning is valid, for certain people, in certain circumstances.

A perfect example of why it’s called personal finance.

Advisors who favor paying off your mortgage focus on the resulting simplicity and certainty. It eliminates a high fixed cost from your monthly budget, reducing the retirement income you need. This is especially important during a market crash, when your portfolio is down, and you want to avoid, or at least minimize, selling shares.

Seen from that perspective, retiring your mortgage reduces risk and increases stability.

The advisors who argue the opposite focus on flexibility and opportunity.

If you pay off your mortgage, you’re tying up a large chunk of your investable capital in an illiquid asset that provides no income – home equity. This is often described as a “phantom return” equal to the interest rate of the loan you’re paying off.

As Chris Chen, CFP, Wealth Strategist, Insight Financial Strategists, says, “The decision isn’t as straightforward as having cash hanging around in your checking account. For example, you may have held your 30-year mortgage for, say, 20 years. At that point, most of your payment goes toward paying off the principal, essentially moving money from your checking account into your home equity. Very little goes to interest. Suppose you have to take an IRA distribution to pay off the mortgage. Does that distribution interfere with your other goals, such as Roth conversions? Does the distribution make you jump a tax bracket, resulting in a higher tax bill? There is no way to know until you run the scenario.”

Jeffrey J. Smith, Founder & Managing Partner, Owl Private Wealth Advisors, expands, “Paying off your mortgage for most is a financial goal that has been worked for multiple decades. Up until 2020, many soon-to-be retirees likely had a mortgage rate of 5%+, but now we see that same demographic of soon-to-be or recent retirees locked in at historically low rates sub 4%, these historically low rates have made the decision a bit murkier.

“For many, the decision to pay off or not to pay off the mortgage is part math and part emotion. If they have excess savings in non-qualified accounts, it likely makes sense to pay off the mortgage with those funds simply for the sleep-well factor.

“If overfunded with qualified retirement savings, it becomes more complicated. Paying off the mortgage with those funds will have implications not only for your current tax year but also for 2 years later, with the potential for higher Medicare Income-Related Monthly Adjustment Amount (IRMAA) premiums, given the 2-year look-back. As stated above, this is a personal decision that can only be made after a careful discussion with the client and their advisor on what is best for their personal financial goals.”

Peter Bo Rappmund, Principal at Counterpoint, agrees, “I lean toward paying off the loan when the math is close and the mortgage creates real friction in a client’s retirement plan. The clearest ‘yes’ cases I see are when a client has a higher-rate mortgage (6% or higher) that they took out in the last few years, the payoff doesn’t require liquidating assets that would trigger a meaningful tax event, and after the payoff, they still have 12–24 months of liquid reserves plus comfortable headroom in their portfolio to cover essential expenses. I’m also more inclined to recommend a payoff when a client takes the standard deduction anyway, that, post-Tax Cuts and Jobs Act (TCJA), is most retirees, because they’re getting no tax benefit from the interest, so the mortgage rate is effectively the after-tax rate.

“Behavior matters too. For clients who genuinely sleep better without the debt and who aren’t going to redeploy their freed-up cash flow into something riskier, the psychological return is real and worth pricing in.”

Especially today, when so many mortgages are fixed at historically low rates, like our 30-year fixed 3% loan. That’s a very low return compared to what that capital could likely earn if invested for retirement income.

According to DQYDJ.com, the median net worth for Americans in their late 60s is $394k. That’s not very high relative to what’s needed for a comfortable retirement. Worse, however, is that two-thirds of that net worth is tied up in home equity, leaving just $132k to generate income to supplement Social Security retirement benefits.

Anything that ties up a large fraction of your net worth in home equity makes it that much harder to have a reasonable retirement income.

Seen from this perspective, a mortgage isn’t just a liability. It’s a tool for maintaining liquidity, increasing retirement income, and increasing your margin of safety.

That’s why the argument isn’t really about whether keeping a mortgage is good or bad.

It’s about what risk you’re trying to reduce or remove, and which risk you’re more comfortable living with.

Do you prefer predictability and stability, risking a lower standard of living, or would you rather optimize for higher income along with potentially better long-term outcomes?

Neither is universally better.

Each solves for different objectives, which is what makes this a matter for careful, personalized assessment.

How Paying Off Your Mortgage Affects Your Entire Retirement Plan

From the above, it should be clear that framing this as a “mortgage = good/bad” decision is what leads to confusion and disagreement.

Because paying off your mortgage isn’t a simple decision with pros and cons that are independent of the rest of your financial picture.

It’s just one part of your overall finances, along with your income, investments, and spending, and how large or small, and how flexible or fixed, they are.

It’s more useful to shift the question from “Should I pay off my mortgage before or early in retirement?” to “How does paying my mortgage off before retirement (or in early retirement) affect my overall financial safety?”

Once you change your perspective like that, whether to keep the mortgage or pay it off stops being a standalone decision and becomes an integral part of your overall financial plan.

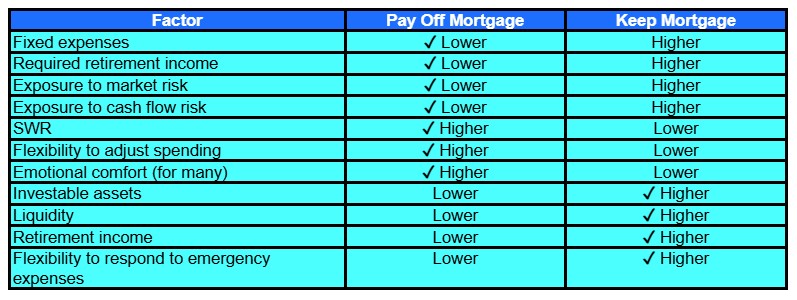

Paying off your mortgage:

- Reduces your fixed expenses.

- Lowers the retirement income you need to generate.

- Per research by David M. Blanchett, PhD, CFA, CFP®, reducing the fixed fraction of your retirement budget lets you increase your safe withdrawal rate (SWR) by ~7% (Blanchett, Head of Retirement Research at Morningstar Investment Management, found that reducing your fixed expense fraction from 75% to 25%, with certain reasonable assumptions, increases SWR from 4.1% to 4.4%).

However, paying off the mortgage also:

- Reduces your investable assets.

- Reduces your retirement income.

- Reduces liquidity and flexibility to respond to unexpected expenses and/or unexpected opportunities, should your circumstances change.

Obviously, keeping your mortgage does the opposite.

- Keeps fixed expenses higher.

- Requires higher retirement income.

- Reduces SWR.

- Keeps investable assets higher.

- Increases retirement income.

- And maximizes liquidity and flexibility.

That’s the trade-off most people miss.

They focus solely on the mortgage decision and miss its implications for flexibility, adaptability, and safety in retirement. And, in retirement, adaptability and safety are every bit as important as optimization, if not more so.

Table 1 shows the factors affecting your decision and how each influences it. In each line, the check mark indicates the preferred outcome.

Why Fixed Expenses Matter More Than Most People Realize

While you’re working, fixed expenses can be a very good thing.

A fixed-rate mortgage means your principal and interest payment never increases during the life of the loan. No landlord raising rents, and no variable-rate loan letting the lender increase your interest rate when the market turns against you.

Predictable and stable.

As long as your income stays stable, you have little to worry about. And if something unexpected happens, you can, e.g., work longer hours, start a side gig, and/or cut expenses elsewhere.

In retirement, your earnings stop.

Instead, you depend on Social Security, pensions, if any, annuities, if any, and withdrawals from your portfolio.

The first three are predictable, but small to non-existent for most people.

The main source for a comfortable retirement is the last, portfolio-based, assuming you saved enough. Unfortunately, the markets are anything but predictable.

On average, stocks return about 10% a year. But they could gain 50% one year and drop 40% the next.

That’s why flexibility and margin of safety matter even more in retirement.

Fixed expenses like a mortgage, that can’t easily be reduced, make you less flexible.

If markets decline or expenses spike, especially early in your retirement, you have lower discretionary spending, reducing the area where it’s usually the easiest to trim costs when needed.

If you need to cover higher expenses and/or have to sell more shares at depressed prices during a bear market to make ends meet, your risk of running out of money increases.

On the flip side, if more of your spending is discretionary, you have more levers to pull to respond to a market crash and/or an expense spike. You can temporarily reduce travel, delay replacing the car, scale back gift-giving, etc., all without disrupting your core lifestyle for long.

On the other hand, even with somewhat higher fixed expenses, a significantly larger portfolio increases your baseline retirement income, which gives you a greater margin of safety, either by allowing you to increase your discretionary spending even more (so a larger fraction of your budget is discretionary) or by drawing a smaller percentage of your portfolio value each year.

Why Downsizing Doesn’t Eliminate the Mortgage Trade-off in Retirement

Downsizing seems like an attractive option for many retirees facing cash-flow limitations.

You sell an expensive home that’s larger than you need, and buy a smaller, less expensive one. This lets you eliminate your mortgage or at least replace it with a smaller loan.

Ideally, that smaller loan means lower monthly payments.

Except when it doesn’t, like in our case.

As mentioned above, our current mortgage rate is so much lower than the current market rates that we could move to a home that costs half as much as our current one, take a new mortgage with 20% down, which would significantly reduce our mortgage balance, and end up with a higher monthly payment than what we’re paying now.

At the same time, downsizing will reduce other costs:

- A smaller home is easier to manage and cheaper to maintain.

- It also tends to reduce utility expenses.

- A less expensive home usually means lower property taxes.

- It’s also typically less expensive to insure.

All of these reduce monthly cash flow needs, which is an important goal in retirement.

So, we’re still likely going to downsize, at which point we’ll come up against a similar trade-off. What do we do with the equity we unlock from our current home when we sell it?

Do we use most of it to buy a less expensive home outright, with no mortgage, or do we use a small portion of that equity to put down just 20% for a new loan?

This decision goes back to the trade-offs we described above, for eliminating your mortgage before retirement or keeping it in place.

The former would dramatically reduce our cash flow needs and fixed expenses. Still, it would also cost us the opportunity to increase our investable assets and the greater margin of safety that higher retirement income provides.

The latter would reduce our cash flow needs and fixed expenses, but nowhere near as much, because we’d still have the large mortgage payment. However, it would significantly increase our portfolio size, and, along with that, our retirement income and the resulting margin of safety.

Downsizing changes the specifics, but it doesn’t eliminate the trade-offs and the decision.

A Better Framework for Deciding Whether to Pay Off Your Mortgage in Retirement

As we said before, there isn’t a single, universally correct answer that tells you to eliminate your mortgage before retirement (and stay debt-free thereafter), or not.

But that doesn’t mean you have to guess.

You just need better questions and a better decision framework.

Rather than considering the mortgage payoff question in a vacuum, you need to evaluate the multiple impacts on your overall financial situation.

- With the mortgage vs. without it, how much of your budget is fixed and non-negotiable, and how much is discretionary? The higher your fixed expenses, the more income you need in retirement, regardless of your portfolio’s performance in any given year. This puts more pressure on your investments and makes it harder to adapt when needed.

- Next, how much of your fixed expenses are covered by predictable sources like Social Security retirement benefits (which also get adjusted up for inflation), pensions, and annuities? The higher the portion of fixed expenses that you can cover from predictable income, the less you need to take from your portfolio, which is especially important when, not if, the market crashes. This gives you more flexibility in managing your investments.

- Now, look at liquidity. How much of your net worth is tied up in your home equity, which is illiquid and doesn’t generate income that lets you cover unexpected (or even planned-for) expenses? Paying off the mortgage (and not taking out a new one) increases the part of your net worth that’s tied up and non-productive like that. Keeping your mortgage (or taking out a new one when downsizing) does the opposite.

- Beyond the numbers, it’s time to look at the emotional aspect. When the market crashes, how comfortable will you be with having to continue making fixed mortgage payments? Or would eliminating that mortgage make it easier to stick with your financial plan? Your answers to this point are at least as important as the results of the above three calculations.

- Finally, consider your margin of safety. Is your portfolio large enough to comfortably support your lifestyle, even when things don’t go exactly as planned? Or are you so close to the edge that you need to do something to increase your margin, e.g., by increasing your productive investments?

Putting all these factors together is how you can make a holistic decision that accounts for the multiple ways that eliminating or keeping the mortgage will affect your retirement in the long term.

After all, that’s the critical goal here.

Not to become debt-free at all costs, and not to maximize returns at all costs.

But to build a plan that offers you a combination of stability, flexibility, margin of safety, and long-term sustainability that you’re most comfortable with and lets you stick with the plan.

Rappmund offers a comprehensive, balanced look at when to pay off vs. when not to. “I lean toward paying off the loan when the math is close, and the mortgage creates real friction in a client’s retirement plan. The clearest ‘yes’ cases I see are when a client has a higher-rate mortgage (6% or higher) that they took out in the last few years, the payoff doesn’t require liquidating assets that would trigger a meaningful tax event, and after the payoff, they still have 12–24 months of liquid reserves plus comfortable headroom in their portfolio to cover essential expenses. I’m also more inclined to recommend a payoff when a client takes the standard deduction anyway, that, post-Tax Cuts and Jobs Act (TCJA), is most retirees, because they’re getting no tax benefit from the interest, so the mortgage rate is effectively the after-tax rate.

“Behavior matters too. For clients who genuinely sleep better without the debt and who aren’t going to redeploy their freed-up cash flow into something riskier, the psychological return is real and worth pricing in.

“I push back hard when paying off the mortgage would require a large taxable distribution from a traditional IRA or 401(k), or a concentrated capital gains realization. Especially if it pushes the client into a higher marginal bracket, triggers IRMAA surcharges, or causes more of their Social Security benefit to become taxable.

“I also advise against it when the mortgage is a legacy (3% or lower) loan; that’s an inflation hedge and a negative-real-rate liability you generally don’t want to retire early. And I won’t sign off on a payoff that leaves a client house-rich/cash-poor, because home equity is the least useful asset in a downturn. You can’t eat it, and a Home Equity Line of Credit (HELOC) can be frozen by the bank at exactly the time you need it most.”

But even when the math seems clear, mistakes are common. Rappmund shares several common mistakes people make: “The single most common mistake I see is comparing the mortgage rate to a hoped-for portfolio return without adjusting for risk, taxes, or sequencing. A client says, ‘My mortgage is 4%, and my portfolio earns 8%, so it’s obvious.’ That comparison is wrong on two fronts: paying off the mortgage is a guaranteed, after-tax return equal to the mortgage rate, while the 8% is a pre-tax, risk-bearing expected return that includes years like 2008. The right comparison is the mortgage rate vs. the after-tax yield on a similar-duration, low-risk bond. On that basis, the decision is much closer than people think.

“The second mistake is solving for net worth instead of cash flow. Retirement is often fundamentally a cash-flow problem, not a balance-sheet problem. Two clients with identical net worth can have radically different retirement experiences depending on how much of their monthly expenses are fixed and inflexible.

“And the third, which I see all the time, is making this decision in isolation, separate from the tax plan. Pulling $300k out of an IRA in a single year to clear a mortgage can cost a client tens of thousands in avoidable taxes and Medicare premium increases, and it permanently shrinks the tax-deferred base that was going to compound for the next 20 years.”

So how should you actually evaluate the trade-offs? Rappmund describes how he helps clients with this, “I help clients weigh the tradeoff between reducing fixed expenses and preserving liquidity and investment income in retirement by separating the question from the math and asking what role this decision plays in the plan. We map out essential expenses (housing, food, healthcare, insurance) vs. discretionary, and we look at what’s already covered by guaranteed income (Social Security, pensions, and annuities).

“If the mortgage payment is the difference between essentials being covered by guaranteed income and not, that’s a strong argument for retiring the debt; you’re effectively buying yourself a higher floor and reducing sequence-of-returns risk in the early retirement years, which is when portfolio damage is most permanent.

“From there, we run the actual numbers in the financial plan, modeling paying it off, keeping it, and a third path. And I almost always show a third option, because most clients don’t realize it exists. That path is something like recasting the mortgage after a partial paydown or carving out a dedicated mortgage reserve in short-duration Treasuries or a laddered CD portfolio that earns close to the mortgage rate and gives the client the option to extinguish the loan later if rates or circumstances change.

“That tends to be the right answer surprisingly often, as it captures most of the psychological benefit and avoids a one-time tax event. The frame I leave clients with is that liquidity is itself a form of insurance, and in retirement, it’s one of the cheaper kinds you can own.

“Paying off the mortgage converts a flexible asset (cash and securities) into an illiquid one (home equity), and that conversion is irreversible without taking on new debt at whatever rates happen to exist when you need it. So, the question isn’t really ‘should I pay it off?’ Rather, it’s ‘what’s the right amount of fixed-expense reduction I can buy without giving up more flexibility than I can afford to lose?’”

The Uncomfortable Truth About Entering Retirement Debt-Free

For many retirees or near-retirees, believing the conventional wisdom that “you must enter retirement debt-free” is worse than outdated.

If accepting that paying off your mortgage is a go/no-go gate for entering retirement forces you to:

- Delay retirement for years.

- Tie up too high a fraction of your capital in home equity that generates zero income.

- Reduce your liquidity to the point where you have no good options when something unexpected happens.

Then, following this “rule” can increase your risk and possibly cause you far more financial harm than good.

It’s counterintuitive. Eliminating your mortgage feels like it should reduce your risk, but in some situations, it can leave you more exposed rather than less.

It removes a fixed obligation, simplifies your finances, and reduces the retirement income you need. But it does so while reducing your retirement income, increasing the risk that you’ll need to sell assets when they’re depressed, and leaving you with less liquidity and flexibility.

Over a decades-long retirement, in many situations, those risks may be the ones you’re less comfortable carrying.

That’s why there isn’t a universally correct answer to the question of eliminating your mortgage before retiring. It’s because the “enter retirement debt-free” rule, like any other financial rule, is designed to offer a simple shortcut for making decisions.

But your situation isn’t simple.

It’s multi-faceted and different than anyone else’s.

A complexity that simple “rules” can’t capture.

The Bottom Line: Should You Pay Off Your Mortgage Before Retiring?

As frustrating as it may be, I can’t give you an answer on whether you should wait until you’ve paid off your mortgage before entering retirement, or even whether taking out a new mortgage in retirement when downsizing makes sense.

That’s because my answer is just that – mine.

You need your answer.

And that answer depends on many factors:

- How large is your nest egg?

- How high a retirement income do you need to be comfortable?

- How will paying off your mortgage affect those two answers?

- What risks are you comfortable carrying, and which ones do you need to avoid?

- Which decision gives you the best chance of sustaining your desired lifestyle in retirement over the long haul?

- Can you, emotionally, stick with a plan that keeps a mortgage into retirement?

For many people, these factors result in a preference for paying off their mortgage.

For many others, they’ll point to keeping the mortgage in place for as long as possible.

Both approaches are right, given the right circumstances. And both are wrong given the wrong situation.

Your bottom line must be based on a clear understanding that the mortgage payoff decision must be made as part of a comprehensive assessment of your personal situation, goals, and risk preferences.

Because to have a good retirement, your decisions can’t be based on box-checking.

They need to be made as part of a comprehensive plan that you can live with and stick to, through good markets and bad, because you will live through both.

As Dr. Steven Crane, Founder of Financial Legacy Builders, says, “I’d only strongly recommend paying off a mortgage if the payment is creating stress or the person needs simplicity to sleep at night. Beyond that, the math doesn’t always support it. I actually push back on people who rush to pay it off just because it ‘feels safe.’ In a lot of cases, they’re trading liquidity and flexibility for a psychological win.

“The biggest mistake is treating the mortgage like the enemy instead of looking at the full picture. I’ve seen retirees drain a large chunk of their savings to wipe out a low-interest mortgage, only to put themselves in a tighter position long term. They feel better emotionally, but financially, they’ve boxed themselves in. I frame it as control vs. comfort. Paying off the mortgage gives you comfort, no payments, and a clean slate. Keeping the mortgage often gives you more control, more liquidity, and more flexibility if something changes. Most people default to comfort without realizing what they’re giving up. Debt isn’t the problem in retirement. Poor planning is. A mortgage can be managed. Running out of options can’t.”

A practical way to start is this: picture both scenarios.

One where your mortgage is gone, but your portfolio is smaller, and one where your mortgage remains, but your portfolio is larger and more flexible.

Which scenario gives you more confidence that you can handle whatever comes next?

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor