What this article covers

Massachusetts advisors explain how one-time income events — RSU vests, business sales, large Roth conversions — can unexpectedly trigger the state’s 4% millionaire tax surcharge, and why proactive timing is the only reliable way to avoid the damage.

Massachusetts has one of the country’s heaviest state tax burdens.

According to the Tax Foundation, it ranks eighth nationally in per-capita state and local tax collections, at $9,341 per resident, more than 30% above the national average

But even if you earn a high income, you may assume that Massachusetts millionaire tax surcharge will never affect you, because you don’t make a seven-figure salary.

And most years, you’d be right.

But then you complete a business sale, get a large bonus, Restricted Stock Units (RSUs) vest, or carry out a large Roth conversion. And suddenly, a year that felt financially successful now comes with a state tax bill thousands, or even tens of thousands of dollars higher than you expected.

Worse, many of the best opportunities to reduce the damage may already be gone by the time you realize it happened.

Key Takeaways

You Don’t Need a Seven-Figure Salary to Trigger Massachusetts’ Millionaire Tax Surcharge

A large RSU vest, business sale, Roth conversion, or sale of appreciated assets can push an otherwise mid-six-figure earner above the 4% surtax threshold in a single year. Once that happens, a significant portion of income gets taxed at 9% or more — and most of the best opportunities to reduce the damage are already gone.

Massachusetts Tax Planning Is Not the Same as Federal Tax Planning with Different Numbers

Massachusetts applies its own income categories, sourcing rules, and residency requirements that diverge meaningfully from the federal tax code. Short-term capital gains are taxed at 8.5%, collectibles gains at 12%, and MA-sourced income can create tax obligations even after you move. Optimizing your federal return while ignoring these rules can still produce a costly state tax surprise.

The Best MA Tax Strategy Is Proactive Income Timing, Not Moving or Loopholes

Spreading income across tax years, sizing Roth conversions to stay under the surcharge threshold, structuring business sales as installments, and aligning charitable giving with high-income years can significantly reduce exposure. Moving to a no-income-tax state rarely solves the problem — MA taxes most income earned in the state regardless of where you live.

Massachusetts Tax Planning Isn’t Just Federal Tax Planning with Different Numbers

Massachusetts has its own tax rules, surcharges, income categories, sourcing rules, and residency complexities. These differ from the federal tax code in several important ways.

For most income, Massachusetts applies a flat 5% state income tax rate. But income above the millionaire-tax threshold gets hit with an additional 4% surtax. The threshold adjusts annually for inflation and is $1,107,950 for 2026.

Massachusetts also taxes some categories of income differently:

- STCG is generally taxed at 8.5%.

- Long-term gain (LTCG) from selling or trading collectibles is taxed at 12%

- Residency and MA-sourced income rules can create tax obligations even after you move.

All this means that you can do a good job managing federal taxes while still creating avoidable Massachusetts tax consequences.

In many cases, the most valuable planning opportunities exist only before a major taxable event occurs. Once the event happens, most such options are gone. That’s because filing taxes correctly and planning major income events strategically are not the same thing.

According to financial professionals who work with high-earning MA residents, the biggest opportunities usually come from proactive planning around timing, structure, and income recognition, not aggressive tax tricks.

Joon Um, CFP®, EA, CLU®, ChFC®, of Secure Tax & Accounting, says, “One of the biggest mistakes high earners make is assuming federal tax strategies automatically work the same way in Massachusetts. For people earning over $1M, the biggest savings usually come from planning early around stock comp, business structure, residency, and timing of income, not aggressive tax tricks.”

And this is especially important in tax years where your income is unusually high.

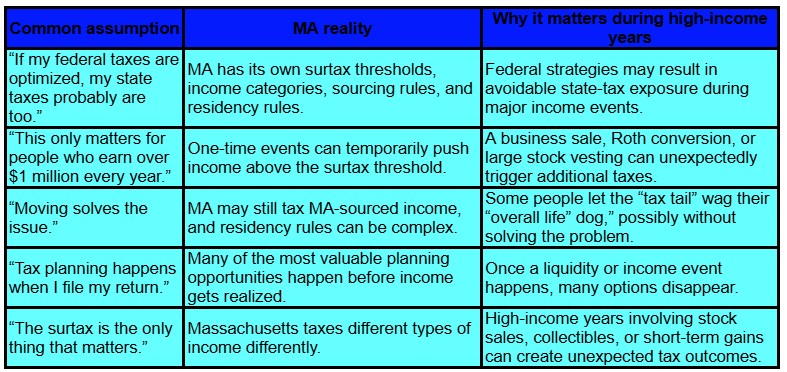

Table 1 discusses common assumptions regarding tax laws and how they break down when it comes to Massachusetts state income taxes.

How a Single High-Income Year Can Trigger Massachusetts’ Millionaire Tax Surcharge

Advisors point out that Massachusetts’ high tax bite isn’t limited to the top 1% (or 0.1%) of earners who routinely exceed the millionaire-tax surcharge threshold.

Many more people hit the threshold because one or more one-time income bumps hit in the same tax year.

Chris Chen CFP, Wealth Strategist, Insight Financial Strategists, says, “Many people will say that they are not at $1M of income (yet). However, the sale of a business, vesting options or RSUs, a large Roth conversion, or the sale of a vacation home, among other events, can easily push someone over the threshold and result in a surprise assessment.”

Even if you earn a mid-six-figure annual income most years, you don’t think of yourself as the intended (or likely) target of the 4% millionaire-tax surcharge. But a single, especially high-income year can cost you tens of thousands of dollars that could be mostly avoided, if you take the proper advance planning steps.

For example:

- A large block of RSU vests.

- You sell a large amount of appreciated stocks, bonds, or other financial assets

- You get an especially large bonus.

- You decide to proactively address your eventual Required Minimum Distribution (RMD) problem by doing a Roth conversion.

- You sell a significant short-term trading position, causing a large short-term capital gain (STCG), that’s taxed at 8.5% while also pushing you toward millionaire-tax surcharge territory.

- You sell a business in return for a large lump sum.

- You sell a vacation home that has appreciated in price.

None of these moves are intrinsically bad.

It’s just that a combination of them can unexpectedly push you above Massachusetts’ millionaire-tax surcharge threshold, and suddenly a large portion of your income gets taxed at 9% or more.

This shows that income timing and structure matter much more than many people realize.

Between these, and the misconception that optimizing for federal taxes means your Massachusetts state tax mostly “takes care of itself,” come Tax Day, you could find yourself staring at a shockingly high state tax bill.

Why Timing Matters More Than Tax Tricks

Many online sources tout aggressive tax tips and exotic “loopholes the rich use” as ways to lower your taxes.

These are often unrealistic and/or unlikely to survive serious scrutiny.

Instead, what financial planners advise is planning and timing your income in the most advantageous way. This means:

- Spreading income across multiple tax years when you can.

- Managing Roth conversions strategically so they don’t spike your taxable income in the same year that sees other one-time income boosts.

- Structuring business sales thoughtfully, possibly taking payments in several annual installments.

- Batching charitable giving from several lower-income years to a single especially high-income year.

- Understanding how your different types of income get taxed, and how they interact.

Chen says, “One of the easier examples of planning could be to size a Roth conversion so that total income falls under the $1,107,950 threshold in 2026.”

He also notes that some income spikes can be set up in installments to avoid the millionaire surtax, “Sometimes, these events can be planned to reduce the impact. A business owner could structure the sale of their business around their other income and the $1,107,950 threshold. For example, assuming little other income, they could plan for installments of, say, $1M, instead of taking a lump sum.”

The goal isn’t to eliminate taxes. It’s to prevent a temporary high-income year from leading to unnecessarily large tax liability.

For most affluent residents, that’s a far more realistic approach than making major life decisions primarily around taxes.

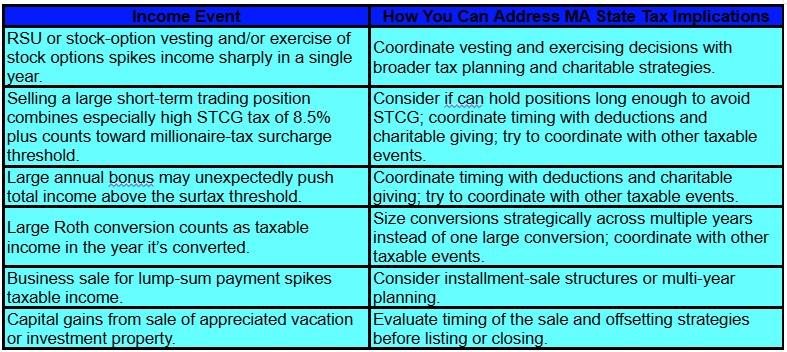

Table 2 lists some of the most likely culprits that could push income high enough to result in an outsized Massachusetts state income tax bill, and how you may be able to avoid it.

All of these strategies require advance planning and taking tax-mitigation action proactively, rather than waiting for tax-filing season, by which point most of these opportunities have evaporated.

What Massachusetts-Savvy Advisors Often Evaluate First

The best tax-reduction value comes less from deductions than from sophisticated tax planning.

As Um shares, “Usually, the first thing I review is where the income is coming from and whether planning could have been done before a major bonus, sale, or liquidity event.”

Here’s what advisors working with affluent Massachusetts residents look at first.

- What are your income sources and how do they get taxed?

- Could several major taxable events stack in a single year?

- If so, how can we improve their timing to reduce taxes?

- How can we best align your charitable goals with high-income years?

- Will your proposed residency assumptions, if considered, hold up under scrutiny?

Most advisors recognize that simply moving out of state isn’t necessarily the right move.

Chris Chen says, “The biggest mistake would be thinking that relocating to a neighboring state, often NH or FL that do not have income taxes, will fix the problem. In general, a taxpayer would still be liable for Massachusetts sourced income.”

He adds, “Most Massachusetts residents with earned income in excess of $1M earn that money because their job or their business is in the state. Which means that moving is often not practical.”

Um notes, “I’ve definitely seen people consider moving because of state taxes, but states are getting much more aggressive with residency audits now.”

That’s not to say that moving never makes sense.

It may make perfect sense for some retirees or people with highly flexible income sources, especially if community, friends, and family considerations don’t make staying the right choice.

As Chen notes, “I know some millionaire earners who relocated due to the new millionaire tax. However, according to state data, most millionaire earners have not pulled the plug to relocate. That being said, people who have moved into retirement with that level of income are much more likely to move elsewhere.”

But most affluent Massachusetts residents are probably better served by understanding how their income, timing, and major financial decisions interact with state tax rules before considering massive life changes.

The Bottom Line: Massachusetts Tax Exposure Is Manageable If You Plan Before the Income Event

As unappealing as the Massachusetts millionaire tax surcharge is for high earners in the state, it’s far less catastrophic than many online sources make it sound.

Especially if your baseline annual income isn’t in the multiple-seven-figure range.

However, if you’re a high earner, you may well have a few especially high-income years as a result of one-off income boosts, and face especially high state tax bills in those years. That’s if you don’t proactively plan and execute the most appropriate timing for income and offsets such as charitable giving.

This is especially the case if you, for example:

- Receive large amounts of stock compensation.

- Sell a business or highly appreciated assets, especially if they make you realize STCG.

- Carry out especially large Roth conversions.

- Experience major one-time liquidity events.

The most effective ways to avoid needlessly high Massachusetts state taxes aren’t about aggressive or exotic loopholes, nor about moving out of state if that doesn’t make sense from an overall-life perspective.

It’s about understanding how MA-specific tax rules interact with your major income events, and taking appropriate action to time them optimally, before they occur.

Because once a major taxable event already happened, the best opportunities to reduce the resulting Massachusetts tax bill have likely already evaporated.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher