Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Why the first five years after you stop working may determine if your retirement survives, and what to do about it

In this article, we look at:

- Why the first five years of your retirement are especially dangerous.

- How sequence-of-returns risk can derail your retirement.

- What research says about retirement failures.

- Practical strategies that can protect your retirement plan.

- What you have to avoid doing to prevent a bad situation from turning much worse.

What We Tend to Focus On

Although I worked for 40 years, for the first 25 of those, I earned too little to set aside much, if anything, for retirement.

That’s why, during the remaining 15 years, I did (almost) everything I could to build up our nest egg. Beyond investing significant amounts each of those 15 years, and picking (mostly) the right funds, I have to acknowledge that luck played a role, too. During that period, the market significantly outperformed its long-term average, giving us a strong tailwind.

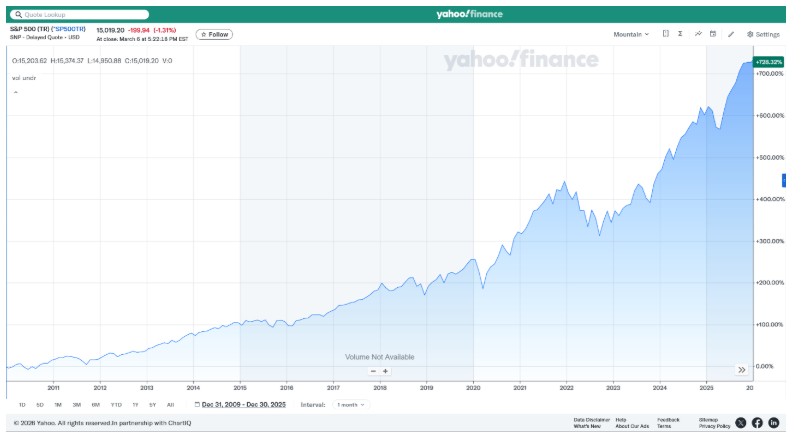

From 2010 to 2025, the S&P 500 achieved a 728% total return (Figure 1), a nominal annualized return of 14.1%, and an inflation-adjusted annualized return of 11.3%. That’s almost 80% higher than 16 years would have returned at a 10% annualized rate.

Between our efforts and favorable markets, by the end of 2025, I reached “work optional” status and decided to mostly retire. I add that word, “mostly,” because I continue to do some consulting work and also get paid for writing these articles.

When You Retire Matters, a Lot!

First, let’s acknowledge that the year you retire can have a massive impact on your retirement portfolio.

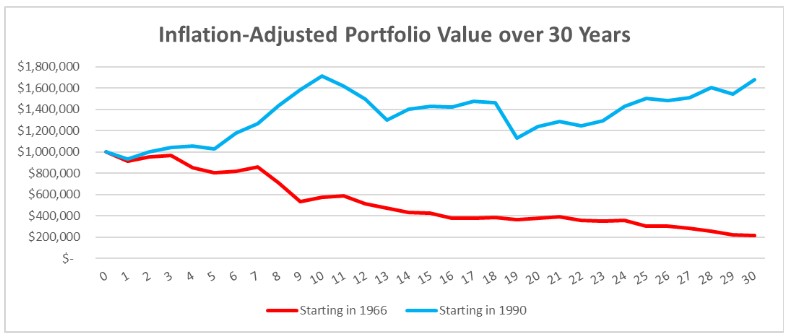

Let’s look at inflation-adjusted portfolio value over the course of a 30-year retirement for two hypothetical retirees using the 4% rule. The first, less fortunate one retired in 1966, while the second “chose” to retire at a much more fortunate time, in 1990.

As Figure 2 shows, after 30 years in retirement, the 1990 retiree’s portfolio was worth, after adjusting for inflation, nearly 70% more than its initial value, while the 1966 retiree’s portfolio lost nearly 80% of its initial value. Overall, the difference over 30 years was nearly 8-fold!

The Pitfall Most of Us Don’t Consider

It’s possibly the biggest risk to retirement success.

The so-called “sequence of returns risk,” i.e., the order in which market gains and losses happen, may matter more than your average returns.

Catching a good break here, or a bad one, can make or break retirement success. Especially if your retirement lasts much longer than 30 years.

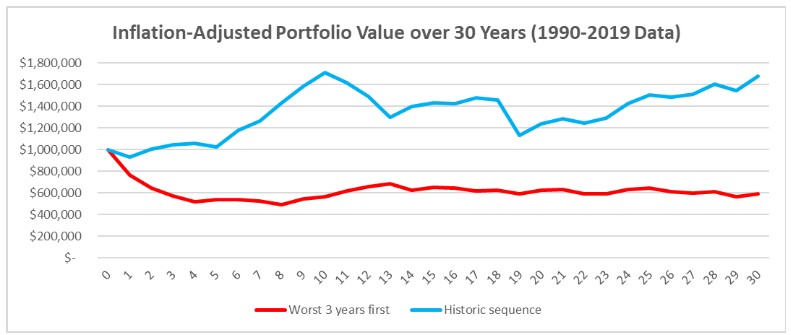

Take a hypothetical retiree who retired in an “alternate-history” 1990, where market returns for the following 30 years stayed the same, but were reordered such that retirement kicked off with the worst three years, followed by the remaining 27 years in the original order.

Figure 3 shows that despite having the same 30 years’ worth of annual returns and withdrawing the same $40k in inflation-adjusted dollars, the “alternate 1990” portfolio ended 65% lower than that of the retiree who experienced the actual history of returns from 1990. Instead of gaining nearly 70% over 30 years, the “alternate-history” retiree’s portfolio lost nearly 40%.

That’s bad enough, but it can get much, much worse.

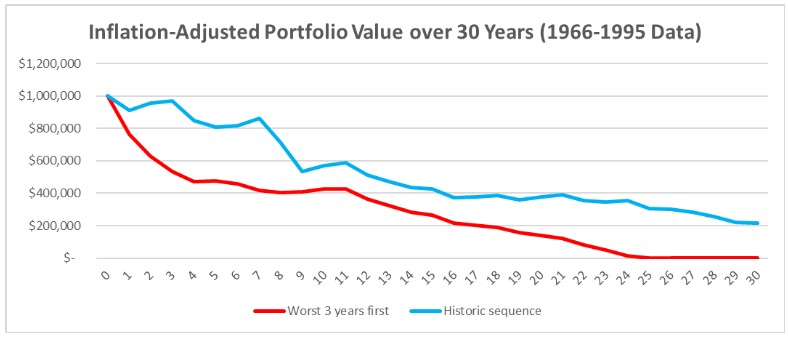

Let’s redo the same exercise with a hypothetical retiree who retired in 1966 vs. one who retired in an “alternate history” 1966. Here, again, the worst three years kicked off their retirement.

As Figure 4 shows, instead of the already less-than-stellar loss of nearly 80% of portfolio value over 30 years, the “alternate-history” 1966 retiree’s portfolio went to zero by their 25th year of retirement. Imagine being twenty-five years into retirement and realizing your portfolio is all gone!

Why such a difference, if they experienced the same set of returns, just in a different order?

Indeed, had there been no annual draws, the portfolios of the 1966 retiree and the “alternate” 1966 retiree would have ended at the same value after 30 years. However, the annual draws were drawn in both cases, but the number of shares the “alternate” 1966 retiree would have needed to sell each year to draw the same $40k would have been much greater than for the original 1966 retiree.

Early losses force you to sell more shares when prices are low, leaving fewer shares available when markets recover.

That’s why the alternate 1966 portfolio failed to survive the full 30 years. It lost too much capital in the first three years, so that even when the remaining “better” 27 years arrived, it was too late to recover.

That’s the nightmare scenario retirees fear most.

The lesson is simple but uncomfortable: retirement success depends not only on how much you saved or even on your average market returns throughout retirement. What markets do during your first few years of retirement can be equally critical.

Is This Just Anecdotal or Systematic?

Research shows that sequence-of-returns risk is more than an anecdotal situation.

According to Morningstar’s “The State of Retirement Income: 2025” report, they ran Monte Carlo simulations and required a 90% success rate for a given strategy. In other words, they defined a successful strategy as one that didn’t run out of money in at least 90% of simulated 30-year market scenarios.

They then checked how the 10% scenarios that ran out of money in less than 30 years differed from the 90% of scenarios that didn’t run out.

They say, “For… the 10% of simulated random trials in which the retiree exhausted their savings before the end of retirement… nearly 70% of these ‘failures’ involved trials in which the retiree’s investments had lost value by the end of year 5 of retirement.”

This implies that market returns in your first five years of retirement may well determine whether your retirement plan succeeds or fails. The first five years are especially important because losses during that period permanently damage a portfolio’s ability to recover.

Ben Simerly, CFP®, Financial Advisor & Founder, Lakehouse Family Wealth, also sees sequence of returns risk as a critical consideration, “As a firm focused on near- and recent retirees, sequence-of-return risk is the biggest monster under the bed that clients don’t know can hurt them. While most prospective clients ask about what sexy stock or fund tip we have or our pricing structure, I don’t think I’ve ever been asked about an early-retirement or near-retirement recession in a first meeting, or what to do about it.

Omar Morillo CFP ChFC AIF, Founder & Senior Wealth Advisor, Imperio Wealth Advisors agrees, “Sequence-of-returns risk is most dangerous in the early years of retirement, when withdrawals begin, and the portfolio has less time to recover from market declines. A practical way to address this is to first secure the spending required for essential expenses through guaranteed income sources. When those core needs are covered, the rest of the portfolio can remain invested with a longer-term perspective rather than being forced into defensive moves during volatile markets.”

Put differently, retirement success often depends less on your average long-term returns and more on what markets do during the first five years after you stop working.

Other Risks Early in Retirement

The sequence of returns is indeed a critical risk, but it’s not the only significant risk. Other risks include:

- Longevity risk: If you live significantly longer than average, your likelihood of running out of money increases.

- Healthcare expense risk: If you suffer catastrophic medical expenses, you have a greater risk of retirement failure.

- Inflation risk: If prices rise faster than your portfolio can accommodate, your risk of failure grows. This relates to your personal rate of inflation, given the categories of goods and services you buy, rather than the generic Consumer Price Index (CPI).

Morillo adds another risk, “Long-term care is another financial risk that retirees often underestimate. A prolonged care event can dramatically increase spending, disrupt a portfolio’s withdrawal strategy, and force the liquidation of assets at unfavorable times. Without a plan for that possibility, even well-funded retirements can face significant strain in later years.”

Chris Chen CFP, Owner, Insight Financial Strategists, cautions of the opposite risk from the sequence of returns, “I’ve observed that it’s difficult for new retirees to look at their retirement risks holistically. Many who are aware of the sequence of risk returns tend to become too conservative, increasing their inflation risk, especially when the expected life expectancy is long. That happens because many who retire at, say, 65, should expect to live another 30+ years, at least from a retirement planning standpoint. So, the financial conservativeness that retirees gravitate to in order to counter sequence of return risk and not run out of money can translate into too much conservativeness that increases the risk of running out of money in a different way.”

How to Mitigate Sequence-of-Returns Risk

As we saw above, the most dangerous years of retirement are usually the first five.

That’s why the strategies below are designed to protect retirees especially during those crucial first years. They can help mitigate the risk that poor early-retirement market returns will eviscerate your portfolio (note that these won’t apply equally for all retirees).

- Phased retirement: If you and/or your spouse continue to bring in part-time non-portfolio income early in retirement, the impact of a market crash is much more muted. This includes cases where one spouse retires before the other. Related to this, if you can “unretire” for a year or two if your portfolio crashes early in retirement, you can avoid selling depressed assets. My wife and I implement this strategy, as she continues to work for a few more years, and I’m just “mostly retired.”

- Buckets strategy: Allocating several years’ worth of expenses to bonds lets you cover expenses during a possible bear market early in retirement without selling any equities. Allocating several more years’ worth of expenses to cash lets you cover expenses without selling either equities or bonds, should both suffer negative returns, until markets recover. In our case, I’m keeping a couple of years’ worth of expenses in cash and another three years’ expenses in bonds.

- Mike Hunsberger, ChFC®, CFP®, CCFC, Owner, Next Mission Financial Planning, agrees, “To protect against sequence of return risk, I typically recommend clients maintain 3-5 years’ worth of spending in liquid, protected investments. This can prevent them from having to take out money if the stock market decreases early in retirement.” Chen also likes the buckets approach, “I use the bucket method to balance the need for low short-term volatility with the need for long-term growth to support a retiree’s lifestyle. I find that it helps create a more stable and more predictable retirement plan.”

- Dynamic withdrawals: Several withdrawal strategies have you reduce your spending if your portfolio value decreases too much. These so-called dynamic strategies include, e.g., the “Guardrails Approach” and the “Risk-Based Guardrails Approach.” Related to this, try to keep your non-discretionary expenses to as low as possible a fraction of your retirement budget. This offers greater flexibility to adjust your spending if and when your strategy requires it. We haven’t had to start drawing on our portfolio yet, but I plan to use a version of the Guardrails Approach once we do.

What Not to Do – How to Avoid Making a Bad Situation Worse

Behavioral finance research shows we feel the pain of loss twice as keenly as we enjoy an equivalent gain. This “loss aversion” creates a psychological trap that’s especially severe if you experience market losses early in retirement.

Before retirement, given that you’re covering expenses from non-portfolio income, market downturns are simply opportunities to buy more assets at a discount. And since most bear markets (losses of more than 20%) reverse in under two years, it’s easier to stay the course.

However, once you retire and live off portfolio income, severe market losses are very triggering. Seeing your portfolio shrink due to market losses, at the same time as it shrinks due to your withdrawals, can be terrifying, even if your plan was designed to accommodate these scenarios.

Brennan Decima, Owner, Decima Wealth Consulting, puts it like this, “One of the biggest risks in retirement is underestimating the impact of a bad market right before or shortly after retirement. Market volatility is an opportunity in the accumulation phase, because regular paycheck contributions take advantage of buying low and speeding up the recovery. However, a major drop in the market around retirement creates quicksand. The market goes down, and now, instead of buying, retirees are forced to sell when the market is down. This risk can be devastating if the right amount of protection is not in place.”

Another behavioral finance factor, recency bias, makes it feel like the losses you’ve just experienced will continue forever.

When markets crash early in retirement, before you’ve had a chance to experience your plan working well, loss aversion and recency bias can make it incredibly difficult to avoid panic selling your depressed shares, locking in losses, and preventing your portfolio from ever recovering, leading to retirement failure.

The same risk mitigation strategies mentioned above can help you avoid your worst instincts from derailing your retirement plan. The goal isn’t just to optimize your retirement math, but also to make it emotionally sustainable in the face of market crashes.

After all, it isn’t a question of “if” markets will crash, but rather of “when” they will do so. And while you can’t control when market crashes happen, you can design a retirement plan that helps you survive them.

Morillo points out a related mistake: “One of the most common mistakes retirees make is entering retirement without securing a reliable income floor. Many people carefully insure against medical expenses through Medicare supplement coverage, yet they leave themselves fully exposed to market volatility. Establishing a baseline of guaranteed income through sources such as pensions, Social Security, or carefully structured annuities can stabilize a retirement plan and reduce the pressure to sell investments during market downturns.”

Hunsberger relates another mistake, “One mistake I see retirees make is underestimating how much they will actually spend in early retirement. Conventional wisdom used to say spending would drop early in retirement. I find that for most retirees, especially early retirees, spending stays level or may actually increase early in retirement as they look to do all the things they put off doing while they were working. Early retirement should be a period of experimentation. Try new things to make sure you have purpose and fulfillment. Both of these things are incredibly important to have a happy retirement.”

Simerly adds several things to be more mindful of beyond simple sequence of returns, “The two biggest areas of sequence-of-returns risk that are typically ignored are asset category withdrawal strategies and investments that focus on results rather than costs. Asset category withdrawal strategies are simply a fancy way to pull cash when markets are down, rather than from the more aggressive investments that need a chance to catch up. In reality, it gets more complex. Do you pull from actual cash? Or money market funds? Or bonds, and which bonds? Or maybe your I-bond account with the treasury department, or should you use the conservative bucket in your advisor’s investment portfolio? And then how do you refill those asset types after drawing them down? How do you handle the reallocation of funds and the creation of income?

“The reality is that most near-retirees and recent retirees, as well as many advisors, are not thinking about these questions. When trouble strikes, they are winging it and have no downturn strategy in place. The second issue of investment costs is one that I believe was created by marketers, not by markets.

“At some point in history, some investment companies realized that if they marketed based on fund cost, it didn’t matter how a fund performed. People flock to low-cost no matter what the outcome. Because investments are all basically the same, right? Wrong. In my opinion, the reality that the wealthy understand is that what is marketed to the general public is usually the cheapest and weakest form of investing. And the kicker? The general public has mostly the same access to better investments as the wealthy. It’s about desire and knowledge to access them, not the access itself. That’s where either some googling or professional help comes into play. In reality, every investor should be focused on the net-return, read: after expenses and fees, over an extended period of time, say 10 years minimum if not far more, alongside net return during downturns.

“In short, focus on after-expense returns and returns during downturns, instead of the expenses. And that’s just the basic principle. In real use, there are a multitude of investments that are built to help reduce downturns, but will still aggressively pursue gains in good times, relative to a desired level of risk. The key advantage of expanding your investment horizons or working with your advisor is that a whole new world of possibilities opens up in reducing the sequence of returns risk and making money last in retirement.”

The Bottom Line

Even if, like me, you’ve been able to accumulate a nest egg sufficient to reach “work optional” status, how the markets behave in the first few years of your retirement can make or break your plans.

That’s why it’s crucial to incorporate into your plan mitigations that reduce the impact of potential early market losses, both in concrete monetary terms and in emotional terms, that let you stay the course without derailing yourself.

Key Takeaways for Pre-Retirees and Retirees Early in Retirement

- Market returns in the first five years of retirement matter far more than most people realize.

- Early losses force you to sell more shares when prices are lowest, and once that capital is gone, recovery becomes extremely difficult.

- Strategies like phased retirement, buckets, and dynamic withdrawals can mitigate this risk.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor