Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

You can manage your own investments. Millions of people do — and some do it quite well. But “can you do it yourself?” has never been the most important question. The better question is: What might it cost you not to have help? In this article, financial writer Opher Ganel — a decades-long DIY investor who recently reached “work optional” status before hiring an advisor for the first time — explores what the research actually says about the value of professional financial advice, the real-world mistakes advisors help clients avoid, and a practical framework to help you decide whether going it alone is still your best move.

If you’re asking whether hiring a financial advisor is worth it, you’re probably closer to the decision than you think.

I came late to this question. I took the DIY (Do It Yourself) route for decades. It worked.

I reached “work optional” status and, three months ago, mostly retired.

Then, as a sanity check, I hired a financial advisor to review my plan.

And that’s when it hit me: Did I miss out on a lot by not working with a financial advisor earlier?

Key Takeaways – Are Financial Advisors Truly Worth It?

The real cost of DIY isn’t the fee you pay — it’s the value you may be leaving behind.

Most DIY investors compare an advisor’s 1% AUM fee against the near-zero cost of managing their own portfolio. But that framing misses the less visible costs: suboptimal tax decisions, behavioral mistakes during market downturns, missed planning opportunities, and the compounding impact of small inefficiencies over decades.

Research shows advisor value goes well beyond investment returns.

According to Vanguard, working with a financial advisor can add an estimated 3% to annual returns — but clients report the most meaningful benefits come from peace of mind, better decision-making, and time saved. In fact, 76% of advised clients reported saving a median of more than 100 hours per year managing their finances.

The right question isn’t “do I need an advisor?” — it’s “would I do better with one?”

DIY investing can be a smart, legitimate approach — especially if your finances are straightforward and you’re disciplined. But for those approaching major financial events, managing growing complexity, or simply wanting to optimize rather than settle for “good enough,” a skilled advisor can deliver value that compounds just as powerfully as the returns they help protect.

Why DIY Investing Isn’t Enough on Its Own

Anyone can invest. That’s the easy part now.

With a few clicks, you can:

- Open a brokerage account.

- Invest in low-cost index Exchange-Traded Funds (ETFs).

- Build broad diversification at minimal cost.

- Automate contributions.

- Rebalance periodically.

- Let time do the heavy lifting.

So, it’s a fair question.

If it’s simple enough to do with a few clicks every few months, is paying for a financial advisor’s help worth the cost?

Understandably, most people look at the prevalent 1% of assets under management (AUM) annual fee and think it sounds like a lot, especially compared to what feels like a near-zero-cost DIY approach.

And sometimes it is.

But framing it like that misses a more interesting and important question: What might it cost you to keep going without an advisor?

Because it isn’t simply 1% of, e.g., a $1 million portfolio, i.e., $10k a year vs. no cost for DIY.

It’s that 1% vs. several less obvious costs:

- Missing opportunities to improve returns or reduce risk.

- Making costly behavioral mistakes, like panic-selling at the worst time.

- Leaving tax savings and planning opportunities untapped.

- Making suboptimal decisions because you’re operating without coordinated expertise.

This is where I am now. Sure, I’ve been very successful by almost any metric. But how much more successful might I have been had I hired a great advisor 10 or even 15 years ago?

Not because what I did was wrong, but because it may not have been optimal.

Should You Hire a Financial Advisor? Here’s a Quick Answer

At the most basic level, here’s who’d be more likely to benefit by working with a financial advisor and who wouldn’t.

You’d be more likely to benefit from professional advice if:

- Your financial life is becoming more complicated.

- You’re not completely confident you’re optimizing what you’ve built.

- You’d rather not spend the time managing every detail yourself.

- You want a second set of eyes to help you avoid mistakes.

- You want more than “fine.” You want “optimal.”

DIY may be your better bet if:

- Your finances are relatively simple.

- You follow a disciplined, low-cost approach.

- You’re comfortable making and sticking to long-term decisions.

- You prefer to go with “simple, inexpensive, and fine” over “optimal.”

- You enjoy managing your money and staying on top of it.

Most people who consider hiring an advisor find themselves somewhere in between.

If that’s you, ask yourself which sounds closer to your situation. And keep in mind that your answer may very well change over time.

That’s why, in this article, instead of considering if you need an advisor, we’ll dig into whether working with an advisor could help you do better, not just financially, but in how you use your time and make decisions.

What Does Research Say About the Value of a Financial Advisor?

The headline number is eye-popping.

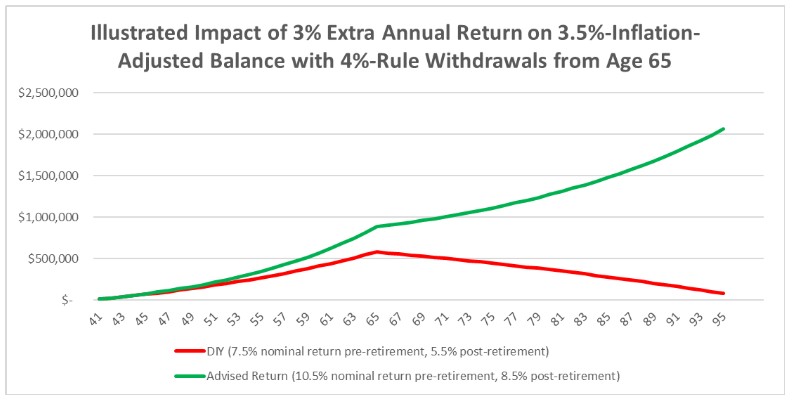

According to Vanguard, advisors add an estimated 3% to their clients’ annual returns. Figure 1 uses that 3% number to illustrate the possible impact of such an excess return over an investment lifetime, with the DIYer reaching the end of Year 30 of retirement with an $81k inflation-adjusted balance and the advised investor reaching a $2.1 million inflation-adjusted balance at that point (an example scenario, not a guaranteed result).

It’s important to note that the above number, as widely quoted as it is, is an estimate. Your actual results will be affected by, e.g., how well you respond to behavioral coaching, asset allocation advice, and cost-control recommendations.

A survey of Vanguard advisor clients reports that said clients attribute one-third of their three-year returns to their advisors’ help. Note that although this is client perception, not a measured increase in returns, it does highlight how those clients view the financial value of the advice they received.

But research suggests that the value of advice comes less from outperforming markets and more from improving behavior, tax efficiency, and decision-making.

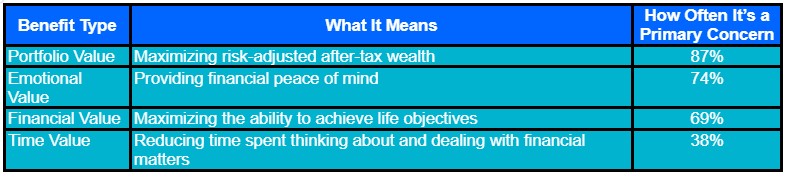

A recent Vanguard paper, The emotional and time value of advice, says the focus “often overlooks other important benefits that investors gain from paid professional financial advice, such as peace of mind and the time they save by delegating their financial lives to an advisor,” and offers the following more complete list of benefits:

- “Portfolio: Maximizing risk-adjusted after-tax wealth.

- “Emotional: Providing financial peace of mind.

- “Financial: Maximizing the ability to achieve life objectives.

- “Time: Reducing time spent thinking about and dealing with financial matters.”

Vanguard’s research found that 86% of advised clients reported experiencing the above emotional benefit (88% of clients advised by a human), and 76% reported experiencing the above time benefit, reporting a median annual time saving of over 100 hours thinking about and dealing with their finances (78% of clients advised by a human).

When asked for their primary reasons for seeking out advice, Vanguard found the following (Table 1):

- Portfolio value: 87%.

- Emotional value: 74%.

- Financial value: 69%.

- Time value: 38%.

Thus, it’s clear that the emotional and time benefits were experienced even by clients for whom these weren’t the primary motivation for seeking advice.

Another Vanguard paper, Assessing the value of advice, found that clients who rated their advisory service most highly ascribed 45% of the value they received to the emotional value of the service.

In plain English, this means a good advisor offers far more value to clients, including helping you make better decisions, reducing your financial stress, saving you time, and improving coordination across the full breadth of your financial picture.

This doesn’t mean that every advisor will be a good fit for you (or a good advisor, period), nor that you personally need an advisor.

What it does mean is that when considering whether or not you’d benefit from hiring a good advisor, you need to think more broadly than simply about improving your investment returns.

What Most DIY Investors Get Wrong About Financial Advice

The value of financial advice is not primarily about investment selection. It’s about improving decisions, coordinating complex financial choices, and reducing costly mistakes over time.

Research can, and does, tell you what value a good advisor can provide, and how widely that’s valued by clients.

What it misses is how and why a good advisor can provide that benefit in ways that exceed what DIY investors achieve.

And that’s why most people underestimate the difference.

Having helped clients as a coach in the past, I came across an interesting saying, “You can’t read the label if you’re inside the jar.”

Whether a coach or an advisor, that’s a big part of how and why you can help people who are already knowledgeable. It’s the outside perspective, unclouded by an emotional attachment to the result.

Said more plainly:

- You often don’t know what you don’t know, so you can’t see your own blind spots. This is why a second set of eyes is crucial, especially when making important decisions. As Ben Simerly, Financial Advisor and Founder of Lakehouse Family Wealth, says, “Anyone can save some money and pick a fund. Whether or not an account is being managed to a far better outcome is a matter of time, learning, expertise, and knowing what you don’t know.”

- When the results affect your future well-being and that of your loved ones, it’s hard to stay objective and unemotional. That makes it hard to stay the course during tough times.

This is why even experts don’t go it alone, often hiring other experts to help them with their own finances.

Simerly speaks to this, “As the maxim goes, ‘For he who will be his own Counsellour, shall be sure to have a Fool for his Client.’ This is true for lawyers, as it’s often understood, but is more broadly true when seen as giving oneself counsel in general. In reality, even professionals are blind to a wide array of areas, including their own biases, failures, and limits of their genuine expertise. The best doctors have their own doctors. The best lawyers have their own lawyers. And the best advisors have their own advisors.

“Even the best Olympic runners, possibly the most ‘solo’ sport ever, never try to be their own running coach, too. Even I, as a pro, still learn new things every day. So, how is an amateur supposed to keep up with that learning curve? Beyond that, how many DIYers have been on hundreds of calls with 401(k) companies and/or read hundreds of investment prospectuses that include advisor-only details without being an advisor? What’s given to the general public is different than what’s offered behind the licensure wall.”

Even ignoring the above (which you shouldn’t), there’s an even bigger difference.

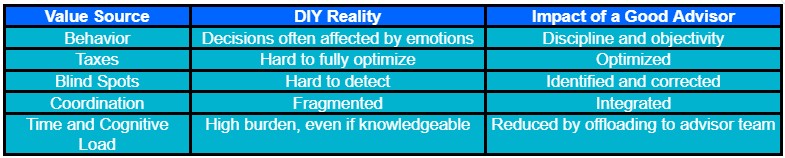

As a DIYer, you can keep researching, learning, and implementing what you learn. However, you’re working with a sample of one – your own situation. And any statistician will tell you that a small sample, especially a sample of one, makes for poor predictive value.

A good advisor, however, brings to the table:

- Experience and learning from multiple client situations.

- Coordination across taxes, investments, retirement planning, and estate planning, using input from teams of specialists and professional-grade software tools that you, as a DIYer, can’t easily match, no matter how smart or knowledgeable you are.

Good Enough vs. Optimal: What Financial Advice Can Actually Do for You

If you’ve reached a seven-figure net worth, you’ve already proven you can do well on your own.

You’ve met, and in a very real sense, exceeded “the standard.”

You’re unlikely to make a catastrophic mistake.

However, you probably do make lots of less-than-optimal decisions (or fail to make optimal ones). As a result, you’re probably:

- Paying somewhat higher taxes than the minimum you must legally pay.

- Making retirement income withdrawals from different account types in a somewhat less-than-optimal order.

- Allocating your investments in a way that will likely result in a somewhat lower long-term, risk-adjusted return, and making some fear- and/or greed-driven decisions.

None of these has a large enough impact to be immediately noticeable, and some years it may not even show up much, if at all.

However, combined and running over years and decades, they will likely have a material impact on your financial and emotional results.

The challenge is that you won’t see it happening while it’s happening.

This is why assessing the value of hiring a good financial advisor vs. DIY is so hard. The short-term impacts don’t jump right out at you. The massive impact only shows up after years, when you’ve already left a great deal of value on the table without noticing.

That’s why the core question isn’t if you can do this yourself.

You can. You’ve proven that already.

The core question is whether hiring a good advisor would let you do even better, with less stress and a smaller time commitment (Table 2).

That last entry in Table 2 is especially underappreciated by most DIYers.

You don’t have infinite time, so the time you spend managing your family’s finances comes at the expense of time you have available for other priorities, such as spending time with your family, on your wellness, and on your career.

Will you get a better financial, physical, and emotional return on time invested in managing your finances, or delegating that to an advisor and spending the freed-up time with your spouse and family, staying fit and healthy, and developing your career?

So, how much time are you willing to dedicate to your finances at the expense of those other priorities?

Plus, as an individual, you can’t compete with the time spent by teams of professionals who each spend dozens of hours each week working on multiple clients’ financial lives and learning from that and from continuing education training.

Having said all that, Simerly cautions that not all those who list themselves as “financial advisors” are experts in managing clients’ overall finances. “So many ‘financial advisors’ are forced to list themselves as ‘financial service professionals,’ but are actually insurance agents by profession. They don’t have years of experience managing wealth and investments, tax planning expertise, or working with a team that is 30 years their senior. As a result, they deliver advice that is as simplistic and scripted as the firm behind them can possibly make it. At that level of service, it’s no wonder hiring an advisor is questioned. The outcome may not be much different than doing it yourself.”

When Hiring a Financial Advisor Is Worth It

Here are things that are typically true for those who’d get the most benefit from hiring an advisor.

- Your financial life is becoming more complicated.

- You’re making decisions with long-term consequences (retirement timing, Social Security claiming timing, withdrawal strategy, tax strategy, estate planning, etc.).

- You’re looking for optimal results rather than “good enough.”

- You find yourself second-guessing important decisions.

- You’d rather focus your time on other priorities, such as family, wellness, and career.

When Managing Your Own Finances Is the Right Call

Here are things typically true for those who can likely stay DIYers without losing too much.

- Your financial situation is relatively straightforward.

- You follow a disciplined, low-cost investment strategy and can stick with it through market crashes.

- You’re comfortable making and sticking to long-term decisions and don’t keep second-guessing yourself and stressing over things.

- You’re willing and able to invest enough time to stay informed.

- You’re fine with a “good enough” outcome.

That last point is especially important because if that describes how you feel, DIY is most likely good enough for you, and paying for advice isn’t crucial.

The Real Cost of Not Hiring a Financial Advisor

By contrasting these two lists, you can see that the core question isn’t whether or not you can stick with DIY.

It’s the tradeoff between the things you’re trying to optimize for. If you’re looking for a combination of the following, a good financial advisor can be of great value.

- Optimal financial outcome.

- Reduced time and emotional and cognitive load.

- Greatest simplicity and acceptable cost.

The real tradeoff isn’t cost vs. no cost. It’s visible fees vs. less visible inefficiencies. And those inefficiencies compound over time.

How to Decide If You Need a Financial Advisor: A 3-Question Framework

If you’re still on the fence about hiring a financial advisor, use this simple approach. Ask yourself:

- Am I confident that my decisions are good enough for my goals, even during market crashes, and comfortable taking responsibility for the outcome?

- Would my outcome benefit from a review by a second, expert, objective set of eyes?

- Can I (and do I want to) spend the necessary time on educating myself and otherwise managing our finances, or would I rather delegate it so that I can focus on my other life priorities (family, wellness, career, etc.)?

Your answer to these three questions will tell you more than any theoretical headline number or example outcome graph ever could.

So far, we’ve looked at what research says. Now let’s look at what this actually looks like in real life.

Common Financial Mistakes Advisors Help Clients Avoid

I asked several professional financial advisors to share the biggest mistakes they’ve seen clients make, or helped clients avoid. Here’s what they shared.

Kevin Newbert, Financial Advisor of Ausperity Private Wealth, shares five such mistakes:

- “Selling equity too late or too concentrated: executives who held too long because they believed in the company and watched a $3M position erode to $800k. We build systematic diversification tied to tax efficiency, not emotion.

- “Entering a business sale without pre-sale planning: one of the most expensive mistakes I see. Qualified Small Business Stock (QSBS), 83(b) elections, charitable structures, installment arrangements, trust planning… these only work before the deal closes. A client who came to us after the Letter of Intent (LOI) had already eliminated most of their options.

- “Underestimating the tax hit on a liquidity event: a business owner expected to net $6M on an $8M sale. Proper pre-close structuring could have saved over $700K. The plan wasn’t in place. Most of it was avoidable.

- “Spending drift after a liquidity event: clients moving from high W2 or K-1 income to living off a lump sum often overspend during the first few years. We build a capital sufficiency model early so there’s a clear, defensible number rather than a guess.

- “Leaving rollover equity unanalyzed: Private-Equity-backed founders often accept rollover terms without stress-testing the concentration risk or understanding how it fits the broader plan. We model it before they sign.”

The takeaway here is that many of the most expensive mistakes happen before major financial events, when planning opportunities still exist.

Cole Williams, CFP®, CIMA®, BFA™, Founder of Vessel Financial Planning, shares two somewhat counterintuitive instances:

- “A common mistake I help clients avoid isn’t reckless spending, but the opposite. Many of the people I work with save well and started early, but they’re overdoing it in retirement accounts while putting on hold real goals such as family vacations, a home purchase, a car, and the kids’ education.”

- “One client came to me focused on the numbers. But early in our work together, she and her husband each completed a values exercise independently. Meaningful work, community, and diversity showed up in her top five. Her then-current job didn’t align with any of those, and she suspected it. She left. From a planning standpoint, I recommended temporarily reducing her husband’s 401(k) contributions to improve their cash flow and redirect savings into non-qualified accounts. That gave her a full year of runway to be selective. She passed on roles that offered competitive salaries but not the influence or impact she was looking for. When she landed the right job, she described it as beyond organizational leadership. It made a meaningful difference, and she was excited to wake up in the morning. You can’t show that in a portfolio report, but it’s what the planning work is there to do.”

Here, the takeaway is that a good advisor can help clients achieve better life outcomes that they value highly.

Dr. Steven Crane, Founder of Financial Legacy Builders, says:

- “Some of the biggest mistakes I’ve helped people avoid are actually pretty simple. Cashing out retirement accounts too early, taking on unnecessary debt, or making major financial decisions without understanding the long-term consequences. I’ve seen people unknowingly cost themselves six figures over time just from a few poorly timed moves. In those cases, the value of advice isn’t theoretical; it’s immediate.”

Takeaway: When you’re wealthy, it’s easy to make mistakes that can cost six-figure sums. A good advisor helps you recognize the pitfalls and avoid them.

Uziel Gomez, CFP®, founder of Primeros Financial, shares:

- “Clients have come to me with their emergency fund sitting in a savings account that wasn’t earning any interest. That money could have been working for them in a high-yield savings account or a CD.

- “I also work with many recent graduates whose income has recently increased. With that shift, some were under-withholding without realizing it, which could lead to an unexpected tax bill when they file their taxes.”

The takeaway here is that many people can make mistakes that are simple and easy to fix, but only if they’re aware of them.

Simerly says:

- “I’ve never worked a case where someone handling their finances for themselves hadn’t missed significant savings, increased returns, or pitfalls. Not once. And that includes my time as a newbie when I knew less than the proverbial doorknob. A second set of eyes can be worth the world.”

What Financial Advisors Say Is the Greatest Value They Provide

Next, I asked the advisors what they see as the greatest value they bring, and who would not benefit from it.

Newbert says, “My practice is built around one idea: income alone is not a financial plan. The clients I work with, from private-equity-backed founders navigating a liquidity event, to business owners approaching an exit, to equity-compensated executives in tech, healthcare, and consumer packaged goods, have built real wealth through hard work. But complexity scales with success, and most of them make high-stakes financial decisions without a coordinated strategy.

“What I bring is integration. Tax planning, equity comp strategy, investment architecture, and long-term cash flow modeling, working together, not in silos. I act as a personal CFO, helping clients answer the two questions that matter most at this level: ‘what can I actually spend?’ and ‘how do I make this last?’

“This provides the most benefit for clients who built their wealth through ownership, equity, or entrepreneurship, and are ready to stop winging it. Usually, they have $250K+ in income, with real complexity on the horizon: an equity award, a business exit, a liquidity event, or concentrated risk they haven’t addressed. They’re engaged, they care about family and legacy, and they understand that every dollar of planning at this level has measurable ROI. For the right client, the return on advice is often 10–50× the fee.

“On the other hand, the value isn’t compelling if you have a simple balance sheet, stable W-2 income, and no major financial decisions in sight.”

Williams offers, “The value I bring clients starts with something most financial conversations skip: what actually matters to them. Clients tell me they feel heard for the first time when talking about money. That often translates into allowing them to spend on experiences and comforts that align with their values right now, not just someday.

“Clients get the most out of working with me when they’re honest about what they want, including with each other. Many work in medicine or hospitality, where thinking about themselves can feel uncomfortable. But when they’re willing to look at that honestly, the results are real: mortgages paid off ahead of schedule, vacation homes that stop feeling like pipe dreams, retirements entered into confidently, and kids graduating without crippling debt. These outcomes make for more meaningful conversations than anything on a performance report.

“I’m also honest with clients who aren’t ready to make changes. Working with me won’t have the same return on investment for them, and I tell them that directly.”

Dan O’Rourke, Director of Multifamily Office Solutions, Strathmore Capital Advisors, says, “For wealthy investors, good advice is often less about generating more return and more about preventing expensive, avoidable mistakes. Many self-directed investors do a great job building wealth, but the transition from accumulation to turning assets into reliable, after-tax income is where advice often becomes most valuable. Things like taxes, withdrawal strategy, asset location, estate planning, and behavior during volatile markets can matter more than picking the next great investment.”

Crane agrees, “The biggest value I bring isn’t picking better investments. It’s helping people make better decisions. Most financial damage doesn’t come from markets; it comes from behavior. I’ve had clients who were ready to pull out of the market during downturns, make emotional decisions with large sums of money, or completely mismanage taxes. Stopping one bad decision can be worth far more than any fee they’ll ever pay.

“The people who get the most value from an advisor are the ones who want clarity and accountability. They don’t need someone to impress them; they need someone to help them stay on track and make consistently smart decisions.

“The people who get the least value are usually those who are already disciplined, keep things simple, and don’t overreact. They can do just fine on their own. Where I think the industry gets it wrong is how fees are structured. A portfolio doesn’t suddenly become five times more complex just because it’s five times larger. At some point, people should be asking whether they’re paying for real advice or just paying more because they have more.”

Jakub Kubrak, CEO and Founder of Kubrak Wealth Advisors, has a slightly different take on fees. He says, “Fees are only an issue in the absence of value, and during volatility is where advisors bring the most value. A good advisor will bring good market interpretation and discipline to help clients reach their goals. Most investors fail at reaching their goals because they aren’t good at staying disciplined or interpreting markets.”

Gomez says, “Having someone clients can turn to as a sounding board to talk through opportunities and potential risks can make a big difference. It also helps to have someone who can provide accountability, explain how the financial system works, and build their confidence along the way. With step-by-step guidance, the process can feel clearer, more manageable, and empowering.

“The clients I’ve seen make progress are usually the ones who are open to change and stay engaged in the process. I can walk through what may be in their best interest, but whether things get implemented often comes down to where they are in their readiness. I’ve worked with people who are dealing with debt and patterns of overspending, and many are aware that their current approach may not move things forward. At the same time, making the tradeoffs needed to shift those habits can feel difficult. That tension tends to be part of the process, and movement often starts once they feel more ready to take those steps.”

Key Findings: Is a Financial Advisor Worth It?

Across both research and real-world examples, a clear pattern emerges:

- The biggest value of advice often comes from making the right decisions, not picking the best investments.

- Major financial events can give rise to costly mistakes, especially for the wealthy.

- Small inefficiencies can compound into high, long-term costs.

- And much of this is hard to detect without an outside perspective, and most of the difference is hard to see while it’s happening.

Which brings us back to the key question: Would you do better with help?

Bottom Line: Is Hiring a Financial Advisor Worth the Cost?

So, are financial advisors truly worth hiring?

I can’t give you a definitive answer that’s true for you.

It depends, but not (just) on whether or not you can invest for yourself. Because if you’re at a 7-figure net worth, you probably can.

And many do, and it works out well enough for them.

Most investors don’t fail because they lack knowledge. They fall short because they miss small opportunities to optimize over long periods of time.

What it really depends on is whether you think you’d do better with professional help.

- Have a better risk-adjusted return.

- Make better decisions and lose less sleep over them.

- Avoid mistakes that will compound to your detriment over time.

- Spend more time on other priorities, such as family, wellness, and career.

- Feel more confident and less anxious, especially during market turmoil.

For some, the answer will still be no, and that’s ok.

If your finances are simple, you’re disciplined and confident, and you’re ok with a “good enough” outcome, DIY can be your best bet.

But for others, and even for those DIYers at a later date, the answer may be that the value of a good advisor, in terms of finances, portfolio, emotion, and time, would be more than worth the cost.

Especially if you want an optimal, rather than “good enough,” outcome.

In my case, I didn’t hire an advisor because I failed, or because I couldn’t stay the DIY course.

I hired one because I wanted to make sure there wasn’t any “gotcha” that I didn’t know that I didn’t know. I wanted a professional, objective, second opinion.

Finally, I wanted to see if I could go from “good enough” to “optimal.”

Because ultimately, the question isn’t just ‘Is it worth the fee?’

It’s also “What’s the potential cost of missing something without knowing it?”

That last cost can often turn out to be higher than any of us expect.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor