A dynamic asset allocation investment strategy employed by financial advisors attempts to reduce risks by adjusting portfolio holdings based on timely factors.

When the stock market declines by 1%, 5%, or 20%, should you be concerned if your investment portfolio earmarked for your retirement falls by an equal amount?

The answer will depend upon your investment objectives and tolerance for risk. Unfortunately, for many people who thought their portfolios were diversified and protected from suffering declines just as severe as major stock market pullbacks, the 2008 Financial Crisis and the 2020 COVID Crash proved otherwise.

While no investment strategy with exposure to asset classes like stocks and bonds is immune to losses when prices fall, a dynamic asset allocation approach attempts to reduce the severity of declines in investment portfolios when markets pull back while still achieving the long-term performance returns needed to meet investment objectives.

Suffice it to say that constructing and monitoring dynamic asset allocation portfolios requires considerable education, confidence, and fortitude. If you’re interested in the potential benefits of investing with a dynamic asset allocation approach, you may want to hire a financial advisor who specializes in this area.

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in building and managing dynamic asset allocation portfolios for their clients.

Fortunately, many financial advisors offer virtual services so you can meet online no matter where you (or they) live. This means you can choose to hire a specialist financial advisor who lives hundreds of miles away if you decide their knowledge and experience managing portfolios using a dynamic asset allocation approach is a better fit to help with your unique financial planning needs.

Financial Advisors Who Specialize in Dynamic Asset Allocation

💡 In the Q&A below, you’ll gain insights from financial advisors who specialize in building portfolios using dynamic asset allocation to help their clients achieve their investment goals with the potential for reduced losses when markets decline.

🙋♀️ Do you have questions not answered below? Use the form on this page to submit your questions, and we’ll update this article with answers from the financial professionals and educators in the Wealthtender community. You can also contact the financial advisors featured in this article directly to set up an introductory call or ask your questions by email.

Find a Financial Advisor Who Specializes in Dynamic Asset Allocation

📍 Click on a pin in the map view below for a preview of financial advisors who specialize in dynamic asset allocation.

📍Double-click or pinch pins to view more.

📊 Get to Know Financial Advisors Who Specialize in Dynamic Asset Allocation

This page is organized into sections to help you quickly find the information you need and get answers to your questions:

- Q&A with Financial Advisors Specializing in Dynamic Asset Allocation

- Get Answers to Your Questions About Dynamic Asset Allocation

- Browse Related Articles

Q&A: Financial Advisors Specializing in Dynamic Asset Allocation

Get to Know:

↗️ Todd Stankiewicz (Harrison, New York) | ↗️ Zack Swad (Santa Rosa, California)

Answers to Investing Questions with Todd Stankiewicz, CFP®, ChFC®, CMT®, ABFP®, EA

We asked Harrison, New York-based financial advisor Todd Stankiewicz who specializes in managing dynamic asset allocation portfolios for his clients, to help us learn more about the potential benefits of this approach to portfolio construction.

Q: How does your approach to dynamic asset allocation differ from a traditional buy-and-hold strategy?

Todd: Buy-and-hold sounds disciplined until you are sitting across from a client who just watched half their portfolio disappear. I have been through it. In 2008, the S&P 500 dropped roughly 57% from peak to trough. In early 2020, markets fell over 30% in a matter of weeks. In 2022, both stocks and bonds declined together, leaving traditional “balanced” portfolios with nowhere to hide. That was not merely a drawdown; it was a correlation breakdown. The foundational assumption behind the classic 60/40 portfolio, that bonds provide ballast when stocks fall, failed for the first time in decades. Investors who believed they were balanced had no refuge, facing a fundamentally different kind of risk than a pure equity selloff.

The emotional and financial damage from those drawdowns is real, and for many people it takes years to recover, if they recover at all.

My approach is built around responding to what the market is actually doing, not hoping it will bounce back on schedule. As a Chartered Market Technician, I use price trends, momentum signals, and technical indicators as an early warning system. When the weight of the evidence shifts, we shift. The goal is not to predict the future or time every move perfectly. It is to recognize deteriorating conditions early enough to reduce exposure before a routine pullback turns into a devastating loss. A static portfolio forces you to sit and absorb the full impact. A dynamic approach gives you the ability to act.

Q: Who is the ideal client for a dynamic asset allocation strategy?

Todd: The clients who benefit most from this approach are people who do not have the luxury of waiting it out. At the top of that list is the business owner. Their company is often their largest asset, and it is completely illiquid. The investment portfolio sitting alongside that business is their financial lifeline. If markets drop 40% and they need to make payroll, fund operations, or protect their family’s lifestyle, they cannot afford to wait three to five years for a recovery. Their liquid wealth has to stay intact and accessible.

I also work with pre-retirees in that critical window between 50 and 70 who have spent decades building wealth and are approaching the finish line. A deep drawdown at that stage can delay retirement by years. And for clients already in retirement who are taking regular distributions, the math gets even more unforgiving. Selling into a declining market locks in losses permanently.

That is sequence-of-returns risk, and it is the single biggest threat to a retiree’s long-term financial security.

The threat is not limited to a stock market crash. As 2022 showed, an environment where supposedly safe bond allocations fail at exactly the wrong time can be just as damaging. Dynamic allocation is built to potentially detect not only drawdowns, but also shifts in correlation, when the old defensive playbook stops working. The common thread across all of these clients is straightforward: they need their portfolio to work for them right now, not just eventually.

Q: Does dynamic asset allocation cost more, and how do you think about the value it provides?

Todd: I think the cost question gets framed backwards most of the time. People fixate on the advisory fee, but the real cost in investing is the loss you cannot recover from. If your portfolio drops 50%, you need a 100% gain just to get back to even. That is not a typo. A 100% gain. Depending on where we are in the market cycle, that recovery can take years. After the Dot Com Bubble Burst it took over 10 years for the S&P 500 Index and to reach previous highs. For someone who needs that capital for their business, their retirement, or their family, those years matter enormously.

At SYKON Capital, we operate on a fee-only model. We do not earn commissions or receive compensation for product sales. Standard regulatory trading costs, such as SEC fees, may apply as they do with any brokerage account, but there are no advisor incentives tied to how often we trade or what we recommend. The fee is transparent, and it is aligned with one outcome: growing and protecting your wealth.

The value of dynamic allocation is not just the potential to sidestep the worst of a downturn. It is also the confidence it gives clients to stay invested and engaged with their plan instead of panic-selling at the bottom, which is where the most permanent damage happens. In our experience, that combination of downside awareness and emotional stability is worth far more than the fee.

Q: What role does liquidity play in how you construct dynamic portfolios for your clients?

Todd: At SYKON Capital, liquidity is king. It is the foundation of everything we build. We seek to hold positions in instruments that have traditionally been liquid and trade on public exchanges: stocks, ETFs, and funds that can be bought or sold on any trading day under normal market conditions. We do not generally use alternatives, private placements, or any vehicle with a lock-up period. The reason is simple: if you cannot move, you cannot adapt. And the entire point of dynamic allocation is the ability to adapt when conditions change.

This matters especially for business owners. Their company is already illiquid. It cannot be sold overnight if they need capital. Their investment portfolio should not add another layer of illiquidity on top of that. When a business owner needs to pull funds for an unexpected expense or an opportunity, the portfolio should be ready. The same applies to retirees taking income distributions. If part of your portfolio is locked up in a fund with a multi-year redemption schedule, you lose the flexibility that makes dynamic management effective. We aim to keep our clients in a position where they can act quickly, whether the goal is to reduce risk during a downturn or to access capital when life demands it.

Q: Does dynamic asset allocation mean you are always playing defense?

Todd: That is probably the biggest misconception about this approach, and it is worth clearing up. Dynamic asset allocation is not a strategy built around hiding in cash and waiting for the storm to pass. It is built around following the evidence. And when the evidence says markets are trending higher, the goal is to be fully invested and participating in that upside.

Think about the bull runs following 2009, 2020, and the AI-driven surge of 2023 and 2024. Investors who sat on the sidelines waiting for the next crash missed some of the most powerful rallies in market history. One of the biggest risks in investing is not just being down in a bear market. It is being out of the market during a bull market.

Dynamic allocation, done well, keeps you invested when conditions support it and reduces exposure when they do not.

As a Chartered Market Technician, I use technical signals to read market momentum and trend strength, not just deterioration. When price action and breadth are confirming a healthy uptrend, that is a signal to stay engaged, not to retreat. The daily noise, the recession headlines, the geopolitical fears, the predictions about where the market is headed next week, none of that drives portfolio decisions. The data does. That discipline is what allows clients to tune out the noise and stay invested in strong markets with conviction, rather than second-guessing every move higher.

Dynamic allocation is not about avoiding markets. It is about trying to be in the right position for the environment in front of you.

Get to Know Todd Stankiewicz, Financial Advisor and Dynamic Asset Allocation Specialist:

View Todd’s profile page on Wealthtender or visit his website to learn more.

Answers to Investing Questions with Zack Swad, CFP®, CWS®, BFA™, AWMA®, AAMS®

We asked Santa Rosa, California-based financial advisor Zack Swad who specializes in managing dynamic asset allocation portfolios for his clients, to help us learn more about the potential benefits of this approach to portfolio construction.

Q: When meeting with new clients, how do you describe what dynamic asset allocation is?

Zack: A dynamic asset allocation is an alternative to a strategic allocation, which is typically based on “Modern Portfolio Theory” (MPT). Unlike a strategic allocation, which has a mostly-fixed percentage in each asset class (stocks, bonds, etc.), a dynamic allocation considers certain factors to determine which investments make the most sense at a given time.

Pretend you (and your investment portfolio) are in an airplane, and you have a pilot (the portfolio manager) flying the plane. The pilot can see through the windshield, and he also has an indicator dashboard. The indicator dashboard begins to blink and sends a signal to the pilot, informing him that if he keeps flying in the same direction and at the same speed, he will run into a storm in twenty minutes. What does the pilot do? Of course, he will try to avoid the storm. He will change course, or he may need to slow down or lower the plane.

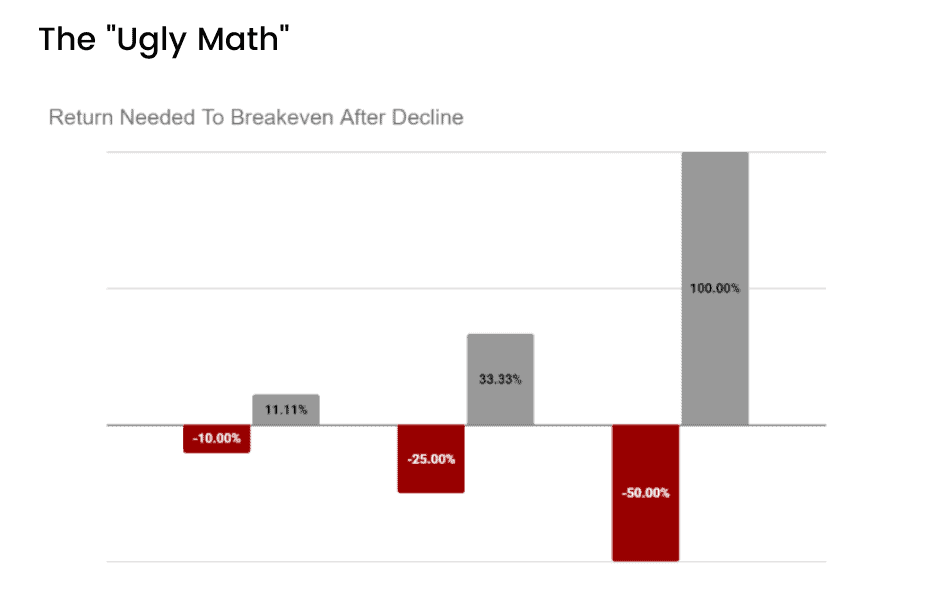

A dynamic asset allocation works similarly. It attempts to avoid catastrophic losses by actively managing the risk in a portfolio. At the same time, because a dynamic allocation typically does a better job of avoiding large losses, it doesn’t need to return as much when the markets are up. As you can see in the “Ugly Math” chart below, the less a portfolio declines, the less return it needs to get back to even and start making new profits.

For example, if you have $1,000,000 and lost 10%, you would have $900,000. To get back to even, you would need to make $100,000 or an 11% return. On the other hand, if you have $1,000,000 and experience a 50% loss (similar to what was seen for “buy-and-hold” stock investors during the 2008 financial crisis), you would then have $500,000. To get back to even, you would need to make $500,000 or double your investment (i.e., 100% return), which can take many years and is tough to bear psychologically.

Different managers use different factors and indicators to determine how to make allocation changes, so it’s important to learn more about their specific processes. You can read more about our process in the “What is an adaptive asset allocation” part of our FAQs section on our website. I’m also happy to provide research papers that I’ve used to inform our investment philosophy and process. Simply email info@swadwealth.com for more information.

Q: How did you first learn about dynamic asset allocation, and what led you to specialize in managing dynamic asset allocation portfolios for your clients?

Zack: I first learned about dynamic asset allocation while I worked as an advisor at Charles Schwab. Charles Schwab had a strategy called “Windhaven” that utilized this approach. Also, one of their partner RIA firms that I worked with had been successful for decades by using an active risk management approach. This inspired me to do more research on the topic, so I began reading countless books and research papers. I found that there were certain factors and indicators that have worked consistently throughout history, providing superior returns with less risk.

Furthermore, as someone who specializes in retirement planning, many of my clients cannot afford a major loss in their portfolio, which could significantly delay their retirement or force them back to work if they are already retired. I believe a dynamic allocation approach does a better job of mitigating that risk for them compared to a strategic allocation.

Get to Know Zack Swad, Financial Advisor and Dynamic Asset Allocation Specialist:

View Zack’s profile page on Wealthtender or visit his website to learn more.

Q: Are there particular market environments where you feel dynamic asset allocation is especially valuable to investors?

Zack: I believe a dynamic allocation is best in any market environment; however, it is especially valuable when interest rates or inflation are rising. Traditional portfolios typically have a fixed percentage of their assets in bonds. Unfortunately, bond performance can be hampered by rising rates and inflation. A dynamic allocation allows an investor to move into areas that may be better suited for the current environment instead of holding all asset classes at all times.

Investors need to be careful when considering making a change to a dynamic allocation during bear markets. It’s important to talk to a financial advisor to see if it is “too late” to reduce the risk in your portfolio and determine if there are any tax considerations.

Q: How does the cost of a dynamic asset allocation portfolio compare with a strategic asset allocation?

Zack: Commissions can be higher with a dynamic asset allocation because there is the potential for more trading. Also, because a dynamic asset allocation requires more research and attention, some advisors may charge more for this investment approach. Lastly, because there is more trading or “turnover,” the strategy can incur more taxes if held in a taxable account. With that being said, based on research, I believe the tax drag of our strategies is outweighed by the risk management and return potential.

Q: How do you work with clients to determine whether their investments will be managed with a dynamic or strategic asset allocation?

Zack: When I first started in the industry over 11 years ago, I believed there was only one way to do things. However, after working with hundreds of real people, I found it wasn’t that simple. People are complex, and companies like Dalbar have proven over and over again that investing and savings behavior is the number one factor on an investor’s portfolio return.

Because of this, I educate and ask my clients questions to help determine their investment philosophy. Then, I will align their portfolio to that philosophy, which I believe will give them the best chance of success. The key to investing is sticking with a well-thought-out strategy, one that you will stick with in good times and bad times. Where most people go wrong is they want to change their strategy or allocation style at the wrong time.

Q: For people interested in learning more about dynamic or adaptive asset allocation, are there online resources you recommend people consider?

Zack: For those interested in learning more about dynamic, tactical, and adaptive asset allocation styles, I recommend checking out the extensive work, research, and white papers produced by Mebane Faber. Meb is the co-founder and Chief Investment Officer of Cambria Investment Management and the author of multiple books on investing.

I would also look into the work done by Gary Antonnaci and his book “Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk.” Gary has over 40 years of experience as an investment professional, received his MBA from Harvard, and his research on momentum investing was the first place winner in 2013 and the second place winner in 2012 of the Founders Award for Advances in Active Investment Management given annually by the National Association of Active Investment Managers (NAAIM).

Are you a financial advisor who specializes in dynamic asset allocation?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience. (Subject to availability and terms.)

✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender

✅ Or request more information by email:

Resources to Help You Choose a Financial Advisor

✅ Top Questions to Ask a Financial Advisor

✅ How Much Does a Financial Advisor Cost?

🙋♀️ Have Questions About Dynamic Asset Allocation?

About the Author

Brian Thorp

Founder and CEO, Wealthtender

Brian and his wife live in Texas, enjoying the diversity of Houston and the vibrancy of Austin.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.