Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

A few years before retiring, I realized something troubling.

Nearly all of my portfolio sat in tax-deferred accounts. That meant that once Required Minimum Distributions (RMDs) began, my taxable income, and thus my taxes, would spike, whether I needed the money or not.

I asked our accounting firm, which offered annual tax strategy meetings, whether Roth conversions made sense for us, and if so, how much and when.

Their answer was both surprising and disappointing. They said it was outside the scope of their expertise.

Really? Roth conversions, outside the scope of tax strategists?

It turned out to be a case of, “If you want it done right, do it yourself.”

So, I turned to the huge spreadsheet I developed to project our income, expenses, taxes, and net worth for the next several decades, and added two new pieces:

- Estimated annual taxes

- Adjustable annual Roth conversion amounts for the 10 years I had until RMDs hit

I’d have loved to tell you the results led to a clear and inescapable conclusion.

Unfortunately, that would be a lie.

The projected results were nuanced:

- In the years we’d run the conversions, our taxes would naturally increase, significantly reducing our projected net worth by the time we had to start RMDs.

- Then, gradually, our net worth would recover and climb back to breakeven in my mid-80s.

- To really benefit, we’d need to survive into our 90s or beyond.

- Even then, the difference would have amounted to just a couple of percentage points of our net worth at that point.

In short, I’d need to voluntarily write large tax checks in my 60s and 70s and then wait decades to benefit, with only a one-in-seven chance of reaching my 90s, a famously changeable tax code, and projections far less precise than 2%.

All of that made Roth conversions feel like an expensive bet on a future I might not even see.

So, is the logical conclusion that there’s no point in converting, ever?

Not so fast.

Now that I’m retired, I added another tweak to my spreadsheet, optimizing the source of money we’d draw to cover expenses, how much we’d take each year from our relatively small taxable accounts vs. tax-deferred ones.

This showed me that there will be some years when our taxable income will be low enough that our marginal federal tax rate will be 12%.

When that happens, Roth conversions can make sense.

But how can you decide whether to do a Roth conversion, and if so, when and how much, without building a monster spreadsheet?

That’s what this article is all about.

The Immediate Tax Impact of Roth Conversions

When you convert money from a tax-deferred account to a Roth, the converted amount is treated as taxable income that year. That increases your current-year tax bill.

If the conversion pushes your income high enough, you may land in a higher marginal bracket and even have to pay Medicare surcharges (more on that later). That can be an expensive mistake.

But what if you convert from a post-tax traditional IRA?

If you hold both pre-tax and post-tax funds across your traditional IRAs, the IRS applies the pro-rata rule. Each dollar converted is treated as a proportional mix of both.

For example, if you have $495,000 in pre-tax IRA funds and $5,000 in post-tax contributions, then 99% of any conversion would be taxable income.

Another important note is that, if you’re younger than 59½, withdrawing converted funds less than five years post-conversion gives rise to a 10% penalty on top of the tax hit.

A possible workaround is to roll pre-tax IRA funds into a tax-deferred 401(k), if your plan allows it, reducing your pre-tax IRA balance to zero before converting the post-tax portion. That can work in certain situations, but it is beyond the scope of this article.

The key point here is simple. Roth conversions usually create an immediate tax cost, driving people to look for a “window” when that tax impact would be lowest.

Roth “Windows” – Helpful, But Not Definitive

Several scenarios are often mentioned as ideal times to convert.

- When you expect tax rates to increase in the future.

- After a market crash, when you can convert assets at temporarily depressed prices.

- During a temporary income dip, such as following a job loss, a no-bonus year, etc.

- When you’re still filing married filing jointly, before your widow(er) must file as single.

- If you plan to move from a high-tax state to a state with lower (or no) state income tax, converting after the move offers more value.

- In early retirement, before RMDs begin, when taxable income may be lower.

The first requires a functioning crystal ball. (If you have one, I have some questions about the future.)

The second and third can work, but require you to pay higher taxes when you can least afford it.

The fourth and fifth are valid reasons to consider converting when other factors align, but they don’t stop it from being a bad idea if the brackets don’t support it.

The sixth is the most persuasive. You retire. Your taxable income drops. Your marginal tax rate falls. Thus, it must be the best time to convert aggressively.

That logic sounds airtight.

And in some cases, it’s exactly right.

The problem is that in many other cases, it’s incomplete.

A lower tax rate today doesn’t automatically improve your long-term outcome. The benefit depends on how long you live, future tax brackets, RMD size, and taxable income flexibility.

That is why a generic “window” narrative can be misleading.

Roth conversions aren’t about following a generic rule. They’re about managing your marginal tax brackets over many years.

The danger isn’t because Roth conversions are necessarily bad. It’s in converting aggressively out of fear, rather than clarity.

For some retirees, conversions can make sense, and emphatically so.

For others, the benefit may be modest, delayed, and/or dependent on assumptions that may never materialize.

Which brings us back to the core problem: How do you decide, without building a massive projection model, whether converting makes sense for you?

Roth Conversion Strategy – a Three-Legged Stool

Detailed projections are the best way to assess if, when, and how much to convert.

This can be using a spreadsheet, if you have a good grasp of all the relevant factors, or you can ask your financial advisor to run the numbers, including Monte Carlo simulations of market returns.

If you don’t want to build such a spreadsheet and don’t have (and don’t want to hire) a financial advisor, three straightforward considerations offer a framework to identify if Roth conversions are likely to work out well.

- Tax Rate Difference

- Time Until RMDs

- Income Flexibility

If one leg is weak, the stool wobbles. If more legs are weak, let alone missing, it collapses.

Let’s dive a bit deeper into these legs.

Leg #1: Tax Rate Difference

For any specific year in which you’re considering a conversion, how does your current marginal tax rate compare to your likely rate once RMDs hit?

This includes state and local income tax and surcharges such as Medicare’s Income-Related Monthly Adjustment Amount (IRMAA). For 2026, the IRMAA Part B surcharge ranges from $974 to $5,844 annually, on top of the base premium. That’s a significant concern for those whose taxable income gets pushed too high.

Vanguard makes a compelling case that how you pay for conversion-related taxes may significantly impact the math: “… the tax payment source can shift the break-even point in meaningful ways. For example, when conversion taxes are paid from a taxable account — particularly one holding tax-inefficient assets or cash — the BETR [break-even tax rate] drops well below the investor’s current marginal tax rate. Likewise, basis in a traditional IRA or the potential for future backdoor Roth contributions can shift the math in favor of converting. This creates a wider ‘conversion zone,’ where even modestly lower future tax rates can still justify a Roth conversion.”

BETR takes into account the current marginal ordinary income tax rate, the basis of assets sold to fund tax payment for the conversion, investment time horizon, annual investment return, and dividend yields. Under Vanguard’s assumptions, someone in a 35% bracket who pays conversion taxes from idle cash could see the break-even tax rate drop to 14%!

The larger and more certain the spread between tax rates (or BETR and future rates), the stronger this leg of the stool.

If your current marginal federal rate is 12% and you expect RMDs to push you into the 24% bracket, or even the 22% bracket, that makes for a compelling conversion case.

If your current rate is 22% and RMDs aren’t likely to push you any higher than 24%, paying much more in taxes now to possibly save 2% in 10+ years is far less compelling.

This is what my own assessment was before I retired, and stays the same for most years now that I am retired.

But not for all years.

Clearly, none of us (not even those in Congress) can guess how the US tax code will change over the coming years or decades. What I do here is assume the rates will stay the same, with the brackets adjusting for inflation. This isn’t intended to be accurate, just a best guess for how an uncertain future will unfold in at least this one regard.

Leg #2: Time Until RMDs

How long do you have until RMDs hit?

RMDs now start at age 73, but if you don’t have to start before January 1, 2033, that will be pushed further out, to age 75.

Does that give you five years? Ten? Fifteen?

The longer your runway, the less certain the calculus.

- More time for the tax code to change.

- More time for investments to grow tax-deferred (or tax-free if converted).

- More time for your spending habits to change.

- More time during which you could die.

My spreadsheet projected a breakeven point in my mid-80s. To benefit meaningfully, I’d need to live into my 90s, which is less likely than not.

This does not make conversions useless. It means the payoff is distant and uncertain, while the cost is immediate and guaranteed.

You’d have to prepay taxes today for a benefit that may not arrive for 20-plus years, if ever. That’s a serious trade-off, not a casual decision.

The longer you need to wait for an eventual benefit, the more cautious you should be.

One caveat to that is that if you’re considering a Roth conversion as an estate management tool, that will, by definition, benefit your heirs no matter how long you live.

Leg #3: Income Flexibility (Source and/or Amount)

This is one that many people overlook.

How flexible is your taxable income?

This could be because you can choose how to cover expenses, from taxable (ordinary income rate or long-term capital gains rate), tax-free, or tax-deferred money. It can also be because a large fraction of your budget is discretionary, allowing you to reduce spending in years when the tax impact is greatest.

This lets you deliberately lower your taxable income some years to make a Roth conversion more beneficial, while pushing higher taxable income into other years.

This is what I’m planning to do, now that I’m retired.

In years when I sell a property held for more than a year, I’ll owe taxes on any appreciation and/or depreciation recapture at lower long-term capital gains tax rates. However, this won’t push me into a higher marginal tax bracket.

The proceeds from such a sale may allow me to cover expenses without needing to draw tax-deferred money that triggers ordinary income taxes. This will allow me to make a highly beneficial Roth conversion, paying no more than 12% federal income tax, far lower than the brackets I’ll be in once RMDs hit.

If you have little flexibility here, your case for conversion becomes that much shakier.

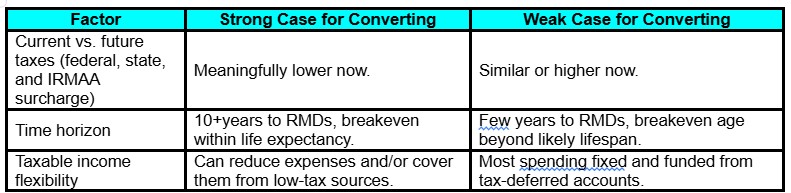

When the Conversion Stool Is Most Stable

This is when a Roth conversion is most beneficial to you:

- Your current marginal tax rate is meaningfully lower than it will be once RMDs start.

- You have a long runway to time conversions strategically and for the converted funds to grow tax-free in a Roth account.

- You can deliberately manage your budget and how you fund it.

When the Conversion Stool Is Most Wobbly

This is when a Roth conversion is least likely to benefit you:

- Your current tax rate isn’t meaningfully lower (or even higher) than what it will be when RMDs kick in.

- Your breakeven point is decades away.

- Future benefits depend on optimistic assumptions.

- You have little to no flexibility in controlling your taxable income through lowering spending and/or funding at least some of it from taxable, low-tax, or tax-free sources.

In such cases, you may still benefit, but the margin of safety is thin and the upside uncertain. The potentially small eventual benefit likely won’t justify the immediate cost.

If you prefer a quick diagnostic instead of a spreadsheet, here’s how the three legs work:

What the Pros Say

I asked financial advisors for their thoughts on Roth conversions. Some of what they say may not be surprising, but some goes beyond conventional wisdom.

Jeffrey J Smith, Founder and Managing Partner of OWL Private Wealth Advisors, says, “To quote Ed Slott, ‘Your IRA is an IOU to the IRS.’ It may make sense to rip the band-aid off and accelerate the conversions to keep the marginal tax rate and Medicare IRMAA increase to only a few years early on in retirement, preferably more than two years before turning 65. If you have non-qualified funds to pay the taxes due, this can significantly increase the overall results, not only for the IRA owner but ultimately their beneficiaries. Like the tax code itself, a decision to convert or not isn’t a black or white answer for most, but we all know the saying that the only certainties in life are death and taxes. With a Roth conversion, you can decide when to pay the taxes, at a tax rate you know now, versus not knowing where you will fall in future years. That second part is out of your control.”

Mike Hunsberger, Owner, Next Mission Financial Planning, agrees, “The biggest factor [affecting the benefit of a Roth conversion]is future tax rates. It’s hard to know what those will be.” He adds several more important things,“Another big impact is whether you’ll actually use the converted dollars or if they will be passed on to your heirs. If the latter, it’s important to consider theirlikely tax rates when they inherit. Finally, it’s always useful to understand what happens when the first member of the couple dies, and the remaining spouse reverts to single tax rates. The important thing to remember is not to over-convert. If you don’t have other projected income, keeping some tax-deferred money can help you fill up the lower tax brackets in retirement, possibly in a lower tax bracket than what you converted at.”

Stephen Mazer, Senior Wealth Advisor and Principal, Rational Wealth Solutions, points out how the decision is deeply dependent on your personal situation, “There are NO rules for who should or shouldn’t proceed with a Roth conversion, or when to do it. Solutions should be considered based on many factors. One of Thomas Sowell’s famous quotes, ‘There are no solutions. There are only trade-offs,’ applies here. Did you know you may not have to pay the taxes owed out of your own current accounts? Did you know there are ways to keep full market volatility/risk and other ways to negate much, if not all, of the market downside/risk during the conversion period? Talking with someone familiar with these strategies and who understands your goals will shine a light on what might be appropriate for your situation, bringing clarity to the process.”

The Bottom Line

At its core, a Roth conversion is a trade-off, paying guaranteed costs today for a likely benefit tomorrow that may be worth the cost and the wait.

Roth conversions are not about generic “windows” or rules.

They’re a bet that depends on three factors: (1) your tax-rate spread, (2) your time horizon until RMDs and your lifespan, and (3) your taxable income flexibility. When all three align, you’re most likely to gain a significant advantage from a conversion.

When one or more is weak, your benefit is less certain and likely smaller.

Conversions reduce your tax uncertainty, but at a cost you need to be willing to pay.

You don’t have to have an advisor (though a good one offers a lot of value).

You don’t need a monster spreadsheet.

You don’t need certainty about the future.

You just need a solid decision framework that clarifies your trade-offs.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor