Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

So, you’ve been diligent and maybe even a little frugal.

You’ve squirreled away money in IRAs, a 401k or two, perhaps a 403b… Hopefully, enough to enjoy a well-deserved, comfortable retirement.

To reward you, Uncle Sam (and possibly your state taxing agency) gave you tax deductions to make it easier to invest for the future.

However, those were tax deferrals, not credits, and at some point, it’ll be time to pay the piper (or at least the IRS).

Enter the dreaded Required Minimum Distributions (RMDs)…

What Are RMDs?

As the name implies, RMDs are the minimum amounts you’re required to draw (or distribute) from your deferred-tax retirement accounts. Accounts such as the non-Roth versions of:

- IRAs

- SEP IRAs

- SIMPLE IRAs

- 401(k) plans

- 403(b) plans

RMDs are designed to force you to gradually draw down your retirement accounts, so you have to pay the taxes you deferred for all those years.

When Are RMDs Due?

The nice thing is that you don’t have to take these as soon as you retire. You used to have to start taking them in the year in which you turned 72. Then, SECURE 2.0 was signed into law, and if you hadn’t started taking RMDs, you need to start:

- At age 73, if you were born between 1951 and 1959.

- At age 75, if you were born in 1960 or later.

In each case, you can put off your RMD until April 1 of the year after you reach the relevant age.

How High Are Your RMDs?

To calculate your RMD for the year, you need to total the value of all your affected retirement accounts as of December 31 of the year you turn the relevant age.

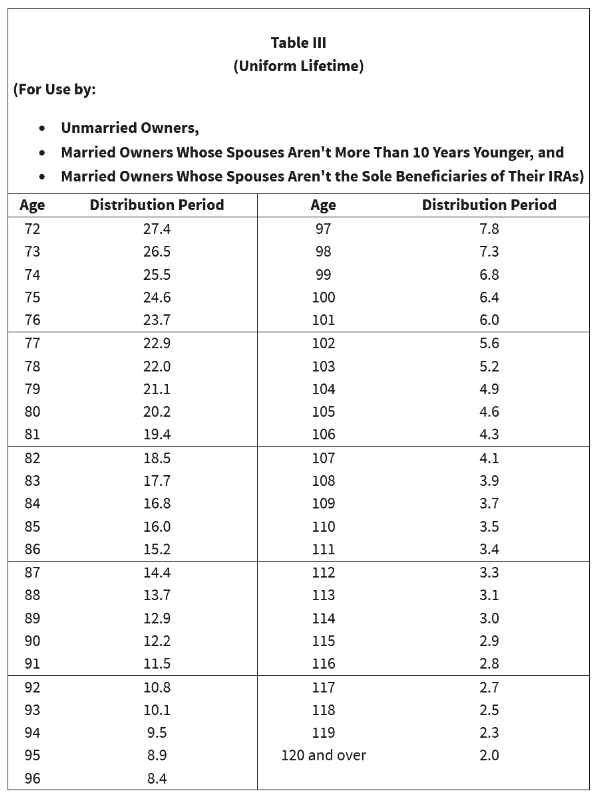

Then, you divide that amount by the applicable factor from the Uniform Lifetime table that applies to your situation. For people who are unmarried, or whose spouses aren’t more than 10 years younger, or whose spouses aren’t the sole beneficiary of the relevant accounts, that would be Table III below.

For example, if you have a total of $1 million in the relevant accounts and you have to start drawing RMDs at age 75, your first RMD would be $1,000,000/24.6 = $40,650.

If you reach age 90 and your relevant accounts’ total balance at that time is $750k, your RMD that year would be $750,000/12.2 = $61,475.

If you’re one of the fortunate few who reach age 100 and your relevant accounts still hold $600k, your RMD that year would be $600,000/6.4 = $93,750.

Can You Reduce Your RMDs?

Yes, you can, by carrying out Roth conversions.

You’ll still need to pay regular income tax on the converted amounts, but any further growth will be tax-free.

Another way works if your spouse is over 10 years younger than you. In this case, you can use Table II instead of the above Table III, and the RMD factors are higher so your RMDs are lower.

Can You Defer Your RMDs if You’re Still Working?

This is the one way you can defer taking RMDs.

If you’re still working past your RMD starting age and own less than 5 percent of your employer (not owning any stock in your employer counts as zero, and thus is ok), your retirement account that’s sponsored by that employer isn’t included in the RMD calculation.

If your employer allows rolling other retirement accounts into their retirement plan, and if you roll over any other non-Roth retirement account balance into your employer-sponsored retirement account before you start taking RMDs, you can avoid taking any RMDs until you’re no longer on that employer’s payroll.

Is There a Penalty for Not Taking RMDs?

Yes, there is.

It used to be the government would take half of any shortfall, so if your RMD was supposed to be $50k and you failed to take it, they’d confiscate $25k out of your accounts.

SECURE 2.0 reduced that forfeiture to 25 percent, so in the above example, they’d take $12.5k of your money. There is also a corrections time frame, and if you take your RMD within that window, the forfeiture drops to 10 percent, or $5k in our example.

And that’s in addition to the ordinary income tax due on the distribution.

Do You Pay Income Tax on the Full Amount of the RMD?

Not necessarily.

If you already paid taxes on some of the amounts in the relevant accounts (e.g., if not the full contribution you made was tax deductible when you made it), you owe income tax just on the untaxed fraction of the balance in the relevant accounts.

What Can I Do with RMD Money that I Don’t Need to Spend?

As you can see from the above table, each year the RMD fraction increases. If your account balances don’t fall faster than that increase, your RMD amount will increase over time.

Especially if you were diligent about saving for retirement, and even more especially if you invested astutely and your balances grew significantly, at some point your RMD will be (much) higher than what you need to cover your expenses.

Since you can’t put the excess back into a retirement account, what can you do with it?

Here are the 7 best ways to use it.

1. Spend It on Something from Your Bucket List

You set aside money all those years for when you retire. Now you’re retired, and the RMD is (much) higher than you need to cover expenses.

That makes it available for anything that will be especially enjoyable.

Like that cruise to Antarctica or Alaska that you always dreamed about but could never convince yourself to splurge on something like that.

2. Gift-tax-free Transfer to a Loved One

If you have loved ones for whom you intend to leave money, consider gifting them some of the money now, while you’re still alive.

When doing so, you can (for 2024) exclude up to $18,000 per giver per recipient without owing gift tax. Thus, if you’re married, the two of you can leave $36,000 per recipient. If the recipient is married, you can double again to $72,000 by gifting each of the younger couple half of that amount.

3. Make a Charitable Donation

Qualified charitable distributions (QCDs) let you use distributions to charitable causes that then count toward your RMD (up to $100k per year per donor, so up to $200k per year for a married couple filing jointly). QCDs need to be made directly from your IRA custodian to the qualified charity of your choice.

Since the charitable donations are tax deductible, you won’t owe income taxes on those amounts.

4. Reduce Taxes Using Net Unrealized Appreciation (NUA) of Your Employer’s Stock

If you have company stock in your 401(k), you could transfer it into a taxable brokerage account (see below) as an in-kind transfer (i.e., you transfer the shares themselves rather than selling and transferring the resulting cash).

Normally, when you distribute from a tax-deferred account, whether as cash or in-kind, you owe regular income tax on the current market value of the distribution (less any amounts that were already taxed).

For in-kind distribution of your employer stock, however, you only pay regular income tax on the amount you paid for the stock (your basis), leaving untaxed the NUA in the stock. Then, when you sell the stock from your taxable account (at least 12 months after you bought it), you pay the far more favorable long-term capital appreciation tax on the gain you realize.

Here’s an example. Say you paid $200,000 over time for shares in your employer that you placed in the company 401(k). As time went by, the shares appreciated and are now worth $1,200,000. If you sell the shares and transfer the $1,200,000 to your taxable accounts as cash, you’d owe regular income tax on the full amount. If you’re in the 37 percent tax bracket, that would be $444,000 owed.

Instead, say you distributed the stock as an in-kind transfer. You now owe the 37 percent just on your $200,000 basis, or $74,000. Then, even if you were to immediately sell the shares from your taxable account, you’d owe another 20 percent on the $1,000,000 that wasn’t taxed, or $200,000. Your total tax bill would thus be $274,000 instead of $444,000 — a savings of $170,000!

5. Pay for a Loved One’s College Expenses (and Even Their Retirement)

SECURE 2.0 added several interesting and useful features.

For example, you could fund a 529 college savings account using your excess RMD money (which might even give you some state income tax relief). Then, once the 529 account has been open for 15 years, you can roll over up to $35,000 per beneficiary (lifetime limit) into a Roth IRA for them.

Note that the beneficiary must have enough earned income in the year in which you want to roll money over into their Roth IRA and the amount rolled over cannot exceed the year’s Roth contribution limit.

6. Buy Life Insurance

If your RMD leaves excess money, you could use the after-tax excess to pay for a life insurance policy. The death benefit of such a policy can help your beneficiaries pay for taxes they may owe on your bequest (if any) and can also recover the money lost to the taxes you had to pay when taking the RMDs.

7. Transfer to Taxable Accounts

If your emergency fund is running low, you could use excess RMD money to refill those accounts.

If all else fails, you can always invest the excess RMD money in taxable investment accounts.

There, any further growth will be taxable, but if you hold the investments for more than 12 months, realized gains will be subject to the lower tax rates on long-term capital gains, currently between 0 percent and 20 percent (vs. the maximum regular income tax rate of 37 percent).

Since the money will now be in a taxable account, consider choosing tax-efficient assets.

In certain situations, you might prefer to make such distributions as in-kind transfers, even if the investments aren’t your employer’s company stock (see above). For example, if the investments are volatile and/or are down substantially and may be poised for recovery. In this situation, you don’t want to risk losing money between the sale and repurchase of the assets. Alternatively, the assets may be relatively illiquid (e.g., real estate, bullion, etc.), in which case an in-kind transfer avoids paying the out-and-in commissions and fees.

The Bottom Line

Having to take RMDs means you were savvy and fortunate enough to be able to set aside a substantial amount of money in tax-advantaged accounts. However, that doesn’t make it any more fun taking more money out than you need to cover expenses and paying regular income tax on the distribution amounts.

Omar Morillo, CFP®, Founder of Imperio Wealth Advisors, www.imperiowa.com, especially agrees with 3 of these 7 ways of making the best of this scenario, saying, “When our clients have unneeded RMDs, there are ways of using them that can provide personal fulfillment and financial advantages.

“Donating to charity is a popular choice that not only allows clients to support causes they’re passionate about but can also offer tax benefits. A QCD can directly transfer funds from an IRA to a charity, potentially reducing taxable income and fulfilling RMD requirements without increasing tax liability.

“Investing excess RMD money into taxable accounts is another smart move. This can help diversify investments and potentially generate additional income or growth outside of the more rigid structures of retirement accounts.

“Finally, fulfilling bucket-list goals is a rewarding use of excess RMDs. Retirement is an ideal time to pursue dreams and experiences you deferred during your working years. Using RMDs to pay for travel, a new hobby, or any other personal aspiration can significantly enhance your quality of life and provide a sense of accomplishment and joy in your retirement years.”

Find a Financial Advisor

Do you have questions about your financial future? Find a financial advisor who can help you enjoy life with less money stress by visiting the Wealthtender advisor directory.

Whether you’re looking for a specialist advisor or prefer to find a financial advisor near you, you deserve to work with a professional who understands your unique circumstances.

Have a question to ask a financial advisor? Submit your question and it may be answered by a Wealthtender community financial advisor in an upcoming article.

This article originally appeared on Wealthtender. To make Wealthtender free for our readers, we earn money from advertisers, including financial professionals and firms that pay to be featured. This creates a natural conflict of interest when we favor their promotion over others. Wealthtender is not a client of these financial services providers.

Disclaimer: This article is intended for informational purposes only and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor