Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Have you thought about retiring early?

Maybe in your 30s? 40s? 50s?

One couple, Billy and Akaisha Kaderli, did just that. They saved up $500k by the time they were 38 years old, in 1991, invested it, and called it a career.

Now, 30 years later, their portfolio is worth $1 million. Adjusting for inflation, that’s $514,201 in 1991 dollars. This means that after 30 years of living on about $30,000 a year funded by returns from their portfolio (plus income from part-time work blogging etc.), their inflation-adjusted portfolio value is about 2.8% higher than when they started (an annualized increase of 0.09%).

Not great, but not too shabby.

If you want to learn more about the Kaderlis’ journey, they answer the 20 questions they get asked most frequently here.

Let’s see what problems you have to overcome if you want to retire early, and what you can afford with $500k, $1 million, or $2 million in assets.

5 Problems with Early Retirement

The “holy grail” for adherents of FIRE, or Financial Independence Retire Early, is to amass as much money as possible, as quickly as possible. Although there are many FIRE “flavors,” for the most part you need to do two things.

First, live as frugally as possible so you can save and invest a very high percentage of your income. Second, plan to continue living a frugal lifestyle in retirement (e.g., the Kaderlis’ $30,000/year), which usually means moving someplace with a super-low cost of living and forgoing many things that most people aspire to or want in their lives (e.g., the Kaderlis went car-less many years ago, and in place of a large home they own a 1000-sqft “low maintenance, high amenity humble abode”)

This brings us to some problems with early retirement.

1. Length of Retirement

If you retire earlier, your nest egg has to last longer. According to the IRS, the life expectancy of a 38-year-old American is 45.6 years. By age 67, it drops to 19.4 years. This means that retiring at age 38, you must plan for an average of 26 years more in retirement than at age 67. If your nest egg lasts exactly as long as your life expectancy, you have a 50/50 chance of outliving your money, because by definition half the people outlast their life expectance. If your parents lived into their 90s like mine, you should plan for more years in retirement.

2. Fewer Options in Case of Market Declines

If you’re still working and a bear market decimates your nest egg, you can keep working a few more years to cover your expenses, letting your portfolio recover once the market comes back. If you just retired and your portfolio suffers a 30% or bigger “shave,” your already tight budget may no longer be achievable.

According to Investopedia, there were 11 bear markets between 1956 and 2021. As shown in the table below, the S&P 500 dropped between 20% (the smallest decline that qualifies as a bear) and 56%. These bear markets were as brief as a single month, or as long as 31 months.

| Bear Start Year | S&P 500 Decline (%) | Duration (Months) |

| 1956 | 22 | 15 |

| 1961 | 28 | 7 |

| 1966 | 22 | 8 |

| 1968 | 36 | 18 |

| 1973 | 48 | 21 |

| 1980 | 27 | 21 |

| 1987 | 34 | 3 |

| 1999 | 20 | 3 |

| 2000 | 49 | 31 |

| 2007 | 56 | 17 |

| 2020 | 34 | 7 |

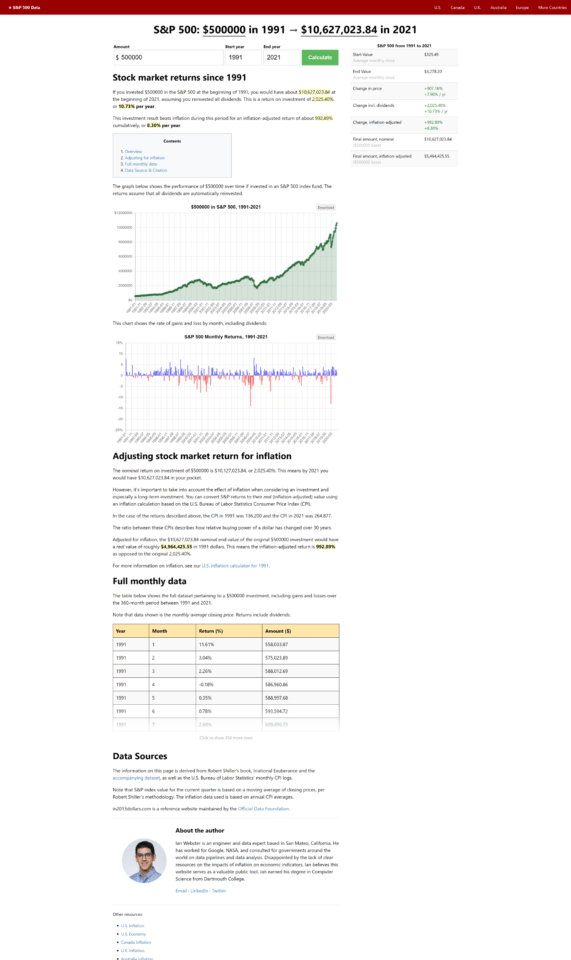

A nifty website called in2013dollars lets you see how the market performed over any stretch of time. The following screenshot shows how the market behaved from 1991 to 2021.

As you can see, the Kaderlis were very lucky in that the first bear market to hit after they retired was 8 years into their retirement, and with a 20% loss was barely enough to qualify as a bear at all.

At no point after their retirement did the S&P 500 fall below its 1991 level. Had they retired just before the 2020 bear, their $500k would have dropped to about $255k, and their plans would have crashed and burned with the market. This is a perfect illustration of the so-called “sequence of returns risk.”

3. No Social Security at Retirement, and Much Lower Eventual Benefits

Since the earliest you can claim (greatly reduced) social security benefits is at age 62, retiring in your 30s, 40s, or 50s doesn’t allow you to count on those benefits to reduce your retirement funding gap. According to CBPP, the average Social Security benefit in 2020 was about $18,170 a year. While this isn’t much, if you’re planning to live on $30,000, getting $18,170 reduces your nest egg requirement by over 60%!

Worse yet, if you retire early, your eventual benefit will be much lower. This because the Social Security Administration uses your 35 highest annual income numbers (from which you paid payroll taxes). If you started paying into the system at age 22 and retire at age 38, you’re giving up at least 54% of your eventual benefit. Since most people’s earnings increase through their 30s, 40s, and 50s, the drop in your benefit will be even greater.

4. No Medicare at Retirement

If you retire in your 60s or later, most of your health insurance needs will be covered by Medicare. Retire in your 50s or earlier and you need to buy private health insurance for years or decades, or like the Kaderlis did at least part of the time, go “naked,” taking the risk that a major illness or accident may wipe you out financially.

5. Financial Insecurity

If you plan to live on $30,000 a year, and something forces you to move back to the US (or other high-cost country), you’re almost certainly looking at a big problem. Either you cut your standard of living to the bone or worse, run out of money.

So, What Can You Afford on $500k, $1 Million, or $2 Million in Assets?

The common rule of thumb is the so-called “4% rule.” Research conducted in the 1990s looked at historical returns and concluded that a 60/40 portfolio would have survived the worst 30-year period if you withdrew 4% in your first year in retirement, and then adjusted the dollar amount each year to account for inflation.

Based on this “rule,” $500k, $1 million, and $2 million would allow a first-year draw of $20k, $40k, and $80k, respectively.

However, current projections show a much more muted expected return from both stocks and bonds in the coming decades. This suggests a safer draw might be 3.5%, implying first-year draws of $17.5k, $35k, or $70k, respectively.

The Impact of Early Retirement

Since early retirement means you’d need to provide for a years- or decades-longer retirement, even 3.5% may be too optimistic if you’re retiring in your 50s or earlier. In that situation, you’d be well advised to reduce your initial draw to 3% or less, implying a first-year draw of $15k, $30k, or $60k, respectively.

3 Things You Can Do to Improve Your Retirement Standard of Living

If we set aside the option of continuing to work and save for several more years or decades, what else can you do to be able to afford a more decent standard of living than a less-than-appealing $30k with a million dollars in assets?

First, you need to develop a budget that has more discretionary costs and less in fixed expenses. For example, if you have a $1750/month mortgage payment (or rent) to cover, that’s $21,000 in annual cost that you can’t do anything about. Even a $1000/month housing cost would use up 40% of your $30k/year draw. Add in a car loan payment, and paying for food and medicine may become impossible.

If you can do as the Kaderlis did and do without a car, and reduce your housing costs significantly, you have more wiggle room to cut your discretionary expenses if the market drops for a while, so you don’t have to eat too deeply into your principal. If most of your spending is discretionary, research shows you might be able to safely draw as much as 7% of your portfolio value in your first year of retirement. For the above portfolio sizes, that would be $35k, $70k, or as much as $140k, respectively!

Second, instead of seeing retirement as a time to sit on the couch and wait to die, see it as a time to pursue your life passions. Working part time on things you love will fill your time with productive activities that give meaning to your life. This will also reduce the time you need to fill up with leisure activities that may cost money. Finally, it’ll provide some income to reduce the drag on your portfolio, or to enable you to live (somewhat) more expansively than a $30k/year budget would allow.

Third, research where you might be able to move such that:

- Cost of living is much lower for the quality and standard of living you want

- High-quality, affordable healthcare is available

- Personal safety is acceptably high

- You’d enjoy the climate

- You can (learn to) speak the language

- Visas and work permits (if needed) are available (and visitor visas are available for family and friends who may want to visit)

- Fun, low-cost activities are plentiful

- Communication with family and friends you leave behind is easy

- Healthy food is affordable

The Bottom Line

Retiring on $500k was possible in the 1990s, as proven by the Kaderlis. Doing the same today would require $1 million, if not more, given the more muted market returns expected in the coming decades.

If you want to retire on even $1 million, you’ll likely be able to safely draw only $30k – $35k in your first year, adjusting for inflation each year from that dollar amount. This means you’d better be prepared to forgo most if not all luxuries, move to a low-cost country, and probably continue working part-time doing something you enjoy for which others would be willing to pay you.

If you structure your life such that almost all your expenses are discretionary, you’ll be able to increase your year-one draw very significantly, perhaps to as much as 7%. For a $1 million portfolio, that’s $70k. For $2 million in assets, it’s a comfortable $140k.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor