[Cryptocurrency’s downward spiral in the fourth quarter of 2025 reinforced a visceral understanding of the asset’s volatility and the difficulty of determining the rationale for the continued sell-off. Articles during this period were prevalent with head-scratching and grappling with the market dynamics behind the price collapse. All the while, retail and professional investors were being burned in crypto ETFs, which had reached over $150 billion in assets.

This crypto price downturn underlined the fact that we are all investing in an extreme state of uncertainty, and relying only on assumptions, extrapolations, and predictions in such an environment is a risk that needs to be actively managed. Suggestions for adding a price trend risk management system or overlay became a topic of discussion.

To explore this further, I reached out to Rocco Pellegrinelli, CEO and Founder of Trendrating – an advanced alpha discovery and trend analytics research platform that offers investment managers a risk and opportunity management overlay to any portfolio holdings, including crypto ETFs. He sent me a research flyer that illustrated how his AI-driven price trend model issued crypto ETF trend downgrades well before conventional research or traditional methodologies detected the shift. The research was first published on December 3, 2025, on FactSet and Bloomberg, which provided a strong validation of Trendrating’s capability to anticipate market shifts before they became apparent. This early warning mechanism is crucial in the crypto space, where volatility is high, and quick adjustments can make a significant difference in managing both risk and opportunity for investors. I asked him questions to better understand how his research platform was designed to validate and capture price trends on the growing number of crypto ETFs.]

Hortz: Can you explain your thinking behind building the Trendrating research platform?

Pellegrinelli: Our goal has always been to develop the investment research tools that professional investment managers need and deserve by offering broader market intelligence than what conventional data and tools provide. We fill this critical knowledge gap.

We firmly believe that professional managers’ investment strategies and models will profit from better information that is based on pragmatic fact-finding. This enables the discovery of factual insights that have a measurable impact on the quality of the investment decision process.

Our core belief is simple: understanding and respecting price trends is not optional – it is essential. Market research needs to reflect not only fundamentals but also sentiment, momentum, and patterns that often precede headline events.

Hortz: What does “respect for” and monitoring price trends provide investment managers?

Pellegrinelli: On the one hand, it provides an early warning system. It’s like being able to feel the slight vibration of a railroad track coming from a distant but fast-approaching train or being able to see beneath calm waters to discern the gathering undercurrents and rip tides that could potentially pull strong swimmers, or investors in our case, dangerously underwater.

Likewise, positive price trend indicators signal the building of favorable underlying momentum – reading the gathering trade activity as it is happening in real-time, from large institutional and other major players building positions.

This provides great support for managers in their buying and selling decisions.

Hortz: How is this applied to crypto ETFs?

Pellegrinelli: Instead of trying to figure out the big picture as to what is going on in the crypto industry or attempting to forecast Bitcoin’s price direction, the research platform focuses on reading the underlying trade activity of a crypto ETF to see what is actually happening on the ground, to determine what pressures are building that can affect the ETF price.

We remain cooly independent from the crypto story and prognostications about cryptocurrencies. We harbor no biases or desired outcomes on the underlying assets that we are monitoring. We focus on validating price trends as they are happening. This provides us with clarity and dedication to our singular efforts to provide a more targeted risk and opportunity management system for our professional investor clients.

Hortz: How is your Trendrating system different than other trend analysis tools?

Pellegrinelli: Unlike other trend rating systems, our advanced AI-driven trend analytics can isolate every trade to validate and capture price trends as they are happening, as opposed to others that may mathematically work off of day-end prices or other methods.

Conventional methodologies can have drawbacks that need to be managed. Momentum can be late, as it requires several months of price action before identifying a trend and therefore works primarily with long-lasting trends. Technical analysis indicators can help, but many of them can be inconsistent across different market cycles (ranging or trending) and volatility phases.

Trendrating offers an AI-driven, multi-factor model that decodes buying versus selling pressure, the driving force behind medium-term trends. Our advanced AI technology makes it easy to monitor over 17,000 stocks globally and receive timely alerts on any trend reversal.

That is why our research platform was able to issue a bear trend signal across crypto ETFs near their tops before most of the price drop damage was done. Their sharp drop illustrates how quickly market sentiment can turn and how fast huge losses are produced. That is why best-in-class research and methodology to detect price trend reversals in time should be part of any sound investment process.

Hortz: Any other thoughts you can share on how advisors, asset managers, and other professional investors can use this type of advanced price trend analysis research tool?

Pellegrinelli: We specifically designed our modern data research platform with AI technology (including an AI Assistant) and enhanced market intelligence capabilities that, in a few clicks, can be quickly added as a research and decision-making overlay to any investment manager’s current investment process, including management of crypto ETFs.

We currently invite and offer managers extended free trials to demonstrate and prove with facts how our advanced AI price trend analytics and alpha discovery research platform can provide enhanced market intelligence, strengthen risk management, and improve investment performance for any manager, using any investment methodology.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

Find financial advisors in Burlington, Vermont ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Burlington for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Burlington featured on Wealthtender you may want to add to your shortlist.

Featured Burlington Financial Advisors

As you prepare to interview financial advisors in Burlington who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Burlington

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Burlington.

The Benefits of Hiring a Financial Advisor in Burlington

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Burlington, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Burlington? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Burlington Financial Advisor

Before hiring a financial advisor in Burlington, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Daniel Kenny, Chief Executive Officer, and Kristian Borghesan, Chief Marketing Officer, of FutureVault | Image Credit: Institute for Innovation Development

[Digital Vaults combined with AI and private Large Language Models (LLMs) create an increasingly important category of data management — Intelligent Document Processing (IDP) — where static documents are transformed into dynamic enterprise assets. Firms can now extract, structure, and contextualize critical data from documents, at scale and automatically, into an intelligent system that delivers real-time insights, automated workflows, and compliance-ready outputs.

This technology category has been growing at a CAGR of 37% because it provides financial organizations significant value compared to standalone data. The technology can be used to summarize documents, extract key data points, and query across multiple documents or an entire document vault. Integrating IDP capabilities with a digital vault platform provides a powerful solution for managing and deriving insights from an organization’s massive amount of document-driven data.

To better explore the technology evolution of AI-powered Digital Vaults, we reached out to Daniel Kenny, Chief Executive Officer, and Kristian Borghesan, Chief Marketing Officer, of FutureVault – an award-winning white-label, AI-Powered Digital Vault platform for financial institutions. They have been early pioneers of the Client Life Management Vault™ and this emerging Intelligent Document Processing solution.]

Hortz:Can you explain what Intelligent Document Processing is and why it has emerged as an important technology advancement for financial firms?

Kenny: Intelligent Document Processing, often referred to as just IDP for short, refers to the use of AI, machine learning, and language models to automatically classify documents, extract relevant data, and understand context across unstructured content such as PDFs, scanned images, emails, documents, and forms. Unlike traditional Optical Character Recognition (OCR), which simply converts text from an image into characters, IDP now understands what a document is, what information matters, and how that information should be used downstream. In financial services where documents are foundational to many critical client interactions, operational processes, and regulatory requirements, this distinction is critical.

IDP has emerged as an essential capability because the industry has reached the limits of manual and semi-automated document handling that is required to not only scale but even to simply manage the status quo.

Borghesan: Institutions and firms are managing growing volumes of documents while facing tighter regulatory scrutiny, higher client expectations, and pressure to operate more efficiently. Traditional processing methods introduce risk through inconsistency, incompleteness, and human error, and they scale linearly with headcount.

It is essential to acknowledge that data embedded in documentation is worth materially more than raw data due to the context it holds and represents, as well as its inherent richness. In the context of applications, loans, and especially legal matters, disputes, and litigation, the document is almost always the golden source of truth.

IDP addresses this by turning documents (where data is captive) into structured, reliable data that can be governed, audited, and integrated into enterprise systems. Something financial institutions have needed for a long time but have not had the tools to do this effectively and at scale until now.

Hortz: Can you expand on the benefits and use cases of Intelligent Document Processing for financial services?

Borghesan: The benefits of IDP extend well beyond efficiency, although that is often where firms see impact first. By automating document classification, validation, and data extraction, IDP materially accelerates processing times across onboarding, compliance, account servicing, audits, reporting, and so on. Tasks, over the course of a year, that once required manual review of thousands, better yet, millions of pages can be completed in hours or days with far greater consistency and traceability.

Just to give you one real-world example, we recently partnered with a large insurance conglomerate on a document processing initiative involving approximately twenty million pages of scanned historical documents. Using IDP, we classified and identified document types, extracted specific data fields from each, and delivered the output in a structured format ready for ingestion into their internal systems. The project was completed in roughly five weeks.

Kenny: On the flip side, using traditional, manual document review, this effort would have required dozens of resources and taken years to complete. In reality, it would likely never have been completed at all. That gap between what is theoretically possible and what is practically achievable is where IDP delivers its greatest value.

Hortz: How do AI and LLM systems unlock the value of data contained within documents, and how do they determine what information to extract?

Kenny: AI and private large language models (LLMs) unlock document value by interpreting context, structure, and meaning rather than relying on rigid templates or fixed rules. Financial documents vary widely in format, language, and quality – particularly when dealing with scanned or legacy content. LLMs are able to understand these variations and identify relevant information even when documents are incomplete, inconsistent, or poorly structured, which is where traditional automation almost always fails and leads to operational leaks.

Borghesan: The information extracted from documents is usually driven by the business rules and requirements of the enterprise. Different functions care about different data and different firms might be required to evidence differing information and data. Compliance teams may focus on completeness, signatures, and disclosures. Advisors may need beneficiary details, asset values, or restrictions. Operations teams may prioritize identifiers and system-ready fields. Effective IDP systems are designed to align extraction logic with specific use cases, ensuring that the output is accurate, relevant, and usable—not just technically extracted, but operationally meaningful.

Hortz: What specific capabilities are you designing for advisors and clients by integrating AI and LLMs with digital vault technology?

Borghesan: For advisors and clients, the integration of AI and private LLMs contained within a secure digital vault provides a “single source of truth” where all documents across the relationship reside, reducing friction and increasing clarity.

Today, it is more than common for critical client information to be spread across dozens of documents across multiple systems, making it time-consuming and costly to assemble a complete picture; not to mention this results in a poor experience on both sides. By applying an intelligence layer on top of a digital vault, advisors can surface timely and relevant information and insights across documents without manually searching or combing through files one by one.

Kenny: This foundation enables higher-value capabilities such as rolled-up document summaries and Next Best Actions for advisory teams. Advisors can quickly understand what has changed, what is missing, or what requires attention – whether that is expiring documents, incomplete records, or opportunities to deliver better advice all around.

The goal is not necessarily automation for the sake of automation, but to remove administrative burden and reduce the risk of oversight, allowing advisors to focus on informed decision-making and higher-quality client engagement.

Hortz: What other advancements or applications do you see emerging with Intelligent Document Processing?

Kenny: The next major advancement in IDP that we see is the shift from reactive processing to proactive, autonomous, end-to-end workflows. Rather than documents being reviewed after the fact, intelligence can be applied as documents enter the system from any source (client, third-party systems, advisor uploads, etc.), triggering actions such as routing tasks, updating records, flagging exceptions, or initiating follow-ups automatically. This reduces delays, eliminates manual handoffs, and improves overall governance.

Borghesan: Over time, this leads to autonomous processing loops where document data continuously improves enterprise operations. Incomplete or inconsistent information is identified immediately, risks are surfaced earlier, and downstream systems stay aligned without manual intervention.

For institutions, lines of business, and advisory teams this means stronger controls, cleaner data, and better client experiences and personalized advice delivered at scale.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

Image Credit: Institute for Innovation Development

[The capital structures of companies in the high-yield universe have expanded greatly from traditional high-yield bonds to an array of alternative financing solutions that include bank loans and private credit. Regardless of the growth of these various credit instruments, it remains a cyclical asset class with spreads widening/tightening based on market fundamentals and idiosyncratic issues around capital structures, providing an enhanced opportunity set for income investors.

To better understand how the growth of the alternative credit markets expands opportunities for high-yield investors, we were introduced to Donald E. Morgan, Managing Partner & Chief Investment Officer and Doug Pardon, Co-Chief Investment Officer of Brigade Capital Management– a global alternative asset management firm, founded in 2006, that employs a multi-strategy, multi-asset class approach to investing across the broad credit universe. They have been developing best-in-breed credit expertise in fundamental corporate and alternative credits with a proven, cycle-tested active investment process to deliver risk-adjusted returns aligned to client needs.

We asked them questions to better understand their perspectives on the global credit universe, their Brigade High Income Fund (BHIIX), and their research and portfolio construction process utilizing credit rotation across the full high yield capital structure.]

Hortz: Can you give us a brief overview of the high-yield investment universe and some of the different investment areas you are working with?

Morgan: When most people think about the high-yield universe, they are thinking about corporate high-yield bonds. That asset class is a trillion-dollar-plus marketplace comprised largely of unsecured fixed-rate bonds that historically financed leveraged buyouts. That is still the core of what many fund managers focus on.

Throughout our careers, Doug, the team, and I have looked at the entire capital structure of companies which gives us a broader perspective on what we call “opportunistic” or “multi-asset credit”. It has increasingly been known as the alternative credit space where a broadly syndicated loan market has developed. These are typically first lien, but are sometimes second lien loans. These securities tend to be floating rate with five to seven years in maturity and attractive yields.

Pardon: We also have a large, structured credit team that has been actively involved in the development of the collateralized loan obligations (CLO) market over the last 15 or 20 years. These are structured vehicles that purchase broadly syndicated loans and are structured to fund those investments through the issuance of debt. There are BBB and BB portions of CLOs that would be part of our universe.

Other areas include preferred stocks, busted convertible bonds, and stressed and distressed debt. We are looking for risk-adjusted opportunities across a very broad universe of higher yielding securities that are generally sub-investment grade.

Hortz: How would you describe your fixed-income multi-strategy and multi-asset class investment style and methodology?

Morgan: Our high-yield strategy allows us to opportunistically invest in the below-investment grade asset classes we just mentioned. Within these asset classes, we have a multi-sector approach driven by our research team. Our analysts cover different industries and sectors, searching across the full spectrum of high-yield credit for risk-adjusted opportunities that we believe offer much better relative value.

We also employ a bottom-up strategy. The research team is looking at individual companies and modeling them. Even in “bad” sectors, there can still be good ideas discovered from a bottom-up perspective. By analyzing these asset classes and industries, and then employing bottom-up research, we develop a large set of ideas and opportunities that we focus on. From there, we narrow down this universe based on the best risk/reward opportunities. The full focus is to protect principal by having a “margin of safety” for downside protection. Beyond that, we are looking to maximize the yield while also seeking total return.

Pardon: Additionally, we have a top-down macro and tactical twist to our multi-strategy approach. You will find that these asset classes are cyclical and experience opportunistic events. Something will happen in the economy – there will be a recession, credit spreads will widen and the asset class can experience high volatility in those periods, or there will be some sort of financial crisis over a shorter period of time that will cause spreads to blow out.

When credit spreads are wide, we feel like the market’s offering you a lot of “fat pitches”. We will actively move down in credit quality focusing on weaker B and CCC securities primarily within the high-yield bond universe.

Conversely, when credit spreads are tight, we will tend to lean into some of these other asset classes where we would be looking for alternative opportunities, including bank loans, and upgrade the credit quality of the portfolio by focusing on stronger B or BB securities to maximize liquidity.

Hortz: Can you further explain some of the alternative credit areas you follow and how you opportunistically manage these different sectors to add income and growth to portfolios?

Morgan: There are inefficiencies in all asset classes, including these other high-yield investment areas. What we are always looking for is when they are offering much better relative value or when, for whatever reason, we have a significant advantage over our competitors.

For instance, we have exposure to busted convertible bonds and have the flexibility to opportunistically increase that exposure when we see attractive value. If you think about a convertible bond, most are issued at par at a time when people are optimistic about the company’s stock price. Over time, if that stock has traded down for whatever reason – missed earnings, industry fundamentals – these bonds, because they are highly sensitive to the stock price, will trade down and hit what is referred to as a bond floor. They tend to have 2% – 3% coupons, which means this bond floor can be 75-80 cents on the dollar.

Now you have a security that is not very sensitive to the underlying equity. It has a low current yield because the coupon is low, but an attractive yield to worst due to the lower dollar price. If that bond trades from the eighties to par, you are going to have a high total return on that security. We will look at those credits and value them. If we feel that there is particularly good asset coverage and downside protection, we will step in.

The convertible bond market basically becomes an inefficient market in the sense that there are not a lot of people focused on this universe. The convertible arbitrage funds have gotten out of these securities. A convertible mutual fund wants more equity sensitivity. This is sort of an unloved security within a small asset class.

Pardon: On the CLO side, if you buy a broadly syndicated loan at SOFR+300 basis points (“bps”), you are usually facing a single individual issuer, and the outcome of that investment is going to be solely focused on how that issuer performs. Conversely, in the CLO market that issues BB or BBB securities, a lot of these securities are bought by hedge funds or levered vehicles, and in periods of market volatility, you will see sellers of CLO debt out of these vehicles.

When volatility forces levered players to sell, we will step in and buy a BBB CLO at a spread that is wider than the overall underlying issuers of the broadly syndicated loan market. So, you can own a BBB bond of a CLO that owns 400 different issuers, versus an individual issuer loan where you are facing that single company. And the only way to really have realized losses on that investment is if 10% of the portfolio defaults year after year, which is highly unlikely. In those types of environments, the inefficiency arises because there are more sellers and illiquidity. We can step in and, from a relative value perspective, do so at a higher spread in these securities than individual loans with much better downside protection.

We will also look at preferreds. Recently, there was a financial institution that wanted to issue preferreds to raise regulatory capital. Preferreds can pay dividends, in kind or in cash, but we structured this preferred 5% wider in yield than their underlying unsecured bonds. We also put a feature in where there would have to be a minimum level of high cash interest. I would say that our ability to do this gives us an advantage and you are just not going to find a lot of high-yield investors that are looking at the preferred part of the market.

So those are a few of the things that we look at. We also will look at stressed municipal debt, commercial real estate or other areas, but that gives a flavor of the types of differentiated areas we can opportunistically take advantage of.

Hortz: Talk to us about the capabilities of your proprietary in-house research. How was it structured differently to compete with other researchers and be effective across the full high-yield credit universe?

Morgan: One of the differentiating factors for our firm is that we have always been a partnership from day one and a lot of our research analysts are equity partners in the firm, creating one team that is growing together. I also think that the breadth of the research and the experience of our team members stack up very well against our competitors. We have 19 people on the research side with senior analysts having an average of over 20 plus years of experience, covering the same sector(s) for the majority of their careers. They have seen industry cycles and developed deep knowledge in these areas of what drives success or failure for companies within their respective industries.

The other differentiator is that the research team covers the entire capital structure of companies we are covering. Our chemical analyst is not just covering their high-yield bonds but also any syndicated loans, busted convertibles, preferreds, and fielding club deals for loans looking for extra yield and growth potential. We are all working together on the High Income Fund, so we do not have separate teams within the firm. Those are some of the differentiating factors.

Pardon: We built our firm into a diversified investment business extending our high yield expertise into some of the more interesting areas of the expanding marketplace and building the stability of a broader-based firm. The uniqueness of our overall organization has become an attractive place for specialized investment analysts to land and help us build our team. With our team, an analyst has a diversified skill set having invested for many years, not only in long-only, but also as a hedge fund investor. That adds a little bit of a unique dynamic.

Hortz: How is your Brigade High Income Fund (BHIIX) strategy positioned within your broader platform, and what makes it distinct from other high income or multi-sector credit funds?

Morgan: Within our platform, this Fund is an opportunistic high-yield credit fund that can expand into multi-sector and especially alternative credits. It is our only retail mutual fund across our investment platform, so for these investors, it is the only way to get access to our institutional high-yield investment process.

What sets this Fund apart from the broader retail high-yield mutual fund universe is the expanded high-yield universe that we are open to and actively investing in. You will see our core base of income generating high-yield bonds go up or down – depending on where we are on the credit cycle – and we can increase our weightings to alternative credit markets that can help either dampen volatility, maintain high income, generate total return, or meet other investment and risk control objectives. While there are other high-yield funds that have flexibility, having dynamic and purposeful access to alternative credits like structured credit, bank loans, as well as participating in club deals, allows us to have a more diversified and differentiated high-yield income approach.

Another nuance of this differentiation is that most of our peer group runs incredibly diversified and one-dimensional portfolios, with hundreds and hundreds of issuers at very small weightings across the portfolio. We have a more concentrated approach, and while we are benchmark-aware, we are not closet indexers by clearly being in other asset classes that are not in the broader high-yield index.

Pardon: As mentioned before, we will always have a core base of high-yield bonds generating income, but we will spend a lot of time thinking about where we are in a particular credit cycle and looking for where the best high-yield investments appear across our expanded opportunity set. Our opportunistic, or tactical, investment approach is where we are truly most differentiated.

A lot of the larger funds in this category are highly diversified, but for the most part, they may be focused on getting beta exposure to the asset class. While that is fine for some people, there is an opportunity to generate a fair bit more than that if you can have an opportunistic approach, coupled with the ability to perform deep research into alternative credits that are not as easy to find. Those two pieces are what we bring to the table.

Hortz: What type of investor or portfolio objectives is this strategy best suited for?

Morgan: We address investors who seek high income and capital preservation- such as retirees living on a fixed income. Our goal is to strive to meet those objectives through sector rotation and individual bottom-up security selection of securities that are out-yielding the market, where we see high current risk-adjusted returns and income. We place strong emphasis on capital preservation and maintaining a margin of safety in our investing approach.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

You opened a certificate of deposit (CD) when rates were attractive, and now it’s maturing. You have a decision to make and it’s one that deserves more thought than simply letting it auto-renew.

Whether you’re in your prime earning years, transitioning toward retirement, or managing a windfall from a life change like divorce or inheritance, understanding your CD maturity options can help you make the most of your money.

This guide walks through what happens when a CD matures, your reinvestment choices, and how to decide what’s right for your financial plan.

What Happens When a CD Matures?

When your CD reaches its maturity date, the bank or credit union returns your principal plus any accrued interest. At that point, you typically have a grace period, usually 7 to 10 days, to decide what to do next.

During the grace period, you can:

Withdraw your funds penalty-free

Reinvest in a new CD (often at current rates)

Move your money to a different account type

Do nothing and allow the CD to automatically renew

If you don’t take action during the grace period, most institutions will automatically roll your CD into a new term at whatever rate they’re currently offering, which may be lower than what you originally earned.

Important: Once the grace period ends and the CD renews, withdrawing early typically triggers a penalty (often several months’ worth of interest).

Your CD Maturity Options: A Clear Breakdown

Option 1: Reinvest in a New CD

If you don’t need immediate access to the cash and current CD rates are competitive, reinvesting can make sense. You lock in a new rate for a set term and continue earning predictable, FDIC-insured returns.

When this works:

Current rates are equal to or better than your maturing CD

You have other liquid savings for emergencies

You’re comfortable with the term length (6 months to 5 years)

Watch out for: Lower rates than your original CD, or tying up money you might need sooner than expected.

Option 2: Build a CD Ladder

A CD ladder is a strategy where you divide your money across multiple CDs with staggered maturity dates. For example, instead of putting $25,000 into one 5-year CD, you might open five CDs of $5,000 each, maturing in 1, 2, 3, 4, and 5 years.

Why this works:

You gain access to a portion of your funds each year

You reduce interest rate risk by not locking everything in at once

You maintain higher average returns than keeping everything in savings

As each CD matures, you can either withdraw the funds or reinvest at the current rate for a new 5-year term, keeping the ladder going.

Option 3: Move to a High-Yield Savings Account or Money Market

If you value flexibility over maximizing returns, moving your matured CD into a high-yield savings account or money market account can be a smart move.

When this makes sense:

You might need the money within the next 6–12 months

Interest rates are rising and you want to avoid locking in a lower CD rate

You’re building or replenishing your emergency fund

You’re in a transition period (career change, pending home purchase, divorce settlement)

Today’s high-yield savings accounts often offer competitive rates without the commitment or penalties of a CD.

Option 4: Invest for Growth

If your CD was part of a longer-term savings strategy and you don’t need the funds soon, you might consider moving some or all of it into investments like stocks, bonds, or a diversified portfolio.

When this could work:

You have a solid emergency fund in place (3–6 months of expenses)

Your time horizon is 5+ years

You’re comfortable with market fluctuations

You’re saving for retirement or other long-term goals

Caution: Unlike CDs, investments are not FDIC-insured and carry the risk of loss. This option is best suited for money you won’t need in the short term.

You might also consider using matured CD proceeds to fund or top off retirement accounts like a Roth IRA or 401(k), especially if you have contribution room and want to take advantage of tax-deferred or tax-free growth.

Option 5: Use It Strategically

Sometimes the best use of matured CD funds is tactical, paying off high-interest debt, funding a home improvement that adds value, or covering a major planned expense like a wedding or education costs.

Consider this option if:

You’re carrying credit card debt or other high-interest loans

You have a specific goal or purchase planned within the next year

The opportunity cost of keeping the money in a CD outweighs the interest earned

How to Decide What’s Right for You

Here’s a simple framework to guide your decision:

Step 1: Assess your liquidity needs Do you have an adequate emergency fund? Will you need this money in the next 1–2 years?

Step 2: Compare current CD rates to alternatives Are new CD rates competitive? How do they compare to high-yield savings, money markets, or short-term bonds?

Step 3: Evaluate your overall financial plan Where does this money fit in your bigger picture? Are you saving for retirement, a home, or simply preserving wealth?

Step 4: Consider your timeline and risk tolerance Are you comfortable with market risk, or do you prefer the safety and predictability of FDIC-insured options?

Step 5: Act during the grace period Don’t let inertia make the decision for you. Mark your calendar and set a reminder before your CD’s maturity date.

Common Mistakes to Avoid

Letting your CD auto-renew without reviewing rates. You might lock in a lower rate than what’s available elsewhere.

Withdrawing early and paying penalties. Plan ahead so you can access funds during the grace period.

Ignoring inflation. If your CD rate doesn’t keep pace with inflation, your purchasing power erodes over time.

Forgetting to diversify. Keeping too much in CDs, especially in a rising rate environment, can limit your financial flexibility and growth potential.

Not shopping around. Banks and credit unions vary widely in the rates they offer. A quick comparison can sometimes boost your return significantly.

Frequently Asked Questions

What is the grace period for a maturing CD?

Most financial institutions provide a 7- to 10-day grace period after maturity during which you can withdraw or reinvest your funds without penalty. Check your CD’s terms to confirm.

Can I withdraw my CD at maturity without penalty?

Yes. During the grace period, you can withdraw your principal and interest with no early withdrawal penalty. After the grace period, if the CD has renewed, early withdrawal penalties typically apply.

Should I roll over my CD or move to a high-yield savings account?

It depends on your goals. If you won’t need the money soon and current CD rates are attractive, rolling over makes sense. If you need flexibility or rates are rising, a high-yield savings account may be better.

How does a CD ladder work?

A CD ladder spreads your money across multiple CDs with different maturity dates. This gives you regular access to portions of your savings while maintaining higher average interest rates than a single savings account.

Can I use matured CD funds to contribute to my IRA or 401(k)?

Yes, as long as you meet IRA or 401(k) contribution requirements and limits. This can be a smart way to move money from a taxable CD into a tax-advantaged retirement account.

What happens if I do nothing when my CD matures?

Most institutions automatically renew your CD at the current rate for a similar term. This may or may not be in your best interest, especially if rates have dropped or your needs have changed.

Final Thoughts

A maturing CD isn’t just a renewal notice, it’s a financial checkpoint. It’s an opportunity to reassess your goals, compare your options, and make an intentional choice about where your money goes next.

Whether you reinvest, ladder, move to savings, or invest for growth, the key is making a decision that aligns with your broader financial plan and life stage.

When choosing a financial advisor, Americans prioritize trust. Yet many advisors struggle to effectively convey their trustworthiness when prospects research them online. Advisors using Nitrogen’s growth platform to deliver data-driven client experiences can amplify that advantage with Wealthtender’s online reputation features, creating a competitive edge to drive outsized growth in 2026 and beyond.

In the Nitrogen 2025 Advisor Growth Survey of over 1,000 investors and 425 advisory firms, one finding in particular caught the attention of our team at Wealthtender: 30% of investors cited “trust and personal rapport” as the single most important factor when choosing a financial advisor, ranking it higher than investment track record, credentials, fee structure, or range of services offered.

Later in the year, our Wealthtender 2025 Study of $100K+ Households Seeking Financial Advice produced a related finding, showing that 83% of people want to find and read online reviews about advisors before making a hiring decision. This overwhelming majority is essentially saying: “I need to know what other clients think. I need proof that this advisor can be trusted.”

But here’s the challenge both surveys uncovered: while advisors excel at building trust through face-to-face client interactions, many have struggled to demonstrate that same sense of trust with prospects who are increasingly finding and researching advisors online, even after a personal referral.

The solution? A powerful combination of proven client-facing technology and authentic social proof, powered by Nitrogen and Wealthtender.

Nitrogen’s survey found that organic marketing (content and SEO) has overtaken referrals as the top lead source for the first time, with 28% of advisors citing it as their primary channel. This shift reflects a fundamental change in consumer behavior, particularly among the next generation of prospective clients who are much more likely to research advisors online before ever picking up the phone.

Wealthtender’s research confirms and amplifies this trend with compelling data:

97% of people plan to contact multiple advisors before making a hiring decision

96% will still research an advisor online even when that advisor comes highly recommended

83% want to read online reviews about advisors before making their decision

61% consider positive online reviews on independent websites essential for determining an advisor’s reputation

Think about what this means: Nearly everyone is comparison shopping, almost everyone is doing their own research regardless of referrals, and four out of five won’t seriously consider you without reading what your current clients have to say about working with you.

When prospects evaluate financial advisors today, they’re trying to answer one question: “Can I trust this person with my financial future?” And they’re looking to other clients’ experiences for that answer.

Why This Matters for Nitrogen Users

If you’re already leveraging Nitrogen’s growth platform with its popular Risk Number®, proposal generation, and client engagement tools, you’re positioned for success.

But here’s the opportunity many advisors are still missing: How do prospects discover this about you before they become clients? And more importantly, how do they see proof that other clients trust and value your approach?

You could have the most thoughtful risk assessment process in place, but if prospects can’t find reviews from clients praising that process or the experience they can expect if they hire you, you’re invisible in the research phase where 96% are actively looking and 83% are specifically seeking reviews.

The Missing Piece: Making Trust Visible

This is where the combination of Nitrogen and Wealthtender becomes incredibly powerful for advisors looking to accelerate their growth.

Think about it: You’re using Nitrogen to deliver exceptional, technology-driven portfolio management. You’re having meaningful conversations about risk tolerance. You’re providing data-driven insights that build trust with every interaction. Your clients appreciate the modern, transparent experience. But prospects can’t see that. And according to Wealthtender’s research, 83% of them are actively looking for it.

The Wealthtender Advantage for Nitrogen Users

Wealthtender was built specifically to solve this visibility problem for financial advisors. Here’s how it works in tandem with Nitrogen to position you for growth this year:

1. Capture Authentic Client Feedback

Your clients already trust you. Nitrogen’s Check-ins feature even shows that client portfolio sentiment improves over time, even during market downturns. Wealthtender makes it easy to systematically collect and showcase this feedback through verified client reviews.

Given that 83% of prospects are actively seeking these reviews, every satisfied client who doesn’t leave a review represents missed opportunity with dozens of potential prospects.

2. Demonstrate Your Technology Edge

When prospects visit your Wealthtender profile, your client testimonials may offer insights into the client experience enhanced by Nitrogen-powered tools. For example, clients writing reviews about their experience working with you might touch on:

How your risk assessment process helped them understand their portfolio

The clarity and transparency your technology-driven approach provides

The confidence they feel seeing data-driven insights backing your recommendations

The value of your proactive communication during market volatility (which 85% of investors in Nitrogen’s survey said they find valuable)

Remember: Wealthtender’s research found that 61% of people consider positive online reviews on independent websites essential for determining an advisor’s reputation. This means your client reviews aren’t just nice-to-have, they’re a critical factor in a prospect’s decision-making process.

3. Build Trust Before the First Meeting

Nitrogen’s research found that 68% of investors would consider switching to an advisor who provides more personalized communication and technology-driven insights, if the benefits were made clear. Your Wealthtender profile offers an opportunity to make those benefits crystal clear to prospects before they ever reach out.

And since 96% of prospects will research you online even if you come recommended, your Wealthtender profile is likely one of the first substantive impressions of your practice beyond a simple referral, whether they view your profile directly or discover insights sourced by Google or AI search tools from your Wealthtender profile.

4. Stand Out in the Comparison Process

Here’s a critical insight from Wealthtender’s research: 97% of people plan to contact multiple advisors before making a hiring decision. This means you’re always competing against at least one or two other advisors.

When prospects are comparing their options, those with strong online reviews have a decisive advantage. If two advisors seem equally qualified on paper, but one has several detailed client reviews and the other has none, the choice becomes obvious.

5. Convert More Leads

Remember that 45.7% of advisors in the Nitrogen study identified “managing client investment performance expectations” as their biggest barrier to landing new clients? When prospects read reviews from current clients that convey their satisfaction with their experience, that barrier dissolves.

A Real-World Scenario

Let’s say you’re a Nitrogen user in Denver. A 45-year-old technology executive searching online for a local financial advisor who specializes in equity compensation finds three options:

Advisor A: Professional website, list of services, bio. No reviews visible. The executive moves on.

Advisor B: Similar website, plus mentions they use “cutting-edge technology” (but no specifics about what or why it matters). Two Google reviews from three years ago. The executive remains skeptical.

Advisor You (Nitrogen + Wealthtender): Professional website and Wealthtender profile showcasing verified client reviews with specific feedback like:

“My advisor uses tools that help me understand why my portfolio is structured the way it is.”

“When markets are rocky, my advisor proactively reaches out with data showing why we shouldn’t panic. That level of communication and insight is exactly what I was looking for.”

“I’ve worked with three advisors over the years, but this is the first time I’ve really understood my investments. Her communication style and the technology she uses makes everything so clear.”

The executive is part of the 83% who want to read reviews and the 96% who will research online. Your Wealthtender profile provides them exactly what they’re looking for: proof that other clients trust you, specific examples of your technology-driven approach, and validation that you deliver on your promises.

Who do you think that executive calls first?

Nitrogen Got It Right: Your Roadmap for Growth

The annual Nitrogen Advisor Growth Survey is a great read for advisors planning and recalibrating their growth strategy to grow faster than peers. Combined with Wealthtender’s research on how Americans actually find and hire advisors, these studies provide a complete picture of both what consumers value and how they search for advisors.

The surveys’ key findings create your roadmap for success in 2026:

Trust is paramount (30% rank it #1, and 83% seek proof through reviews)

Online research is universal (96% research online even after referrals)

Reviews are critical (83% want to read them; 61% view them as essential)

Risk tolerance understanding is critical (91.6% rate it 8+ out of 10)

Technology creates differentiation (when prospects can see how you use it through client reviews)

Data-driven insights build confidence (90% trust advisors more when they use advanced analytics)

Fee transparency matters (73% consider it crucial for establishing trust)

Take Action: Turn Insight Into Growth This Year

If you’re already a Nitrogen user, you’re delivering an exceptional client experience backed by sophisticated technology. The question is: are you capturing and showcasing that value in a way that meets prospects where they are: online, researching advisors, and looking for proof that you can be trusted?

Here’s your action plan for the year ahead:

1. Join Wealthtender (it takes just 2 minutes and we’ll create your profile for you)

Remember: 96% of prospects research online even after getting referrals

83% want to read reviews before deciding

Your profile puts you in front of both groups

2. Implement a Systematic Review Collection Process

After client check-ins or conversations using Nitrogen tools

On your birthday and/or anniversary of your firm

After a set period of time upon becoming a client (e.g., at a 6-month milestone)

Every review you don’t collect is opportunity lost with the 83% of prospects seeking them

3. Highlight Your Technology-Driven Process

Showcase how you use risk tolerance assessment

Feature your data-driven investment approach

Emphasize your proactive communication strategies

Let clients describe these benefits in their own words

4. Let Your Results Speak

Share authentic client stories about their experience

Demonstrate the value of your Nitrogen-powered process

Build trust with prospects before the first conversation

Remember: 61% view positive independent reviews as essential

The Nitrogen-Wealthtender Advantage

Nitrogen’s 2025 Firm Growth Survey confirms what investors value most. Wealthtender’s 2025 research reveals how they search for it. Together, these studies paint a clear picture: the advisors who will thrive in 2026 and beyond are those who combine genuine trust, technological sophistication, and authentic social proof, and make it all visible where prospects are actually looking.

If you’re already using Nitrogen to deliver an exceptional, data-driven client experience, it’s time to make sure the 96% of prospects who are researching advisors online can find you, and the 83% who want to read reviews before deciding can see proof that other clients trust you.

The firms that experienced 11%+ organic growth last year (57% of survey respondents) didn’t succeed by accident. They aligned what they deliver with what investors actually want, and they found ways to make that value visible to prospects in the channels where decisions are actually made.

As we move through 2026, this alignment will become even more critical. The advisors who win will be those who not only deliver excellence but make it impossible for prospects to miss.

If Nitrogen is your growth platform for client delivery, Wealthtender should be your growth platform for client acquisition.

Ready to amplify your Nitrogen advantage in 2026?Join Wealthtender today and start converting the trust you’ve built into the visibility you need to grow.

Want to see how individual advisors and leading wealth management firms are successfully using Wealthtender to grow their business? Visit Wealthtender.com/grow or schedule a demo to learn how you can start converting more prospects into clients with the industry’s first digital marketing platform for AI-optimization and compliant online reviews.

About the Author

Brian Thorp

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Book a Demo

Select a day in the calendar below to schedule a meeting with Brian Thorp, Wealthtender founder and CEO.

Find financial advisors in Hanover, New Hampshire ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Hanover for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Hanover featured on Wealthtender you may want to add to your shortlist.

Featured Hanover Financial Advisors

As you prepare to interview financial advisors in Hanover who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Hanover

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Hanover.

The Benefits of Hiring a Financial Advisor in Hanover

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Hanover, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Hanover? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Hanover Financial Advisor

Before hiring a financial advisor in Hanover, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

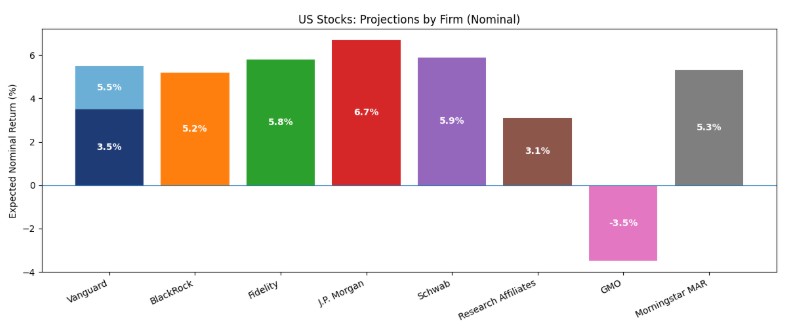

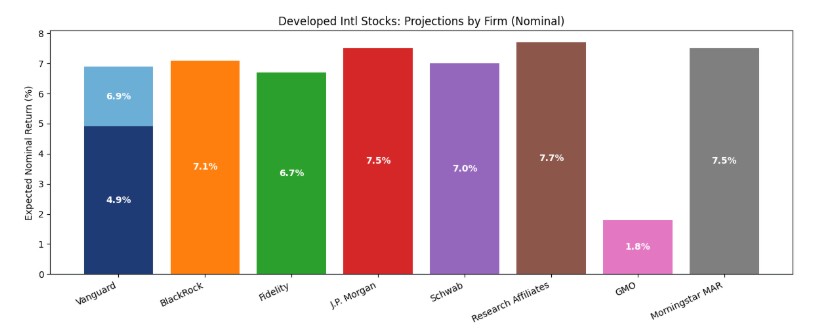

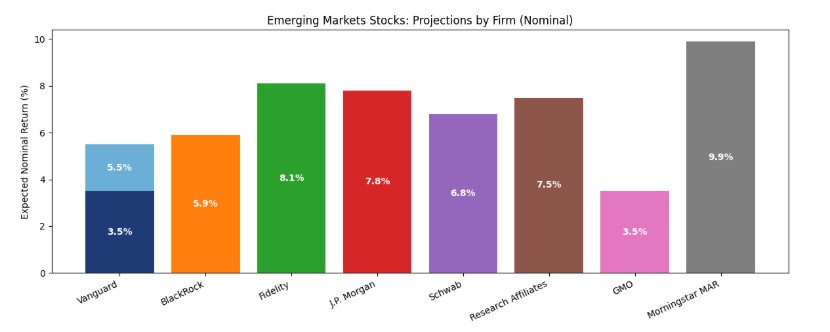

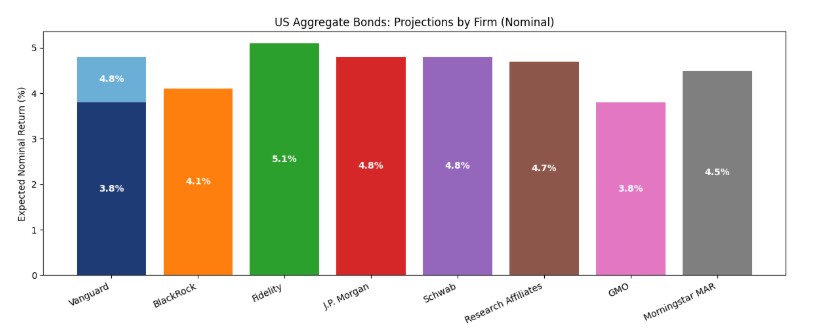

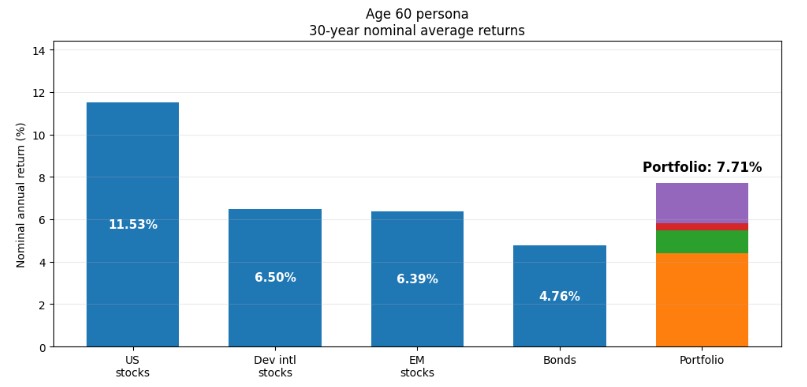

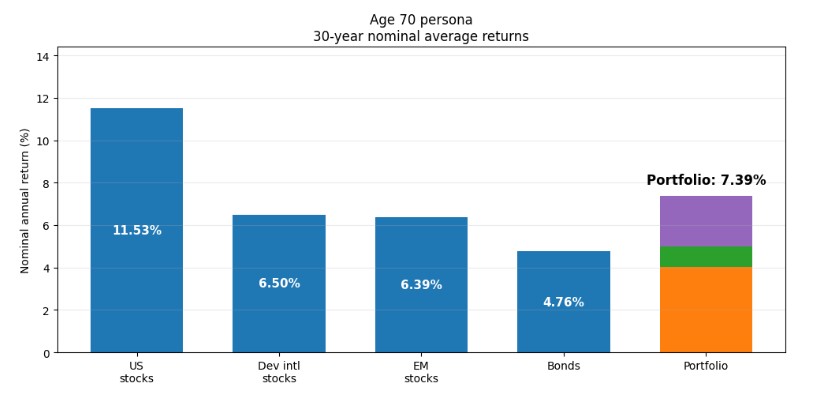

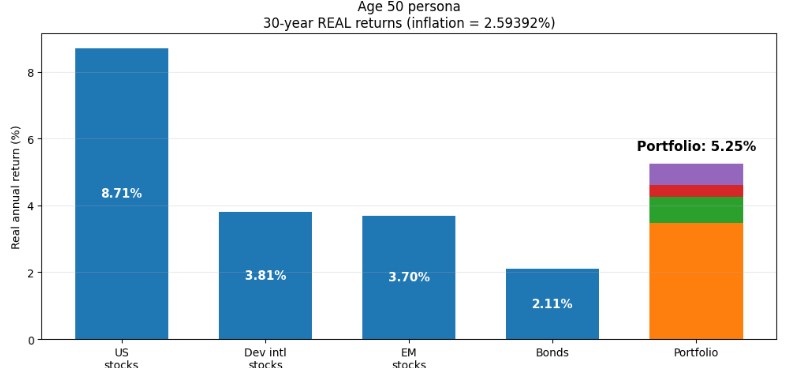

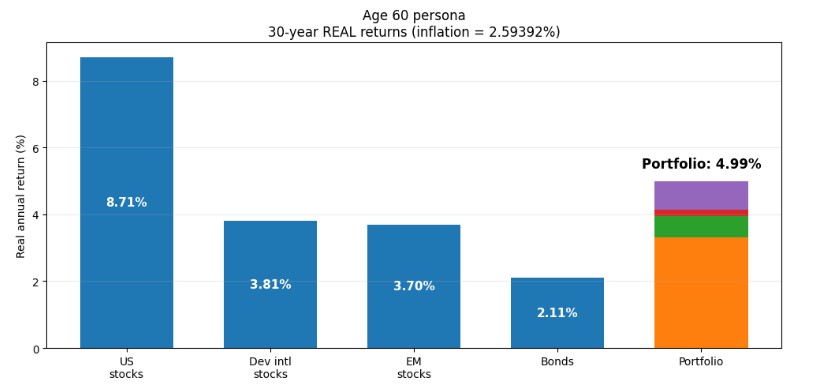

Every year, Morningstar Research reviews medium-term market return projections from several Wall Street firms.

The 2026 Morningstar Research report was just published, and, if you believe the projections, your financial plan may require some significant revisions.

I know I’ll consider how my plan may need to be adjusted.

What the Report Includes and Caveats to Note

The report is information-dense and, used correctly, lets us tailor our financial plans to what’s coming, rather than simply assuming market returns over the coming decade will match long-term historic ones.

However, there are some important caveats.

Time Frames Vary Between Projections

For each of four asset classes, the report provides the returns for the next 7-10 years by several Wall Street firms, including Morningstar Multi-Asset Research (Morningstar MAR), though some financial firms provide 10-15-year projections (JP Morgan), 20-year projections (Fidelity), or even 30-year projections (BlackRock and Vanguard, with the latter providing a range of returns for each asset class) instead. As a result, these projections should inform our medium-to-long-term planning, not what to do this year or next, nor what to expect over the long term, unless you concentrate on the three firms offering such projections.

Projections Aren’t Prophecies

The author cautions that these are projections, not guarantees. They’re intended to inform your planning, but you can’t count on them unfolding exactly as projected.

The Numbers Don’t Directly Address What You’ll Experience – They’re Nominal and Pretax

The projected returns are in nominal (except for Grantham Mayo Van Otterloo, or GMO) and pre-tax terms, which means that your plan needs to account for inflation that’s relevant to your personal basket of goods and services, as well as what your personal tax situation will be in retirement.

The Numbers Aren’t Exactly Apples-to-Apples

The different firms don’t necessarily look at the exact same asset classes. For example, JP Morgan, Research Affiliates, and Schwab only include large-cap equities in their US equity projections, BlackRock’s developed-market equities are limited to European companies, etc.

And Now, to the Numbers

Here are the market projections from the eight firms for each of the four asset classes. Note that, just for this section, I converted GMO’s numbers from the real (inflation-adjusted) returns quoted in the report to nominal numbers to better correlate with the other seven firms’ numbers, all of which were nominal.

Fig. 1. Medium-to-long-term market return projections for US equities (graphic created with ChatGPT).Fig. 2. Medium-to-long-term market return projections for developed-market equities (graphic created with ChatGPT).Fig. 3. Medium-to-long-term market return projections for emerging-market equities (graphic created with ChatGPT).Fig. 4. Medium-to-long-term market return projections for US bonds (graphic created with ChatGPT).

Now that we’ve seen the numbers, we’ll look at what they mean for you. As we’ll discover below, taken together, these projections throw three major curveballs for investors. Instead of basing your financial plan on long-term historical returns, you should plan on a decade or so of (1) a dramatic collapse in expected US equity returns, (2) international stocks outpacing US stocks, and (3) bonds offering returns so close to equities that stocks’ risk premium becomes minimal.

If you’re still planning based on long-term historical averages, these projections suggest you may be planning for the wrong future. Here’s why these curveballs are heading our way, what they mean, and what you can do to prepare.

How We’ll Interpret the Above Numbers

How much can we trust these projections?

To answer that, here’s a quote I often share: “It’s really hard to make accurate predictions, especially about the future.”

It sounds like something Yogi Berra could have said (and is often misattributed to him), but it was actually a quip by 1922 Nobel prize laureate, Danish physicist Nils Bohr, paraphrasing an old Danish folk saying.

With that in mind, I’ll borrow an analysis tool I used as a grad student doing research at the European high-energy physics lab (CERN) back in the 1980s. Since physicists don’t know how the universe works, the best we can do is make educated predictions and test them against experimental results.

One way to assess our systematic errors is to use multiple methods to make the same prediction and see how widely the results diverge. The more they diverge, the less accurate we believe them to be, and unless we have reason to believe outliers more than other results, we end up with less uncertainty if we discard those outliers.

Since the different firms use different methodologies, we can do the same here, discarding the highest and lowest predictions for each asset class, and assessing how much the remaining six projections vary.

Before we decide which number is highest or lowest, we’ll average Vanguard’s conservative and optimistic numbers to arrive at a single point prediction, giving it the same weight as the other firms’ projections.

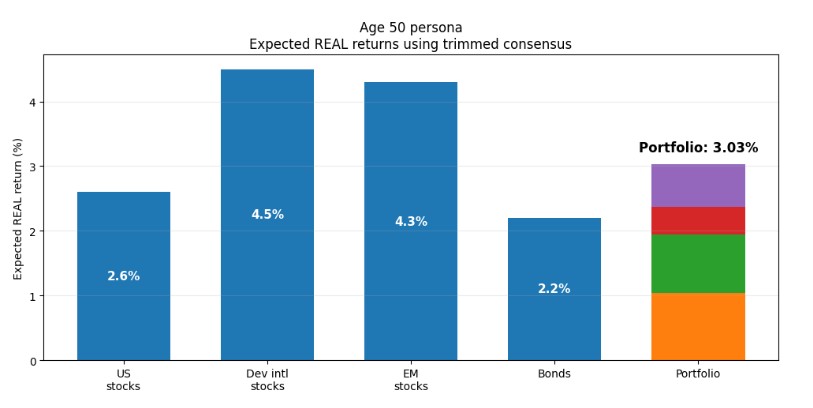

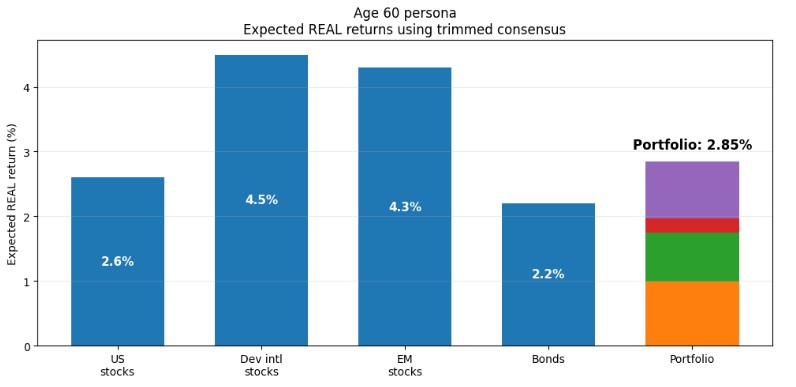

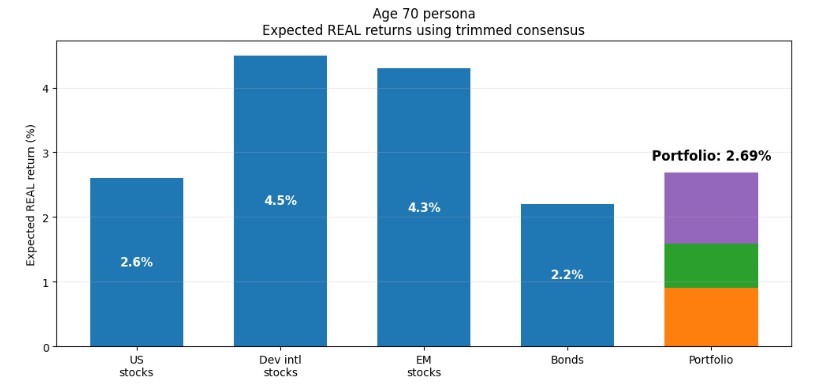

The following four graphs give us these projected annual returns for the four asset classes, with the “trimmed average” returns in the black bar at the right. However, since what matters most is how your portfolio does in inflation-adjusted, or real, terms, we show real returns, after correcting for the St. Louis Fed’s projected inflation for the next decade, 2.32166%.

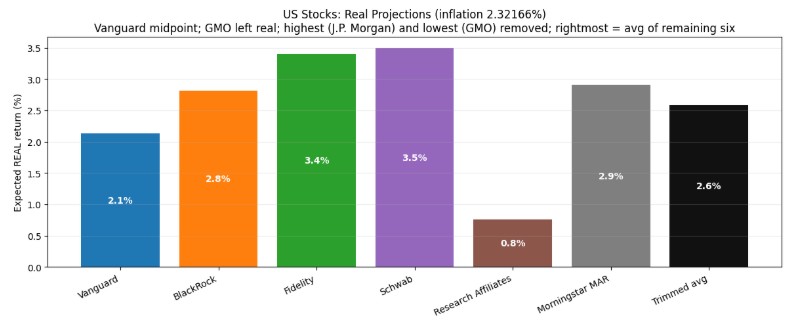

Fig. 5. Medium-to-long-term real average annual market return projections for US stocks, using the mid-point for Vanguard’s projections and removing the highest and lowest “outlier” projections to arrive at a “trimmed average” projection given by the right-most, black bar (graphic created with ChatGPT).

Here, for US stocks, even after removing the outliers, we see a spread between 0.8% and more than four-fold higher, 3.5%, projected real returns. This suggests to me that the eventual returns may be more likely to stray further from the 2.6% trimmed average projected real return.

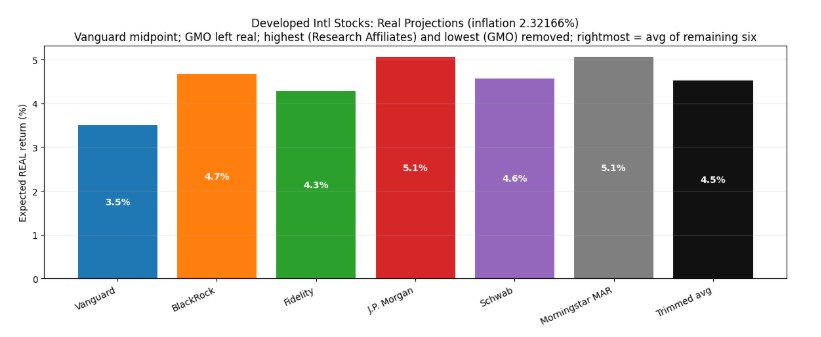

Fig. 6. Medium-to-long-term real average annual market return projections for developed-market stocks, using the mid-point for Vanguard’s projections and removing the highest and lowest “outlier” projections to arrive at a “trimmed average” projection given by the right-most, black bar (graphic created with ChatGPT).

The spread between the second lowest and second highest projected real returns is much smaller for developed market stocks, between 3.5% and 5.1%. The second highest is only 46% greater than the second-lowest projection. This suggests to me that this asset class’s eventual real returns may end up closer to the trimmed average number of 4.5% than will be the case with US stocks.

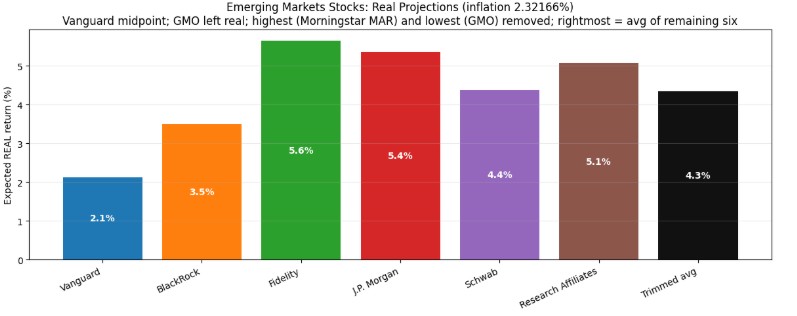

Fig. 7. Medium-to-long-term real average annual market return projections for emerging-market stocks, using the mid-point for Vanguard’s projections and removing the highest and lowest “outlier” projections to arrive at a “trimmed average” projection given by the right-most, black bar (graphic created with ChatGPT).

Emerging market stock real return projections aren’t as widely spread as those of US stocks, but are more spread out than the numbers for developed markets. They vary from 2.1% to 2.7× higher, 5.6%. Thus, I expect the eventual return may stray from the 4.3% trimmed average more than will be the case for developed markets but less than for US stocks.

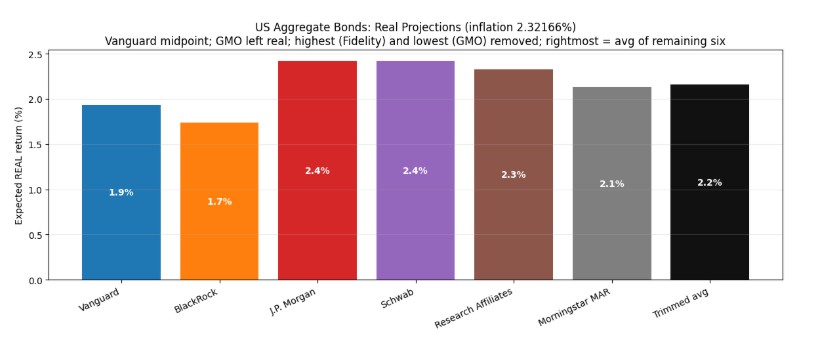

Fig. 8. Medium-to-long-term real average annual market return projections for US bonds, using the mid-point for Vanguard’s projections and removing the highest and lowest “outlier” projections to arrive at a “trimmed average” projection given by the right-most, black bar (graphic created with ChatGPT).

Here, the projected real returns vary from a second lowest 1.7% to a second highest 2.4%, just 41% higher. This suggests that the eventual bond return may stray from the trimmed average of 2.2% by the smallest amount, compared to the three stock asset classes.

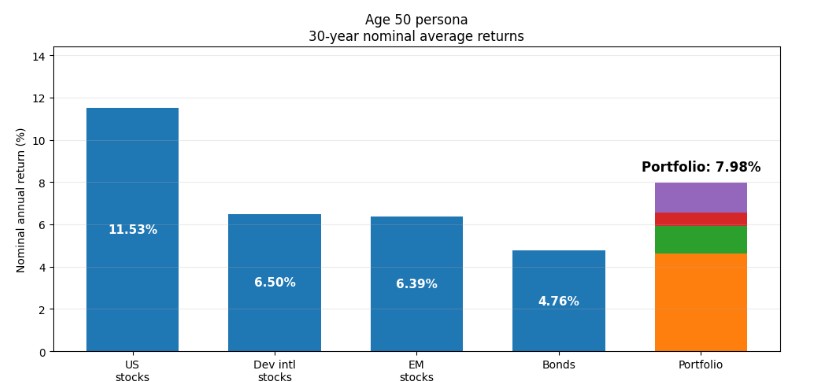

To see how this may affect people’s investment results, let’s consider three hypothetical investors: