The July 2025 signing of the new tax and spending law, H.R.1 One Big Beautiful Bill Act (OBBBA), preserved key elements of the 2017 Tax Cuts and Jobs Act (TCJA), as well as introduce many new tax policies. The bill has more than 800 pages (see final text), many provisions of which do not pertain to individual income taxes, therefore this article will attempt to highlight those that impact high-net-worth individuals.

Income Tax Rates

OBBBA permanently extended the reduced tax rates enacted by the TCJA, and all brackets continue to be indexed for inflation after 2025. The provision adds an additional year of inflation adjustment to the end of the 10% and 12% brackets (where the 22% bracket begins). This means that most taxpayers effective tax rates, the total percentage amount of tax paid on income, is slightly reduced because of being taxed a little bit more at the 10% and 12% rates and a little bit less at the higher rates. (Section 70101)

Standard Deduction

The increased standard deduction created by the TCJA is now permanent and annually adjusts it for inflation. For the 2025 tax year, the standard deduction was modestly increased to $15,750 for individual filers/$31,500 for joint filers. (Section 70102)

Itemized Deduction Limit for Top-Bracket Taxpayers

The new limitation only applies to high-income taxpayers in the top 37% tax bracket, which reduces allowable itemized deductions by 2/37 of the lesser of:

The taxpayer’s total itemized deductions; or

The amount by which their taxable income plus total itemized deductions exceeds the 37% bracket threshold (before applying the limitation).

(Section 70111)

SALT (State & Local Taxes) Deduction Cap

Effective 2025, the state and local tax (SALT) maximum deduction increases from $10,000 to $40,000, and increases 1% each year through 2029, however it phases out when modified adjusted gross income (MAGI) exceeds $500,000, which brings it back to $10,000 max. (Section 70120)

AMT (Alternative Minimum Tax) Exemption Phaseout Thresholds Reduced

Beginning 2026, the law includes changes that slightly increase AMT exposure. The AMT exemption phaseout thresholds will permanently revert to their 2018 levels ($500,000 single / $1 million joint filers), indexed for inflation thereafter. However, when the taxpayer’s AMT income exceeds the threshold amount, OBBBA doubled the AMT exemption phaseout rate from 25% to 50%. Which means once you reach that AMT income where the exemption begins to phase out, the taxpayer will be taxed at 1.5 times the AMT tax rate of 28%, which translates to a 42% marginal rate in that range. (Section 70107)

Increased Estate and Gift Tax Exemption

OBBBA permanently extends the estate and lifetime gift tax exemption and beginning in 2026, increases the amount to $15 million per person ($30 million for married filing jointly), indexed for inflation. For high-net-worth individuals, this is particularly good news as the exemption amount was set to be cut in half. As a result, this provides an opportunity to transfer significantly more wealth without incurring federal estate or gift taxes. (Section 70106)

Charitable Contributions

For taxpayers who make qualified charitable donations, the new provision imposes a limit on donations for those who itemize, so they will not get their full benefit. Donors who list their charitable gifts on Schedule A will forego an amount equal to 0.5% of their adjusted gross income (AGI). For example, someone with $400,000 of AGI would receive no deduction for the first $2,000 of charitable donations. In addition, top-bracket taxpayers will only be able to take their itemized deduction at 35%, not 37%. An important note is the disallowance is a fixed amount for each year.

High-income taxpayers, particularly those who will regain the benefit from the expanded SALT deduction that begins in 2025, may want to accelerate contributions to maximize their charitable tax breaks, as the new law will not go into effect until the 2026 tax year. One consideration is to implement a donor-advised fund (DAF), which would allow a giver to contribute a large amount to receive the full deduction in 2025, and distribute smaller gifts from the account over time. Another idea is to implement “bunching” of charitable donations, which means you make one large donation in a single year instead of donations spread over several years. For example, let’s say you typically donate $30,000 per year, so consider donating $150,000 in 2025, qualifying for a larger itemized deduction in 2025. (Section 70425)

New Eligible 529 Plan Expenses

Beginning in 2026, qualified expenses for 529 education savings plans will be expanded to include more K-12 and homeschool expenses, such as curriculum, books and instruction materials, tutoring costs as long as it’s someone outside the home and not a relative, standardized testing fees, college enrollment fees, and post-secondary credentialing expenses. (Sections 70413 and 70414)

Conclusion

The new tax and spending law effectively serves as a replacement of the Tax Cuts & Jobs Act of 2017, with some referring to it as ‘TCJA 2.0’. Provisions either permanently or temporarily extended aspects of the tax code, which helped make it easier to plan multi-year strategies, but ultimately it is not as radical a tax overhaul as we saw in 1986 and 2017.

OBBBA’s overall effect on high-net-worth individuals is more nuanced than the headlines suggested, but certainly the permanence of reduced income tax rates, expanded SALT deduction (at least for those under the $500,000 MAGI phaseout), and a larger estate and gift tax exemption are clear wins, offering opportunities to lock in long-term tax efficiencies. However, the law also includes targeted limitations designed to quietly raise revenue from top earners. The new itemized deduction cap for the 37% bracket, tighter AMT phaseout rules, and charitable contribution restrictions beginning in 2026 will erode some of the political fanfare. For those with significant exposure to these changes, the net impact may be modestly negative, particularly if they are already near or above the new income thresholds.

The key takeaway is that the difference between benefiting and losing under these rules will often come down to timing: making strategic moves in 2025 and structuring income, deductions, and gifts to align with the most favorable years. For high-net-worth households, this is a moment to revisit tax, estate, and charitable plans to ensure the law’s changes work for and not against them.

Find financial advisors in College Station, Texas ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in College Station for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in College Station featured on Wealthtender you may want to add to your shortlist.

Featured College Station Financial Advisors

As you prepare to interview financial advisors in College Station who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Advisors Who Serve Clients in College Station

These advisors can meet with you in person in College Station.

The Benefits of Hiring a Financial Advisor in College Station

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in College Station, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in College Station? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an College Station Financial Advisor

Before hiring a financial advisor in College Station, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

[The creation rate of ETFs has demonstrated great industry and investor interest signaling rapidly expanding growth and innovation. The U.S. has led this accelerating charge with 746 new ETFs launches in 2024 and 481 launches in the first half of 2025.

Fueling this growing movement has been new ETF participation from active investment managers, alternatives going mainstream, advisors running model portfolios, and family offices. Also adding to the rising momentum is a more modernized turnkey process into this marketplace through time- and cost-efficient platform launch capabilities that help new ETF sponsors gain entry with a speed-to-market approach.

To better understand the mechanics of ETF creation and how you can launch your own ETF, we were introduced to J. Garrett Stevens, Chief Executive Officer of Exchange Traded Concepts – an SEC registered investment adviser that created the first white-label ETF firm in the world specializing in helping new ETF sponsors create, launch, and manage custom ETF vehicles as a turnkey solution.

We asked him questions to learn more about his ETF-IN-A-BOXTM launch solution and how financial firms can participate strategically in the continued growth and diversification of the ETF marketplace.]

Hortz: What motivated you back in 2011, in the still early days of ETFs, to launch the first white-label ETF platform?

Stevens: My motivation for launching a white-label ETF platform came from my personal experience launching my own family of ETFs. We made our initial filings in 2008, and what we learned was that it took twice as long and cost twice as much as it was supposed to in getting those first ETFs to market. That process was extremely painful. We put all the infrastructure in place – built our own trust, our own board of directors/trustees, engaged all the service providers, and paid lawyers nearly a million dollars just to get all the legal filings done.

The pivotal moment was when we were closing three of our ultimately unsuccessful ETFs, I actually got several phone calls from people saying, ‘Hey, we want to buy you. We just want to take advantage of the SEC exemptive relief application process and your place in line. You already have the infrastructure fully built out. We want to launch our own ETFs, but we do not want to wait a year.'”

That is really where the white label idea came to me. Since we already had everybody and everything structurally in place, why don’t we help other people launch their funds? So, we essentially turned our ETF experience into a service business that can help other ETF sponsors avoid the painful, expensive, and time-consuming process we have experienced and be able to leverage the infrastructure we already had built to create a more efficient path to market for new ETF issuers.

Hortz: Can you review what are the major component functions behind creating and launching an ETF that new sponsors need to plan for?

Stevens: The major ETF component functions of launching an ETF include:

Legal and Regulatory – you need attorneys doing filings for the ETFs, the ongoing reporting, and compliance.

Board of Trustees – you are required under the 40 Act to have an independent board of trustees.

Trading and Portfolio Management – the infrastructure and team of traders and portfolio managers that will actually do all of the trading in the funds.

Regulatory Requirements – you have to have a liquidity risk management program, and if you have derivatives, you have to have a derivative risk management program. Everything has to be filed with FINRA. Your distributor has to review it and approve it before you can use it.

Custom Basket Process – the custom basket process makes ETFs tax efficient. Most firms have no idea how to do that process.

Marketing and Distribution Considerations – once you get into the 40 Act world, it is a whole other can of worms from a regulatory perspective and what you can and cannot say. Distribution is a complex process that a lot of people do not fully understand or get confused with what strategy to pursue.

Many firms underestimate the complexity of these components, particularly the custom basket process and regulatory requirements unique to ETFs.

Hortz: How and to what extent does a turnkey platform approach ring out time and expenses from launching an ETF?

Stevens: The main benefit of a turnkey approach is offering an already pre-built comprehensive ETF infrastructure where the organizational work is all done, essentially eliminating the lengthy setup process required when starting from scratch. This results in game-changing, dramatically faster launch timelines.

To illustrate this, when you come to launch an ETF on our platform, we can draft your prospectus in about two weeks, and get it filed with the SEC, which has a 75-day review period. That means we can have you ready to go in 90 to 100 days to full launch of your ETF. If you do that on your own, it is going to take six months to a year to get all that done.

As to cost savings, a platform can leverage and negotiate wide-spread cost reductions through its economies of scale representing its collective client base. In our case, we have over 110 ETFs that we advise or sub-advise right now that represents about $15.5 billion in Assets Under Management (UAM). So, we get favorable pricing from the various service providers, much less than if individual ETF sponsors negotiated on their own. We are also able to spread costs across all funds which means our clients are paying a fraction of the organizational costs, instead of all of them.

Also, having an experienced independent board made up of a wide range of ETF professionals with specialized knowledge that understand ETFs, how they work, and the lay of the land of ETF vendors and needed specialty services, is another key factor in reducing costs, accelerating speed to market, and delivering expertise and quality to the platform and our ETF sponsor clients. It is not that easy to find board members who have been in the ETF world for a long time.

For all the reasons mentioned above, that is why a turnkey approach provides such significant value.

Hortz: Besides creating & launching an ETF product, can you explain your ongoing portfolio management services?

Stevens: We decided to offer ongoing ETF portfolio management services since we saw that many traditional investment firms lack the experience and expertise with ETF-specific investment processes, like custom baskets, which are critical for maintaining tax efficiency.

We can also act in a sub-advisory role, we have a trading desk with a team of traders and portfolio managers that can do all of the trading in the funds for our clients, we can do the custom basket process, as well as index tracking, rebalances, security selection support, and tax efficiency management.

Hortz: What are some of the major misconceptions or inaccurate assumptions that some investment/asset managers have about launching ETFs that they should be aware of?

Stevens: There seems to be a persistent series of key misconceptions that investment and asset managers have about launching ETFs that relate to the regulatory environment, marketing limitations, and the reality of building a successful ETF in today’s crowded marketplace. These include:

“If You Build It, They Will Come”Mentality – One of the biggest misconceptions out there is that there is a ready market waiting to take advantage of your ETF investment opportunity. We have to remind people all the time that this is not that kind of an industry or marketplace like the early ETF days. We now have over 4,500 ETFs out there and we are in the midst of an ETF explosion of new launches.

Launch Day is Just the Beginning – With all the work that goes into launching the ETF, many get excited on that first trade date and look at that as the finish line, but they need to realize that is only the starting line…. That is when the hard work really begins.

Distribution and Marketing Challenges – The hard work of sales, marketing, and distribution of ETFs has its own dynamics and challenges that a lot of sponsors new to this marketplace do not fully understand or get confused about.

Wirehouse Approval Process – For new ETF sponsors, you should not count on the big wirehouses as a key part of your initial strategy as they have high asset minimums and track record requirements before they will even start the due diligence. They are likely not going to approve your ETF for years.

Because of these continuing misconceptions and others, we set up ETC Marketing Services to offer personalized marketing and distribution services to help more strategically raise the profile, visibility, and engagement for your ETF products.

Hortz: What are the most meaningful ETF trends you have been seeing from your vantage point?

Stevens: I think the major shift that has happened is from ETF Index Funds to Custom ETF Strategies to mirror existing active strategies. When we first got into this business, it was mostly index funds. They proliferated around new indices and ideas for a theme, whether it was on trends, robotics, country/regional/industry focuses, you name it, there was and continues to be endless variations being created.

The current propulsion of new ETF creation is being driven to some extent by active investment managers creating tax efficient versions of their existing strategies offering clients the option of putting their taxable money in the ETF and the non-taxable money in the SMA account. Advisors running model portfolios are also creating ETF versions because anytime they make portfolio changes in their model, currently they are creating taxable events, and it does not generate any, or at least minimal capital gains in the ETF investment vehicle.

New market participants we see increasingly launching ETFs are family offices and hedge funds. The latter because of their frustrations in not being able to market their hedge funds due to sophisticated investor rules. They are realizing they can do their active strategy or a light version strategy in an ETF.

An interesting trend I am seeing emerge is a new focus on client-specific ETF products rather than the mass market. If you can get $30-$40 million in an ETF, it is breakeven, covering its own expenses, and so then you can build and offer the ETF vehicle specifically for your clients. I think you are going to continue to see this trend expand of advisors building custom ETF products just for their client base or demographic.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

Most wealthy Americans work with a financial advisor. In fact, over 76% of people with at least $500,000 in investable assets report working with one. Advisors focus on planning strategies to achieve their long-term financial goals, from legacy and succession planning to philanthropy, allowing high-net-worth individuals to focus on their family, career, and enjoying life while delegating wealth management to professionals.

Have you ever thought about hiring a financial advisor? According to a 2025 Wealthtender study of 500 U.S. adults with household incomes over $100,000, it’s clear that many Americans believe that hiring a financial advisor is a smart move to achieve their long-term goals and aspirations for a comfortable retirement.

If you have a significant net worth, you’ve almost certainly received solicitations from financial advisors looking to sell you their services. I typically receive such letters, often inviting my wife and me to a free dinner at a nearby Ruth’s Chris Steak House. Should we go, we’d doubtless have to sit through a long presentation trying to convince us to hire them.

But should we?

What Is a Financial Advisor?

Before we continue, let’s start by defining “Financial advisor”. “Financial advisor” is a very broad term.

I looked through a (fairly random) list of about 170 financial advisors and found 40 titles (some pros listed multiple titles).

Just for grins, here they all are (feel free to jump past the whole list!)

Accredited Asset Management Specialist (AAMS)

Accredited Financial Counselor (AFC®)

Accredited Investment Fiduciary(AIF®)

Accredited Investment Fiduciary Analyst (AIFA®)

Accredited Wealth Management Advisor (AWMA®)

Behavioral Financial Advisor (BFA®)

Certified Digital Asset Advisor (CDAA®)

Certified Divorce Financial Analyst (CDFA®)

Certified Elder Law Attorney (CELA®)

Certified Exit Planning Advisor (CEPA®)

Certified Financial Education Instructor (CFEI®)

Certified Financial Planner (CFP®)

Certified Financial Therapist (CFT-I®)

Certified Investment Management Analyst (CIMA®)

Certified Kingdom Advisor (CKA®)

Certified Private Wealth Advisor (CPWA®)

Certified Public Accountant (CPA)

Certified Retirement Counselor(CRC®)

Certified Student Loan Professional (CSLP®)

Certified Wealth Strategist (CWS®)

Chartered Alternative Investment Analyst (CAIA®)

Chartered Financial Analyst (CFA®)

Chartered Financial Consultant (ChFC®)

Chartered Life Underwriter (CLU®)

Chartered Retirement Planning Counselor (CRPC®)

Chartered SRI Counselor (CSRIC®, where SRI is sustainable, responsible, and impact investing)

Enrolled Agent (EA)

Financial Solutions Advisor (FSA®)

Master of Business Administration (MBA)

Master of Science in Financial Planning (MSFP®)

Master of Science in Personal Financial Planning (MSPFP®)

Master of Science in Taxation (MST®)

Master Planner Advanced Studies (MSAPTM)

Military Qualified Financial Planner (MQFP®)

Personal Financial Specialist (PFS®)

Registered Financial Consultant (RFC®)

Registered Investment Advisor (RIA®)

Registered Life Planner (RLP®)

Retirement Income Certified Professional (RICP®)

Wealth Management Certified Professional (WMCP®)

Each of these implies a different education, training, and/or focus.

Some are academic degrees, while others are professional certifications.

Some take years to acquire, while others can be attained through short programs.

Some get paid by the hour, others by the type of service, and yet others by commissions and/or assets-under-management fees. Some even charge a combination of the above.

Some require the professional to be a fiduciary – putting their client’s best interest ahead of their own, while others don’t (though this doesn’t preclude them from acting with professional integrity).

Image Credit: Depositphotos.

What Do Financial Advisors Do for You?

In the broadest terms, a financial advisor will help you manage some, most, and potentially all aspects of your money. Some examples include:

A recent survey conducted online by Logica Research for First Citizens Bank asked 1000 Americans with at least $500k investable assets (putting them in the 79thnet worth percentile or higher) various questions, including several about working with financial advisors.

Of the 1000 surveyed, 764 (over 76 percent) said they worked with a financial advisor.

The answer is thus “Yes” much more often than “No.”

Of those 764, 89 percent believe their advisor helped them grow their wealth faster than they would have on their own.

Only three percent disagreed with that (the rest had no opinion).

In my case, the answer is also yes, because I work with an accountant.

What Are the Biggest Benefits of Working with an Advisor?

Asking the 764 who work with advisors what were the biggest benefits they derived, they answered:

Feeling better prepared for the future (66 percent)

Reducing stress (58 percent)

Saving time (45 percent)

Allowing them to focus on the important things in their life (43 percent)

Having a plan for passing on wealth to heirs (29 percent)

Not worrying about what happens when they die (15 percent)

Not worrying about taxes (12 percent)

Of all these, if I ever hire a CFP, for example, feeling better prepared would rank highest for me, followed by not worrying about taxes.

I’m too much of a detail-oriented-to the-nth-degree control freak to ever feel less stress or not worry if I handed our investment management and other financial planning matters to someone else.

I’d likely duplicate their work and if my conclusions were different from theirs, they’d better have a pretty darn compelling case!

What’s the Most Important Criterion When Picking an Advisor?

All 1000 were asked what they thought would be the most important thing to consider when choosing an advisor. Their answers were:

Reputation (52 percent)

Credentials/Certifications (48 percent)

Fee structure (47 percent)

Transparency (43 percent)

Recommended by trusted people (33 percent)

Confidentiality (25 percent)

Personability (24 percent)

Philosophical alignment (19 percent)

Why They Hired an Advisor

Those 764 who work with an advisor stated several reasons that led them to hire their advisor:

Growing wealth (41 percent)

Preparing for retirement (23 percent)

Creating a financial plan (23 percent)

Managing taxes (6 percent)

Building an inheritance (6 percent)

Personally, I’d rank them differently: transparency in the top slot, philosophical alignment, personability, reputation (especially among people I know who have similar financial circumstances), confidentiality, credentials, and fee structure.

When Did They Hire Their Advisor?

Those who work with an advisor first hired their advisor when they were, on average, 37 years old. There was some differentiation between generations – the 251 Millennials averaged age 29, the 208 Gen-Xers averaged age 36, and the 158 Boomers averaged age 43.

All 1000 were then asked what age they thought would be best to start working with an advisor. The most common answer was “Any age” at 38 percent. Another 32 percent recommend ages 26 to 40. The age range up to 25 was suggested by 26 percent. The remaining four percent thought the proper time would be at age 41 or older.

The overall average recommended age was 30.

Looking From the Other Side

I thought it would be interesting to see this from the perspective of financial advisors.

So, I asked them.

The following are my questions and answers from several financial advisors.

Q1. In your experience, why do the wealthy use financial advisors?

Answers:

Chris Wilbratte, Echelon Financial responds, “The wealthy use financial advisors because they focus on their area of genius and delegate wealth management to advisors who are subject matter experts in their field. The wealthy want to be good stewards of their money. They often don’t have the time to focus on the markets and managing their money, so they hire advisors to ensure their money grows and is protected.”

Vincent D’Eletto, COO at Investment Insight Wealth Management points out, “Affluent Americans do use financial advisors, but their approach is often distinct from those who are still working toward financial independence. While many may seek advice on investments and retirement planning, affluent individuals tend to focus on more complex goals. These include philanthropy, managing multi-generational wealth, establishing succession plans, and fulfilling altruistic aims. For them, it’s not just about growing their assets but ensuring that their wealth aligns with their values and legacy for future generations. They seek a broader, more strategic approach that covers a wide range of financial and personal objectives.”

He continues with an example, “We’re currently working with a long-term affluent client who has already achieved financial independence. At this stage, the focus has shifted from traditional wealth building to establishing a philanthropic foundation that his family can oversee for generations. What’s particularly interesting is that he wants to remain actively involved in the investment decisions for the fund, so we’re creating a structure that allows him to guide the investment strategy while maintaining the foundation’s long-term objectives. This type of goal reflects how affluent clients often prioritize legacy planning and the integration of personal values into their financial strategies.”

Ray Prospero, Partner Advisor, AdvicePeriod agrees, “I’ve found that affluent investors choose to use a financial advisor because they tend to lead busy lives and prefer to delegate their financial management to a professional. By doing this, they are free to focus on their other priorities such as their career, family, and hobbies. Additionally, depending on the complexity of their finances, they can use the specialized expertise of their advisor to address areas such as tax planning and estate planning.”

Chris Magaña, Strategic Advisor & Principal, IMS Capital Management shares an interesting experience, “Our clients are incredibly sharp; they hire us because they know their time is better spent elsewhere, like growing their business, spending time with family, or diving into their passions. Lately, though, we’ve been attracting a different breed: business owners by day and hedge fund managers by night (or so I suspect). Their financial IQs are off the charts, and they genuinely enjoy digging into market details and Roth conversions. At first, I felt a little insecure; I didn’t believe our value proposition was strong enough for these clients, so I asked. Their responses surprised me. They said, ‘Sure, I love this stuff, but I won’t be around forever. What I need is peace of mind, knowing there’s a team I trust implicitly once I am gone.’ These folks know something about the meaning of true wealth, building a legacy with people you trust.”

Q2. What services do advisors offer beyond those listed above?

Answers:

Carman Kubanda, CFP®, ChFC®, Financial Planner at Innovative Wealth Building mentions one such service, “Good advisors are now incorporating tax planning into their routine services. Tax considerations are broad, and include, e.g., tax-loss harvesting strategies, Roth conversions, and even ‘I’m buying a new car what account should I pull from?’”

Jen Swindler, CFP®, CDFA®, AFC®, Owner & Advisor at Money Illustrated elaborates, “When doing consultation calls with prospects, I often tell people that hiring an advisor is not a net-worth-driven decision, but more of a feeling. For example, you may have reached a point where you don’t feel like you can manage their finances fully on your own due to lack of sufficient time, interest, or knowledge; they have an awareness of their gaps in knowledge and feel they’re missing financial opportunities; you feel a sense of financial overwhelm and don’t know where to start. Because so many advisors today offer planning options where an asset minimum isn’t required, it’s become much more approachable to the mass affluent. If you’re experiencing financial overwhelm, searching for an advisor who offers what you need at a price you can afford is much more doable.”

She then lists several lower-cost or free options, “Many people assume that financial advisors are primarily for asset management, but today, many advisors offer behavioral coaching, budgeting, debt management planning, student loan analysis, and advising while you’re building wealth. If you’re in a situation where you’re struggling to pay bills, are taking on debt to make ends meet, and can’t afford a financial advisor’s fees, an AFC®, qualified financial coach, or free counseling center would likely be better options. Looking for an AFC® through a program like AFCPE is a great place to start.”

Stephan Shipe, Ph.D., CFA, CFP®, CEO, Financial Advisor, Scholar Financial Advising says, “Tax strategy and efficiency are important considerations for wealthy clients. Many wealthy clients require advice on non-financial market assets such as real estate, alternative investments, or closely held businesses. Legacy goals also include the advisor helping prepare family members for inherited wealth.”

Q3. What is the profile of the ideal client for an advisor?

Answers:

Kubanda says, “An ideal client would be responsive and willing to listen to the advice they’re given.”

Omen Quelvog, MQFP®, Financial Advisor with Clear Insight Wealth Management offers an interesting take on this, saying, “The classic answer to matching an ideal client to an advisor is, ‘It depends.’ That’s the beauty of the financial advising profession. As a client with a need, their ideal advisor is often related to the client’s profession or background. Whether a doctor, military veteran, business owner, farmer, etc., each profession has nuanced benefits an advisor would be expected to know to be deemed competent and trusted. The most advantageous service offered that is difficult to articulate in any marketing campaign, is the intangible benefits of an unemotional third party assessing your overall financial health. With that assessment comes the provision of permission, assurance, and comfort, knowing you have a trusted resource in your corner.”

Lawrence D. Sprung, CFP®, Founder, Wealth Advisor at Mitlin Financial shares his take, “When starting with a financial advisor the fit should be high on your list. If there’s no fit, there’s no relationship. What I mean by this is that you want to be sure the challenges and goals you are looking to work through with the advisor are things they have experience helping other families work through too. If the advisor has little or no experience in the areas where you want help, that advisor will not be a good fit. Our firm will not move forward with a family unless we feel confident that we can assist them through the opportunities and challenges they face. This allows us to build long-term meaningful relationships with the family and ensure we do not create a situation where we over-promise and under-deliver. We prefer to under-promise and over-deliver.”

David Nash, CFP®, founder of Tend Wealth says, “The ideal client for a financial advisor is someone who values saving time and achieving peace of mind, particularly as their income and wealth grow. Small mistakes or missed opportunities can have compounding effects, leading to more significant issues down the road. A good advisor is patient and available to explain your options, helping you make more informed decisions about the trade-offs involved in various tax-saving and investment strategies. Even W-2 employees with high earnings can benefit from working with an advisor who applies a tax-sensitive investment approach. Effective tax planning around retirement contributions and withdrawals, spanning both their working and retirement years, can result in significant tax savings over time.”

Matthew R. Pogirski, CFP®, AAMS™, founder of Unburdened Financial Planning offers a more spiritual approach, “Our ideal client is someone who knows that peace is not found in possessions or things. Peace is found in knowing and being known. As a Christian, this starts with a relationship with Jesus, but also our relationship with ourselves and others. Our ideal client knows they are not at peace but need help in achieving peace by being known and having a plan that helps them realize who they truly are.”

Q4. Who should not hire an advisor?

Answers:

Pogirski is clear on this, “Someone who is trying to beat the market, buy a hot stock, or pursue quick gain as their goal in life is not a good fit for us as advisors.”

Nash agrees and cautions, “You shouldn’t hire an advisor if you expect them to help you get rich quickly through exclusive investments unavailable to you otherwise. Some advisors may try to promote their ‘proprietary’ approach or sell you complex investment products that often come with higher fees or commissions. It’s easy for advisors to make promises and then take unnecessary risks with your money, hoping for positive outcomes.”

Q5. What should a client expect when starting to work with an advisor?

Kubanda says, “When starting to work with an advisor, you should expect to dive into all matters financial and familial. The more information your advisor has, the better they can guide you and help you reach your goals.”

Pogirski agrees, “A new client should expect their advisor to take time, a lot of time, to get to know them. To understand who they are. This involves asking deep questions about how they feel about money.”

Nash expands, “When starting with a financial advisor, you should expect a series of meetings to review your current financial situation and explore your short-term and long-term financial goals. During this process, the advisor will gather all the necessary information to create a personalized financial roadmap that guides you from where you are to where you want to be. While the initial process might feel intense, once it’s complete, the advisor can alleviate much of the burden, offering you sound financial guidance and a clear path forward.”

Magaña gives his take, “A great advisor sets clear expectations from the jump. Their focus should be helping clients master what’s within their control, like tax efficiency, smart diversification, strategic gifting, and proper asset allocation. A great advisor shouldn’t waste time obsessing over what’s beyond your control, like short-term market wiggles, inflation spikes, or today’s panic-inducing market headlines. That’s why capitalism gave us the Wall Street Journal and the Financial Times.”

Is a Financial Advisor Right for All Wealthy Americans?

Not everyone will need a financial advisor.

If your only income is from W2 wages, your tax returns are likely so simple that preparing your returns with the help of tax prep software would be quick, easy, and just as good as what you’d get by paying a CPA much more than the cost of the software.

If your investing philosophy is that low-cost index ETFs are all you need since you don’t believe active investing can beat the market over the long haul, why would you want to pay an investment manager?

However, if your financial situation is complex, if you want to try and beat the market over years and decades (a tall order), or if you have a significant net worth and want to protect that wealth, hiring a financial advisor of one sort or another (or several different professionals) would be very helpful.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Whether you’re a foreign national living in the US with a green card or working on a non-immigrant visa (H-1B, TN, E-3, O-1, L-1, H-1B1), you have unique needs when it comes to financial planning. If you’re on a path toward US citizenship or planning to return to your home country, the financial decisions you make today can have a significant impact on your financial future.

It can feel overwhelming for immigrants to try and navigate the complexities of the US tax system, not to mention making sense of the numerous retirement and savings accounts and their potential tax benefits. Beyond taxes, understanding how to make the most of your employee benefits, saving for retirement, and funding your children’s education are additional priorities that can take a lot of time to figure out on your own.

Fortunately, there are financial advisors who have walked in your shoes and know what it’s like to arrive in the United States feeling confused and unsure about money matters. By hiring a financial advisor who specializes in working with immigrants and foreign nationals, you’ll feel more confident knowing you can ask questions and get answers that other advisors simply wouldn’t know or understand.

It’s easier today than ever before to find a specialist financial advisor dedicated to working with immigrants and foreign nationals in the US. Beyond researching financial advisors in your neighborhood, which could significantly limit your access to specialists, you may find the best financial advisor for you lives several states away and is easy to work with virtually, often via Zoom online meetings, for example.

So is a financial advisor who specializes in serving immigrants right for you?

Let’s learn more by getting answers from financial advisors featured on Wealthtender who offer their perspectives on the potential benefits of working with a specialist for immigrants.

👩💼 Get to Know Financial Advisors Who Specialize in Serving Immigrants

This page is organized into sections to help you quickly find the information you need and get answers to your questions:

Q&A with Financial Advisors Who Specialize in Serving Immigrants

Get Answers to Your Questions About Financial Planning for Immigrants

Browse Related Articles

– Financial Advisors Who Specialize in Serving Immigrants –

We asked Austin-based financial advisor Jane Mepham to answer three questions she often hears from the immigrants she serves when helping them develop a financial plan for their future.

Q: I’m currently in the US on a work visa. Why should I consider hiring a financial advisor in the US?

Jane: The US financial system is complex and can be very confusing to somebody new to the country. A good financial advisor is invaluable, as they can guide you not only in setting yourself up financially but also in helping you prioritize competing financial needs. You are going to have a lot of questions, especially in the first year: for example, setting up a budget (which might include supporting your family overseas), choosing the right kind of retirement plan (critical especially when you don’t know where you are going to retire), health, life (not every company will agree to insure you), or disability insurance. A financial advisor can easily guide you through these issues.

One of the most significant issues you are likely to face is the tax implications of being a US person, keeping in mind that the US taxes you on worldwide income and your immigration status. You’ll need to figure out if you should be filing taxes as a tax resident or non-resident.

Additionally, you may have reporting requirements if you hold overseas accounts, due to the FBAR and FATCA filing requirements. At this juncture, a financial advisor becomes critical, as they can help you figure out these issues. Picking the right advisor and working with them over a couple of years may prove to be the best decision you’ll make in your life in the US.

Here are some resources that may answer some of your questions as you begin your work visa journey in the U.S.

Q: What should I consider before participating in my US employer’s 401 (k) plan?

Jane: The 401 (k) plan is a retirement plan offered by many US employers. Every employee, including those on work visas, is eligible to participate. Different companies have different waiting periods. Here are some things to consider before participating:

Regardless of how long you intend to stay in the country (work visas are not permanent), contributing to the 401 (k) plan reduces your taxable income, meaning you get to pay lower taxes now.

Typically, we’d recommend maxing out the plan. In 2025, you can invest up to $23,500 if you are under the age of 50. Over 50, you can add $7,500 (catch-up contributions), and if between 60 and 63, your catch-up contribution is $11,250. If you’re unsure about being able to max it out, consider whether your company offers a match and plan to save up to that amount to receive the free money (employer match).

The goal is to take advantage of compound interest and keep your money in the market for an extended period.

If your company offers a Roth 401 (k), or a mega backdoor Roth IRA, tread lightly. This is because many countries do not recognize the tax-free nature of the account, and therefore, if you leave the US with the account, they may end up taxing these accounts. A good conversation to have with your advisor.

Another thing to consider are the investment options offered in the plan. If there are life-strategy or target-date funds, those are the easiest ones to start with. If the investment options are below par, again consider saving up to the employer match.

Q: If I’m planning for my children to attend college in the US, what’s the best way for me to save for their education?

Jane: Immigrants tend to value education greatly, and they are willing to do whatever it takes to help their kids attend the best schools. To accomplish this goal, start saving for college as soon as possible. There are several ways to do this, and each has its own advantages and disadvantages.

529 plan – This is a government-provided plan specific to education and, in this case, college. The money goes in after taxes, grows tax-free, and comes out tax-free if it’s used for education-related expenses.

Every state has its own plan and most of them will allow non-residents to open a plan there. There are about six states that don’t allow outsiders into their plan. In terms of location, if your state offers a tax break (deduction or tax credit), then it makes sense to consider opening a plan in that state.

Finally, please note that the beneficiary must be a citizen or a permanent resident to utilize the funds in the plan. If the intended beneficiary is not yet a citizen, you can open the account with yourself as the beneficiary and change it later to the children when they become citizens or permanent residents.

There are schools outside the US that honor the accounts, so if you end up leaving before your kids have a chance to use the funds, this is a possibility.

The latest tax bill OBBBA signed this year (2025) has expanded the list of expenses that the 529 plan can fund.

If you end up not using the money for education-related expenses, you’ll pay taxes and a 10% penalty fee on the earnings. Here is a blog post that answers a question I see come up a lot in this space about opening a 529 plan if on a work visa.

Roth IRA Account – We typically think of this as a retirement account, but it can also be used for saving for college. Your income must be below a certain threshold to open the account, but with the backdoor Roth option, the income threshold is no longer an issue. But keep in mind the issue discussed above about how your home country may treat this account if you end up leaving the US at some point.

In 2025, the max that can be put into the account is $7,000 ($8,000 if over 50). Ideally, both parents should open separate accounts. The initial contribution can be withdrawn anytime, penalty-free, for education-related expenses while allowing the earnings to continue growing for retirement. If you withdraw the earnings for college expenses, the 10% penalty does not apply; however, you will still pay taxes on that amount.

At age 59 and ½, the earnings can also be withdrawn tax-free and penalty-free to pay for college expenses.

Brokerage Account – There are no tax advantages to this account, but it gives you a lot of freedom in what you do with the money, how you invest it, etc. If the funds are held in the account for more than a year, you’ll pay capital gains taxes, which are lower than ordinary income tax. It’s the most flexible account for those who are not sure where they’ll be over the next couple of years.

In applying for college aid, the account is included as the parents’ assets.

Custodial Accounts – The two main accounts in this space are UGMA (Uniform Gift to Minors Act) and UTMA (Uniform Transfer to Minors Act). Keep in mind that even though you are the account owner, the child legally owns the money in the account. They gain control of the account when they reach the legal age as defined by the state. It’s a great way to start gifting kids’ money early on in life, but consider that at the legal age, they may choose not to use the account for college education, and there is nothing you can do about it. It’s considered a child’s asset for college funding considerations.

Coverdell Education Savings Accounts (ESA) – This account is very similar to a 529 plan, but is limited in how much you can contribute. You can save up to $2,000 per year, per beneficiary, and use it only if your income is below $110,000 ($220,000 if married).

All the above plans can be combined to create something ideal for each family, depending on their unique situation. A financial advisor can help you pick the best plan, keeping in mind your immigration status, your income, your needs, and other issues specific to your family.

Question: Besides the retirement and college funds, what else should I be thinking about as a foreign national in the US?

There are a couple of other areas you want to consider and take care of before you can sit back and relax.

Emergency Fund: Plan to have 12 months of living expenses plus the cost of a return ticket for the family. It’s even more critical for foreign nationals on work visas, where losing your job can cause you to have to leave the country in a rush.

Estate Planning: Ensure your US estate plan is complete, especially if you have young children. You can have international guardians (especially if your family is overseas), but this may be based on your state. In such cases, you may need to have local guardians. If you have assets overseas, consider a country-specific will for that country.

Along the estate planning line, if you start to accumulate wealth, and there is a possibility of leaving some of it behind, it’s crucial to plan how you are going to deal with estate taxes. Typically, if you are an NRA with US-situs assets, your estate tax exemption is a low $60,000; therefore, it is advisable to be proactive about planning for these estate taxes.

Overseas Investments: If you have overseas assets of any kind (rental, stock, etc.), they need to be reported in your US tax filing. Failure to file can result in substantial penalties, which may significantly impact your US finances. You also want to be sure about what the investments are – avoid foreign-registered funds at all cost, and they are likely to cost you a lot in taxes in the US.

Three Questions with Tamara Witham, CFA, CFP®:

Tamara Witham is a financial planner based in Harrison, New York, who specializes in serving first-generation Americans and foreign-born families. She answered three questions that she frequently tackles when meeting with her clients.

Q: What is a common financial planning challenge unique to first-generation Americans and foreign-born individuals and families that you frequently encounter when working with your clients? How do you work with them to overcome this challenge?

Tamara: First-generation Americans and foreign-born individuals are often overwhelmed by the complexities of the U.S. financial system. After helping foreign-born families for many years, we’ve learned the importance of a customized approach that respects our clients’ cultural backgrounds and values. We aim to address the confusion by explaining key terms and strategies in plain language while creating a financial plan tailored to their retirement dreams and goals.

Whether they plan to retire here or abroad, we can help them navigate investment and tax considerations to develop a strategy for building long-term savings. Suppose a client plans to retire outside of the U.S. Certain tax-advantaged retirement accounts may not provide the same advantages as if they stayed stateside. We’re here to simplify the process and help clients make informed decisions to save and prepare for the lifestyle they envision.

A concrete example is understanding and simplifying the decision to purchase insurance. Insurance needs can vary significantly between the U.S. and other countries. Adequate coverage is crucial to protecting loved ones financially. Many employers provide basic life insurance between one- and two-times base salary. In our experience, this base benefit may not be enough to adequately protect a family in the event of a premature death. Additionally, employer policies may not be portable if an employee leaves. Many families utilize private insurers to guarantee complete customizable protection. We explain options to find the right amount and type of policy based on each situation.

Navigating U.S. health insurance also poses challenges. We help compare company, private, and public exchange plans so families can obtain optimal coverage. We also explore the options of associated Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA).

Disability insurance can replace income lost to injury or illness. However, supplemental policies are expensive, pricing out some families. Also, many insurers deny claims for those residing abroad, even with premiums paid, which may be necessary for someone looking to return to his or her native country in the event of a disability.

Every family has unique priorities and risk tolerance. Through discussion, we craft tailored recommendations on available coverage to suit our clients’ finances and safety needs. We aim to educate clients about offerings so they will make informed choices to safeguard their families’ financial security.

Q: How do the services you offer first-generation Americans and foreign-born individuals and families distinguish your firm from other advisory firms?

Tamara: According to research by Herbers and Company, nine in ten investors want their advisors to help with tax planning, and three-quarters want help with retirement planning services. However, few advisory firms offer both services, and even fewer do it well. GreenLife has focused on concrete solutions for our clients’ tax planning and retirement needs.

The U.S. income tax system is often more complex than many of our clients’ respective native country’s tax systems, especially concerning reporting foreign-held income. In the U.S., full income tax reporting of worldwide financial assets and income is required, meaning the IRS may tax assets held abroad. Tax residency status is not the same as immigration status. As a U.S. resident with overseas assets, several complex reporting requirements may apply, which can trigger U.S. tax residency status.

We use tax planning software to incorporate a client’s tax profile into our financial planning services. We’re excited to offer tax planning as part of our firm’s comprehensive financial planning because taxes impact virtually every aspect of one’s finances.A client’s tax return is a financial fingerprint: it’s unique for that person, complete with valuable clues and information, all buried in dozens of pages and hundreds of numbers. Understanding the return equips us to have more valuable and actionable conversations with our clients. Additionally, we demystify the world of income taxes and help clients understand this vital piece of their unique financial picture.

Tax planning includes reviewing a tax return in depth to identify potential opportunities, both now and in the future, to minimize lifetime tax liabilities. Tax planning differs from tax preparation, which may focus on compliance with current tax laws and rules.By analyzing a client’s current and prior tax returns, we can recommend steps to potentially lower the next year’s tax bill and uncover other long-term planning opportunities.

Here are some of the ways we may be able to leverage a client’s return during financial planning and investing strategies:

Tax-Efficient Portfolio Management: Being fluent in a client’s tax status informs better investment strategies, such as realizing capital gains rather than ordinary income for greater tax efficiency.

Retirement Optimization: Knowing a client’s tax details helps us determine the role of each retirement account in his or her overall financial planning strategy. Conversations often focus on Roth IRA conversions.

Tax-Sensitive Withdrawal Strategies: Taxes are one factor when withdrawing retirement funds. We can illustrate how proper tax management is critical for withdrawal decisions.

Coordination with a Client’s CPA: Understanding a client’s tax profile allows us to collaborate effectively on an integrated financial strategy with tax professionals.

Ongoing Tax Management: Tax laws change frequently. We can suggest adjustments to address new laws and regulations by reviewing returns. We can run projections to see how potential changes (e.g., filing status, dependents, the sale of a business, stock option exercises, etc.) may impact a client’s upcoming tax liability and model how potential changes may impact upcoming tax liabilities.

Q: For first-generation Americans and foreign-born individuals who are unsure whether or not they should hire a financial advisor at the current point in their lives, what guidance can you provide to help them make a more informed and educated decision?

Tamara: For first-generation Americans and foreign-born individuals who are navigating the complex financial landscape of a new country, hiring a knowledgeable financial advisor sooner rather than later can provide significant advantages. An advisor well-versed in cultural differences can offer tailored guidance aligned with each client’s values and goals, helping build a solid financial foundation through comprehensive planning for investment strategies, retirement, and risk mitigation.

Acting now is better than delaying until later if an individual has specific financial planning needs. The earlier he or she implements a plan, the more investments can potentially grow through compounding interest over time. An advisor can also identify and address risks like insufficient insurance coverage and excessive debt before these issues escalate. Setting clear financial goals from the start, whether for retirement, education funding, or a home purchase, increases one’s chances of success with a defined roadmap.

Working with an advisor can save thousands of dollars through optimized tax planning strategies and ensure a client claims eligible deductions and credits. As careers and family dynamics evolve, an advisor can help adapt a client’s plan to manage transitions like job changes, marriage, and having children – a proactive approach that protects long-term financial security.

Not all people need an ongoing relationship with a Certified Financial Planner. Some may already have a good grasp on managing finances and making decisions. While ongoing advisory services may not be necessary, everyone can benefit from at least an initial consultation. Most advisors, including our firm, offer complimentary meetings to assess if there is a good fit and explore how the advisor can provide value based on the individual’s circumstances. There is little downside to contacting an advisor for this initial consultation.

Ultimately, procrastinating on financial planning can harm those who need it. Starting sooner allows one to capitalize on wealth-building opportunities while avoiding costly mistakes. The earlier one works with an advisor, the better positioned they will be to achieve their financial objectives.

Are you a financial advisor who specializes in serving family-oriented professionals?

✅ Get added as a specialist in this area in our next monthly update (Subject to availability and qualification criteria.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender ✅ Or request more information by email:

Slide Show: Financial Advisors for Immigrants & Foreign Nationals

🙋♀️ Have Questions About Financial Planning for Immigrants?

Get answers from the Wealthtender network of financial professionals and educators.

Brian and his wife live in Texas, enjoying the diversity of Houston and the vibrancy of Austin.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Wealthtender Study of $100K+ Households Seeking Financial Advice

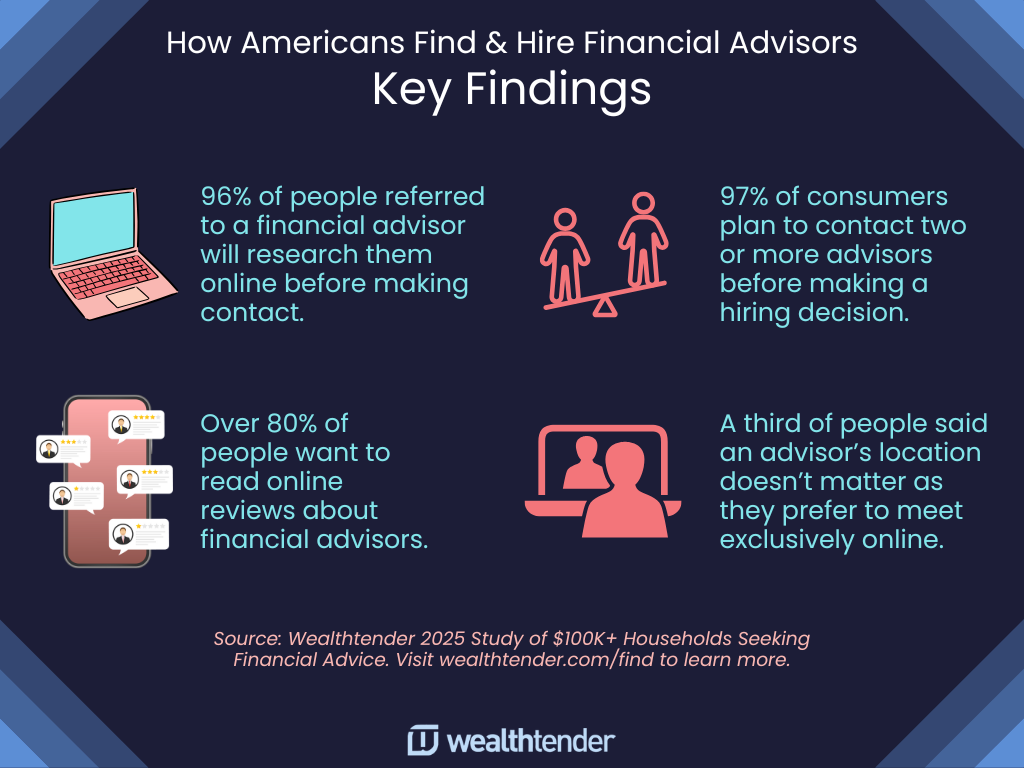

August 2025: A survey of 500 U.S. adults with household incomes over $100,000 reveals that most consumers will use online resources to find or compare financial advisors before making a hiring decision even after receiving a referral, and most won’t shy away from advisors using Artificial Intelligence (AI) tools.

If you’re thinking about hiring a financial advisor, you may want to know how others plan to approach the process. In late July 2025, Wealthtender surveyed 500 U.S. adults earning over $100,000 who plan to hire an advisor within the next five years to understand exactly how they intend to start their search, create a shortlist, and choose one advisor over another.

This report reveals how the advisor search is evolving, the online tools people trust most, and what clients think about advisors using AI. You’ll also find practical tips to guide your own search, so you can confidently find and hire the right advisor for your unique needs.

Five Key Takeaways:

1. While many Americans start their search for a financial advisor with a referral from friends or family, almost everyone will dig deeper: 97% plan to interview multiple advisors and 96% will do further research online before making a hiring decision.

2. To decide if an advisor is the right fit, the most popular next step for 83% of respondents is to research the advisor’s reputation by looking for online reviews and awards, followed by an introductory call with the advisor (73%) and visiting the advisor’s website (72%).

3. Before contacting an advisor, survey respondents said the two most important pieces of information they want to know are the advisor’s areas of specialization (64%) and fee/pricing structure (62%).

4. Most respondents are generally comfortable with advisors using artificial intelligence (AI) tools to streamline admin tasks, somewhat comfortable with AI to help generate personalized financial plans, though uncomfortable with investment decisions outsourced to AI.

5. A third of respondents said an advisor’s location is not a factor as they prefer to meet exclusively online.

Republishing Guidelines: You are welcome to republish or reference any part of this Wealthtender study, including embedded graphics. We kindly ask that you include proper attribution to “Wealthtender 2025 Study of $100K+ Households Seeking Financial Advice” and include a link back to the full study at wealthtender.com/find.

Before we dive into the details, it’s important to note that this study intentionally excluded many respondents who work with a financial advisor today and said they are satisfied with no plans of making a change. (This finding is not a surprise as our 2025 Voice of the Client Study reflects overwhelming consumer satisfaction with advisors based on their online reviews.)

1. Where People Start Their Search for a Financial Advisor

Finding the right financial advisor can feel overwhelming, but you’re not alone in wondering where to begin. The good news? Most Americans start their search in predictable places, and you can follow a similar roadmap to find the right advisor for you, too.

In the chart below, you’ll see how people said they plan to start their search for an advisor. Survey participants were not limited to a single response since many people plan to use multiple resources to find and evaluate advisors.

Personal connections lead the way… When it’s time to find a financial advisor, 62% of people will turn to their most trusted source first: friends and family. There’s something reassuring about getting a recommendation from someone you know and trust, especially when it comes to your financial future. Nearly half (49%) will also reach out to other professionals in their network (e.g., accountants, attorneys, or their bank) recognizing that these experts often have valuable insights about reputable advisors.

… But technology is catching up fast. Online search is quickly becoming just as important as word-of-mouth recommendations. Half of all survey participants plan to use traditional search engines like Google or Bing to find potential advisors. This isnt surprising as people want to know what’s out there beyond just the one or two names of advisors they may hear recommended by family or friends.

Online directories and social media platforms gain popularity. Online advisor directories like Wealthtender will be used as a starting point by about one-third of consumers (32%), while social media platforms like LinkedIn, Reddit, and Facebook influence about 22% of people.

Many people appreciate opportunities to learn. Educational events like online webinars (19%) and in-person seminars (18%) hosted by advisors in their local communities also play a valuable role, especially for those who want to get a feel for an advisor’s expertise and communication style before arranging an introductory meeting.

Key Takeaway & Section Resources:

Most people use multiple approaches to find advisors, and you should too. Start with your personal and professional network if they have advisors to suggest, but don’t stop there. The combination of trusted recommendations and your own online research will give you the best foundation for identifying a handful of advisors you feel may be worth contacting.

🔎 Find a Financial Advisor on Wealthtender

Thousands of people visit wealthtender.com each month to find and evaluate financial advisors. When you’re ready to start your search, consider the resources below that can help you find an advisor nearby, one who specializes in areas that may be important to you, and hundreds of advisors whose clients have submitted thousands of reviews to help you make a more informed hiring decision.

Knowing that most people will use multiple approaches to find a financial advisor, it’s important to diversify your sources for client acquisition to improve your likelihood of getting found.

While referrals remain the top source for consumers to find advisors (62%), the data reveals a critical insight: the most successful firms employ a multi-channel approach. With 50% of prospects using search engines and 25% leveraging AI tools like ChatGPT, advisors who only rely on referrals are missing significant opportunities.

Immediate Action Items:

Optimize for AI Search Tools: Create content to answer common financial planning questions in formats that AI tools can easily reference (e.g., using FAQ schema). ChatGPT and Gemini often cite authoritative, well-structured content when making advisor recommendations and implementing an AEO (Answer Engine Optimization) strategy can enhance your visibility in AI search tools.

Search Engine Visibility: Invest in SEO/AEO-optimized content targeting local and niche-specific categories (e.g., “retirement planning advisor in Austin for Dell employees” or “CFP for tech executives with equity compensation”).

Social Media Strategy: With 22% of prospects using social media to start their search, develop a consistent presence on one or more platforms focusing on educational content combined with posts showcasing your client testimonials to accelerate the trust-building process with prospects.

Leverage Educational Events for Lead Generation The 19% of consumers showing up to online webinars and 18% attending in-person events represent high-intent prospects. These individuals are actively investing time to learn, indicating serious consideration of hiring an advisor.

Partner with Wealthtender for Search Optimization:

Joining Wealthtender directly addresses multiple data points from this section:

Professional Credibility: Profiles with verified client reviews enhance your digital authority, whether prospects are initiating their search online or received a personal referral and looking to validate your credibility before making contact.

32% Directory Usage: Wealthtender is visited by ~50,000 consumers each month, many of whom are actively looking for a financial advisor. As the leading find-an-advisor directory and industry’s first compliant testimonial collection platform, your profile on Wealthtender ensures you’re getting found.

Search Engine Amplification: Wealthtender profiles are optimized for SEO and AI to increase your likelihood of appearing more frequently in Google searches and in answers generated by AI tools like ChatGPT.

AI Tool Integration: Wealthtender’s structured data format (e.g., financial services schema, review schema, FAQ schema) makes advisor profiles more likely to be referenced in Google AI Overviews and AI tools like ChatGPT when prospects ask for advisor recommendations.

🤓 Dive Deeper into the Data

wdt_ID

Which resource(s) do you plan to use to find a financial advisor?

Referrals from professionals (e.g., accountant, attorney)

49.20%

14.11%

246

9

Attend an in-person event (e.g., educational seminar, lunch & learn)

17.80%

5.11%

89

10

Attend an online event (e.g., educational webinar)

19.00%

5.45%

95

11

Other

0.60%

0.17%

3

2. Almost Everyone Will Research Multiple Advisors Online Before Hiring One

Even if your best friend or next door neighbor raves about their financial advisor, you shouldn’t hire them without doing your homework first. And you’ll be in good company as 96% of people in our survey said they would still research an advisor even if that advisor came highly recommended.

Referrals Matter, But Consumers Will Still Do Their Own Homework

A related insight worth considering is that almost all survey participants plan to evaluate multiple advisors before choosing who to hire.

A referral is just the starting point, not the finish line. Your financial situation is unique, and what works for someone else might not be the best fit for you. The advisor who helped your colleague navigate a career change might specialize in something completely different from what you need.