Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Avoid the one mistake people make that can expose your 401(k) money…

Do you have a 401(k) account?

It’s almost as likely as not.

According to Statista, there were 133 million employees in the US in September 2022, and the Investment Company Institute (ICI) says there were 60 million active 401(k) participants that month, or 45% of all employees.

If you’re one of those 60 million, there’s something you should know.

While a 401(k) account can’t be taken from you as a result of a lawsuit, there’s one mistake you must avoid or (some of) your 401(k) money may be exposed to lawsuits.

401(k) Accounts Are (Almost Entirely) Protected, But…

In 2005, the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) was passed, making filing for bankruptcy under Chapter 7 rather than Chapter 13 more difficult. BAPCPA also put in place protections for money held in qualified retirement plans.

According to the Benefit Financial Services Group, “Under BAPCPA, assets held in all qualified plans (such as 401(k), profit sharing, thrift, money purchase, ESOP, and defined benefit plans), 403(b) plans, and state and local government-sponsored 457 plans are expressly excluded from the bankruptcy estate… Assets in traditional and Roth IRAs are protected up to a $1 million limit, without regard to rollover amounts.”

Note however, according to Lord Abbett, one of the oldest money management firms in the US, “BAPCPA draws no distinction between owner-only retirement 401(k) plans and other qualified retirement plans with respect to bankruptcy exemption. Outside bankruptcy, however, it appears that owner-only plans may be subject to attachment by creditors.” (my emphasis)

As for traditional and Roth IRAs, those were protected up to $1 million in 2005, with a cost-of-living adjustment (COLA) once every three years. As of this writing, that limit stands at $1,512,350.

Note that 401(k) money is not protected against tax liens or your spouse (who is considered a co-owner of those monies).

The Mistake You Must Avoid

Aside from failing to maintain a great relationship with your spouse and the IRS, the big potential gotcha that could expose at least some of your 401(k) money to judgments is how you roll it over after leaving your employer.

BAPCPA offers an unlimited exemption from your bankruptcy estate for your 401(k), 403(b), and other employer-sponsored retirement plans, as well as for any IRAs that were funded solely by money rolled over from such employer-sponsored accounts.

However, if you roll such 401(k) money into an existing IRA that held money not rolled over from such accounts, it loses that unlimited exemption.

In that scenario, your IRA is only protected up to the (COLA-adjusted $1 million IRA exemption).

Thus, while it may somewhat simplify your finances to not open a new IRA for the rollover, that simplicity may cost you dearly down the line.

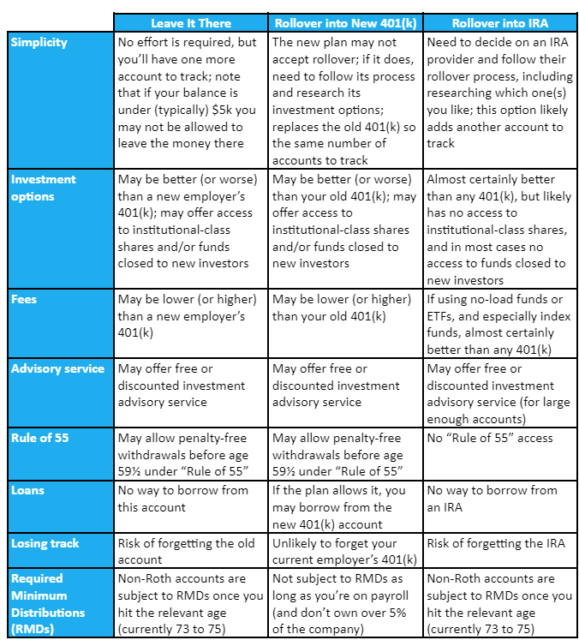

3 Ways to Maintain Your 401(k) Money’s Unlimited Exemption

Here are 3 ways to maintain the unlimited exemption for your old 401(k) money.

- Leave it where it is.

- Roll it over into your new employer’s 401(k) (if allowed).

- Roll it over into a new IRA (or an established one that has only money from prior 401(k) rollovers).

What are the pros and cons of each of these?

Here’s a table that summarizes them:

Note especially that you can legally avoid RMDs even on your non-Roth 401(k) balance as long as you remain on the payroll of a company you don’t own or one where your ownership is no more than 5% of the company.

Financial Professionals Say That’s Not All You Should Consider

The above aren’t the only considerations.

Stephan Shipe, PhD, CFA, CFP®, Owner & Lead Advisor at Scholar Financial Advising, LLC cautions, “Specifically for high earners, rolling 401(k) money into an IRA can make future Roth conversions run into the pro-rata rule. This is a common issue for those looking to perform a ‘backdoor’ Roth conversion because having any pre-tax dollars in any IRA leads to a taxable event when converting new after-tax IRA money into a Roth IRA.”

Nathan Mueller, MBA, Financial Planner and Financial Coach at Blackbird Financial Planning points out two additional important details, “Rolling over into an IRA often makes sense. It provides more investment options, and the money is in your name. I’ve seen companies go through bankruptcy where employees’ retirement accounts were frozen until the bankruptcy court determined if employees got to keep their retirement savings.

“However, I don’t always recommend rolling into an IRA. For example, if you roll over a 401(k) account with an outstanding loan, the remaining balance on the loan is considered a distribution and may be subject to a penalty and taxes.”

Amanda Howerton, Senior Advisor at Rather & Kittrell adds two more considerations, “If the 401(k) is pre-marriage/separate property and the IRA is considered marital property (or vice versa), you may want to keep them separate in case of divorce. Once you comingle monies, all the money will be considered marital property and will likely get divided if you divorce.

“Before a rollover, consider establishing a Roth IRA for any post-tax/Roth 401(k) dollars. This allows the new Roth IRA to grow tax-free with eventual tax-free distributions.”

P. Timothy Uihlein, CFP®, MBA, Partner, Managing Director, and Senior Wealth Manager at Vincere Wealth Management says, “One major reason I advise clients not to roll over an old 401(k) to an IRA is losing loan privileges (if the old plan allows it). While often the terms aren’t ideal, it offers a solution to address a short-term liquidity issue.”

Jen Swindler, CFP®, AFC®, Senior Wealth Manager also at Vincere Wealth Management, cautions against leaving 401(k)s with old providers, especially for smaller balances, “I’ve seen many people unexpectedly receive a distribution check from a prior 401(k) plan. They often don’t understand why they’re receiving it, sometimes cash it, and then later owe taxes and a penalty.”

Freeman Linde, CFP®, La Crosse Financial Planning offers a final caution, “Most people should avoid leaving an old 401(k) account as is. The more time passes from when you leave that job, the harder it gets to manage the money. HR departments change and your former employer may switch 401(k) providers. Keeping your money consolidated into as few accounts as possible makes it easier to manage.”

How Many People Have More Than the BAPCPA IRA Exemption Amount?

The Washington Post reported that according to Fidelity Investments, it had nearly 300,000 401(k) millionaires at the end of 2022, compared to 442,000 a year earlier.

They also showed about 280,000 IRA millionaires, a 25% drop from the end of 2021.

However, the S&P 500 (total return, including dividends), which dropped 18.1% from the end of 2021 to the end of 2022, was back up at the end of July 2023 to just 1.2% below its value at the end of 2021.

Thus, we can extrapolate the number of Fidelity 401(k) millionaires is near its December 2021 level of 442,000, and the number of Fidelity IRA millionaires is near 373,000.

Fidelity has 21.5 million 401(k) participants. According to US Census data, there are about 52.6% as many IRAs as 401(k) accounts, so Fidelity likely has around 11.3 million of those. Thus, about 2.0% of 401(k) participants and 3.3% of IRA owners have over $1 million in their 401(k) and/or IRA, respectively.

Scaling from Fidelity’s 21.5 million 401(k) accounts to ICI’s estimate of 60 million 401(k) participants, there are about 1.2 million 401(k) millionaires in the US. Similar scaling gets us to about 1.0 million IRA millionaires.

Since it’s hard to know how many 401(k) millionaires are also IRA millionaires, we’ll neglect the overlap and estimate that up to 2.2 million Americans have at least $1 million in their 401(k) and/or IRA.

Using DQYDJ’s net worth percentile calculator, having over $1,512,350, places you in the 93.5th percentile (excluding primary residence equity) vs. the 90.5th percentile for $1 million.

With 123.6 million households in the US, about 68.4% of those with at least $1 million have more than $1,512,350. That’s about 1.5 million Americans with enough wealth that if it was all in IRAs, at least some of their money would be exposed to bankruptcy judgment.

The Bottom Line

Chances are that you aren’t yet a 401(k) and/or IRA millionaire.

From the above, we see there are only about 2.2 million of those fortunate and disciplined enough to have achieved that lofty goal. Increasing the threshold to the $1,512,350 BAPCPA exemption for IRAs reduces the count further to about 1.5 million Americans.

For those people who are unlikely to exceed the IRA exemption limit, Douglas Greenberg, President, Pacific Northwest Advisory says, “While it’s essential to be aware of the potential loss of unlimited exemption when merging 401(k) funds with an existing IRA containing non-rollover funds, this doesn’t mean one should always avoid it. Especially if you’re unlikely to exceed BAPCPA’s IRA exemption, you should weigh the simplified financial management and potential investment options against the risk of losing the exemption for some excess IRA money.”

However, if you regularly invest as much as possible into your 401(k) account, you may ultimately join that wealthy group.

And then, don’t forget to avoid the one mistake when deciding what to do with your 401(k) account managed by your old employer.

You can (in most cases) leave the money where it is, (may be able to) roll it over into your new employer’s plan, or roll it over into a new IRA (or an established one as long as it only contains money from prior 401(k) rollovers).

In addition, if you’re a millionaire, consider buying an umbrella insurance policy. It’s an inexpensive way to protect your wealth if you get sued.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals.

Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Find a Financial Advisor

Do you have questions about your financial future? Find a financial advisor who can help you enjoy life with less money stress by visiting Wealthtender’s free advisor directory.

Whether you’re looking for a specialist advisor or prefer to find a financial advisor near you, you deserve to work with a professional who understands your unique circumstances.

Have a question to ask a financial advisor? Submit your question and it may be answered by a Wealthtender community financial advisor in an upcoming article.

This article originally appeared on Wealthtender. To make Wealthtender free for our readers, we earn money from advertisers, including financial professionals and firms that pay to be featured. This creates a natural conflict of interest when we favor their promotion over others. Wealthtender is not a client of these financial services providers.

Disclaimer: This article is intended for informational purposes only and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

What to Read Next:

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor