Discover financial advisors trusted by residents of Palmer, Alaska in the only local directory featuring 5-Star Certified Advisor Review™ recipients and Wealthtender Voice of the Client Award™ winners—recognition earned for exceptional client feedback. Compare fiduciary, fee-only advisors, CFP® professionals, and specialists to find the right fit for your unique financial needs.

Whether you have lived in Palmer for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Palmer featured on Wealthtender you may want to add to your shortlist.

Featured Palmer Financial Advisors

As you prepare to interview financial advisors in Palmer who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Palmer

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Palmer.

The Benefits of Hiring a Financial Advisor in Palmer

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Palmer, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Palmer? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Palmer Financial Advisor

Before hiring a financial advisor in Palmer, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

The phrase “millionaire tax” conjures a clear mental image: someone with a yacht, a second home, and a net worth that most people will never approach. But the reality of how these taxes actually work is far more complicated and far more likely to affect people who don’t fit that picture at all. In states like California, Massachusetts, New York, and Washington, these taxes are triggered by a single year of income exceeding $1 million, regardless of your net worth or what you normally earn. That means a business owner selling a company they spent decades building, a professional with a strong bonus year and a few well-timed stock sales, or even a retiree whose tax-deferred balance has grown large enough to generate substantial Required Minimum Distributions could all find themselves in the crosshairs often without realizing it until it’s too late to do anything about it.

When you ask people, most support “taxing the rich.” That’s understandable. Arguably, even fair. After all, it’s mostly an extension of having a progressive tax system. And no, “progressive” here doesn’t mean the opposite of “conservative.” It means that as your income increases, your marginal tax rate also goes up, so you pay a higher portion of your income in taxes. At least, in principle.

For several years now, more and more states have added a “millionaire tax” to their tax code. This now includes high-tax states like California and New York, as well as nominally no-income-tax states like Washington.

And if, like me, you’ve never brought in over $1 million in a single year, it can seem like a non-issue. Whereas, if you do earn that much, asking you to pay a bit extra to support your less fortunate and often struggling neighbors, shouldn’t be very controversial.

But this framing misses some important details that can end up biting people who don’t fit that class of ultra-high-income earners. Maybe even you and me.

Key Takeaways

1

State millionaire taxes are triggered by a single year of high income — not by being wealthy or consistently earning seven figures.

Seven states and Washington, D.C. have enacted millionaire taxes that apply to annual income exceeding $1 million, regardless of your net worth or what you typically earn. A business sale, stock option exercise, large capital gain, or even a substantial bonus can spike your income into the target zone for a single year — leaving you paying a tax that was never intended for someone in your financial situation.

2

Stacking multiple income events in the same tax year is the most common — and most avoidable — way non-millionaires get caught by millionaire taxes.

No single transaction needs to exceed $1 million for you to trigger the tax. A combination of events — an options exercise, a portfolio rebalance, a partial business sale, and a strong bonus — can collectively push your taxable income over the threshold. Spreading these events across multiple tax years, when possible, is one of the most effective ways to avoid an unnecessary and outsized tax bill.

3

Even without a windfall, large tax-deferred retirement balances can force retirees into millionaire tax territory through Required Minimum Distributions.

Decades of maxing out traditional IRAs and 401(k)s can build balances large enough that IRS-mandated RMDs generate over $1 million in taxable income annually in advanced age — with no voluntary transaction required. Strategies like Roth conversions in lower-income years and carefully managed withdrawal sequencing, ideally begun years before RMDs start, can help reduce this late-life exposure.

What Is a “Millionaire Tax” and How Does It Work?

In most states, these taxes are set up as either a surcharge on income over $1 million or as one or more tax brackets that apply only to taxable income above $1 million.

This means that if your taxable income is under $1 million, you don’t pay this tax; even if you do have such a high income, only the portion over $1 million (or whatever higher bracket) gets taxed at the “millionaire tax” rate(s).

Why You Don’t Have to Be a Millionaire to Owe a Millionaire Tax

First and foremost, people normally think of “millionaires” as people with a net worth over $1 million (which, per DQYDJ.com, includes nearly 20% of American households).

But as described above, these “millionaire taxes” apply to income over $1 million, regardless of your net worth.

Normally, again per DQYDJ.com, this would apply to fewer than the top 1% of income earners in the US.

The problem is that you don’t have to earn that much consistently to be hit by these taxes. You could fall into this trap in a given year, even if:

Your annual income is usually far lower than $1 million.

Your net worth is far below $1 million.

You don’t think of yourself as either wealthy or high-income.

Why?

Because these taxes look at your annual income separately every single year.

One-Time Income Events That Can Unexpectedly Trigger the Millionaire Tax

There are multiple ways that you could temporarily fall into this bucket, even if your income is normally below the threshold. Here are a few ways your income could exceed $1 million in a single year:

You sell a 7-figure+ business.

You exercise stock options with a high enough profit.

You sell investments with a high enough appreciation.

You receive a large enough bonus.

Any of these can spike your annual income in a single year high enough that you get caught by your state’s millionaire tax.

Table 1 shows seven states and one district where this matters most.

Jurisdiction

Millionaire Tax Structure

California

1% surcharge on income over $1M above already-high 9.3% base tax rate for high earners.

Maryland

New brackets, including 6.5% for income above $1M ($1.2M) for individuals (married filing jointly, MFJ); up to 0.75% higher than the old highest rate.

Higher bracket, at 10.75%, for income over $1M. This is 1.78% more than the next-highest bracket.

New York

Higher bracket for income over $1.08M for individuals ($2.16M for MFJ), with two more brackets, 10.3% on income above $5M, and 10.9% above $25M. For NYC residents, this is in addition to city income tax rates of 3.078% to 3.876%, with the highest rate bracket starting at $50k for individuals (MFJ $90k).

Washington, DC

Highest tax bracket for income over $1M, taxed at 10.75%, 1% higher than the next-highest bracket.

Washington

A new tax levies 9.9% on income over $1M. This is in addition to a tax on high capital gains.

Table 1. Where “millionaire taxes” have already been enacted, and their structure.

And since the population of these eight is about 97 million, nearly 30% of the total US population, there’s a distinct chance that you’re at least potentially in the crosshairs.

How Stacking Income Events in One Year Creates an Unexpected Tax Problem

Even if no single event spikes your income high enough, if multiple such events happen in the same tax year, you’re hit.

Not many people ever sell a business for a 7-figure (or higher) payday, get a 7-figure bonus, or realize a 7-figure gain on an options or stock sale.

But what if two or more smaller versions of these stack on top of each other in the same tax year?

Perhaps your regular income is $200k; you realize $450k gains when exercising options; you rebalance your taxable portfolio, and realize another $250k in capital gains; and you sell part of a business you’ve been building for years, netting another $500k.

None of these is over $1 million, but combined, they exceed the $1 million tax threshold.

And if you’re, say, in Massachusetts, you get hit with that 4% surcharge on $400k, even if you don’t consider yourself wealthy or an ultra-high-income earner.

An extra $16k in state taxes may not sound like much. But that’s on top of the ~$70k you’d pay without the millionaire tax (even assuming none of your realized capital gains are short-term, taxed by Massachusetts at 8.5% or long-term gains from the sale of collectibles, taxed at 12%!), plus however much you pay the IRS.

Why Focusing Only on Maximizing Income Can Backfire at Tax Time

When it comes to finances, most people focus on:

Increasing their compensation as much as possible.

Getting the best price for their business.

Maximizing the value of their stock options.

Optimizing their investment portfolio allocations to meet long-term investment goals.

Focusing on just the immediate financial outcomes, without considering the tax impacts of timing, sets you up for potentially paying a tax for which you were never the intended target.

What the Wealthy Do Differently

Wealthy households, especially those with ultra-high incomes and who work with advisors, take a more holistic approach, addressing income timing as much as income maximization.

They don’t just ask if a financial move makes sense.

They also ask, if it does, when it would make the most sense to make it.

Instead of allowing large taxable incomes to stack in one year, they look for ways to:

Spread large gains across multiple years.

Avoid combining multiple major events in one year.

Coordinate decisions across investments, compensation, and business activity.

This doesn’t eliminate or evade taxes.

What it does is minimize paying taxes at unnecessarily high rates and/or triggering excess taxes and fees, such as millionaire taxes or Medicare Income-Related Monthly Adjustment Amount (IRMAA) surcharges.

The takeaway here is that millionaire taxes end up targeting not just their intended target, the ultra-wealthy, ultra-high-income earners. You can get caught up in the trap without being a millionaire or regularly earning 7 figures.

All it takes is having one or more special income-related spikes that push you into the target zone.

That’s where planning and timing make a difference.

How RMDs Can Push Retirees Into Millionaire Tax Territory

There’s another way you could fall into this trap, even with no mistimed income spikes.

Successful professionals with multi-6-figure incomes look for ways to shelter income from taxes throughout their careers. For example, by maxing out contributions to deferred-tax retirement accounts like traditional IRAs and 401(k) plans.

Over the course of a multi-decade career, with just a little good fortune and avoiding major investing mistakes, this can build into a multi-million-dollar tax-deferred balance.

Couple high tax-deferred balances with longer life expectancies, especially for wealthy, highly educated people, and Required Minimum Distributions (RMDs) may become another path into the millionaire-tax trap.

The IRS requires you to withdraw an ever-increasing percentage of your tax-deferred balances each year once you hit the RMD trigger age. The IRS provides the RMD factors (Table III on that website is most likely to be relevant) by which you divide your balance to show how much you must take out (and pay taxes on).

Table 2 below shows how that translates into “millionaire-tax danger zone” balances for certain older ages.

Age

RMD Factor

Implied Balance for ~$1M RMD

90

12.2

~$12.2M

95

8.9

~$8.9M

100

6.4

~$6.4M

Table 2. RMD factors and implied tax-deferred balances that cause $1-million taxable income.

This matters because withdrawals from these accounts are treated as taxable income in the year when they’re drawn.

As a result, if your balance grows large enough and you’re old enough, you can fall into the millionaire-tax trap without any voluntary transaction or special income spikes.

No business sale, option exercise, stock sale, or poorly timed bonus.

Just a successful investing career and advanced age push you into the crosshairs.

No, not everyone reaches such advanced ages.

But it’s not all that rare.

According to data from the Social Security Administration’s actuarial life table:

About 22% of men and 33% of women aged 67 live to age 90.

Roughly 6.8% of men and 13% of women live to age 95.

A smaller but still meaningful group reaches age 100.

Avoiding RMDs is hard, short of dying too young or being too poor, but good planning can mitigate things.

3 Strategies to Avoid the Millionaire Tax Trap

Here are 3 things you can do to reduce your risk and/or impact of getting caught up in a trap that isn’t meant for you, and paying needlessly high tax rates.

1. Spread Major Income Events Across Multiple Tax Years

As mentioned above, even if no single income spike is high enough to make you a target, enough individually low spikes can become an issue when combined in a single year.

To avoid this, when possible, spread large income events across multiple years. For example:

Stagger options exercises.

Sell assets in a tax-aware way, e.g., by selling losers along with winners.

Time business transactions with care, e.g., spreading income over two or more years.

Not everything is within your control, but be mindful of what is.

Maximizing your financial gains is worthwhile, but always consider your after-tax benefit rather than just the pre-tax win.

Before pulling the trigger on a big transaction, ask yourself what the impact would be on your taxable income, and thus your taxes, for that year.

John Davis, CFP®, EA, founder of JKD Financial, says, “The most common ‘millionaire tax’ traps aren’t for the consistently wealthy; they’re for the everyday saver hitting a one-time liquidity event. I see this most often during the sale of a long-held family business or a massive Roth conversion intended to front-load tax liability in retirement. Events like these can skyrocket a taxpayer into their state’s highest bracket for a single year, even if their typical lifestyle doesn’t resemble a millionaire’s.

“The planning decision that makes the biggest difference in avoiding unnecessary state income taxes from income spikes is switching your focus from ‘annual tax’ to ‘lifetime tax.’ By intentionally managing a moderate level of tax liability every year, we avoid the massive, one-time spikes that trigger these surtaxes. However, when a spike is unavoidable, like a business sale, the best strategy is ‘winning in the margins.’ This means pairing that income with proactive offsets like Donor Advised Funds (DAFs) for charitable giving and being purposeful with tax-loss harvesting in taxable brokerage accounts

“Timing these sorts of events can sometimes be difficult to navigate, as they can happen quickly. With most things related to financial and tax planning, the key is being proactive. I help clients reduce state-level liability by using Treasury obligations or municipal bonds (where applicable), which often provide favorable state tax treatment. I also look for ‘gap years,’ windows between retirement and Social Security, to spread out income events. Every dollar we can shift out of a high-tax spike into a lower-income year is a direct win for the client’s bottom line.”

Michael Anderson, CFP of AdviceOnly, agrees with that last, “I help clients in Southern California, where the one-year holding period of stocks doesn’t qualify for a superior long-term capital gains treatment. Instinct is often to liquidate equity compensation in the year of retirement, but if it’s fully vested, I recommend waiting. That way, a retiree can control a high-income spike and liquidate over lower-income years in retirement.”

2. Understand What Your State’s Millionaire Tax Actually Targets

Don’t assume you’re safe from a millionaire tax simply because neither your net worth nor your typical income is in the 7-figure-plus range.

Seven states and the District of Columbia have enacted millionaire taxes, but the specific details vary.

For example:

Minnesota’s additional tax targets net investment income rather than wages.

Massachusetts applies a 4% surtax to income above the threshold.

Washington’s millionaire tax interacts with capital gains differently.

Check what your state’s tax law actually says, and keep in mind that it may say something different next year, since 2 more states are considering implementing such a tax, and more may well follow.

Knowing this can help you structure transactions, pick assets to sell, and time realized gains differently.

3. Plan Ahead for RMDs Before They Become a Tax Problem

If most of your nest egg sits in tax-deferred retirement accounts such as IRAs and 401(k) plans, and you live long enough, RMDs can cause you grief late in life.

To address this, consider:

Appropriately timed Roth conversions.

Managed withdrawal timing.

Optimal division of withdrawals before RMDs between different account types.

These decisions are best made years before RMDs begin, let alone before they become large enough to cause problems.

Another strategy that many propose is moving to a lower-tax, or no-tax, state, one that doesn’t have a millionaire tax.

That’s a major life change that may or may not be appropriate for your specific life situation. In my opinion, most people can solve the problem without such a major life disruption.

The Bottom Line: You Don’t Have to Be a Millionaire to Pay Like One

Whether or not you think millionaire taxes are fair, if your state has one, you need to consider it.

Even if you aren’t wealthy and your typical income is far short of $1 million, current millionaire taxes don’t consider your net worth or your usual income.

They consider your income each year separately, and if it spikes high enough due to one or more one-time events, or even late-life RMDs, you get hit.

Dr. Steven Crane, Founder of Financial Legacy Builders, agrees, “Most people don’t realize you don’t have to be rich to get taxed as if you are. One big year, selling a business, exercising stock, or even a large retirement withdrawal, can push you into a bracket you’ve never been in before. Rather than your lifestyle, it’s about when the income hits. The biggest win I’ve seen is simple in theory but hard in practice: controlling when income shows up. Most people focus on how much they make, but taxes are driven by timing. Spreading income out over multiple years makes the difference between keeping control and unnecessarily handing over a big chunk of change. I tell clients to stop thinking of big financial moves as single events and start thinking of them as sequences. You don’t have to do everything at once. Whether it’s stock options, a business sale, or withdrawals, breaking it up strategically can keep you out of brackets you never needed to be in.”

This is why you need to plan for your peak income years, and for when RMDs may push you into $1-million-plus taxable income.

Yes, you can move to a state that doesn’t have such a tax.

But for most people, it’s enough to pay close attention to properly timing your income and considering the tax implications of financial decisions.

However, that kind of planning is most effective when you do it long before the consequences hit.

Are You Ready to Hire a Financial Advisor?

You’ll find a growing number of financial advisors featured on Wealthtender. You can search based on the areas of specialization most important to you and where they’re located, or browse our financial advisor directory for more search options to find advisors who may be a good fit for you.

Find Your Next Financial Advisor on Wealthtender

📍 Click on a pin in the map view below for a preview of financial advisors who can help you reach your money goals with a personalized plan. Or choose the grid view to search our directory of financial advisors with additional filtering options.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

If you live in a high-tax state like California, New York, or Maryland, the idea of moving somewhere with no state income tax like Florida or Texas probably sounds like an obvious financial win. And for some people, it genuinely is. But the mistake most people make isn’t moving to a no-income-tax state, it’s treating a complex, life-altering decision as if it has a simple, single-variable answer. Because when you factor in what actually changes — property taxes, insurance costs, public services, infrastructure, and the less-quantifiable things like proximity to family — the math gets a lot more complicated than your last state tax return suggests.

Key Takeaways

1

Moving to a no income tax state saves money on one line item — but often raises costs on others.

States without income tax still need revenue, so they typically offset it through higher property taxes, sales taxes, and fees. According to Tax Foundation data, Florida and Texas have lower overall per-capita tax burdens than the national average — but the gap may be smaller than your income tax bill alone suggests, especially once housing, insurance, and daily living costs are factored in.

2

This is a full-life tradeoff decision, not a tax decision.

Moving to a lower-tax state means accepting a different mix of public services, infrastructure quality, insurance costs, and distance from family — none of which show up in a tax calculator. Financial advisors consistently report that lifestyle factors, proximity to family, and day-to-day quality of life matter more to their clients than tax savings once the move is made.

3

The move makes the most sense when your tax savings are large, your lifestyle tradeoffs are acceptable, and you’ve pressure-tested your assumptions.

High earners in high-tax states like California or New York can see the largest absolute savings — potentially tens of thousands of dollars annually — which can justify the move when the non-financial tradeoffs are acceptable. The people most likely to be satisfied after moving are those who evaluated the full picture first, not just the headline tax rate.

Many people look at states with no income tax, like Texas and Florida, with more than a little envy. Especially high earners in high-tax states like California and New York think, “No state income tax? Sign me up!” And it makes a good bit of sense.

If you can legally stop paying tens of thousands of dollars in state taxes, why wouldn’t you?

As a Maryland resident paying the fourth-highest state-income-tax rates and fifth-highest overall taxes in the nation, I get the appeal. I pay much more in taxes than someone in a similar financial situation living in Florida (5th-ranked overall tax competitiveness index in the nation) or Texas (7th-ranked). But I know what this buys me, and the tradeoff works for me.

That’s the part that’s critical to think all the way through, but that not many do.

Yes, moving to a no-income-tax state can absolutely lower your tax bill. But that doesn’t necessarily translate into an overall improvement of your life, or even of your financial picture. In many cases, the costs just shift to different budget line items.

Moving to a no-income-tax state isn’t necessarily a mistake in all cases. The mistake is to use a single variable, like state income taxes or even the overall state tax burden, to make a life-altering decision that depends on far more than just taxes.

To make this decision wisely, you have to recognize that it isn’t really a tax decision. It’s a full-life tradeoff. And if you miss this critical point, you risk experiencing a major disappointment, as your expected savings from taxes, after accounting for how other expenses change, may be far smaller than you expected.

Worse, you may find that there are other, non-financial impacts that you wouldn’t have chosen to live with.

You’re already working hard to improve your situation, so the last thing you want is to shortcut the assessment phase and make a move that seems like a no-brainer on its surface, but that ends up providing smaller benefits alongside unexpected, unwelcome side effects.

Because your goal isn’t just to pay lower taxes. It’s to actually be better off, which requires making a solid, fully thought-out decision, not a reckless one.

Benjamin Simerly, CFP®, Founder & Wealth Advisor, Lakehouse Family Wealth, observes that financial gain is the least important aspect of deciding on a move, “I truly believe the biggest factor that should determine where you live is lifestyle. No matter the politics or taxes, good, bad, left, right, of any area, things like traffic, proximity to desired friends and activities, ease of lifestyle, length of time at the grocery store with level of business, etc., become the real decision makers.

“The kicker is that I’ve seen lifestyle be the reason younger folks move to the city, and older folks (with more emphasis on day-to-day ease) move to lower-tax areas.

“Ironically, the more retirement communities pop up for truly active lifestyles, especially closer to where grandchildren might live, the less I imagine people might move because of taxation. So, moving to be close to grandchildren for healthy reasons can be great.With planning, taking advantage of time with family is the number 1 win we see.”

The Tax Savings Are Real, But Incomplete

This is the simple part that most people get right. States like Texas and Florida don’t just have no income taxes. They have a lower overall per-capita tax burden than most states.

According to 2022 data from the Tax Foundation, the average combined per-capita state tax burden in the US is $7,109. Florida comes in at $4,914 (4th lowest), and Texas comes in at $5,469 (17th lowest).

That’s significant. This is why, especially for high earners from high-tax states like California or New York, moving to a no-income-tax state like Florida or Texas can lead to real tax savings. That’s why I’m not arguing that making such a move is a bad idea.

The mistake is assessing such a multi-factor decision through just that single factor. Because when you’re trying to improve your situation without unnecessary risk, it’s easy to latch onto something that looks like a clear win.

But while lower taxes can absolutely help, they don’t guarantee a better outcome. If you don’t consider all the tradeoffs that come with it, you can’t tell if you’ll actually be better off and happier after moving.

When something feels like an obvious win, especially in a complex decision, it’s usually worth slowing down and asking what you might be missing.

What Actually Changes When State Income Tax Goes Away

Obviously, as you’d expect in a no income tax state, the state income tax budget line-item goes to zero.

Win!

But is it truly that simple?

Not really.

All states levy taxes to fund government operations like public safety, courts, water systems, roads, bridges, and other core services. And states also differ in the services and programs they choose to fund.

When a state chooses not to tax income, it still has to fund whatever functions that state’s government takes responsibility for.

So, the question is not whether they’ll collect taxes. It’s what they’ll tax, who will pay those taxes, and what level of services they will fund.

And that’s something you need to evaluate before you move, not after.

If you stop your analysis at, “No state income tax? Win!” it’s easy to think you’ve found a simple way to reduce your costs without much downside.

John Davis, CFP®, EA, founder of JKD Financial, agrees, “The biggest thing people overlook is the total tax impact. States with no income tax still have funding needs (roads, schools, etc.); they just use other revenue sources to meet those needs. This comes in the form of higher property taxes, sales tax, and overall higher fees for normal government programs. These taxes add up and often create a similar out-of-pocket expense as income taxes.

“One of the biggest things I see with my clients, who are mostly near or at retirement, is the additional travel costs. Many of my clients move away from family to no-tax states. Because of that, they end up spending more to either go back to visit family or pay for children and grandchildren to come visit them. This takes away from their travel budget elsewhere, as well as time available to do other trips. I often call the cost of flights and hotels to maintain those family connections the ‘grandkids tax.’

“My recommendation is to start with your desired lifestyle, then do the math. You should look at your income as it currently stands, what you project in retirement, and how that’s taxed in your current state. Many people don’t realize their current state may already exempt their biggest income sources, like Social Security, pensions, or capital gains. These are common income sources for retirees. If your effective tax rate is already low, the friction and cost of moving might be greater than your actual tax savings.”

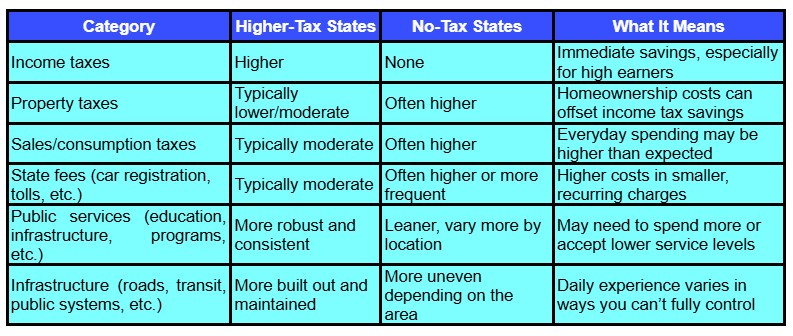

In reality, you may find a move to a no-tax state has unexpected consequences you won’t be as happy about, such as:

High property taxes that increase the burden on homeowners.

High sales or consumption taxes that increase the burden on consumers.

High state fees that increase the burden on, e.g., drivers.

Leaner government services that push many expenses onto individuals and families.

More travel expenses to maintain family relationships.

Thus, real income-tax savings aren’t free.

You may pay nothing through one channel – state income tax, but more through others. Some costs will be obvious. Others show up in different ways, like weaker infrastructure, fewer public services, or higher out-of-pocket spending.

That’s why moving to a no-tax state may be riskier than it appears if you don’t look beyond the headline tax savings.

People who make this move often don’t realize they’re not just reducing taxes. They’re stepping into a different system with different tradeoffs. You may think it’s a straightforward tax decision, but in reality, whether you realize it in the moment or only much later, you’re choosing a different mix of taxes, expenses, services, and tradeoffs.

That means the real question isn’t whether you’ll pay less in taxes. It’s whether you’ll actually be better off living in that new system.

And that’s something you need to evaluate before you move, not after.

The Tradeoff: You Pay Less, and You Often Get Less

No question, paying lower taxes is helpful.

But it isn’t a standalone outcome. It comes with a tradeoff. You aren’t just lowering taxes. You’re changing the wider picture of how you pay and what you get, as we see in Table 1.

Table 1. Tradeoffs that accompany a move to a no-income-tax state may be unwelcome.

This gives you a practical way to assess whether the move actually improves your situation, instead of assuming it will be based on a single factor – state income tax. Rather than “Is paying lower taxes worth the hassle of an interstate move?” your real decision should thus be “Is this overall tradeoff worth it to me?”

Instead of a pure reduction in expenses due to lower taxes, you need to realize that you’re moving to a completely different mix of costs, services, and experience.

You may be happy with some parts of the change and unhappy with others. Unfortunately, if you don’t consider everything carefully beforehand and do your due diligence, you may get blindsided by some of the changes, especially non-financial ones like the consistency and quality of the infrastructure and environment you’ll have to live with.

That’s a much broader decision than most realize when they consider moving to a state where their income tax burden will be lower.

When Moving to a No Income Tax State Makes Financial Sense

In some cases, moving to a no-tax state is exactly the right decision.

For that to be true, certain conditions need to be met that tilt the above-mentioned tradeoff strongly in your favor. First and foremost, you need to be ok with the change in community, moving away from friends and (possibly) family, and the change in your professional environment.

Beyond that, here are some specific cases.

1. Your Tax Savings Are Large Relative to Your Lifestyle Changes

If you’re a high earner living in a high-tax state, your tax savings could amount to many tens of thousands of dollars a year.

For example, a single filer making $500k a year in California, taking the standard deduction, and maxing out their 401(k) contribution would pay about $41k in state income taxes alone.

Moving to, e.g., Texas, even assuming no change in salary, saves that large tax payment.

That can justify the move, especially if:

You’re happy with your expected housing situation.

Your day-to-day spending doesn’t increase too much.

You don’t rely too much on any services that are reduced or less consistent in the place to which you move.

If that’s your situation, the tradeoff is simple and highly beneficial. You give up little and have a big financial win.

2. You’re Not Heavily Dependent on State-Provided Services

Not everyone relies on public services to the same extent.

If you have no school-age kids, you aren’t directly affected by the level of state investment in K-12 education.

If you prefer to drive everywhere, public transport, or lack thereof, is of little concern (though you may want to consider possible impacts on traffic congestion and air quality).

If you don’t use local support systems, having a leaner state government doesn’t affect your quality of life too much.

If the above are all true for you, the tradeoff is, again, a net plus.

3. You’re Willing and Able to Replace What the State Doesn’t Provide

This is a trickier one.

If you do use state-provided services where you live now, and those won’t be provided for you in your new state, you’ll need to replace them or do without.

This can include:

Education options and quality for your school-age kids – private schools are notoriously expensive.

Healthcare access and quality – especially if you’re not in great health, high-quality hospitals that get less state funding are more expensive.

If your new location suffers from poorly maintained infrastructure, that poses inconveniences and even safety concerns that can’t be addressed privately.

If you move to, e.g., Florida, homeowner insurance will likely be more expensive and even hard to obtain in some locations.

If, after considering all these and similar factors, the net savings is still large enough, a move can make sense.

4. Your Values and Lifestyle Preferences Align with the Tradeoff

Some people simply prefer lower taxes, a leaner government that’s less intrusive, and different regional priorities and values.

If these, as they are in your target state, are better aligned with your values and preferences than what you experience now, a move can make sense even if the financial factor isn’t a strict win.

What Does This Mean for Your Decision?

Moving to a no-tax state isn’t overall “right” or “wrong.”

It can be a net positive or a net negative, depending on your personal situation and preferences, and how well the tradeoffs match them.

As long as:

The savings are large enough to be an important factor for you,

The tradeoffs are acceptable to you, and

You’re prepared for the changes you’ll experience.

As long as those conditions are true, the move can work very well.

But if even one of them doesn’t hold, the outcome becomes much less predictable.

That’s when what looks like a clear financial win can turn into a frustrating tradeoff, where the savings are smaller than expected, and the downsides are harder to live with, if not outright unacceptable.

When Moving to a No-Tax State Can Fall Short or Even Backfire

It’s a big decision, and if you’re not careful, things can fall apart.

Yes, it may save you tens of thousands of dollars on paper, but once you consider all the other financial implications, the outcome may not be as favorable as it looks on the surface.

Even more importantly, your new life may fall far short of your expectations, or even short of your current situation, sometimes in ways that aren’t obvious until after the move.

Here are some possible scenarios where this could happen.

1. Your Costs Shift More Than Expected

After the move, you may face higher insurance costs, higher day-to-day expenses due to higher sales tax, and major out-of-pocket expenses for things you don’t want to give up and that are state-funded or state-subsidized in your current state but not in your target state.

If these increases are large enough, they’ll offset much of your state income tax savings.

This may make the benefit of the move too small to justify the non-financial impacts.

2. The Non-Financial Impacts Matter More Than You Thought

Knowing your state income tax is as simple as looking at last year’s state tax return, or possibly asking your accountant for their estimate for the current tax year.

That’s how easy it is to figure out the likely maximum financial benefit.

What isn’t as easy is quantifying and assessing the impacts of:

Lower infrastructure quality.

Healthcare access, quality, and consistency.

Public school quality.

Environmental factors.

General day-to-day convenience.

Connection to family.

These don’t show up in your budget.

But they can have a massive impact on how enjoyable you may find living in your new location. In ways that are hard to ignore once you’re experiencing them daily.

If these things matter to you enough, they can make the move feel like a big mistake, even if the financial impact is positive.

As Simerly says, “The biggest tradeoff that surprises people after they move to a lower-tax state is lifestyle. Tax changes tend to come with lifestyle changes, more or less traffic, more or less time for fun, and more or fewer friends. And my clients who moved to lower-tax areas appreciate lifestyle improvements most. I saw the tax numbers change, but clients saw both their disposable income and the time available to spend it increase. These lifestyle factors tend to be far more important to them than the lower tax.

“If you’re considering moving, my top recommendation is to talk with your children! I’ve met more than a few couples who made a big move, only to have a new grandchild born five states away 6 months later. Family can be the biggest driver of a potential move, no matter the tax changes. The things you can’t replace aren’t things; they’re family.

“If you’ve saved money and have enough to retire comfortably, you can likely afford the extra taxes. The fun you have in retirement, and the time you spend with people and hobbies you care about, these will be far more important.”

3. Your Situation Changes After You Move

Your move may make perfect sense today, even considering the non-financial factors.

But life changes.

Your health could deteriorate.

You may not have kids now, but that could change, and they need to attend school.

Your preferences may evolve.

If this happens, a move that made sense under one set of assumptions may become less attractive.

It isn’t that this would necessarily mean the move was a mistake, but it does imply that you should try to have a wider margin to accommodate such potential changes.

What Does This Mean for Your Decision?

The core mistake people make when making a move that turns out badly is making a multi-factor decision based on single-factor thinking.

When you do this, it’s too easy to:

Make a shallow assessment.

Overestimate the value of the benefit.

Underestimate, or even ignore, the tradeoffs.

This is how what should have been a deep dive into a complex life-changing decision gets inappropriately seen as a slam-dunk no-brainer.

This isn’t to say you shouldn’t move.

It’s to make sure that you don’t short-change your decision-making process.

Because when you broaden your lens, the decision becomes less obvious, but once made, it’s more likely to work out well.

As Dr. Steven Crane, Founder of Financial Legacy Builders, says, “The biggest thing many people miss is that taxes don’t exist in a vacuum. They fixate on state income tax and ignore everything else, property taxes, insurance, cost of living, and even how income is sourced. I’ve seen people move, thinking they’re saving money, only to realize the total picture didn’t change much.

“A lot of people are surprised that life doesn’t automatically get cheaper just because income taxes go away. Housing, insurance, and everyday costs can offset a big chunk of the savings. And beyond money, you’re also dealing with lifestyle changes, being further from family, different services, and a different pace of life. That stuff matters more than people expect.

“I tell clients to run the full picture, not just the headline tax rate. Look at your actual spending, your income sources, and how everything changes in the new state. Then stress-test it. If the move only works on paper but not in real life, it’s probably not the right move. Taxes are important, but they shouldn’t be the only reason to pick where you live.”

How to Actually Evaluate This Decision

Now that you recognize this isn’t a simple tax-reduction decision, here’s a simple, structured way to assess it broadly enough to make a better-informed choice.

Step 1: Quantify the Real Financial Benefit

First, obviously, figure out your expected state income tax savings (accounting for the federal deduction, if you itemize). Then, adjust for other financial impacts:

How will your housing costs change, including property taxes?

How will your daily cost of living change, including sales taxes?

How will your homeowner’s insurance and other policy premiums change?

What things will you need to pay for, which are currently free through state funding, and how much will they cost?

Absolute precision isn’t possible or necessary here.

But directionally, will you save a lot? Enough?

As Simerly says, “In our experience with clients, the most overlooked factor, with the biggest budget impact, lies in everyday expenses, not the primary income tax itself. Gas costs, contractor rates, commodities, goods and services, etc., tend to make the biggest differences in our clients’ budgets, especially in the major categories of transportation and housing-related concerns. Of course, you should always do your own math. If you travel a lot and don’t spend much money at home, these expenses may not be a real concern for you.”

Step 2: Identify What Will Change in Your Day-to-Day Life

Next, look beyond the numbers:

What services and infrastructure do you rely on today?

How will these be different in your new state?

Which of these changes matter to you, and to what extent?

These things can’t be captured in a spreadsheet, but they can make your overall daily experience positive or, conversely, an emotional drag.

Step 3: Pressure-Test Your Assumptions

This is a critical step that many people miss.

Rather than simply assuming everything will work out just fine, start with an assumption that it won’t, and figure out what could cause that negative outcome.

Ask yourself:

What would have to go wrong to make this move feel like a big mistake?

How likely is it for these things to happen?

How confident am I that I’m not missing other risks?

If you’re struggling to answer these questions clearly and with confidence, you’re not done assessing the move.

Step 4: Decide if the Tradeoff Is Worth It for You

There isn’t a universal answer for this question.

But that’s ok, because you don’t need to answer it for everyone, just for you.

If:

your expected net financial benefit is meaningful,

the tradeoffs are acceptable (or even appealing), and

you’re comfortable with the risks,

Then the move makes sense for you.

If not, even with a heavier tax burden, staying put is the better choice.

The Bottom Line

Moving to a no-income-tax state can be very good for your finances.

But that alone isn’t enough to make a solid, well-informed decision.

For that, you need to consider and accept the tradeoffs. The people who are most likely to benefit from such a move aren’t necessarily the ones who pay the most in state income taxes.

They’re the ones who take the time to fully explore and understand all the consequences and tradeoffs of such a major life-changing choice and make a decision that leaves them truly better off, not just paying lower taxes.

Are You Ready to Hire a Financial Advisor?

You’ll find a growing number of financial advisors featured on Wealthtender. You can search based on the areas of specialization most important to you and where they’re located, or browse our financial advisor directory for more search options to find advisors who may be a good fit for you.

Find Your Next Financial Advisor on Wealthtender

📍 Click on a pin in the map view below for a preview of financial advisors who can help you reach your money goals with a personalized plan. Or choose the grid view to search our directory of financial advisors with additional filtering options.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Do you work at Arizona Public Service Company? Get the resources you need and expert insights from financial professionals who specialize in helping Arizona Public Service Companyemployees make the most of their compensation package and benefits.

Whether you’re a new Arizona Public Service Company employee or you’ve moved up the ranks into a management or executive leadership role over a multi-year career, it’s important to make smart money moves with your income and employee benefits. For example:

✅ Do you know the right moves to make to get the greatest value from the Arizona Public Service Company benefits available to you?

✅If you’re thinking about leaving Arizona Public Service Company for another job or planning to retire from the company in a few years, are you taking the right steps today to ensure you will receive all of the compensation and benefits that you’ve earned?

Get the Most Value from Your Arizona Public Service Company Benefits and Compensation Package

Throughout the year, Arizona Public Service Company provides its employees and executives with updates about their benefits ranging from health insurance and health savings plans to retirement plans like a 401(k) and deferred compensation plans. While the company offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Arizona Public Service Company who specialize in helping Arizona Public Service Company employees make the most of their income and benefits.

Whether you work in the Arizona Public Service Company headquarters in Phoenix, Arizona, another office location around the country, or remotely from home, you may have questions about your compensation package and benefits better suited for a financial professional who can offer unbiased advice and guidance.

For example, sensitive topics like discussing the steps you should take before quitting your job at Arizona Public Service Company to work elsewhere or or deciding when you should plan to retire are all conversations that may be more comfortable with a trusted financial advisor.

Should you hire a Arizona Public Service Company specialist financial advisor or an advisor close to home?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in serving Arizona Public Service Company employees.

Fortunately, many financial advisors offer virtual services so you can meet online no matter where you (or they) live.

This means you can choose to hire a specialist financial advisor who lives hundreds of miles away if you decide their knowledge and experience working with Arizona Public Service Company employees is a better fit to help with your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Arizona Public Service Company employees to help them make smart decisions to get the most value from their compensation and benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Do you have questions not yet answered? Use the form below to submit questions anonymously and watch this article for updates with answers to your questions. You can also reach out to the financial advisors below to set up an introductory call or contact them with your questions by email.

💸 Smart Money Insights for Arizona Public Service Company Employees & Executives

This page is organized into sections to help you quickly find the information you need and get answers to your questions:

Q&A: Financial Planning Tips for Arizona Public Service CompanyEmployees & Executives

Get Answers to Your Questions About Your Arizona Public Service CompanyBenefits and Career

Browse Related Articles

Q&A: Financial Planning Tips for Arizona Public Service Company Employees & Executives

Answers to Employee Questions with Karen Koenig

Karen Koenig is a financial advisor based in Surprise, Arizona who specializes in offering financial planning services to Arizona Public Service Company employees. Karen helps her clients get the most value from their Arizona Public Service Company benefits and compensation package so they can enjoy life and feel confident about their financial future.

Q: Is there a particular benefit available to Arizona Public Service Company employees you feel isn’t as well utilized or understood by employees as it should be?

Karen: The defined benefit (DB) pension plan at APS is usually not well understood and/or the difference between it and the 401(k) plan, especially if the employer has both. A defined benefit (DB) plan is an employer-sponsored retirement plan that guarantees a fixed, monthly payout for life, based on a formula considering salary and years of service. Unlike 401(k) plans, the employer bears the investment risk, promising a specific benefit regardless of market performance.

Q: Beyond Arizona Public Service Company employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients?

Karen: I like to talk about several things beyond APS company benefits with my clients to include Education Planning (529 Plans), Taxable Brokerage / Non-Qualified Investment Accounts, Insurance as a Strategy (Not Just Protection), Long-Term Care & Healthcare Planning, Estate & Legacy Planning Integration, and Cash Flow & “Lifestyle Design” Planning. There are many things a person can do to plan for retirement beyond what a company provides for them, and this gives a two-pronged approach to retirement savings.

Q: For Arizona Public Service Company employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

Karen: For employees at Arizona Public Service, retirement isn’t about replacing income from one source—it’s about turning multiple moving parts into one coordinated paycheck. In retirement you need to Understand Your “Income Floor”, Identify the Gaps, Turn Savings into Income (The Right Way), Plan for Taxes, Solve for Healthcare Early, and Build in Flexibility and Confidence. The key is: A pension + savings + benefits = A system working in your favor.

Get to Know Karen Koenig, Financial Advisor for Arizona Public Service Company Employees:

Are you a financial advisor who specializes in working with employees at Arizona Public Service Company or another large company?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with employees at Arizona Public Service Company or another large company. (Subject to availability and terms.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender ✅ Or request more information by email:

🙋♀️ Have Questions About Your Arizona Public Service CompanyBenefits or Career?

Get answers from the Wealthtender network of financial professionals and educators.

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

About the Author

Brian Thorp

Founder and CEO, Wealthtender

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Do you work at Lyra Health? Get the resources you need and expert insights from financial professionals who specialize in helping Lyra Healthemployees make the most of their compensation package and benefits.

Whether you’re a new Lyra Health employee or you’ve moved up the ranks into a management or executive leadership role over a multi-year career, it’s important to make smart money moves with your income and employee benefits. For example:

✅ Do you know the right moves to make to get the greatest value from the Lyra Health benefits available to you?

✅If you’re thinking about leaving Lyra Health for another job or planning to retire from the company in a few years, are you taking the right steps today to ensure you will receive all of the compensation and benefits that you’ve earned?

Get the Most Value from Your Lyra Health Benefits and Compensation Package

Throughout the year, Lyra Health provides its employees and executives with updates about their benefits ranging from health insurance and health savings plans to retirement plans like a 401(k) and deferred compensation plans. While the company offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Lyra Health who specialize in helping Lyra Health employees make the most of their income and benefits.

Whether you work in the Lyra Health headquarters in Burlingame, California, another office location around the country, or remotely from home, you may have questions about your compensation package and benefits better suited for a financial professional who can offer unbiased advice and guidance.

For example, sensitive topics like discussing the steps you should take before quitting your job at Lyra Health to work elsewhere, protecting yourself in advance of a corporate layoff, or deciding when you should plan to retire are all conversations that may be more comfortable with a trusted financial advisor.

Should you hire a Lyra Health specialist financial advisor or an advisor close to home?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in serving Lyra Health employees.

Fortunately, many financial advisors offer virtual services so you can meet online no matter where you (or they) live.

This means you can choose to hire a specialist financial advisor who lives hundreds of miles away if you decide their knowledge and experience working with Lyra Health employees is a better fit to help with your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Lyra Health employees to help them make smart decisions to get the most value from their compensation and benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Do you have questions not yet answered? Use the form below to submit questions anonymously and watch this article for updates with answers to your questions. You can also reach out to the financial advisors below to set up an introductory call or contact them with your questions by email.

💸 Smart Money Insights for Lyra Health Employees & Executives

This page is organized into sections to help you quickly find the information you need and get answers to your questions:

Q&A: Financial Planning Tips for Lyra HealthEmployees & Executives

Get Answers to Your Questions About Your Lyra HealthBenefits and Career

Browse Related Articles

Q&A: Financial Planning Tips for Lyra Health Employees & Executives

Answers to Employee Questions with Maria Castillo Dominguez, CFP®, EA

Maria Castillo Dominguez is a financial advisor based in Hollywood, Florida who specializes in offering financial planning services to Lyra Health employees. Maria helps her clients get the most value from their Lyra Health benefits and compensation package so they can enjoy life and feel confident about their financial future.

Q: As a financial advisor with experience helping Lyra Health employees save for their retirement, how do you help them make the most of their employee benefits?

Maria: I help employees look at their benefits as part of a broader strategy, rather than treating each decision in isolation. That often includes coordinating retirement benefits such as a 401(k) and HSA alongside equity compensation, tax planning, estate planning, and long-term investment strategy. Given Lyra Health has appeared in public reports as a potential IPO candidate, I also believe it can be valuable for employees to evaluate planning opportunities before a major liquidity event, particularly where private company equity may represent a meaningful part of their overall financial picture. Some of the most valuable planning decisions often happen before a major event occurs, not after.

Q: When you first speak with a Lyra Health employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

Maria: During my first conversation, I usually want to understand both the equity compensation picture and the broader financial picture, because they often influence each other. I typically want to understand what forms of equity they hold, whether a significant portion of their net worth may be tied to private company equity, and how they are thinking about liquidity, taxes, and long-term goals. But I also want to understand things beyond equity, including cash flow, emergency reserves, retirement savings, tax exposure, insurance coverage, estate planning, and whether major life decisions, such as buying a home, starting a family, or changing jobs, may be tied to assumptions about future equity outcomes. I also like to understand how they are using other benefits available to them, such as retirement plans, health savings accounts, and other planning opportunities that may be easy to overlook. In my experience, understanding the full picture often matters more than focusing on any one benefit in isolation.

Q: Is there a particular benefit available to Lyra Health employees you feel isn’t as well utilized or understood by employees as it should be?

Maria: Incentive stock options (ISOs) are often one of the biggest planning opportunities I see employees overlook. Many employees focus on the potential upside of the shares, but spend less time looking at whether exercising some options earlier may create tax planning opportunities. If a company is approaching a possible IPO, even with uncertain timing, it may be worth evaluating whether exercising before a future increase in valuation could be beneficial. A lower valuation may mean a smaller spread between the exercise price and fair market value, which can reduce AMT exposure and may allow an employee to exercise more shares before AMT becomes a concern. In some cases, waiting until later can make those decisions more expensive from a tax perspective.

Q: What are some of the unique financial planning challenges you commonly see among your clients who are Lyra Health employees and how do you help them overcome these obstacles?

Maria: One challenge I commonly see is employees underestimating both the risks and planning opportunities tied to their equity compensation, particularly with double-trigger RSUs and ISOs. With double-trigger RSUs, vesting often depends on two conditions being met: first, the time-based service condition, and second, a liquidity event such as an IPO. Employees may have accumulated a substantial number of shares that have met the service condition, but have not yet become taxable because the second trigger has not occurred. When that second trigger occurs, those shares vest and become taxable compensation income at all once, which can create significant tax increase.

I also find employees may underestimate two related risks. First, statutory tax withholding on RSU income is often around 22%, which may be insufficient for higher-income employees and can create underwithholding risk. Second, if shares are subject to a post-IPO lockup period, often around 180 days though terms can vary, employees may face a situation where taxes are due before they have full access to the shares or liquidity to help cover those obligations.

For employees with ISOs, I also often see questions around whether there may be value in evaluating exercises before a future financing round or liquidity event that could result in a higher valuation. In some cases, a lower spread between the exercise price and current market value may create an opportunity to exercise more shares before AMT becomes a constraint. If the valuation increases later, the spread may be larger, which could trigger AMT sooner and limit how many options you can exercise before AMT triggers.

These are highly personal decisions, but they are often areas where planning ahead can create more options than waiting until decisions become compressed by timing or tax consequences.

Get to Know Maria Castillo Dominguez, Financial Advisor for Lyra Health Employees:

Are you a financial advisor who specializes in working with employees at Lyra Health or another large company?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with employees at Lyra Health or another large company. (Subject to availability and terms.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender ✅ Or request more information by email:

🙋♀️ Have Questions About Your Lyra HealthBenefits or Career?

Get answers from the Wealthtender network of financial professionals and educators.

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

About the Author

Brian Thorp

Founder and CEO, Wealthtender

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Ownership typically drives the transfer path. How an asset is titled often determines whether it passes through probate, by beneficiary form, or directly to a surviving co-owner.

Tax treatment depends on the asset inherited. Retirement accounts, real estate, taxable investment accounts, and life insurance can all create very different results for heirs.

A stronger plan connects every moving part. Trusts, powers of attorney, beneficiary forms, and transfer tools work best when they are built to support the same outcome.

Preserving wealth across generations starts with ownership, authority, and transfer design. Idaho families often hold a mix of homes, investment accounts, retirement plans, business interests, and family property that do not all move the same way to those next in line.

Those differences are what make coordination matter. When titles, documents, tax exposure, and decision-makers are lined up in advance, a transfer plan is easier to carry out and far less likely to create delay, confusion, or unintended results.

What Controls Transfers Under Idaho Law

A transfer plan starts with the rules that decide which assets go through court, which pass by contract, and which move automatically under title. In practice, the outcome usually comes down to how an asset is owned, whether a valid will in Idaho exists, and whether a beneficiary form or survivorship feature already controls the transfer.

In Idaho, the probate court process is used to handle property that does not automatically transfer after someone passes away. That can include admitting a will, appointing a personal representative, collecting probate property, paying valid debts and claims, and distributing what remains.

A valid written will generally must be signed by the person making it, or by another person at that person’s direction and in that person’s conscious presence, and it generally must be signed by at least two witnesses.1 Wills must also be signed in the presence of a notary public. A will governs probate property, but it does not control assets that already pass by contract or title, such as property held with survivorship rights or accounts with stated beneficiaries.

Idaho Intestacy Rules and When They Apply

Idaho intestacy rules apply when someone passes away without a valid will, or when part of an estate is left outside the structured plan. When that happens, it could be left up to Idaho law to decide who receives the assets.

Here’s a general overview of Idaho’s intestacy rules:2

If a person passes away, leaving children but no spouse, the children receive the estate.

If a person passes away, leaving a spouse but no descendants or surviving parents, the spouse receives everything.

If a person passes away, leaving parents but no spouse or descendants, the parents receive the estate.

If a person passes away, leaving a surviving spouse and descendants, the spouse receives all community property plus 50% of separate property, and the descendants receive the remaining 50% of separate property.

If a person dies leaving a spouse and surviving parents, the spouse receives all community property plus 50% of separate property, and the parents receive the remaining 50% of separate property.

How Idaho Assets Commonly Pass at Death

After the basic rules are clear, the next step is looking at how transfers usually happen outside the abstract legal framework. This is often where families find planning gaps, especially when account registrations, deed language, and beneficiary designations have not been reviewed in a long time:

Solely owned property: A home, bank account, or other property held in one person’s name with no built-in transfer feature will often become part of probate in Idaho.

Assets with named beneficiaries: Retirement accounts, life insurance, and many financial accounts usually pass according to the beneficiary form on file rather than under the will.

Property with survivorship rights: Married couples in Idaho can hold personal property as community property with right of survivorship, which can allow the deceased spouse’s interest to pass directly to the surviving spouse when the title is set up correctly.3