Most investors think of private markets as a way to diversify beyond stocks and bonds. That’s true, but for high-income earners, the more compelling reason to pay attention may actually be the tax advantages. The right private market investments don’t just add return potential. They may help reduce what you owe.

But the tax benefits don’t exist in a vacuum. To understand why they matter, it helps to first understand what makes private markets worth considering in the first place.

Diversifying Outside Public Markets

Private equity offers exposure to companies and sectors that aren’t (and may never be) available through public exchanges. As part of a diversified portfolio, they can help certain investors reduce their reliance on a narrow group of public market leaders.

Beyond exposure to new opportunities, private markets may help reduce exposure to stock market volatility. While the stock market is heavily driven by investor sentiment, private investments are typically valued at periodic intervals and carried forward with a longer-term mindset. This structure can lend itself well to more intentional tax planning, since transactions and movements happen less frequently.

Finding Private Market Opportunities to Manage Taxes

Private market investors may have access to certain specialized investment vehicles, like tax-aware hedge funds, which are built to maximize after-tax returns. Unlike traditional hedge funds that focus primarily on returns and “hedging” against volatility, tax-aware hedge funds are specifically designed to offset ordinary income that you recognize from a W-2, investment interest, or even a Roth conversion. Another effective tax strategy, designed to harvest capital gain losses, and one of the most effective tools for managing longer-term capital gains taxes, is the long/short separately managed account, or SMA, which we’ll get into below.

Leveraging Separately Managed Accounts (SMAs)

Using long/short separately managed accounts (SMAs), investors harvest capital losses more strategically to offset a large taxable event.

Here’s how it works: A tax-aware long and short SMA helps investors intentionally realize losses in certain positions while maintaining overall market exposure. Those realized losses can be held and carried forward for future use. When a significant taxable event occurs, those stored losses may be used to offset capital gains. This strategy can also be used to divest a highly concentrated stock position.

Such a strategy can create loss harvesting flexibility for certain people, including:

Business owners or shareholders preparing for an exit

Executives with a significant amount of company stock

Investors preparing to sell off a large amount of highly appreciated stock

Rather than scrambling to reduce a tax bill after the fact, a long/short SMA strategy leverages losses that have already been generated and positions them strategically in advance.

Selecting a Manager

The key to accessing and leveraging the tax-saving capabilities of the private market is to work with the right manager. Not all managers have the expertise or discipline to execute a long/short SMA strategy effectively. It requires careful tax management, consistent monitoring, and a long-term focus.

When evaluating managers, look for a documented track record of tax-loss harvesting results, transparent reporting on after-tax performance, and clear communication about how they manage around taxable events. A manager who can’t clearly explain their tax management process probably isn’t prioritizing it.

It may be worth the extra time and research to find a manager with a proven history of successfully pursuing private market tax opportunities. Doing so may help improve your eventual tax savings and ability to achieve potentially higher returns.

Considering Real Assets

Not all investment income is taxed the same way, and in private markets, that distinction can work in your favor. Private market opportunities come in many forms, including real estate funds, which can generate ongoing income that’s treated differently than traditional dividends or bond interest — often in ways that favor the investor.

Private real estate, for example, gives investors access to depreciation, a tax benefit that can offset a portion of the income generated by the investment. The result is that investors may receive cash flow while recognizing less taxable income than they would from a comparable public market investment. Keep in mind that depreciation benefits can vary depending on your income and how the fund is structured, and they may be partially recaptured when the investment is sold. It’s one of those areas where the details matter, and a knowledgeable advisor can help you understand what to expect.

Beyond the tax advantages, private real estate may also offer some cushion against inflation risk. Rental rates and property values are generally not as inflation-sensitive as other assets, and property owners may be able to adjust rents over time to help preserve purchasing power.

Real assets like private real estate can complement traditional stock and bond allocations by adding a different risk, return, and tax profile. For high-income earners already managing a significant tax burden, that’s one more reason to take a closer look at what private markets can offer, not just for growth, but for how income is generated and taxed along the way.

Is Private Market Investing Right for You?

While private markets can offer investors access to more diversified opportunities, they’re not right or accessible for everyone. In many cases, you will need to meet accreditation requirements to participate in certain investments (including hedge funds and private equity). There are varying levels of accreditation, so be sure you are transparent with your advisor and fund manager about your investable assets and what you own.

Accreditation aside, private market investing generally creates long-term commitments that lock up liquidity and may expose your capital to higher risk. While the potential trade-offs may be worth it depending on your goals, review the pros and cons with a knowledgeable advisor before moving your money around.

The strategies outlined here work best when they’re planned well in advance, not after a taxable event has already happened. If any of this resonates with your situation, it’s worth having a conversation sooner rather than later. Reach out to our team and let’s talk through what might make sense for you.

Ask an Advisor: The Hidden Tax Problem With Maxing Out Your 401(k) as a Top Earner

Image Credit: Wealthtender.

You’ve worked hard to get here. A high income, a growing portfolio, and the discipline to max out your 401(k) every year. By most measures, you’re doing everything right.

But here’s a question worth sitting with: do you actually know what your tax bill will look like when you start pulling that money out in retirement?

For high earners in the top tax bracket, the 401(k) is a powerful tool. It’s also one that comes with a future obligation that’s easy to underestimate. Understanding both sides of that equation is where smart retirement planning starts.

The Hidden Tax Problem with Large 401(k) Contributions

As you’re probably aware, your 401(k) is funded with pre-tax dollars, meaning contributions reduce your taxable income in the year they are made. The money in your 401(k) grows tax-deferred as well, which is a notable advantage since funds stay invested, uninterrupted by tax withdrawals, until they’re used in retirement.

Once retirement hits, however, you’ll need to start withdrawing from your account, either to fund your lifestyle or to fulfill required minimum distributions (starting at age 73, or 75 in 2033). Those withdrawals are taxable on both the principal and any growth earned in the account over time.

For high-earners facing today’s highest tax bracket, this future tax liability may be reason to pause and consider whether maxing out 401(k) contributions is worth it. But the larger issue at hand is about whether or not you have a strategic and proactive plan for managing those taxes come retirement, not how much you’re contributing today.

The Solution: Early Tax-Savvy Planning for Your Retirement Income

The traditional 401(k) contributions you make today lower your immediate tax bill—but they also create a future tax liability. Considering your lifetime tax obligations (not just the immediate tax savings) is the first step towards preserving more wealth in the long term.

Your tax liability in retirement is based on how your various income sources are treated.

This is particularly important for high earners to consider. Even if you’re in the highest tax bracket today, you have some control over how you’ll build your own paycheck in retirement—meaning your future annual tax rate could be lower.

In many cases, shifting your thinking ahead of time can set you up for a more tax-advantaged outcome in retirement, given that many solutions can take several years to execute effectively. With enough time and consideration, we can work together to identify the right opportunities to reduce your taxable income. Some potential tax-focused strategies include:

Maximize Backdoor Roth Conversions

A Roth conversion or mega backdoor Roth conversion are commonly used to lower taxable income in retirement. A Roth conversion converts pre-tax 401(k) dollars into after-tax (and potentially tax-free) dollars for retirement.

The challenge with Roth conversions is the more immediate tax liability they create. Any amount converted from a traditional 401(k) to a Roth account will be subject to ordinary income tax in the year the conversion is made. For this reason, it may take several years (even a decade or more) to strategically convert funds while keeping your lifelong tax liability in check.

Utilize Tax-Aware Hedge Funds to Offset Income

Tax-aware hedge funds may also be used to pass through ordinary losses and offset the earned income recognized when we convert 401(k) funds to a Roth account. These funds are structured to manage taxable distributions strategically, making large Roth conversions more manageable over time.

Incorporate a Cash Balance Plan for More Savings

Since 401(k)s include annual contribution limits, they may not provide enough savings potential to address a high earner’s retirement income needs. If you’re maxing out your 401(k) contributions and still looking to set aside more tax-advantaged savings, we can explore additional opportunities to save.

A cash balance plan, for example, serves as a hybrid option between a defined contribution (401(k)) and a defined benefit (pension) plan. These are structurally complex plans that may not be right for everyone, but they allow participants to set aside $100,000 or more annually in tax-deductible contributions. The tax treatment of these plans is very similar to a 401k and the Roth conversion and tax-aware hedge fund strategy can be used for cash balance plans as well, once you are no longer contributing to the plan.

Saving for Retirement as a High-Earner

Being a high-earner in the top tax bracket can present more challenges than most people realize, particularly when it comes to preparing for retirement. If you’d like to discuss your savings opportunities and challenges with a professional, reach out to our team of advisors anytime. We’d be more than happy to take a look at your current savings strategy and discuss opportunities based on your needs.

Have a Question to Ask a Financial Advisor?

When you’re uncertain about money matters, submit your question to Wealthtender, and it may be answered by a financial advisor in an upcoming article or in the Wealthtender Expert Answers Forum.

Need personalized help? Visit wealthtender.com to find the right financial advisor for your unique needs.

This article was originally published on Wealthtender and is intended for informational purposes only and should not be considered financial advice. You should consult a financial professional before making any major financial decisions. Wealthtender earns money from financial professionals, which creates a conflict of interest when these professionals are featured in articles over others. Read the Wealthtender editorial policy and terms of service to learn more. Wealthtender is not a client of these financial services providers.

About the Author

Sean Gerlin, CFP®, CPWA®, ChFC®, CLU®Creating Clarity Out Of Complexity

Areas of Focus

Alternative InvestmentsBusiness OwnersFinancial Life PlanningHigh Net WorthInvestment Management

Compensation Methods

Fee OnlyFlat FeePercentage of Assets ManagedSubscription

Sean Gerlin, CFP®, CPWA®, ChFC®, CLU®

| Envision Wealth Planners

[Asset and wealth managers are operating in one of the most demanding environments the financial industry has faced in decades. Margin pressure, scale imperatives, fee compression, AI-driven disruption, talent shifts, and rising client expectations are all converging at the same time.

Yet despite increasing complexity, distribution/sales teams are still often supported by fragmented training programs, disconnected tools, and episodic coaching initiatives. Firms are investing in activity — but not always building durable capability.

To explore what a modern professional development system should look like, we spoke with Mark Spina, Founder and Managing Partner at AlphaScale, and Tina Singh, founder of The GrowthStack.ai. The firms partner to build intelligence-led development systems that strengthen readiness, execution, and measurable business performance for asset and wealth managers.

The AlphaScale team uniquely combines former asset management distribution leaders with deeply experienced coaches who routinely work with financial advisors. That combination — understanding both the internal pressures of asset managers and the real-world expectations of advisors — informs how their professional development system is designed and reinforced.]

Hortz: What are the key challenges asset managers face in strengthening distribution performance today?

Spina: Through our experience leading asset manager distribution teams and now working alongside firms across channels and geographies, we consistently see three critical gaps limiting growth:

Competency – Inconsistent product fluency and narrative alignment. Reps may know features and benefits, but struggle to articulate portfolio role, thematic positioning, and risk framing with clarity and consistency. Narrative drift quietly erodes credibility.

Skills – Wholesalers often struggle to translate product knowledge into consultative, differentiated conversations. Discovery depth, objection navigation, and next-step clarity vary significantly across teams.

Measurement – Leadership lacks visibility into who is truly improving and what is actually working. Traditional training metrics measure attendance and completion — not readiness, judgment, or execution quality.

These gaps create invisible friction. Conversations appear active, but readiness and consistency are uneven. Mispositioning risk increases. Engagement suffers.

Hortz: How did you turn these observations into a professional development system?

Spina: We saw that most firms attempt to solve these issues through disconnected initiatives — a training here, a coaching session there, perhaps a new technology layered in. The result is activity without durable performance change.

High-performing asset managers, however, systematize their approach. They tie development to outcomes. They reinforce consistent messaging across teams. They create visibility into readiness. They build structured reinforcement loops.

Singh: Drawing on our experience leading distribution teams — and on our daily work coaching financial advisors — we helped design the AlphaScale Professional Development System to also reflect both sides of the conversation.

Asset managers need alignment, clarity, and measurable performance. Advisors expect relevance, context, and practical value. The system bridges those realities.

Hortz: What are the key components of the AlphaScale Professional Development System?

Spina: The system operates through three integrated pillars:

Activation (Product Intelligence) – Readiness on products, themes, and firm positioning.

Activation ensures that teams are prepared before they engage advisors. Through structured Product Intelligence, we evaluate and elevate readiness across product knowledge, market context, portfolio role, risk framing, and narrative discipline. This is not passive training. It is a progressive, gated development that measures applied understanding and aligns teams around the firm’s vision, outlook, and products.

Optimization (Sales Intelligence) – Intelligence and feedback on how readiness translates into sales and retention outcomes.

Optimization focuses on execution quality in real advisor conversations. Our Sales Intelligence layer evaluates how effectively teams structure conversations, conduct discovery, handle objections, and move toward clear next steps. Rather than relying solely on CRM activity metrics, we provide structured insight into execution patterns and coaching signals — without requiring call recording. This transforms activity into actionable intelligence. Leaders can see where conversations are strong, where friction emerges, and where targeted reinforcement will drive results.

Acceleration (Coaching Insights) – Professional development propelled by experienced managers and coaches using system insights to address weaknesses and amplify strengths.

Acceleration is where our hybrid model becomes particularly powerful. Our team includes former asset management distribution leaders who understand coverage models, product launches, and internal alignment pressures — alongside experienced coaches who routinely work with financial advisors and understand how advisors think, decide, and evaluate ideas. Together, they interpret system outputs and translate them into applied reinforcement — scenario-based coaching, strategic messaging alignment, and leadership guidance. Insights do not sit in dashboards. They drive behavior change that resonates with advisors.

Together, Activation, Optimization, and Acceleration create an operating rhythm that strengthens readiness before the call, execution during it, and reinforcement after it.

Hortz: How exactly does this system improve business results?

Singh: The system works because it closes the loop between readiness, execution, and reinforcement — informed by real advisor expectations. Activation reduces mispositioning risk and ensures narrative consistency. Optimization strengthens sales execution quality and highlights where conversion or retention opportunities are being lost. Acceleration ensures that insights are acted upon quickly and in ways that resonate with how advisors actually engage.

Spina: Over time, asset management firms see:

-Stronger advisor engagement.

-More consistent messaging across regions and teams.

-Reduced narrative drift.

-Faster readiness across new products or themes.

-Clearer visibility into what drives sales performance.

The goal is measurable behavior change — not event-based training.

Hortz: How does AlphaScale differentiate itself from other enterprise coaching and enablement platforms?

Singh: Many platforms focus on conversation analytics or training delivery. We operate at the intersection of readiness and execution — specifically for asset management distribution teams:

We do not rely on script adherence metrics.

We do not measure training completion as a proxy for proficiency.

We do not focus solely on deal inspection.

Instead, we evaluate:

Whether your team is truly prepared to represent products.

Whether narratives are applied consistently.

Whether execution quality supports retention and growth.

Where risk and opportunity signals are emerging.

Spina: And we reinforce those insights with practitioners who understand both asset manager realities and advisor expectations. That dual perspective is critical. Asset managers often optimize internally without fully accounting for how advisors interpret and respond. Our team operates on both sides of that equation.

The system is purpose-built for asset managers, combining intelligence infrastructure with real-world distribution and advisory expertise.

Hortz: What advice would you offer asset managers evaluating professional development investments?

Singh: Firms should ask these questions:

1. Does this initiative strengthen readiness before exposure to the market?

2. Does it improve execution quality in real advisor conversations?

3. Does it create leadership visibility into who is improving — and why?

And a fourth:

4. Is it informed by people who truly understand how advisors engage?

Spina: Sustainable organic growth requires more than activity. It requires an integrated, intelligence-led development system grounded in real distribution experience and reinforced by professionals who understand both sides of the advisor conversation. That is what we set out to build.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

Find financial advisors in Flagstaff, Arizona ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Flagstaff for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Flagstaff featured on Wealthtender you may want to add to your shortlist.

Featured Flagstaff Financial Advisors

As you prepare to interview financial advisors in Flagstaff who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Coming Soon: Financial Advisors with their Primary Office Location in Flagstaff

Check back in the future for advisors with their primary office location in Flagstaff.

📍 Additional Advisors Who Serve Clients in Flagstaff

In addition to the advisors featured above, these advisors can also meet with you in person in Flagstaff.

The Benefits of Hiring a Financial Advisor in Flagstaff

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Flagstaff, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Flagstaff? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Flagstaff Financial Advisor

Before hiring a financial advisor in Flagstaff, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Find financial advisors in Sedona, Arizona ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Sedona for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Sedona featured on Wealthtender you may want to add to your shortlist.

Featured Sedona Financial Advisors

As you prepare to interview financial advisors in Sedona who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Sedona

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Sedona.

The Benefits of Hiring a Financial Advisor in Sedona

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Sedona, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Sedona? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Sedona Financial Advisor

Before hiring a financial advisor in Sedona, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Discover financial advisors trusted by Phoenix residents in the only local directory featuring 5-Star Certified Advisor Review™ recipients and Wealthtender Voice of the Client Award™ winners—recognition earned for exceptional client feedback. Compare fiduciary, fee-only advisors, CFP® professionals, and specialists to find the right fit for your unique financial needs.

Thousands of people visit Wealthtender each month to find and compare financial advisors based on their location, education, experience, areas of specialization and online reviews. Wealthtender’s Certified Advisor Reviews™ help consumers make informed hiring decisions with important details about the relationship between reviewers and advisors always displayed to ensure you gain the transparency you deserve when your life savings could be at stake.

Types of Financial Advisors You’ll Find on Wealthtender

On Wealthtender, you can explore a diverse range of financial advisors and wealth management firms that include:

Fiduciary advisors committed to acting in clients’ best interests

CFP® professionals with advanced financial planning credentials

Fee-only advisors compensated solely by clients

Advisors for growing families, people nearing retirement, and business owners

Specialists across multiple categories (e.g., life stage, occupation, ethnicity, lifestyle, religion)

Highly-rated advisors with positive client reviews

Firms of varying sizes with advisors who can meet with you in person or online

Fee-based advisors who offer access to insurance and alternative investments

Financial Advisor Directory for Phoenix, Arizona

How to use this directory: Compare financial advisors in the Phoenix area based on what matters most to you. Use the directory to:

View advisor profiles to evaluate credentials, services, and areas of specialization

Read Certified Advisor Reviews™ to learn what clients value most

Identify advisors recognized with Wealthtender Voice of the Client Awards™

Contact advisors and schedule free introductory video calls

📍 Map: Financial Advisors with their Primary Office Location in Phoenix

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Phoenix.

Wealthtender Voice of the Client Awards™: Top Rated Phoenix Financial Advisors

Wealthtender Voice of the Client Awards™ recognize financial advisors and firms that consistently earn exceptional client feedback. Below are Phoenix-area advisors and firms that have met the criteria for Highly Rated recognition.

To qualify for a Highly Rated award, advisors and firms must achieve an average client review rating of 4.75 or higher (on a scale of 1 to 5) based on a minimum number of eligible client reviews published on Wealthtender within a defined timeframe for each particular award (Timeframe for 2025 Award: 1/1/24 – 12/31/25; Timeframe for Subsequent Year Awards: July 1 of the preceding year through December 31 of the Award Year (e.g., Timeframe for 2026 Award 7/1/25 – 12/31/26). Eligible reviews are limited to clients (as of the review submission date) that advisors/firms must self-attest have no material conflicts of interest and received no compensation in exchange for their reviews. ↗️ View full award methodology & FAQs

Although financial advisors and wealth management firms compensate Wealthtender for marketing services (including eligibility to be considered for awards), Wealthtender’s award criteria is objective and not influenced by compensation. Wealthtender Voice of the Client Awards are not a guarantee of future performance or success and client reviews may not be representative of the experience of all past or future clients.

Frequently Asked Questions

What makes a financial advisor “trusted”?

A trusted financial advisor typically earns positive client feedback over time, operates transparently, and clearly explains how they’re compensated. On Wealthtender, trust is reflected through Certified Advisor Reviews™ that combine insights into the client experience and character of advisors with important disclosures about each reviewer to ensure you gain the transparency you deserve when your life savings could be at stake.

Financial advisors and wealth management firms that consistently receive superior client reviews can also qualify for Wealthtender’s Voice of the Client Awards™ designed to recognize America’s most trusted advisors. Learn More About Wealthtender Voice of the Client Awards™

What are Certified Advisor Reviews™?

Certified Advisor Reviews™ from Wealthtender help consumers make smarter hiring decisions when choosing a financial advisor.

Clients and other individuals can submit reviews for financial advisors and wealth management firms that have turned on the reviews feature. Before each review is publicly displayed, financial advisors agree to disclose important information about their relationship with the reviewer to ensure consumers gain the transparency they deserve when their life savings could be at stake. These disclosures also help financial advisors satisfy compliance with industry regulations.

After financial advisors provide the required disclosures, Wealthtender publishes the review with the Certified Advisor Review™ mark. Learn More About Certified Advisor Reviews™

Can I find fiduciary financial advisors on Wealthtender?

Yes, you’ll find hundreds of fiduciary financial advisors on Wealthtender. Fiduciary financial advisors must act in their clients’ best interest. Before hiring an advisor, always ask if they will act in your best interest as a fiduciary.

For example, financial advisors who have earned their Certified Financial Planner (CFP) designation are fiduciaries. To hold themselves out as a CFP, these credential holders must acknowledge they will adhere to the CFP Board’s Code of Ethics and Standards of Conduct and act as a fiduciary when providing financial advice to their clients. Learn More About Fiduciary Financial Advisors

Can I find fee-only financial advisors on Wealthtender?

Yes, you’ll find hundreds of fee-only financial advisors on Wealthtender. Fee-only financial advisors are paid directly by their clients. Since they aren’t compensated based on the products and services they recommend (e.g., commissions), their compensation model helps reduce potential conflicts of interest.

When viewing financial advisor profiles on Wealthtender, look for the Compensation Methods section that shows ways each financial advisor can be paid for their services, including if they offer fee-only financial planning services. Learn More About Fee-Only Financial Advisors

What distinguishes Wealthtender Voice of the Client Awards™ from other advisor recognition programs?

Wealthtender’s Voice of the Client Awards™ recognize financial advisors and wealth management firms that consistently receive superior client reviews. Unlike award programs with ranking factors that favor financial institutions with the most assets and the fastest revenue growth, the Wealthtender Voice of the Client Awards provide both local financial advisors who choose to remain small and large wealth management firms with the opportunity to be recognized on a metric that matters more to consumers – actual client feedback reflecting the quality of their experience. Learn More About Voice of the Client Awards™

The Benefits of Hiring a Financial Advisor in Phoenix

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Phoenix, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Who are the largest employers in Phoenix?

Phoenix is home to many of the top companies and brand names in the world. The largest employers in the Phoenix area provided by the City of Phoenix include:

Banner Health

American Express

Honeywell

Amazon

Fry’s Food Store

Dignity Health

Chase

Bank of America

U Haul

Do you work for one of the largest employers in Phoenix? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring a Phoenix Financial Advisor

Before hiring a financial advisor in Phoenix, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor in Phoenix, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

[The recent merger and reorganization of two microcap funds provide an interesting window into the mechanics of a unique portfolio management process and a deeper understanding of the microcap market. While the two funds seem like a natural fit based on a decades-long history of both managers employing a similar value-based approach to investing in the same universe of stocks, their shared investment philosophy was only the beginning of an intricate process to combine the two portfolios.

To better understand this investment merger process and get an update on the microcap marketplace, we reached out to Eric Kuby, Chief Investment Officer & co-Portfolio Manager, North Star Micro Cap Fund and Michael Corbett, formerly Chief Investment Officer of the Perritt MicroCap Opportunities Fund. They explained their process of combining the two portfolios as an intensely collaborative effort that used a quantitative factor model to score all holdings, followed by qualitative discussions to understand the investment thesis behind each company.

They both strongly believe small and microcap stocks are entering a new cycle of outperformance, citing historical patterns of “serial correlation” where periods of good performance tend to continue for an extended timeframe. We also discussed several timely microcap sub-topics that we explored together, including the impact of AI on smaller companies, the potential for increased M&A activity, and macroeconomic tailwinds like interest rates and tariff pressures.]

Hortz: What are the regulatory processes involved in merging two separate mutual funds?

Kuby: We saw a great opportunity to merge two long-standing microcap mutual funds with a shared philosophy. We made the necessary regulatory filings and received the approval of the Perritt shareholders through proxy solicitation. The entire process took approximately 3 months.

Hortz: Since the merger of the two funds entailed the merger of two different shareholder bases, how does that influence or direct your investment decisions?

Corbett: The good news is that the two shareholder bases share a common objective in holding the Funds, namely an allocation to an actively managed portfolio of microcap companies that meet the classic definition of value stocks.

Hortz: How did you both practically approach this merger? What were your first few steps in the merger process?

Kuby: The process started with months of going through the portfolios and getting everything into shape. The portfolio managers and research analysts from both firms met regularly to review the holdings, one by one. Whereas there were common holdings the North Star team was already very familiar with, there were many Perritt names we were excited to learn about.

Hortz: Can you explain your quantitative factor model and how you used it?

Kuby: The small cap universe includes thousands of companies, so having a systematic way to narrow the field is extremely important. The factor model helps us do exactly that and it is a great way of focusing our attention on a smaller group of companies that warrant the research.

The model ranks companies using several metrics, with each factor assigned a weighting in the overall score. The purpose is two-fold: it helps us quickly identify undervalued companies that are demonstrating improving fundamentals, while also allowing us to monitor how the current portfolio holdings compare to the broader opportunity set.

Importantly, the model is designed to surface opportunities, not make decisions. Companies that rank highly in the quantitative analysis move into our fundamental research process, where we evaluate them through the lens of our proprietary North Star Six Characteristics investment mosaic.

Corbett: That is really the secret sauce of this business. The model helps narrow the field, but the real work is seeing beyond the numbers – What’s the story of the business, and who are the people running it?

Hortz: Can you walk us through a specific example of a stock that scored highly on your quantitative model and one that scored poorly, and detail the subsequent qualitative conversation that determined its place in the new portfolio?

Kuby: A good example is Legacy Housing (LEGH). The stock scored well in our model because the shares are inexpensive and the balance sheet is strong. The story also made sense given our thesis on the housing market. The U.S. continues to face a housing shortage, and Legacy operates in manufactured housing, which provides a more affordable solution. As mortgage rates have ticked down and housing becomes a policy focus, we believe some tailwinds could emerge for that business.

On the other hand, Motorcar Parts of America (MPAA) is a company we have owned in the past and that has screened attractively at times. But more recently, news around the business has highlighted a more challenging operating environment. It is still an interesting company, but when we stepped back and compared it to other opportunities in the portfolio, it was simply less compelling at the time. So, it moved out of the portfolio and into what we call our “Bullpen”, which is essentially our watchlist of companies we continue to follow closely and could revisit.

Hortz: What are the possible effects of interest rates and tariffs on microcap companies?

Kuby: Much of the initial “tariff tsunami” appears to be behind us. That created a period of uncertainty as companies evaluated supply chain exposure and potential cost pressures. But smaller companies often have an advantage in that they tend to be more nimble. Many smaller companies have already adjusted their supply chains, diversified sourcing, or passed through price increases where possible.

Corbett: Interest rates tend to have a more direct influence on the microcap universe. Smaller companies are often more sensitive to financing conditions because they rely more heavily on bank lending. As interest rates stabilize or begin to decline, access to capital improves, borrowing costs fall, and banks become more willing to extend credit. That can be particularly helpful for smaller businesses looking to invest in growth, manage working capital, or pursue acquisitions. When financing conditions improve and economic visibility increases, investor interest often returns to the space. We are beginning to see signs that capital is flowing back toward smaller companies.

Hortz: What do you see as the potential impact of AI on smaller microcap companies?

Corbett: While the big technology companies get most of the attention for innovations in AI, the impact of the technology reaches far and wide. Smaller microcap companies can use AI to achieve greater efficiency in logistics, marketing, and transactions. The implantation of AI will ultimately enhance margins for these companies.

Kuby: If you think back to the DotCom era, many of the long-term winners were companies that simply became better businesses because they embraced the internet. We believe AI can follow a similar path. It is also very difficult today to predict which of the hyperscalers will be the long-term winners and losers, so our focus is less on picking those outcomes and more on identifying companies that will benefit from adopting the technology.

Hortz: From an investment perspective, can you share a few examples of how you are playing AI in your combined portfolio?

Kuby: Across our combined portfolio, we have meaningful exposure to Industrials, Consumer Discretionary, and Financials. For example, in Consumer Discretionary, investments in data analytics, inventory optimization, and supply-chain efficiencies can improve margins and operating discipline. In Industrials, AI-enabled automation and predictive maintenance can drive better asset utilization and cost control, while in Financials, AI tools are increasingly improving underwriting, fraud detection, and customer analytics. Many smaller companies are nimble and can implement these tools quickly, which may allow them to compete more effectively against larger competitors.

Corbett: We have invested in companies such as Bel Fuse (BELFB) that supply products to the AI innovators, but we have recently turned our attention to more companies that will use AI in their businesses, such as EZCorp (EZPW). EZCorp is a chain of pawn shops that uses AI to implement more sophisticated pricing.

Hortz: Any other microcap companies in your portfolio that you would like to discuss which provide further examples and insights into your stock selection process?

Kuby:Acme United (ACU) is really the poster child for our investment strategy. It checks every box in our Six Characteristics framework. It is a simple business selling safety, first-aid, and cutting tools – products used every day. The company has strong brands, recurring revenue through first-aid refill kits, and extensive distribution with the major retailers.

What stands out most is the exceptional management team, led by CEO Walter Johnsen, who has a long track record of disciplined, shareholder-focused capital allocation. The company has grown steadily across multiple economic cycles while maintaining a strong balance sheet, compounding value through several successful bolt-on acquisitions, operational improvements, and consistent free cash flow. Despite this, the stock has historically traded at valuations that do not fully reflect the quality and durability of the business.

Hortz:With the potential for a small cap and microcap outperformance cycle and renewed M&A activity, what one or two key characteristics make a microcap company an attractive buyout target in the current environment?

Corbett: I have usually answered this kind of question with: “We never purchased companies with the intention of them being bought out. But high-quality companies with a niche business may ultimately be bought out.”

I would also say that today’s environment is attractive for M&A, driven by reduced regulation, favorable interest rates, and lower valuations in the microcap universe. Dr. Gerald W. Perritt used to talk about how stocks often perform in streaks of overperformance and underperformance. Small cap stocks in particular tend to exhibit serial correlation: once they begin performing well, they often continue performing well for a period of time and get the attention of potential acquirers.

Kuby: We really have not seen that kind of sustained period for small caps in quite a while. But when you look at the combination of current valuations and improving earnings growth, the space may be setting up for a very constructive period ahead.

Valuations across the small cap and microcap universe remain relatively attractive, which creates opportunities for larger companies looking to acquire growth or niche capabilities at reasonable prices. So, while we do not buy companies because we think they will be acquired, we do believe that many of the businesses we own possess characteristics that make them logical acquisition candidates over time, particularly in a market environment that is becoming more conducive to deal activity.

Hortz:How would you characterize to shareholders and financial advisors the new composition of the fund resulting from the merger? What specific portfolio statistics or risk metrics improved most significantly through this combination?

Kuby: Several portfolio metrics improved meaningfully through the combination. The portfolio’s long-term EPS growth estimate increased to 15.0% from 13.2%, while valuation measures became more attractive: price-to-sales declined substantially from 1.5x to 1.1x, EV/EBITDA improved from 11.7x to 10.0x, and forward P/E decreased from 18.8x to 14.6x. In other words, the combined portfolio reflects better value characteristics while also offering higher expected growth.

Corbett: The North Star Micro Cap Fund (NSMVX) represents the best ideas from two investment teams that have each spent decades dedicated to the small cap universe. From a structural standpoint, the combination improved diversification and lowered the expense ratio, which are both meaningful benefits for shareholders.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

Find financial advisors in Columbia, South Carolina ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Columbia for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Columbia featured on Wealthtender you may want to add to your shortlist.

Featured Columbia Financial Advisors

As you prepare to interview financial advisors in Columbia who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Columbia

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Columbia.

The Benefits of Hiring a Financial Advisor in Columbia

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Columbia, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Columbia? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Columbia Financial Advisor

Before hiring a financial advisor in Columbia, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Why the first five years after you stop working may determine if your retirement survives, and what to do about it

In this article, we look at:

Why the first five years of your retirement are especially dangerous.

How sequence-of-returns risk can derail your retirement.

What research says about retirement failures.

Practical strategies that can protect your retirement plan.

What you have to avoid doing to prevent a bad situation from turning much worse.

What We Tend to Focus On

Although I worked for 40 years, for the first 25 of those, I earned too little to set aside much, if anything, for retirement.

That’s why, during the remaining 15 years, I did (almost) everything I could to build up our nest egg. Beyond investing significant amounts each of those 15 years, and picking (mostly) the right funds, I have to acknowledge that luck played a role, too. During that period, the market significantly outperformed its long-term average, giving us a strong tailwind.

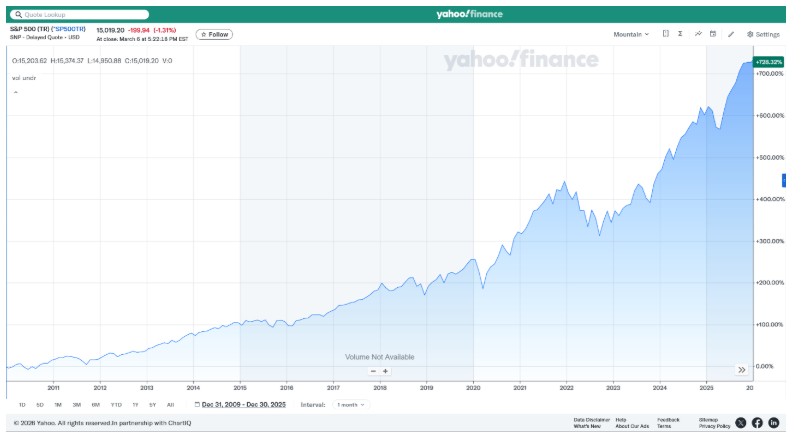

From 2010 to 2025, the S&P 500 achieved a 728% total return (Figure 1), a nominal annualized return of 14.1%, and an inflation-adjusted annualized return of 11.3%. That’s almost 80% higher than 16 years would have returned at a 10% annualized rate.

Figure 1. From 2010 to 2025, the S&P 500 achieved a 728% total return. That’s a far higher-than-average nominal annualized return of 14.1%, and a real, inflation-adjusted annualized return of 11.3% (Courtesy: Yahoo Finance – https://finance.yahoo.com/chart/%5ESP500TR/).

Between our efforts and favorable markets, by the end of 2025, I reached “work optional” status and decided to mostly retire. I add that word, “mostly,” because I continue to do some consulting work and also get paid for writing these articles.

When You Retire Matters, a Lot!

First, let’s acknowledge that the year you retire can have a massive impact on your retirement portfolio.

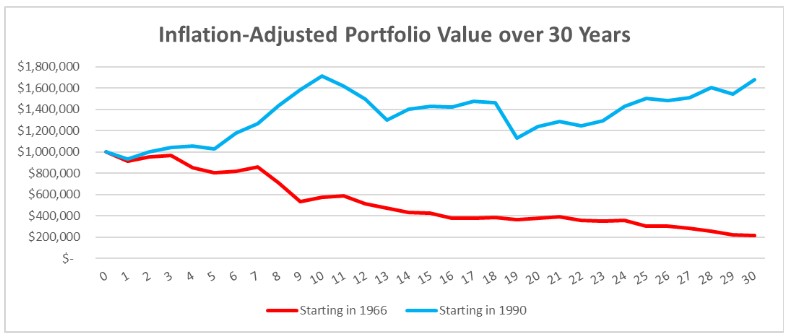

Let’s look at inflation-adjusted portfolio value over the course of a 30-year retirement for two hypothetical retirees using the 4% rule. The first, less fortunate one retired in 1966, while the second “chose” to retire at a much more fortunate time, in 1990.

As Figure 2 shows, after 30 years in retirement, the 1990 retiree’s portfolio was worth, after adjusting for inflation, nearly 70% more than its initial value, while the 1966 retiree’s portfolio lost nearly 80% of its initial value. Overall, the difference over 30 years was nearly 8-fold!

Figure 2. Inflation-adjusted portfolio values for two hypothetical retirees, who retired in 1966 and 1990, respectively, show the massive impact of when you retire, vis-à-vis market returns. Each retired with $1 million, invested 50/50 in large-cap US stocks (using the S&P 500 as a proxy) and US bonds, and withdrew $40k annually (inflation-adjusted). S&P 500 total return, bond return, and inflation data are from Yale economist Robert Shiller – http://www.econ.yale.edu/~shiller/data.htm.

The Pitfall Most of Us Don’t Consider

It’s possibly the biggest risk to retirement success.

The so-called “sequence of returns risk,” i.e., the order in which market gains and losses happen, may matter more than your average returns.

Catching a good break here, or a bad one, can make or break retirement success. Especially if your retirement lasts much longer than 30 years.