Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

I am a big believer in the idea that we should all be more comfortable talking about money and finances. It’s difficult to improve your financial situation if you don’t talk through your issues with people that might be able to help you. One of the reasons people don’t talk about financial issues more is because personal finance terms can sound both intimidating and boring.

Let’s increase our financial literacy and start by reviewing 5 personal finance terms you need to know.

- Financial Independence

- Savings Rate

- Compound Interest

- Net Worth

- Management Expense Ratio (MER)

Personal finance term 1: Financial independence

This is a term that is being used more every day but is there a working definition of financial independence?

Yes.

You have achieved financial independence when your passive income can sustainably cover all your expenses in life. It is the point where you no longer need to work to get by.

What do I mean by “passive income”?

Passive income is simply the income you receive from investments.

- If you own stocks or mutual funds, they pay you a dividend typically every month or every quarter. Additionally, as the value of stocks rises, they can be sold at a gain to create income if you need it.

- If you own Bonds, they pay out interest to you as well.

- If you own real estate investment properties, you receive monthly rent from your tenants.

These are all forms of passive income. Once your passive income is greater than your expenses in life you have achieved financial independence.

True financial independence comes when your passive income can sustainably cover your living expenses. Over time your living expenses and the value of your expenses will change. If the income you can generate from your investments does not keep pace with your living expenses, you will no longer be financially independent. This is something that anyone considering early retirement needs to think about.

Personal finance term 2: Savings rate

Before we can fully understand our savings rate, we need to understand the concept of your “take-home pay”.

Take-home pay: How much of your salary or wages you keep after all taxes and deductions. Think of this as the actual money that gets deposited into your bank account on payday.

Your savings rate is simply the percentage of your take-home pay that you save and invest. For example, if your take-home pay was $1,000 and you invested $100 every payday, you would have a savings rate of 10%.

Your savings rate is the most important metric as it relates to your timeline of achieving financial independence.

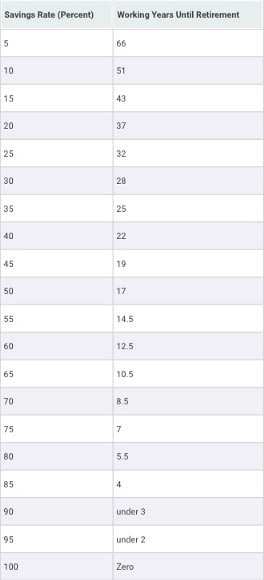

This chart created by Mr. Money Mustache breaks down the relationship between your savings are and how many years you need to work before you reach Financial Independence.

Source: Mr. Money Mustache

Source: Mr. Money MustacheIf you saved 10% of your take-home pay (Which is traditional financial advice) you could reach financial independence in about 51 years.

If you saved 50% of your take-home pay (not unheard of in the FIRE community), you could reach financial independence in 17 years.

Personal finance term 3: Compound interest

Compound interest can be a bit tricky to explain without getting bogged down in mathematical formulas. However, it is a critical concept to understand. Here is the simplest explanation I can think of.

Compound interest is the process of earning interest on your interest.

Let’s break it down into a quick example.

- You invest $100 and earn 10% interest per year.

- After one year you have $110. Your initial $100 principal plus your $10 in interest. We will call this your “simple interest”

- After year two you have $121. Your initial $100 principal plus your $10 in interest on that principal, plus last years $10 in interest on your principal plus $1 in compound interest.

- The compound interest in year two is the interest on the interest you earned in year one. You earned $10 in interest in year one and in year two that interest earned $1 in interest on its own. That’s compound interest.

You might be thinking $1! so what? The power of compound interest is expressed over time. The longer you keep that investment rolling the more compound interest can accelerate your wealth.

In the above example after 30 years, you would have $1,984, of which $1,583 would be the result of compound interest.

Time + Compound Interest = Wealth

This brings me to the next term you need to know.

Personal finance term 4: Net worth

Your net worth is simply an expression of your current wealth.

Your net worth is calculated by subtracting all your debt from all your assets.

Start by adding up all your assets

If you have:

- A house worth $500,000

- $350,000 in your retirement accounts

- $10,000 in cash

- $20,000 in bitcoin

- A car worth $12,000 (I hate counting a car as an asset but technically it is)

You have $892,000 in total assets.

Next, add up all your debts.

If you have:

- A mortgage worth $300,000

- $10,000 in credit card debt

- $10,000 in car loans

You have $320,000 in total debt

Your net worth is $572,000

Personal finance term 5: Management Expense Ratio (MER)

For anyone investing in mutual funds or index funds, it is important to know the Management Expense Ratio (MER) for that fund.

The MER will tell you what percentage of the money goes towards paying fees. On day one when you invest in a fund, you are in the hole by the amount of the MER.

If the fund has an MER of 1% that means the fund will need to earn 1% for the year before you get back to even. If you invest $100 into a fund with an MER of 1% right away $1 goes to pay expenses incurred by the fund, and $99 goes to investing in the assets of the fund.

While 1% may not sound like a big deal in the long-term it can add up to a huge amount of money. Do you remember how we just talked about the power of compound interest over time? The management fees you pay on your investments also have compounding impacts over time. High management fees are one of the reasons I choose to invest in low-cost Index Funds.

About the Author

Ben Le Fort

In the eight years following graduation, he paid off all of the debt and built a seven-figure net worth. Ben holds a Bachelor’s degree in economics from Acadia University and a Master’s degree in Economics & Finance from The University of Guelph.

Ben lives in Waterloo, Ontario, with his wife, son, and cat named Trixie.

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor