Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

Learn the 7 biggest risks that could derail your retirement plans and what you can do to overcome them, so you can enjoy your golden years.

Life is full of surprises, many of the unpleasant variety. As humans, we’re far more committed to avoiding pain or failure than we are to achieving great results.

In professional terms, that’s called being “risk averse.” The more important a goal, the less willing we are to fail, which makes us less willing to take risks, even calculated ones. The problem is that by doing this, we cheat ourselves of bigger wins. If you want bigger wins in life, here’s a simplified version of what I learned from NASA on managing risk, and how you can apply it to your retirement plan, since “Failure is not an option!”

What Is Risk and How to Manage It

In the simplest terms, a risk is the possibility that something will go wrong. Managing risks requires 5 important steps.

- Identify the risks

- Assess each risk’s likelihood and consequence

- For risks with acceptable likelihood and consequence: accept they may happen and don’t worry

- For risks with unacceptably high likelihood and/or consequence: if feasible, change your plan to prevent the risk; if not feasible, craft a mitigation plan that reduces likelihood and consequence

- Reassess each risk’s post-mitigation likelihood and consequence to ensure these are acceptable

Why Retirement Planning Is So Challenging

Planning for retirement is one of the biggest personal finance challenges you face for two reasons. First, a comfortable retirement requires a LOT of money, and since most of us don’t make enough to satisfy all of our current needs and wants plus enough to save “a LOT of money,” that saving must come at the expense of satisfying current wants – delayed gratification anybody?

Second, as physics Nobel laureate Nils Bohr quipped, “Making accurate predictions is very difficult, especially about the future,” more so when that future is decades away, and even more so when you have to predict with plausible accuracy both how the market will fare until (and in) retirement, and how much you’ll need for a comfortable retirement.

Just listen to the financial talking heads, and you’ll quickly realize that none of them can predict market returns with any degree of accuracy for any specific day, week, month, year, or even decade.

According to a US Bank study, 41% of Americans say they use a budget. This means 59% don’t have a budget for their current spending, so how could they possibly have a clue about how much they’ll need in retirement?

The 7 Biggest Risks to Your Retirement Plan and What You Should Do About Them

Let’s start working on the 5 steps of managing the risks to your retirement plan.

Step 1. Identify the risks.

1. Market Risk

As mentioned above, even the experts can’t predict market returns, but if history is any guide, over the course of a multi-decade retirement you should expect 10%+ “corrections” (read “losses”) every 2-3 years, and a bear market (20%+ loss) every 6-7 years. On average, bear markets lasted 14 months, had an average loss of 33%, and took just over 2 years to return to the pre-bear-market value. When your retirement income depends in large measure on the size of your portfolio and its returns, suffering a 33% loss can be devastating.

2. Sequence-of-Returns Risk

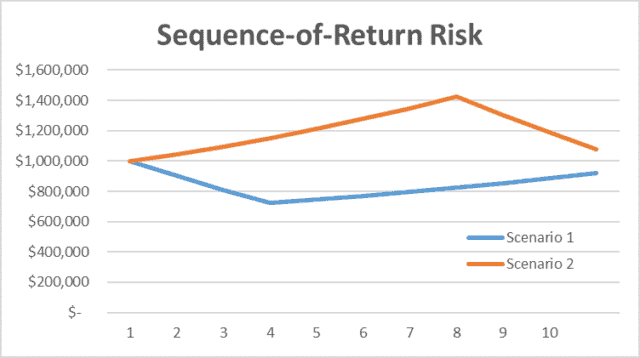

In the simplest terms, sequence-of-returns risk is the risk that the market will drop like a rock just as you start your retirement. The result would be that you’d need to sell when the market is low, in order to fund your retirement needs in the first few years, and this loss would have decades to reverberate through your portfolio.

To demonstrate this, consider two scenarios where in both you retire with a $1 million portfolio, and draw $40,000 a year (for simplicity, let’s assume there is no inflation). In Scenario 1, you experience 6% annual losses in the first 3 years of retirement, followed by 9% annual gains in each of the following 7 years. In Scenario 2, you experience the same returns, but in opposite order. First the 7 years of 9% gains, then the 3 years of 6% losses.

Mathematically, if you neither contribute to your portfolio nor withdraw from it for this decade, the ultimate results would be identical in the two scenarios. However, since you are in retirement in this example, as you can see in the graphic, despite having an identical starting and the same average annual return of 4.26% over the decade in question, you end the decade with a 7.7% loss in Scenario 1 vs. a 7.9% gain in Scenario 2. Just changing the order of returns results in a $155,870 difference in outcome!

Your sequence-of-returns risk is the risk that your early retirement will be more like Scenario 1 and less like Scenario 2.

3. Interest Rate Risk

During retirement, as well as in the last few years approaching it, retirees mitigate market risk by diversifying a significant portion of their portfolio into fixed-income assets such as treasury notes, certificates of deposit (CDs), and savings accounts. This results in a risk that if interest rates drop as they have in recent years, retirees can’t count on as much money from interest payments, and when they have to reinvest this portion of their portfolio because a CD or treasury note reached maturity, their income may suddenly drop significantly.

4. Inflation Risk (Especially Healthcare Inflation)

Historically, most years see prices increase compared to prior-year prices. This is called inflation, and is most often quoted based on the US Department of Labor’s (DOL) Consumer Price Index (CPI). This CPI is calculated based on monthly data on prices of a basket of goods and services. In the worst rolling 20-year period between 1926 and 2018, the dollar lost over 70% of its value! In the average 20-year period, it still lost nearly 53%.

DOL also calculates a so-called “CPI-E” where the “E” stands for “elderly.” The CPI-E uses a slightly different basket, with greater emphasis on healthcare costs, for obvious reasons. Since 1981, the annual CPI averaged a 2.8% increase, whereas the CPI-E increased by an average of 3.1%. The extra 0.3% a year is due in large part to the faster price increases in healthcare, which averaged 5% a year since 1981.

The risk here is that prices start increasing more rapidly when you’re in retirement, which puts pressure on your budget.

5. Investor Behavior Risk

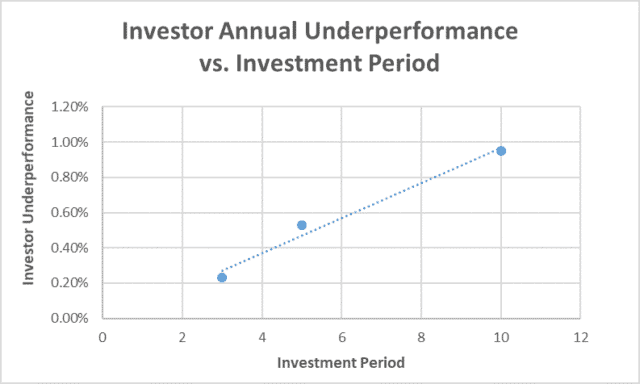

As Ben Le Fort points out in his excellent article about how investors sabotage their own portfolio performance, investors as a group do extremely “well” at buying high and selling low – a great way to lose out good investment returns. Le Fort quotes a Morningstar study that shows that on average, over the 3-, 5-, and 10-year periods ending Dec 31, 2012, investors under-performed the mutual funds they owned by 0.23%, 0.53%, and 0.95%, respectively (see graphic).

One wonders why investor under-performance becomes so much worse as the investment period lengthens. It could be a matter of our emotional behavior – fear, greed, and overconfidence – having more time to wreak havoc on our investments, in which case, you’d expect under-performance to become much worse as the investment period grows to 20, 30, 40, or more years.

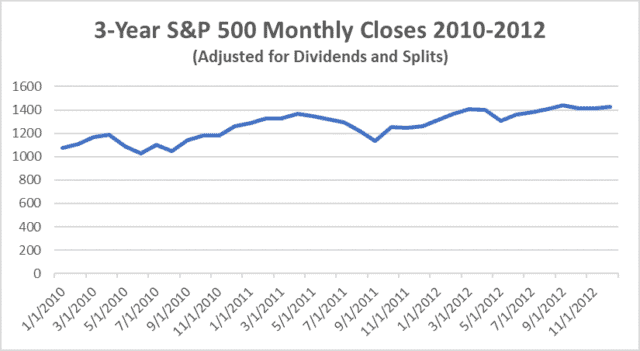

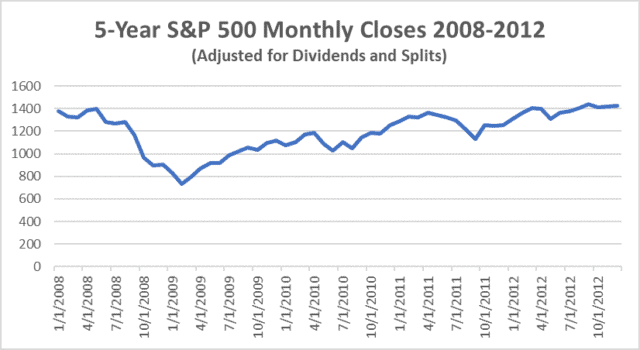

Alternatively, it could be driven by market volatility over the specific period in question. As shown below (data from Yahoo! Finance), market gyrations were worse over the 10-year period ending Dec. 31, 2012, compared to the 5-year period, and worse for that vs. the 3-year period ending on that same date. If this is the reason for the above-shown trend, we could expect under-performance over very long periods to be similar or slightly worse compared to its 10-year level.

What This Means for Your Investment Results

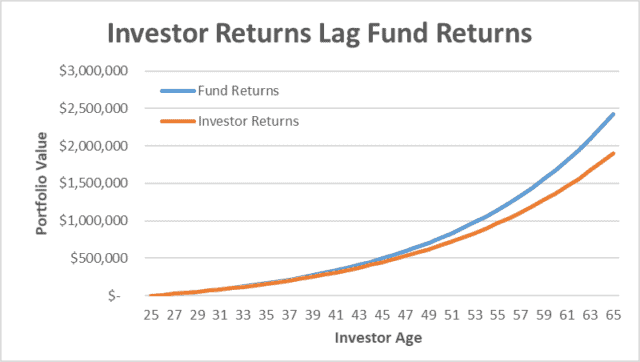

To bring all this into perspective, here’s how badly investors hurt themselves through their emotional investing behavior. The graphic below compares the result for two hypothetical investors who each invest $12,000 at the end of each year from age 25 to 65, where one simply invests and allows the funds’ hypothetical 7.05% annual return to work its magic, while the second tries to time the market and ends up with a 6.1% annual return while investing in those same funds.

Over this hypothetical 40-year period, the active investor’s portfolio reaches a healthy $1.9 million. Not too shabby. However, his buy-and-hold friend’s portfolio reaches $2.4 million investing the same dollar amounts in the very same funds!

The buy-and-hold investor outperforms his active friend by a total of 27%, ending up with over $520,000 more in his portfolio, allowing him to draw an extra $21k a year in retirement according to the 4% rule (though this rule may need to be updated).

6. Longevity Risk

This is the risk that you will outlive your money, which is one of a retiree’s worst fears.

Over the past several decades, our life expectancy in retirement has increased by many years. According to the Social Security Administration (SSA), a worker turning 65 in 1940 was expected to survive about 14 years in retirement. That same number for workers turning 65 in 1990 was over 17 years (averaging male and female life expectancies). Using the SSA’s life expectancy calculator, that number is currently just over 20 years. This shows that life expectancy at age 65 increased by nearly 43% in the last 79 years. More importantly, half of people reaching age 65 now will survive longer than 20 years in retirement.

The SSA’s actuarial table shows that a couple turning 65 today has about a 50% chance that at least one of the two will survive to age 90, a 20% chance that at least one reaches age 95, and nearly a 5% chance at least one lives beyond age 100. Research also shows that the SSA’s numbers underestimate the life expectancy of people who are more affluent than average.

7. Health Risk

According to Fidelity, the average 65-year-old couple that retired in 2019 should expect to spend $285,000 for medical expenses in retirement, excluding long-term care. This number does not take into account any inflation in healthcare costs. Knowing this, you can plan for it when crafting your retirement plan. You can use Nerdwallet’s calculator to estimate your own median expected retirement healthcare costs.

However, the above estimate is the average. The health risk is that you and/or your spouse may suffer some severe health-related crisis or chronic condition that increases your healthcare costs significantly above the average. A serious illness or accident that puts one of you in the hospital for a long period could cost you hundreds of thousands of dollars in hospital bills, prescription drugs (especially if these aren’t part of the so-called “formulary” of commonly prescribed drugs, etc. Having a long-term chronic condition that requires in-home support for many years could similarly devastate your retirement plan.

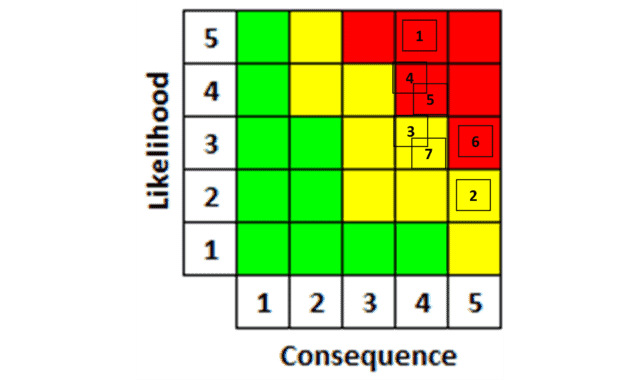

Step 2. Assess each risk’s likelihood and consequence.

Here, we’ll use a NASA tool, called a “risk matrix.” Each of the 7 risks is defined by a number, which I’ve placed in what I think is an appropriate rubric.

Step 3. Accept acceptable risks.

Here, with all risks in yellow or red regions, no risk should be viewed as acceptable.

Step 4. Craft risk-avoidance and mitigation strategies.

Here are some mitigations you should seriously consider implementing to address these 7 biggest risks to your retirement plan.

1. Mitigating Market Risk

The first and most important thing you can do to mitigate the risk that your portfolio will drop in value is to make it as large as possible in the first place. This means investing for retirement as much as you can right now (even if that’s only 1% of your income), and allocating at least half of each raise, each bonus, each cash gift, and each bequest you receive. By not trying to save all of these “found money” situations for the future, you’re far more likely to be able to stay on track with that.

Michael Hunsberger, ChFC®, Owner, Next Mission Financial Planning, adds an important point, “A recent trend I’ve seen introducing risk into clients’ retirement plans is student loan debt. Today, over 8 million adults aged 50 or over have student loan debt, with the number growing rapidly. Parents in their late 40s to mid-50s take out student loans for their kids, which they then pay off over 10 or 20 years. Paying off such loans can crowd out saving and investing for retirement. Students and their parents need to have honest conversations before the parents take on significant student-loan debt, so they understand the long-term ramifications for both parties. As a fellow planner likes to say, the most dangerous words in college planning are, ‘If you get in, we’ll figure it [how to pay] out.’”

Especially as you near retirement, shift your investments so your market risk is reduced. This does not mean moving your entire portfolio permanently out of the stock market and into bonds, CDs, and savings or money market accounts. That would dramatically increase your risk that inflation will eat away at your portfolio’s value, potentially by more than half.

You can consider your age and likely longevity. Some experts recommend subtracting your age from 120 and using that to determine the percentage of your portfolio that you should keep in equities. At age 65, that would be 55%.

However, some researchers recommend moving almost completely out of equities at when you’re close to retirement, and then gradually moving money back into stocks and stock funds (see also the mitigation for sequence-of-return risk).

2. Mitigating Sequence-of-Return Risk

To mitigate this risk, as mentioned above, you could move nearly all your investments out of equities as you approach retirement, and gradually move back into equities over the first 5-10 years of retirement. This will minimize the likelihood and consequence of a potential bear market hitting just as you retire. It will increase the likelihood and consequence of inflation risk, but by staying out of the market for only a few years, that won’t have as devastating an impact on your retirement as would being fully invested in equities and experiencing a major bear market just as you start drawing from your portfolio.

However, Doug Oosterhart, CFP®, Founder &Financial Planner at Lifepoint Planning, suggests being judicious with such moves, saying, “In almost all cases, if a retiree moves most or all of their money to fixed instruments upon retirement, that poses a higher risk than leaving it all invested in equities, since the market’s returns are positive more years than negative. I’d consider moving most or all of one’s money to fixed instruments to be an extreme decision.

“By moving entirely or nearly so to fixed instruments, yes, one might avoid big losses early in retirement. However, they also draw money out of the portfolio when it’s earning a negative real return due to inflation.

“Ideally, a retiree/investor should start by clarifying their retirement income style preference – safety-first or probability-based (a.k.a., contractual guarantees like pensions, annuities, etc.) OR total-return approach (like the 4% rule). Most clients fall somewhere in the middle.

“It’s important to leave some money in equities, in case they first retire at the start of a bull market. However, they should also plan out the first few years of income. Some strategies I use that clients like include using individual bond ladders (now that rates are higher), defined outcome or buffer ETFs that provide a level of downside protection with a solid return potential up to a cap, annuities – a lot of people hate the word, but mathematically, they can provide a good solution for the right client, and guardrails. Guardrails set up trigger limits such that when a portfolio goes down or up far enough the retiree increases or decreases their spending for the following 12-24 months.

“At the end of the day, a retiree has to identify what solution works best for their preferences, as there’s an element of both art and science to retirement distribution planning.”

Another mitigation is to at least have 1-2 years’ worth of retirement expenses in a highly liquid and low risk asset such as money market fund or high-interest savings account. If the market tanks, you can draw from that, and if it soars, you can draw from your equity position and/or from stock dividends and bond coupon payments.

David Edmisten, CFP®, Founder, Lead Advisor, Next Phase Financial Planning, agrees, saying, “The biggest mistake I see clients make is not having adequate cash and short-term reserves in retirement. I’ve had a few clients fall victim to sequence-of-returns risk because they didn’t follow our advice to put a reserve in place.

“When a client takes monthly withdrawals and relies on stock market returns, their portfolio can get into jeopardy when there’s a big stock market decline. Most people are slow to change their spending habits in retirement. But if you’re withdrawing the same sum each month, and your portfolio drops because of market declines and your normal withdrawals, it can devastate the remaining value of your retirement savings.

“We recommend our clients have at least 12 months of their planned spending in cash, and another 3-5 years’ worth of spending in short-term, interest-bearing investments. This gives them several years’ worth of spending dollars that aren’t impacted by stock market declines. It also helps them be patient and avoid the temptation to sell stocks in a bear market because we’ve secured the funds they need to spend to enjoy retirement.”

3. Mitigating Interest Rate Risk

To mitigate interest rate risk, you can purchase immediate annuities or single-premium deferred annuities (SPDA) when interest rates are higher. Choosing a fixed interest option will keep your interest rate from dropping if market interest rates drop or if the stock market underperforms. You can also allocate at least a portion of the equity portion of your portfolio to high-dividend stocks and funds investing in those.

However, Josip Dunat, Wealth Advisor at The Sturkie Wealth Management Group, cautions, “While annuities can be a valuable part of a retirement strategy, some salespeople use clients’ fears of further market losses to lock them into a long, low-cap-rate product that severely underperforms the market over the long run. Last year, some clients showed us statements where their portfolios were credited 4% while the S&P 500 achieved a 27% return. Just like you wouldn’t ask a car salesman if you need a new car, take your financial advice from a professional who’s agnostic around your portfolio and whose priority is the long-term success of their clients.”

4. Mitigating Inflation Risk (Especially Healthcare Inflation)

To mitigate against inflation risk, you can invest in assets that typically grow faster than inflation, such as equities; and ones that are guaranteed to outpace inflation, such as Treasury Inflation-Protected Securities (TIPS).

5. Mitigating Investor Behavior Risk

This is one mitigation that’s entirely up to you. The first step is to honestly assess how big a drop in your portfolio value you’d be willing and able to ignore and stay the course. Then, allocate your investments between equities and assets with lower risk accordingly.

Next, stop obsessing over the markets and don’t listen to all the so-called market mavens. They don’t know any better than you how well the markets will perform tomorrow, or next week, month, or year. Warren Buffet wrote in one of his famous annual letters to investors in Berkshire Hathaway that he doesn’t understand why the same people who would delight in a half-off sale at their favorite store in the mall would panic when the market drops by 50%, giving them a golden opportunity to buy great companies’ stock on sale. When the markets tank, don’t sell in a panic. In fact, consider if it’s a great buying opportunity, and possibly move more money into equities. Conversely, when markets soar, consider taking some profit by rebalancing your portfolio to your planned equity allocation.

If needed, use a financial advisor to help you restrain yourself from figuratively shooting yourself in the foot, by panic-selling in a bear market, which only serves to lock in your losses.

6. Mitigating Longevity Risk

To mitigate against the risk that you outlive your money, make sure you draw a percentage of your portfolio that’s likely to allow a safe multi-decade retirement. The famous 4% rule suggests drawing 4% of your portfolio in your first year in retirement, and adjusting that dollar amount each year by the previous year’s inflation rate. While historical data up to the 1990s showed this would offer a safe method for a 30-year retirement, as I recently wrote, a study by David Planchett shows that a more appropriate initial draw based on forward-looking estimates would be 3%.

Further, you can increase that percentage by growing the portion of your wealth that provides guaranteed income (e.g., Social Security, fixed annuities, pensions, etc.), and decreasing the fraction of your retirement spending that’s non-discretionary (e.g., mortgage payments, utilities, car loan payments, etc.). That latter will give you more freedom to reduce your spending in down years, preserving more of your portfolio’s value.

A fixed annuity, whether an immediate annuity or an SPDA will increase your guaranteed income for life, reducing the likelihood and impact of longevity risk. This also helps reduce market risk, and if the annuity has an inflation-adjustment rider, it can mitigate inflation risk as well.

Finally, consider claiming your Social Security benefits, up to age 70 if you can afford it, which will increase your benefits. Claiming benefits at the early retirement age of 62 will cut your benefits by 30% permanently relative to your full-retirement-age benefits. On the other hand, delaying beyond your full retirement age (FRA) permanently increases your benefits by about 8% for each year of delay. If your FRA is 67, claiming at age 70 will increase your benefits by about 77% compared to claiming at age 62.

7. Mitigating Health Risk

The best way to mitigate your health risk is to shift your lifestyle choices to a healthier diet, regular exercise (which could be simply walking for an hour each day, but would ideally include workouts several times a week). Make sure you have adequate health insurance, including dental coverage since Medicare excludes most dental care.

If you have a high-deductible health insurance policy, it may make you eligible for investing in a Health Savings Account (HSA). This account has better tax advantages than even the best retirement plan. Contributions are tax deductible, you can invest the money and its growth isn’t taxed, and withdrawals used for qualified medical expenses are tax-free. If you contribute into an HSA each year you can, and never withdraw from the account until you retire, you reduce the after-tax cost of your healthcare.

Finally, consider also buying long-term-care insurance to avert devastation of your savings if you need in-home care for years. If you do buy this coverage, purchasing it long before you’re likely to need it, say in your fifties will make it less expensive, and reduce the risk of developing health problems that cause insurers to decline to sell you such a policy.

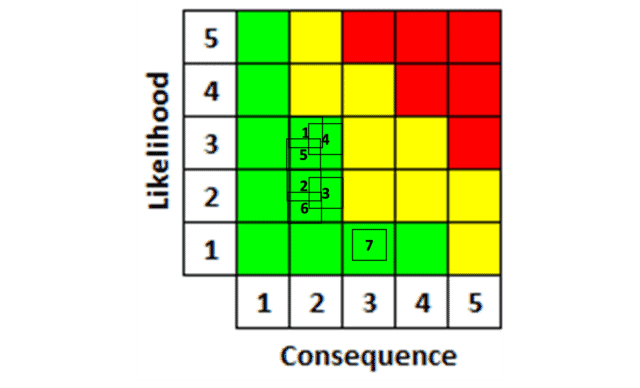

Step 5. Reassess each risk’s post-mitigation likelihood and consequence.

If you successfully and effectively apply all the above mitigations, your risk “fever chart” may look more like the final graphic below. Here, all risks are down to the “safe” green zone. This isn’t to say that your retirement plan is 100% safe from any risk. If nothing else, there could be a worldwide economic meltdown that devastates all asset classes at the same time, forcing you to draw down your portfolio. Another round of stagflation like the 1970s could hit, bringing a combination of high inflation with stagnant or even negative economic growth.

However, following the steps outlined above could dramatically reduce the likelihood of your retirement plan going off the rails, and if bad things happen, the impact on your retirement will be much easier to bear.

The Bottom Line

As I said at the start, life is full of surprises, including many unpleasant ones. This is just how things are. However, if you prepare for the biggest risks and mitigate them, your retirement will likely be more comfortable. As important, you need to avoid unforced errors, e.g., due to poor advice.

Todd Pouliot, AIF, Gateway Financial, gives an example of such an unforced tax-planning error, “The point of good tax planning isn’t about paying the least taxes in any one year, but rather the least taxes over your lifetime. If you fail to make that distinction, things can go badly.

“People often blindly accept advice on Roth conversions without considering Medicare’s Income-Related Monthly Adjustment Amount (IRMAA). I recently took on a new couple who live on Social Security and qualified tax dollars only. They did a rather large IRA distribution and Roth conversion totaling $280k. Neither their advisor nor their CPA reviewed the impact on their IRMAA. They were told to “fill up” the tax bracket by nearly $40k, unaware this pushed them into the $306,000 Modified Adjusted Gross Income (MAGI) bracket. As a result, they’ll have to pay monthly adjusted Part B and D premiums of $264 and $51, respectively!

“This is a perfect example of how poor tax planning can lead to a large loss of assets.”

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Learn More About Opher

Wealthtender is a trusted, independent financial directory and educational resource governed by our strict Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we always operate with integrity and transparency to earn your trust. Wealthtender is not a client of these providers. ➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor