It’s easy to get excited about everything “out there” and forget all the local resources at your disposal. Retirees often have more programs and services available than they might realize. Not every benefit will apply to your situation, but it’s a good idea to know what’s available.

If nothing else, having a good handle on the resources in your local area might help someone else you know in need. It’s important to stay informed about resources for a successful retirement.

Why Local Benefits Matter More Than You Think

Community programs can dwindle and die because of underutilization. Unfortunately, many programs aren’t used due to a common misconception of services being intended for “someone else.” If you qualify for a beneficial program or service, you need to explore it.

Also, by using a benefit or service, you can help others who might benefit from it. There’s nothing better than first-hand experience to help you guide someone else. Regardless, don’t let these benefits go unused!

Reducing Fixed Expenses in Retirement

When it comes to reaching our financial goals, retirement or otherwise, you really only have three main levers: spend less, make more, or adjust your goals. If you’re able to take advantage of programs and services, you can help reduce your expenses. This can be especially helpful for retirees on a fixed income.

Increasing Your “Spendable” Income Without Taking More Risk

At the end of the day, only the money you get to spend matters. If you’re able to take advantage of local tax breaks or incentives, you can increase your “spendable” money. This keeps more money in your nest egg without adding risk.

Many Benefits Go Unused

By some estimates, seniors miss out on billions of dollars of unused federal aid each year. Not everyone qualifies for these programs, but it’s worth taking a look. There are many programs looking to help.

Property Tax Relief Programs

Once you cross the threshold into retirement, taxes often become one of your major expenses alongside healthcare. Even if you paid your mortgage off, you often can’t escape property taxes. Luckily, there are some programs to help alleviate some of your property tax burden.

We can’t speak for all states, but in Missouri and Kansas, where most of our clients live, programs operate very differently. You’ll need to check with your local county, city, and state government offices to find out if they offer tax relief programs. We’ll touch on Missouri and Kansas briefly so you can see what we mean.

Missouri Property Tax Credit and Freeze Programs

For Missouri property tax freeze programs, each county decides whether to participate and how to administer it. With 114 different counties in Missouri, it’s impossible to keep track of them all. Be sure to check with the local county assessor’s and collector’s offices to learn more.

Kansas Homestead and Refund Programs

On the West side of the Missouri River, Kansas operates its property tax freeze programs much differently. There are three separate programs: the Homestead Refund Program, the Safe Senior (SAFESR) Program, and the Senior or Disabled Veteran (SVR) Program. The eligibility criteria for the property tax freeze programs are somewhat restrictive, so you’ll need to check to see if you’re eligible for them.

Additionally, each county can keep overall tax collections the same each year (revenue-neutral), but many don’t.

Why This Matters for Long-Term Planning

The recent explosion in real estate prices since 2020 has caused many seniors’ property taxes to increase significantly. Over time, these higher evaluations can lead to ever higher property taxes for the same home. All while your income may stay the same or even decrease relative to inflation.

Healthcare and Prescription Cost Assistance

Healthcare is one of the most important issues retirees face, if not the single most important issue. Your access and ability to pay for quality healthcare are huge quality-of-life concerns. Be on the lookout for assistance through federal and local government programs.

It’s a good idea to know about these programs even if you’re not eligible. Even if it’s not helpful to you, it may be useful to friends and family who need some assistance.

These often have eligibility requirements, but they vary by program.

Local Clinics and Community Health Resources

Don’t forget to check for other organizations and nonprofits in your local city and county. There are too many resources to list here, but you never know what’s available until you check.

Utility and Everyday Cost Savings

Some programs are specific to certain age groups, disabilities, or other specific qualifying needs.

Utility Assistance Programs

There are several utility assistance programs available to low-income households or senior citizens. Many local electric cooperatives and/or utility companies will have information on their website. A good place to start looking is the local United Way or the nearest Salvation Army.

Transportation and Senior Discounts

If getting to and from the doctor’s office or grocery store becomes difficult, you may be in luck. There are generally several resources available to you. Search for local transportation resources available to you.

Veteran-Specific Benefits

If you or your spouse served in the military, you might be eligible for many services, programs, and discounts. It’s always a good idea to check the National Resource Directory for benefits you may qualify for.

You should be aware of scams. Veterans are never required to pay to apply for or access VA benefits.

Property Tax and Housing Benefits for Veterans

Many states offer an array of tax benefits for military members and veterans. Many of these are specific to the veteran’s VA disability rating, so filing a claim for a service-connected disability should be the first step.

Why Coordination Matters

For veterans, you may need to create a “roadmap” to benefits because many benefits might qualify you for additional benefits. For instance, having a documented service-connected disability may qualify you for additional benefits. Also, you may be eligible for multiple versions of similar benefits.

If you’re not careful, you might end up with a confusing array of benefits which serve similar needs.

Start with Federal, State, and County Resources

Many local benefits depend on funding or eligibility from federal or state benefits. For instance, some prescription programs only apply if you’re already enrolled in Medicare. In other cases, SNAP eligibility might automatically qualify you for other community resources.

However, most local community organizations will help point you in the right direction.

Work with a Financial Planner or Counselor

Just because you’re in a good financial position doesn’t mean you don’t qualify for local resources. It also doesn’t mean you don’t “deserve” help either. If you qualify for a benefit, we’d encourage you to apply.

Most of the time, a financial planner or counselor in the area will have a newsletter or blog with local resource information. Even if you don’t work with them directly, these folks can be a great resource for up-to-date information and insights.

Review Annually

We recommend checking for new benefits and programs each year. It’s common for programs to be shut down or defunded, consolidated, or modified over the years. It never hurts to spend a few minutes checking for new programs.

Bringing It All Together

At the end of the day, knowing your local resources can help you build a more efficient retirement plan. More than likely, your tax dollars fund many of the programs we talked about either directly or indirectly. You may as well get some use from them if you’re eligible.

Stay informed about your local community resources and get the most out of your retirement!

This article reflects the insights and opinions of its author and is not a recommendation or endorsement of their views or services.

About the Author

Clint Haynes, CFP®Helping you build a retirement with pleasure, purpose, and peace of mind.

Ask ten financial advisors whether you should pay off your mortgage before retiring, and you’re likely to get ten different answers — and all of them might be right, depending on your situation. The conventional wisdom that responsible retirees enter retirement debt-free has real merit for some people, but for others it’s a rule that delays retirement unnecessarily, drains liquidity at the worst possible time, and trades a manageable fixed payment for a portfolio too small to weather a market downturn. The real question isn’t whether carrying a mortgage into retirement is good or bad. It’s whether you’re evaluating the right factors — interest rate, tax consequences, guaranteed income, liquidity, and emotional tolerance — to make the decision that’s actually right for you.

Until last year, my wife and I were paying three mortgages. One on our old house, which we kept as a residential rental. Another for an office suite we both use and partially lease to others. The third for our current home.

When we’d had enough of being residential landlords, we sold the rental property, leaving us with two active mortgages. Then I reached a personal and professional decision point: should I mostly retire, or keep running my consulting business full-time?

I chose retirement.

If you were advising me then, you might have asked, “But what about the mortgages? Are you planning to pay them off?” That would have been a fair question. For many people, being debt-free feels like a requirement for retiring responsibly.

In our case, the math didn’t force the issue. We could pay off the mortgage without draining our savings, but both loans carry low fixed rates, so the payments are manageable.

Still, we’ve long planned to downsize. As empty nesters who live close to our kids, we love our home, but it’s more house than we need. But now, things aren’t so simple.

Even if we move to a home costing half as much as our current home and put 20% down, the new mortgage payment would be higher than our current one because today’s rates are so much higher. Downsizing would still reduce our cash-flow needs by lowering utilities, property taxes, maintenance costs, and insurance premiums, so it’ll likely be the right decision in the short to medium term.

But then, we’d face a familiar dilemma: should we buy the next place in cash, or take out a new mortgage and invest the difference? This isn’t a simple “pay it off or don’t” decision.

Even financial advisors don’t all agree. Some say retirees should do everything they can to enter retirement debt-free and stay that way. Others argue that tying up so much net worth in home equity reduces your retirement income and flexibility.

The real issue isn’t whether a mortgage is good or bad, even in retirement. It’s whether you’re evaluating the right factors so you can make the decision that’s right for you.

Key Takeaways

1

Paying off your mortgage before retirement isn’t always the safer choice.

Eliminating a mortgage reduces fixed expenses and provides peace of mind, but it also converts liquid, income-generating assets into illiquid home equity. For retirees with low-rate mortgages or limited portfolio size, paying off the loan can actually increase financial risk by reducing flexibility exactly when you need it most.

2

The mortgage payoff decision must be evaluated as part of your full retirement plan — not in isolation.

Key factors include your mortgage interest rate, the tax consequences of liquidating assets to pay it off, how much of your fixed expenses are covered by guaranteed income sources, and how much liquidity you’ll retain afterward. A large IRA withdrawal to clear a mortgage, for example, can trigger bracket creep, IRMAA surcharges, and a permanently smaller tax-deferred base.

3

A third option — partial paydown with a dedicated mortgage reserve — often beats paying off or keeping the loan outright.

Recasting the mortgage after a partial paydown, or setting aside short-duration Treasuries or a laddered CD portfolio to cover remaining payments, can capture most of the psychological benefit of debt elimination while avoiding a one-time tax event and preserving liquidity. Most retirees don’t realize this middle path exists until a financial advisor models it alongside the two obvious alternatives.

Why the “Pay Off Your Mortgage Before Retiring” Rule Can Backfire

For many people, the idea of keeping a mortgage into retirement feels not just suboptimal, but outright wrong, maybe even irresponsible.

Blame decades of conventional advice that said the only way to retire responsibly is to pay off your mortgage and any other debt you may have.

That doesn’t mean this view has no merit. If you do this:

Your retirement expenses are lower, making your lifestyle easier to sustain.

No lender can come in and take away your home for missing a few payments.

As a result, there’s the very real emotional comfort of owning your home outright.

That’s why it feels so obvious that if you can pay off your mortgage before you retire, you should absolutely do that.

However, this approach treats your mortgage as a standalone problem you need to solve, rather than as one piece of your larger financial puzzle.

And that’s the pitfall.

Because once you choose to accept that you must pay off your mortgage before retiring, it can dramatically delay your retirement age, just because you haven’t yet “checked that box.”

This, even if your overall financial picture can support it,

The result is that you aren’t optimizing for the life you want to live in retirement. Instead, you’re optimizing for following conventional wisdom that may not be wise for you.

Why Financial Advisors Disagree on Paying Off Your Mortgage in Retirement

Some advisors argue passionately that paying off your mortgage as early as possible, especially if you’re about to retire, or already in retirement, is one of the best moves you can make.

Others make just as strong a case for keeping that mortgage in place, especially if the interest rate is fixed and low.

Both sides’ reasoning is valid, for certain people, in certain circumstances.

A perfect example of why it’s called personal finance.

Advisors who favor paying off your mortgage focus on the resulting simplicity and certainty. It eliminates a high fixed cost from your monthly budget, reducing the retirement income you need. This is especially important during a market crash, when your portfolio is down, and you want to avoid, or at least minimize, selling shares.

Seen from that perspective, retiring your mortgage reduces risk and increases stability.

The advisors who argue the opposite focus on flexibility and opportunity.

If you pay off your mortgage, you’re tying up a large chunk of your investable capital in an illiquid asset that provides no income – home equity. This is often described as a “phantom return” equal to the interest rate of the loan you’re paying off.

As Chris Chen, CFP, Wealth Strategist, Insight Financial Strategists, says, “The decision isn’t as straightforward as having cash hanging around in your checking account. For example, you may have held your 30-year mortgage for, say, 20 years. At that point, most of your payment goes toward paying off the principal, essentially moving money from your checking account into your home equity. Very little goes to interest. Suppose you have to take an IRA distribution to pay off the mortgage. Does that distribution interfere with your other goals, such as Roth conversions? Does the distribution make you jump a tax bracket, resulting in a higher tax bill? There is no way to know until you run the scenario.”

Jeffrey J. Smith, Founder & Managing Partner, Owl Private Wealth Advisors, expands, “Paying off your mortgage for most is a financial goal that has been worked for multiple decades. Up until 2020, many soon-to-be retirees likely had a mortgage rate of 5%+, but now we see that same demographic of soon-to-be or recent retirees locked in at historically low rates sub 4%, these historically low rates have made the decision a bit murkier.

“For many, the decision to pay off or not to pay off the mortgage is part math and part emotion. If they have excess savings in non-qualified accounts, it likely makes sense to pay off the mortgage with those funds simply for the sleep-well factor.

“If overfunded with qualified retirement savings, it becomes more complicated. Paying off the mortgage with those funds will have implications not only for your current tax year but also for 2 years later, with the potential for higher Medicare Income-Related Monthly Adjustment Amount (IRMAA) premiums, given the 2-year look-back. As stated above, this is a personal decision that can only be made after a careful discussion with the client and their advisor on what is best for their personal financial goals.”

Peter Bo Rappmund, Principal at Counterpoint, agrees, “I lean toward paying off the loan when the math is close and the mortgage creates real friction in a client’s retirement plan. The clearest ‘yes’ cases I see are when a client has a higher-rate mortgage (6% or higher) that they took out in the last few years, the payoff doesn’t require liquidating assets that would trigger a meaningful tax event, and after the payoff, they still have 12–24 months of liquid reserves plus comfortable headroom in their portfolio to cover essential expenses.I’m also more inclined to recommend a payoff when a client takes the standard deduction anyway, that, post-Tax Cuts and Jobs Act (TCJA), is most retirees, because they’re getting no tax benefit from the interest, so the mortgage rate is effectively the after-tax rate.

“Behavior matters too. For clients who genuinely sleep better without the debt and who aren’t going to redeploy their freed-up cash flow into something riskier, the psychological return is real and worth pricing in.”

Especially today, when so many mortgages are fixed at historically low rates, like our 30-year fixed 3% loan. That’s a very low return compared to what that capital could likely earn if invested for retirement income.

According to DQYDJ.com, the median net worth for Americans in their late 60s is $394k. That’s not very high relative to what’s needed for a comfortable retirement. Worse, however, is that two-thirds of that net worth is tied up in home equity, leaving just $132k to generate income to supplement Social Security retirement benefits.

Anything that ties up a large fraction of your net worth in home equity makes it that much harder to have a reasonable retirement income.

Seen from this perspective, a mortgage isn’t just a liability. It’s a tool for maintaining liquidity, increasing retirement income, and increasing your margin of safety.

That’s why the argument isn’t really about whether keeping a mortgage is good or bad.

It’s about what risk you’re trying to reduce or remove, and which risk you’re more comfortable living with.

Do you prefer predictability and stability, risking a lower standard of living, or would you rather optimize for higher income along with potentially better long-term outcomes?

Neither is universally better.

Each solves for different objectives, which is what makes this a matter for careful, personalized assessment.

How Paying Off Your Mortgage Affects Your Entire Retirement Plan

From the above, it should be clear that framing this as a “mortgage = good/bad” decision is what leads to confusion and disagreement.

Because paying off your mortgage isn’t a simple decision with pros and cons that are independent of the rest of your financial picture.

It’s just one part of your overall finances, along with your income, investments, and spending, and how large or small, and how flexible or fixed, they are.

It’s more useful to shift the question from “Should I pay off my mortgage before or early in retirement?” to “How does paying my mortgage off before retirement (or in early retirement) affect my overall financial safety?”

Once you change your perspective like that, whether to keep the mortgage or pay it off stops being a standalone decision and becomes an integral part of your overall financial plan.

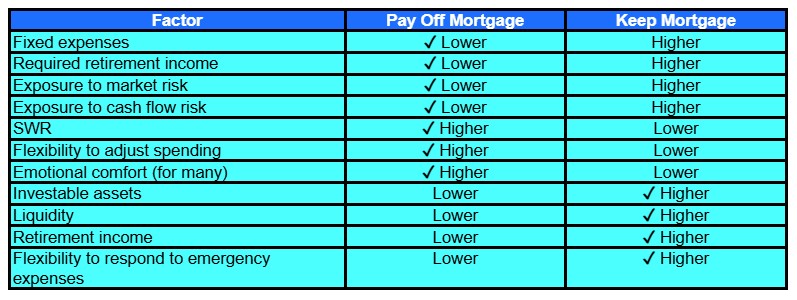

Paying off your mortgage:

Reduces your fixed expenses.

Lowers the retirement income you need to generate.

Per research by David M. Blanchett, PhD, CFA, CFP®, reducing the fixed fraction of your retirement budget lets you increase your safe withdrawal rate (SWR) by ~7% (Blanchett, Head of Retirement Research at Morningstar Investment Management, found that reducing your fixed expense fraction from 75% to 25%, with certain reasonable assumptions, increases SWR from 4.1% to 4.4%).

However, paying off the mortgage also:

Reduces your investable assets.

Reduces your retirement income.

Reduces liquidity and flexibility to respond to unexpected expenses and/or unexpected opportunities, should your circumstances change.

Obviously, keeping your mortgage does the opposite.

Keeps fixed expenses higher.

Requires higher retirement income.

Reduces SWR.

Keeps investable assets higher.

Increases retirement income.

And maximizes liquidity and flexibility.

That’s the trade-off most people miss.

They focus solely on the mortgage decision and miss its implications for flexibility, adaptability, and safety in retirement. And, in retirement, adaptability and safety are every bit as important as optimization, if not more so.

Table 1 shows the factors affecting your decision and how each influences it. In each line, the check mark indicates the preferred outcome.

Table 1. These key trade-offs affect your decision about whether to pay off your mortgage or keep it in retirement.

Why Fixed Expenses Matter More Than Most People Realize

While you’re working, fixed expenses can be a very good thing.

A fixed-rate mortgage means your principal and interest payment never increases during the life of the loan. No landlord raising rents, and no variable-rate loan letting the lender increase your interest rate when the market turns against you.

Predictable and stable.

As long as your income stays stable, you have little to worry about. And if something unexpected happens, you can, e.g., work longer hours, start a side gig, and/or cut expenses elsewhere.

In retirement, your earnings stop.

Instead, you depend on Social Security, pensions, if any, annuities, if any, and withdrawals from your portfolio.

The first three are predictable, but small to non-existent for most people.

The main source for a comfortable retirement is the last, portfolio-based, assuming you saved enough. Unfortunately, the markets are anything but predictable.

On average, stocks return about 10% a year. But they could gain 50% one year and drop 40% the next.

That’s why flexibility and margin of safety matter even more in retirement.

Fixed expenses like a mortgage, that can’t easily be reduced, make you less flexible.

If markets decline or expenses spike, especially early in your retirement, you have lower discretionary spending, reducing the area where it’s usually the easiest to trim costs when needed.

If you need to cover higher expenses and/or have to sell more shares at depressed prices during a bear market to make ends meet, your risk of running out of money increases.

On the flip side, if more of your spending is discretionary, you have more levers to pull to respond to a market crash and/or an expense spike. You can temporarily reduce travel, delay replacing the car, scale back gift-giving, etc., all without disrupting your core lifestyle for long.

On the other hand, even with somewhat higher fixed expenses, a significantly larger portfolio increases your baseline retirement income, which gives you a greater margin of safety, either by allowing you to increase your discretionary spending even more (so a larger fraction of your budget is discretionary) or by drawing a smaller percentage of your portfolio value each year.

Why Downsizing Doesn’t Eliminate the Mortgage Trade-off in Retirement

Downsizing seems like an attractive option for many retirees facing cash-flow limitations.

You sell an expensive home that’s larger than you need, and buy a smaller, less expensive one. This lets you eliminate your mortgage or at least replace it with a smaller loan.

Ideally, that smaller loan means lower monthly payments.

Except when it doesn’t, like in our case.

As mentioned above, our current mortgage rate is so much lower than the current market rates that we could move to a home that costs half as much as our current one, take a new mortgage with 20% down, which would significantly reduce our mortgage balance, and end up with a higher monthly payment than what we’re paying now.

At the same time, downsizing will reduce other costs:

A smaller home is easier to manage and cheaper to maintain.

It also tends to reduce utility expenses.

A less expensive home usually means lower property taxes.

It’s also typically less expensive to insure.

All of these reduce monthly cash flow needs, which is an important goal in retirement.

So, we’re still likely going to downsize, at which point we’ll come up against a similar trade-off. What do we do with the equity we unlock from our current home when we sell it?

Do we use most of it to buy a less expensive home outright, with no mortgage, or do we use a small portion of that equity to put down just 20% for a new loan?

This decision goes back to the trade-offs we described above, for eliminating your mortgage before retirement or keeping it in place.

The former would dramatically reduce our cash flow needs and fixed expenses. Still, it would also cost us the opportunity to increase our investable assets and the greater margin of safety that higher retirement income provides.

The latter would reduce our cash flow needs and fixed expenses, but nowhere near as much, because we’d still have the large mortgage payment. However, it would significantly increase our portfolio size, and, along with that, our retirement income and the resulting margin of safety.

Downsizing changes the specifics, but it doesn’t eliminate the trade-offs and the decision.

A Better Framework for Deciding Whether to Pay Off Your Mortgage in Retirement

As we said before, there isn’t a single, universally correct answer that tells you to eliminate your mortgage before retirement (and stay debt-free thereafter), or not.

But that doesn’t mean you have to guess.

You just need better questions and a better decision framework.

Rather than considering the mortgage payoff question in a vacuum, you need to evaluate the multiple impacts on your overall financial situation.

With the mortgage vs. without it, how much of your budget is fixed and non-negotiable, and how much is discretionary? The higher your fixed expenses, the more income you need in retirement, regardless of your portfolio’s performance in any given year. This puts more pressure on your investments and makes it harder to adapt when needed.

Next, how much of your fixed expenses are covered by predictable sources like Social Security retirement benefits (which also get adjusted up for inflation), pensions, and annuities? The higher the portion of fixed expenses that you can cover from predictable income, the less you need to take from your portfolio, which is especially important when, not if, the market crashes. This gives you more flexibility in managing your investments.

Now, look at liquidity. How much of your net worth is tied up in your home equity, which is illiquid and doesn’t generate income that lets you cover unexpected (or even planned-for) expenses? Paying off the mortgage (and not taking out a new one) increases the part of your net worth that’s tied up and non-productive like that. Keeping your mortgage (or taking out a new one when downsizing) does the opposite.

Beyond the numbers, it’s time to look at the emotional aspect. When the market crashes, how comfortable will you be with having to continue making fixed mortgage payments? Or would eliminating that mortgage make it easier to stick with your financial plan? Your answers to this point are at least as important as the results of the above three calculations.

Finally, consider your margin of safety. Is your portfolio large enough to comfortably support your lifestyle, even when things don’t go exactly as planned? Or are you so close to the edge that you need to do something to increase your margin, e.g., by increasing your productive investments?

Putting all these factors together is how you can make a holistic decision that accounts for the multiple ways that eliminating or keeping the mortgage will affect your retirement in the long term.

After all, that’s the critical goal here.

Not to become debt-free at all costs, and not to maximize returns at all costs.

But to build a plan that offers you a combination of stability, flexibility, margin of safety, and long-term sustainability that you’re most comfortable with and lets you stick with the plan.

Rappmund offers a comprehensive, balanced look at when to pay off vs. when not to. “I lean toward paying off the loan when the math is close,and the mortgage creates real friction in a client’s retirement plan. The clearest ‘yes’ cases I see are when a client has a higher-rate mortgage (6% or higher) that they took out in the last few years, the payoff doesn’t require liquidating assets that would trigger a meaningful tax event, and after the payoff, they still have 12–24 months of liquid reserves plus comfortable headroom in their portfolio to cover essential expenses.I’m also more inclined to recommend a payoff when a client takes the standard deduction anyway, that, post-Tax Cuts and Jobs Act (TCJA), is most retirees, because they’re getting no tax benefit from the interest, so the mortgage rate is effectively the after-tax rate.

“Behavior matters too. For clients who genuinely sleep better without the debt and who aren’t going to redeploy their freed-up cash flow into something riskier, the psychological return is real and worth pricing in.

“I push back hard when paying off the mortgage would require a large taxable distribution from a traditional IRA or 401(k), or a concentrated capital gains realization. Especially if it pushes the client into a higher marginal bracket, triggers IRMAA surcharges, or causes more of their Social Security benefit to become taxable.

“I also advise against it when the mortgage is a legacy (3% or lower) loan; that’s an inflation hedge and a negative-real-rate liability you generally don’t want to retire early. And I won’t sign off on a payoff that leaves a client house-rich/cash-poor, because home equity is the least useful asset in a downturn. You can’t eat it, and a Home Equity Line of Credit (HELOC) can be frozen by the bank at exactly the time you need it most.”

But even when the math seems clear, mistakes are common. Rappmund shares several common mistakes people make: “The single most common mistake I see is comparing the mortgage rate to a hoped-for portfolio return without adjusting for risk, taxes, or sequencing. A client says, ‘My mortgage is 4%, and my portfolio earns 8%, so it’s obvious.’ That comparison is wrong on two fronts: paying off the mortgage is a guaranteed, after-tax return equal to the mortgage rate, while the 8% is a pre-tax, risk-bearing expected return that includes years like 2008. The right comparison is the mortgage rate vs. the after-tax yield on a similar-duration, low-risk bond. On that basis, the decision is much closer than people think.

“The second mistake is solving for net worth instead of cash flow. Retirement is often fundamentally a cash-flow problem, not a balance-sheet problem. Two clients with identical net worth can have radically different retirement experiences depending on how much of their monthly expenses are fixed and inflexible.

“And the third, which I see all the time, is making this decision in isolation, separate from the tax plan. Pulling $300k out of an IRA in a single year to clear a mortgage can cost a client tens of thousands in avoidable taxes and Medicare premium increases, and it permanently shrinks the tax-deferred base that was going to compound for the next 20 years.”

So how should you actually evaluate the trade-offs? Rappmund describes how he helps clients with this, “I help clients weigh the tradeoff between reducing fixed expenses and preserving liquidity and investment income in retirement by separating the question from the math and asking what role this decision plays in the plan. We map out essential expenses (housing, food, healthcare, insurance) vs. discretionary, and we look at what’s already covered by guaranteed income (Social Security, pensions, and annuities).

“If the mortgage payment is the difference between essentials being covered by guaranteed income and not, that’s a strong argument for retiring the debt; you’re effectively buying yourself a higher floor and reducing sequence-of-returns risk in the early retirement years, which is when portfolio damage is most permanent.

“From there, we run the actual numbers in the financial plan, modeling paying it off, keeping it, and a third path. And I almost always show a third option, because most clients don’t realize it exists. That path is something like recasting the mortgage after a partial paydown or carving out a dedicated mortgage reserve in short-duration Treasuries or a laddered CD portfolio that earns close to the mortgage rate and gives the client the option to extinguish the loan later if rates or circumstances change.

“That tends to be the right answer surprisingly often, as it captures most of the psychological benefit and avoids a one-time tax event. The frame I leave clients with is that liquidity is itself a form of insurance, and in retirement, it’s one of the cheaper kinds you can own.

“Paying off the mortgage converts a flexible asset (cash and securities) into an illiquid one (home equity), and that conversion is irreversible without taking on new debt at whatever rates happen to exist when you need it. So, the question isn’t really ‘should I pay it off?’ Rather, it’s ‘what’s the right amount of fixed-expense reduction I can buy without giving up more flexibility than I can afford to lose?’”

The Uncomfortable Truth About Entering Retirement Debt-Free

For many retirees or near-retirees, believing the conventional wisdom that “you must enter retirement debt-free” is worse than outdated.

If accepting that paying off your mortgage is a go/no-go gate for entering retirement forces you to:

Delay retirement for years.

Tie up too high a fraction of your capital in home equity that generates zero income.

Reduce your liquidity to the point where you have no good options when something unexpected happens.

Then, following this “rule” can increase your risk and possibly cause you far more financial harm than good.

It’s counterintuitive. Eliminating your mortgage feels like it should reduce your risk, but in some situations, it can leave you more exposed rather than less.

It removes a fixed obligation, simplifies your finances, and reduces the retirement income you need. But it does so while reducing your retirement income, increasing the risk that you’ll need to sell assets when they’re depressed, and leaving you with less liquidity and flexibility.

Over a decades-long retirement, in many situations, those risks may be the ones you’re less comfortable carrying.

That’s why there isn’t a universally correct answer to the question of eliminating your mortgage before retiring. It’s because the “enter retirement debt-free” rule, like any other financial rule, is designed to offer a simple shortcut for making decisions.

But your situation isn’t simple.

It’s multi-faceted and different than anyone else’s.

A complexity that simple “rules” can’t capture.

The Bottom Line: Should You Pay Off Your Mortgage Before Retiring?

As frustrating as it may be, I can’t give you an answer on whether you should wait until you’ve paid off your mortgage before entering retirement, or even whether taking out a new mortgage in retirement when downsizing makes sense.

That’s because my answer is just that – mine.

You need your answer.

And that answer depends on many factors:

How large is your nest egg?

How high a retirement income do you need to be comfortable?

How will paying off your mortgage affect those two answers?

What risks are you comfortable carrying, and which ones do you need to avoid?

Which decision gives you the best chance of sustaining your desired lifestyle in retirement over the long haul?

Can you, emotionally, stick with a plan that keeps a mortgage into retirement?

For many people, these factors result in a preference for paying off their mortgage.

For many others, they’ll point to keeping the mortgage in place for as long as possible.

Both approaches are right, given the right circumstances. And both are wrong given the wrong situation.

Your bottom line must be based on a clear understanding that the mortgage payoff decision must be made as part of a comprehensive assessment of your personal situation, goals, and risk preferences.

Because to have a good retirement, your decisions can’t be based on box-checking.

They need to be made as part of a comprehensive plan that you can live with and stick to, through good markets and bad, because you will live through both.

As Dr. Steven Crane, Founder of Financial Legacy Builders, says, “I’d only strongly recommend paying off a mortgage if the payment is creating stress or the person needs simplicity to sleep at night. Beyond that, the math doesn’t always support it. I actually push back on people who rush to pay it off just because it ‘feels safe.’ In a lot of cases, they’re trading liquidity and flexibility for a psychological win.

“The biggest mistake is treating the mortgage like the enemy instead of looking at the full picture. I’ve seen retirees drain a large chunk of their savings to wipe out a low-interest mortgage, only to put themselves in a tighter position long term. They feel better emotionally, but financially, they’ve boxed themselves in. I frame it as control vs. comfort. Paying off the mortgage gives you comfort, no payments, and a clean slate. Keeping the mortgage often gives you more control, more liquidity, and more flexibility if something changes. Most people default to comfort without realizing what they’re giving up. Debt isn’t the problem in retirement. Poor planning is. A mortgage can be managed. Running out of options can’t.”

A practical way to start is this: picture both scenarios.

One where your mortgage is gone, but your portfolio is smaller, and one where your mortgage remains, but your portfolio is larger and more flexible.

Which scenario gives you more confidence that you can handle whatever comes next?

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

If you’ve ever pulled up a college savings calculator and felt an immediate knot in your stomach, you’re not alone — and you’re probably not as far behind as you think. The benchmarks that investment firms publish are useful planning tools, but they’re built on assumptions that rarely match any real family’s situation, and they say nothing about what actually determines whether families reach a good outcome. What financial advisors consistently find is that the decisions you make about funding, school choice, and trade-offs matter far more than the balance in a 529 account. Here’s how to stop measuring yourself against a hypothetical family and start focusing on the factors you can actually control.

If you have kids under 18, you’ve probably looked up college savings numbers.

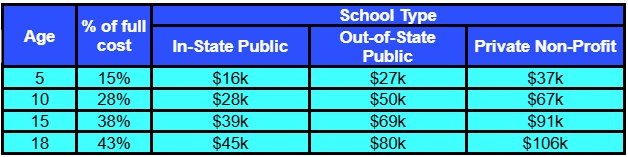

According to T. Rowe Price (TRP), for example, the full cost of attendance for a four-year degree is $103k at a public university for in-state students and $183k for out-of-state students. At a private non-profit school, that cost grows to $244k.

TRP expects parents to save up enough to pay about half of that, considering likely grants, scholarships, loans, and income from current employment during school years.

If you’re anything like my family was while our kids were growing up, it can seem like an impossible task, especially given all the competing priorities, like putting food on the table, keeping a roof over your head, and hopefully saving at least some money for retirement.

Key Takeaways

1

College savings benchmarks measure a hypothetical family, not yours.

Benchmarks from firms like T. Rowe Price assume you started saving at birth, contributed consistently, and knew years in advance which type of school your child would attend. Most families don’t fit that profile. Being behind on paper reflects those mismatched assumptions — not a verdict on whether your child can afford college.

2

Deciding how much you’re willing to pay matters more than how much you’ve saved.

Defining your funding commitment — whether that’s full cost of attendance, in-state tuition only, a fixed dollar amount, or a percentage of total cost — drives every other decision: school choice, loan strategy, scholarship goals, and how realistic your path forward actually is. Two families with identical savings balances can reach completely different outcomes based on this one conversation.

3

Retirement savings should take priority over college savings when you can’t fully fund both.

Your child has decades of options — loans, scholarships, work-study, and school choice — to fund their education. You have far fewer levers to fund retirement, and every year you delay makes the challenge steeper. Financial advisors consistently remind clients that not becoming a financial burden to your children later in life is itself one of the most meaningful things you can do for them.

When our kids were growing up, we never managed to save a single dollar toward their college costs, let alone meet TRP’s benchmarks, shown in Table 1.

Table 1. Guidelines for the amounts to be saved by children’s age and school type, per TRP (based on covering ~50% of total costs).

In practical terms, that means being expected to have tens of thousands saved well before high school. Those are big numbers, especially if you’re starting late.

Say you have a 15-year-old who has her heart set on attending a private university. Do you already have $91k in her college fund?

If you’re not on track with these guidelines, the gap can feel increasingly uncomfortable. You may be asking yourself, “Are we behind?”

And if the answer is yes, you may be thinking, “Are we failing our daughter?”

That’s a feeling I know well from firsthand experience.

Since we didn’t have a college fund, we had to figure out ways to cover those costs as we went, using current income, with trade-offs and uncertainty as our constant companions.

When our son was accepted to our state university’s flagship campus, the University of Maryland, College Park (UMCP), and to a prestigious private school he preferred, we sat him down to discuss what each choice would mean.

We could cover the full costs of a degree at UMCP without taking out loans, but the private school would have left him with many tens of thousands of dollars in student-loan debt by graduation, even considering their offer to reduce his tuition by 50%.

Conversations like this, and the decisions they led to, shaped how we paid for our kids’ degrees, how they approached school and work, and, ultimately, their careers.

All this forced us to face something that benchmarks and guidelines don’t usually address. Those numbers were never intended to be treated as a scorecard.

They’re a useful planning tool, based on specific assumptions, defined savings goals, and the ability to contribute consistently from birth to college graduation. If you’re anything like we were, your life simply doesn’t look like that.

Some families start late.

Some can’t save consistently, or at all.

Even if you saved from your kid’s birth, they may start out willing to attend their state school, only to decide later that they really want to attend a highly selective, super expensive private school. And when that happens, say when they’re 15, even in the unlikely case that you were “on track” up to that point, you’re suddenly less than halfway to where you’re “supposed” to be.

And yet, many of those families still find a way to make it work.

Not by hitting all the benchmarks on time, but by making informed decisions about what they’ll pay for, what they won’t, and how they expect their children to support the process.

Unless you’re uber-wealthy, you can’t avoid all trade-offs. But you can and should make smart choices about the trade-offs you face.

What that looks like is what we’ll cover below.

What College Savings Benchmarks Actually Measure And What They Don’t

The biggest pitfall of benchmarks like TRP’s is if you believe they’re something they’re not, which may then lead you to despair or make unsustainable decisions.

First, what they aren’t.

They’re not requirements, predictions, or guarantees.

They’re just intended to give you a sanity check. And even that’s limited, because they’re trying to give you a plausible path to successfully funding your kid’s college career, without knowing anything about your situation.

How old is your child?

What’s the full cost of attendance at the college your child will attend, and how will that cost change by the time your child graduates?

How many college years will your child need to graduate (4 is the minimum, not a maximum or even the median*)?

How many other children do you have, for whom you need to save in parallel?

How much, if anything, do you already have saved up for their college expenses?

How much can you afford to put into their college fund, and how consistently?

How will you invest that college fund, and what returns will you achieve?

* According to the National Center for Education Statistics (NCES), “In 2020, the overall 6-year graduation rate for first-time, full-time undergraduate students who began seeking a bachelor’s degree at 4-year degree-granting institutions in fall 2014 was 64 percent.” This means that more than one in three students took longer than 6 years to graduate! The median time to graduate was 52 months, and only 44.1% graduated in 4 years.

So, not knowing any of those things, they make assumptions:

You have one child (or the following is true for each of your children).

You started saving from your child’s birth and contribute a consistent amount each month.

You aim to cover 50% of the full cost from your college fund.

Your college fund is invested and will compound at a “reasonable” long-term rate.

You know the cost level of your child’s college (between the three levels they show).

With all these hypotheticals in place, they generate a plausible trajectory that helps you see if you’re ahead, on track, or behind.

But there’s a problem.

You live in the real world, not in their hypothetical “typical” scenario.

You may have started saving later than ideal.

You face competing priorities and may have had months (or years) when you couldn’t contribute as much, or at all, to the college fund.

College costs are unlikely to stay the same over the 20+ years from when your kid is born until they graduate from college.

You may think you’ll send your kid to your state’s school, but they may choose to go to a far more expensive private school.

As Cole Williams, Founder, Vessel Financial Planning, says, “Benchmarks are hard to trust because the true out-of-pocket cost varies so much from family to family. There are too many variables on the front end to know whether you’re ahead or behind.”

Using the benchmarks as gospel is like playing on a tilted playing field with moving goalposts.

Stressful and not very helpful.

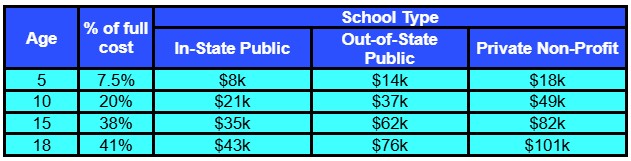

TRP recognizes this and provides a secondary set of benchmarks for parents who can’t save as much as their main model assumes, starting from their child’s birth. This secondary model assumes lower contributions early on, with contributions increasing gradually, as seen in Table 2.

Table 2. Guidelines for the amounts to be saved by children’s age and school type, per TRP’s “Ramp up” model (based on covering ~50% of total costs).

This seems much more practical because many families face higher expenses in the early years, especially for childcare, and their earnings are usually lower than in later years. As these factors reverse, it becomes easier to allocate money for college savings.

This shows that TRP realized their benchmarks need flexibility, though even this “ramp-up strategy” doesn’t necessarily account for your specific situation and how it will evolve over 20+ years.

As you can tell, these benchmarks should be viewed as one reference point, not a judgment or verdict on how successful you are.

They help answer the question: If everything went according to the specific assumptions of these benchmarks, where should I be at this point?

They don’t answer any of these questions:

Am I doing this right?

Have I already failed?

Will my child end up unable to go to college because I haven’t saved enough?

They also don’t tell you what to do next, given your specific situation, which is really the only thing that would make a difference.

Things like:

Discuss school choice with your kid and make clear what you can and likely cannot afford.

Adjust your aim to a smaller portion of the full cost of a degree, with grants, scholarships, and loans covering the remainder.

Have your kid work part-time through college to help pay tuition.

Two families can have identical college-fund balances for kids at the same age but have completely different likelihoods of success, depending on how they address potential shortfalls.

That’s why financial advisors tend to treat such benchmarks as a starting point rather than a plan. They use them to surface potential gaps, then shift to defining realistic goals, prioritizing competing needs and goals, and proposing ways of making the plan work by increasing income, decreasing spending, or a combination of the two.

As Joe Stabile, founder of Coast Financial, explains, “Most families I speak with would like to fund their kid’s college 100% if they could, but also understand it may not be realistic. I’ve found that the best way to give them confidence in their decision is to show them different scenarios on what it would take to fund different levels of college tuition. For example, showing them the monthly savings required to fund 100%, 75%, 50%, and 25% of projected college tuition at different tuition rates. Once they see these numbers and we have a conversation about their family values, they feel much more confident in their approach.”

This kind of scenario planning helps make trade-offs concrete and easier to evaluate.

In other words, benchmarks can tell you how close you are to a plausible trajectory, but don’t tell you what to do about it.

That’s our next focus.

The College Planning Decision That Matters More Than Your Savings Balance

Since benchmarks don’t tell you what to do next, what does?

The answer is both simpler and more uncomfortable than you might expect.

You need to decide how much you’re actually willing and able to pay toward your child’s college.

As Mike Hunsberger, ChFC®, CFP®, CCFC, Owner, Next Mission Financial Planning, puts it, “I find that most families are behind in saving for college and don’t understand what they’re likely to be expected to pay at different schools. While saving for college is important, choosing the best school you can actually afford has far more impact.”

That single decision drives everything else:

What type of school can your child realistically attend, cost-wise?

Will they need to take out student loans, and if so, how large?

Will they need to bring in scholarships and grants?

Will they need to work during college to help cover costs?

How much “catching up” do you have to do?

Without such clarity, you risk defaulting to “We should cover the full cost of attendance at whatever school she chooses.”

Steve Witter, CFP®, CSLP®, Founder of Student Loan Steve, warns, “The biggest mistake I see with parents is telling their kid that ‘if you get into your dream college, we will figure it out.’ With the new student loan borrowing limits and the loss of parents’ ability to repay Parent Plus loans based on income, it’s more important than ever to have a college budget and stick to it.”

Hunsberger agrees, “The most dangerous words in college planning are ‘If you get in, we’ll figure it out.’ Families need a plan and a budget for college. You don’t shop for Ferraris if all you can afford is a Honda. College shouldn’t be any different.”

Doing that could cause you to:

Stretch beyond what you can sustain.

Underfund your retirement nest egg.

Suffer long-term financial stress that lasts long after your kid graduates.

This is why a good financial advisor won’t ask, “How far behind are you?”

Instead, your advisor is more likely to ask, “What role do you want to play in paying for your child’s college?”

Your answer could be, “All costs related to getting the degree at whatever college he chooses.” And if you can afford that, without shortchanging your other priorities, your advisor will work that into your plan.

However, you could instead say, “Full cost of attendance for 4 years at the in-state tuition level,” or a fixed dollar amount, or a set percentage of total cost.

There’s no universally right answer here.

There’s just an answer that’s right for you, your situation, and your priorities.

Williams explains, “School choice still matters, but it’s not as clean as ‘public = affordable, private = expensive.’ There are exceptions on both sides. What matters more is getting clear early on whose shoulders the funding will fall. Are the parents and student willing to take on loans? Is the student prepared to do the work required to get merit-based aid, such as scholarships or grants? How much? These answers matter a lot.”

He then addresses what often happens when there are several children, “I commonly see spouses who aren’t aligned on what college funding should look like, especially with multiple kids, when ‘being fair’ becomes the goal. Fairness is our instinct as parents, but life doesn’t sit still. One spouse loses a job, or bonuses dry up, or, on the flip side, income increases. The financial picture that existed when your oldest started school often looks different by the time your youngest gets there.”

Should You Prioritize College Savings or Retirement Savings?

Except for the wealthiest among us, we all face financial trade-offs.

The biggest such trade-off regarding funding college is how it interacts, not to say interferes, with saving and investing for retirement.

Hunsberger shares how he illustrates this to clients, “I like to frame the savings choice between college and retirement in terms of how much longer the parents will need to work if they decide that funding college is the priority. If their after-tax income is $120,000 and they have 2 kids that they expect will cost $240,000 to get through undergrad, I make sure they’re willing to work for an additional 2 years.”

Williams agrees, “Every family is different, but my general coaching is to put your own oxygen mask on before helping others with theirs. Some parents commit to covering every dollar of their kid’s education without realizing that choice might require them to work three more years before they can retire comfortably. I want them to see that tradeoff clearly before they share any funding expectations with their students.”

I’m sure you’ve heard the common saying, “You can borrow for college, but not for retirement.”

And while it’s not completely accurate, since you can take out a reverse mortgage to help fund retirement, it is directionally true, since those options tend to be expensive, reduce flexibility, and leave you with a smaller cushion later in retirement.

Student loans, on the other hand, are a $1.8 trillion (and growing) industry that includes both federal and private options.

This doesn’t mean that student loans are appropriate in all cases, nor that students don’t often over-extend themselves and then struggle with years or decades of debt repayment.

But it is a broader and more readily available resource.

Peter Bo Rappmund, Principal at Counterpoint, explains, “Regarding how to balance college savings with retirement savings, especially when you can’t fully fund both, the priority is clear: retirement comes first. You put on your oxygen mask, then help your kids. Your child has decades of options to pay for college, including loans, scholarships, part-time work, and school choice. You have far fewer options to fund retirement, and they all diminish the longer you wait. I remind clients that a loving and thoughtful thing you can do for your kids is not to become their financial burden in 20 years. So, we protect retirement at the level we need to commit to, then direct what’s left toward college, and we have an honest conversation with the child about what that means for school choice.”

A Real-World Example: Starting College With $0 Saved

In our situation with my two older kids, this wasn’t a theoretical trade-off.

We barely managed to put something away for retirement. We certainly couldn’t save anything for their college expenses, so we had to figure out what we could and would do.

Their mother and I, seeing our trajectory early on, told them both, from when they were tweens, that we would cover their full cost of attendance for 4 years at UMCP in-state levels.

If they wanted to attend a more expensive school and/or if they took longer than 4 years, it would be up to them to cover the difference. This could be from grants and scholarships, or student loans.

That was the context of our later conversation with our son, which led him to decline his acceptance to the private school he initially preferred and to attend UMCP.

While this wasn’t an easy conversation to have, it was clear.

And it was that clarity that led him to make that choice, because he understood that (a) managers at the private school had a higher regard for UMCP graduates in his field than their own, all other things being equal; (b) it would be far better for him financially to avoid the crushing student debt he’d incur; and (c) his career outcome was unlikely to be affected by school choice in the long term, based on research that shows long-term earnings are often similar regardless of school selectivity.

As a result, he graduated in 4 years with a degree in his chosen field from a highly regarded school and went on to a successful career, all from a starting point of $0 in college savings when he started school.

Rappmund says such conversations are critical, “The biggest mistake I see parents make when trying to fund their child’s college education is when they avoid the conversation. Parents will save diligently for 18 years and then never sit their kid down to say, ‘Here’s what we can pay for, here’s what we can’t, and here’s what we expect you to bring or compromise on.’ That straightforwardness and clarity are worth more than another $20,000 in the 529 plan. The mistake isn’t so much that too little was saved. It’s hoping the numbers will perfectly work themselves out by the finish line.”

This illustrates the limitations of college savings benchmarks.

They focus only on the savings balance and the child’s age. Understandably, they can’t account for the things you can do to address any “paper shortfalls.” Things like setting expectations and deciding what trade-offs you’re willing to make.

Two families can have identical college-fund balances, be equally behind (or on track) on paper, and end up with vastly different ultimate outcomes. Had we encouraged our son to go to the private school, his results would likely have been far worse.

In other words, while how much you’ve saved matters, the decisions you make about funding, school choice, and trade-offs matter far more.

That’s what ultimately determines whether a family ends up with a workable outcome or one that creates long-term financial stress.

As Rappmund puts it, “Benchmarks can be a good sanity check, but shouldn’t be a scorecard. The savings balance tells me where a family stands on a hypothetical track. It tells me almost nothing about whether they’ll reach a good outcome, though. The decisions matter far more. I’ve seen families who were ‘behind’ on paper end up just fine because they had those conversations early. And I’ve seen families who were ‘on track’ get into real trouble because they never did.”

The most important takeaway here isn’t that you shouldn’t try to set aside money for your kids’ college education.

It’s that your goal can’t be to avoid every trade-off; it should be to make the trade-off choices that are right for you and your family.

Articulate and share with your kids what you’re willing and able to pay towards their college expenses. Once you do that, even if you’re far behind on paper, your path forward becomes much clearer.

What to Do If You’re Behind on College Savings

If you made it this far and still feel behind, you’re not alone.

But remember, what matters most isn’t where you are relative to benchmarks based on “typical” assumptions.

It’s what you’ll do next.

TRP acknowledges this and offers more nuanced guidance based on your child’s age.

If your kid is young, they suggest trying to redirect money spent on childcare to college savings. The point isn’t to fix everything immediately by magically making up any savings shortfall, but to concentrate on changing the trajectory.

If your kid is about halfway to college age, they suggest asking family and friends to make college-funding contributions as holiday and birthday gifts, and using income increases, and budget cutting to increase college savings. Here, the point is to make serious changes that make it at least plausible that you’ll hit your goal.

When there’s little or no time left, their guidance is to try to get scholarships, student loans, and paid internships or part-time work while in school. At this point, you’re in the situation we were in. It’s too late to save for college, but you still have options for getting to a good outcome, especially if your kid is willing to attend your state school.

In our case, we did what we needed to do:

Set clear boundaries.

Made trade-offs explicit for our kids.

Set expectations that they’d work while in school and contribute some of their earnings toward their college expenses.

We also took (legal) advantage of our state’s 529 plan rules.

In Maryland, contributions to a 529 plan may qualify for a state income tax deduction, even if the funds are used shortly after you contribute. Thus, when we needed to make a tuition payment, we first put the money into a 529 plan, then withdrew it the next day and sent it to the school.

We couldn’t benefit from the tax-free growth of investing over time in such plans, but we did get the state income tax deduction for the 529 contributions, which helped make those college expenses somewhat more affordable.

The details of 529 plan rules vary by state, so you may or may not be able to do something similar. But the broader point stands. Even late in the process, there are probably ways you can improve your situation.

The Bottom Line on College Savings Benchmarks

Benchmarks are useful tools. But they’re not a guilty verdict when you’re behind on paper.

Instead of stressing over how far behind you may be, focus on what you can still control.

Evaluate and adjust your strategy and the trade-offs you’re willing to accept.

Decide what you’re willing and able to pay.

Make adjustments where you can.

What you’ve saved so far gives you options you wouldn’t have otherwise. But it doesn’t determine your outcome.

The most important factors in determining your results are the trade-offs you choose and the actions you take from this point forward.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

It seems like a tempting offer; lower fees are certainly a benefit, as costs impact total return for investors. However, an early investor discount isn’t the only factor to consider (nor is it the most important) when deciding if a private equity opportunity is right for your portfolio.

Before locking up a portion of your money into a new opportunity, you should know how the investment works, where it fits into your broader plan, and whether the manager is reputable. Two concepts can help you cut through the noise: the J-Curve, which explains why early returns often look discouraging, and fee discounts, which fund managers use to offset that early sting. Understanding how they connect, and what neither one tells you, can help you make a more informed decision.

What Is the J-Curve?

Many private equity funds begin with an investment period where capital is called from the investor (commonly referred to as drawdown funds). During this period, the fund is looking for feasible investments and collecting capital from investors on an as-needed basis. Once they’ve identified and acquired businesses, the capital is deployed, acquisitions completed, and the businesses are infused with funds to help increase profitability.

When the initial acquisition takes place, no value has yet been gained on the investment, meaning returns are nonexistent—possibly even negative.

The acquired companies begin to improve operations and gain value. During this time, investors may be paying management fees or other operating expenses. With no meaningful exits yet (or no companies sold), gains likely haven’t been realized either. The combination shows a slow start for the fund on paper. If you were to plot the path on a chart, it would resemble the letter “J” (hence the name).

As portfolio companies grow, improve, and eventually get sold or recapitalized, returns may start trending upward at a steeper rate.

While an initial downturn in value might surprise new investors, the J-curve is a relatively normal part of how private equity performance typically moves.

So, Why Do Fund Managers Offer Fee Discounts?

Remember, it’s likely that once investors have joined the fund, they’ll see the value of their investment initially drop before (ideally) rising over time. Fund managers recognize that this initial downward dip can feel painful for investors. Many offer reduced management fees as a way to soften the blow and reward early participation.

Lower fees may modestly improve net returns over time and can help reduce some of the drag that often appears during a fund’s earlier stages.

However, a fee discount does not improve the quality of the underlying investments or determine whether a management team is reputable. It also won’t accelerate when portfolio companies are ready to be sold, nor will it reduce risk.

While it may be an effective way to reward those willing to commit capital early in the fundraising process, it should not be a primary reason to invest.

Deciding if Participation Makes Sense

When I evaluate a private equity opportunity with a client, there are a few specific questions I like to start with.

Who is the fund manager?

It’s important to review a fund manager’s track record, paying close attention to how they performed through different market environments. Remember, you’re trusting these managers with your capital. The quality of the team managing the fund is paramount to the success of the investment.

What is the strategy, and does it make sense for you?

Some funds focus on buying mature businesses. Others target growth companies, distressed opportunities, or niche sectors. The strategy should align with your goals, risk tolerance, and broader portfolio design.

Are you comfortable with the time horizon?

Private equity is typically a long-term commitment, often with a 5- to 10-year lifecycle. Your capital will likely be tied up for an extended period, with limited opportunities for liquidity along the way. Investors need to be comfortable planning around that reality.

How does it fit within everything else you own?

While everyone’s asset mix is unique, a private equity allocation will likely need to complement a larger investment strategy, not dominate it.

That is why I often tell clients, you are not investing because of a fee break. You are investing in a manager, a process, and a long-term strategy.

Selecting the Right Opportunity for Your Portfolio

If you’re already thinking about private equity, it’s certainly worth considering the benefit of lower fees for getting in early. Costs matter, and all else equal, paying less in management fees is better than paying more.

You’ve talked about retirement. You’ve even run some numbers. But somewhere beneath the spreadsheets, there’s a question neither of you has quite asked out loud: Are we actually picturing the same future? In blended families, the answer is often no, not because anyone is being careless, but because each partner brings different obligations and a different sense of what “enough” looks like. Blended family retirement planning starts well before the portfolio. It starts with the expectations each of you carries and where they came from.

Those expectations don’t announce themselves. They show up in assumptions about who owns what assets and what obligations to children or former spouses should take priority. Understanding what each person values, and where that comes from, is where meaningful retirement planning in a blended family begins.

Where Financial Expectations Come From (and Why They Differ in Blended Families)

Every financial decision you make today is connected to something you experienced before. Over time, those experiences become internal rules about what money should do for you. In behavioral finance, these are often referred to as “money scripts”—deeply ingrained beliefs that influence how we save and spend, often without us realizing it.

In a blended family, aligning your finances requires aligning the beliefs behind them. That’s why expectations around retirement timing, investment risk, and lifestyle can feel so different even when you’re working toward the same future. It’s a dynamic I examine throughout my book, Blended Family Finances: How to Talk About Money, Plan for the Future, and Build a Life You Love. Because understanding where those beliefs come from is the first step toward building a life that you actually want to live.

Even among higher-income couples, asset division, legal costs, and years of financial disruption can leave partners at very different starting points by the time they remarry. U.S. Census data show that adults who have married more than once are significantly less likely to have accumulated substantial retirement savings compared to those who married only once, and the gap persists even when current income is strong. One partner may carry that history internally, shaping how security and fairness feel to them in ways the other may not immediately see. Those differences matter because they shape real decisions.

This is the emotional math of blended family finances—invisible calculations about what feels protective, threatening, or fair. Feelings like guilt toward children, worry of repeating past mistakes, or a desire to protect what you’ve rebuilt can influence your choices. They’re signals worth paying attention to, even when they resist logical solutions, because they can shape everything from how much you save to how you structure your legacy.

Different Starting Points, Different Timelines: Retirement After Remarriage

Our financial history tells a story. In many blended families, perhaps one partner has spent years steadily rebuilding wealth, while the other is still rebuilding after the financial disruption of divorce.

That gap is well documented. According to a Business Insider analysis of U.S. Census Bureau data, the average married retiree has over $100,000 more saved in retirement accounts than a divorced retiree, a difference driven largely by asset division, legal costs, and lost compounding time. Even among couples who remarried, retirement income remained lower than that of those who had married only once.

For higher-income couples, the absolute numbers differ, but the dynamic remains the same. One partner may arrive at the relationship with a well-funded portfolio and a clear retirement timeline. The other might be earning well right now but still carrying the financial weight of starting over after divorce. Those two pictures don’t automatically align, and when they don’t, expectations around retirement timing, lifestyle, and risk tolerance can drift apart.

Those gaps shape how you plan together. How much should you save now? Whose timeline takes priority? How much risk feels comfortable when one partner still feels the urgency to catch up?

These are the kinds of decisions that require coordination across both past and present relationships. And getting them right starts with understanding what each partner is actually bringing to the table.

Clarity Starts with a Conversation

In blended families, many of the biggest financial challenges don’t come from a lack of planning. They stem from assumptions that were never spoken aloud. Over time, those assumptions harden into expectations, and when expectations diverge, even well-resourced couples can find themselves making decisions that pull in different directions.

Bringing those assumptions into the open is where the real planning begins.

One of the most valuable conversations a couple can have isn’t about the numbers—it’s about the experiences that shaped how each person defines security, responsibility, and what ‘enough’ actually means.

In retirement planning, this is where direction begins. It influences when retirement feels possible, how secure it needs to feel, and how you balance caring for the people who depend on you—past and present—without losing sight of the life you’re building together.

For example, one partner may feel a responsibility to preserve assets for children from a previous marriage, something shaped by promises made, or lessons learned the hard way. The other may be focused on building a shared future as a couple, assuming that resources will be used more fluidly between present lifestyle and long-term goals.

Neither perspective is wrong. But without a conversation, both can influence decisions:

how much risk feels appropriate

how aggressively to save

how retirement is ultimately structured

And over time, those differences show up in how aligned (or misaligned) the plan feels.

That’s why in our work with blended families, planning doesn’t start with projections alone.

It starts by uncovering: he values each person brings into the relationship, the money stories behind those values, and the vision they’re trying to build together

Because once those pieces are clear, the financial decisions that follow tend to make more sense—not just on paper, but in how they feel to both partners.

Aligning Your Retirement Vision as a Blended Family

You each stepped into this relationship with a story already in progress. Blended family financial planning is the work of bringing those two stories into a coherent shared chapter, one that accounts for where each of you has been while building toward something you can both see clearly.