Whether you’re a financial advisor who recently joined Wealthtender and wondering what to expect, a seasoned advisor looking to make the most of your Wealthtender experience, or simply trying to understand how Wealthtender’s digital marketing benefits differ from traditional lead generation, this guide covers all of it. Honestly, with data, and without the sales pitch… well, maybe just a subtle sales pitch.

Key Takeaways

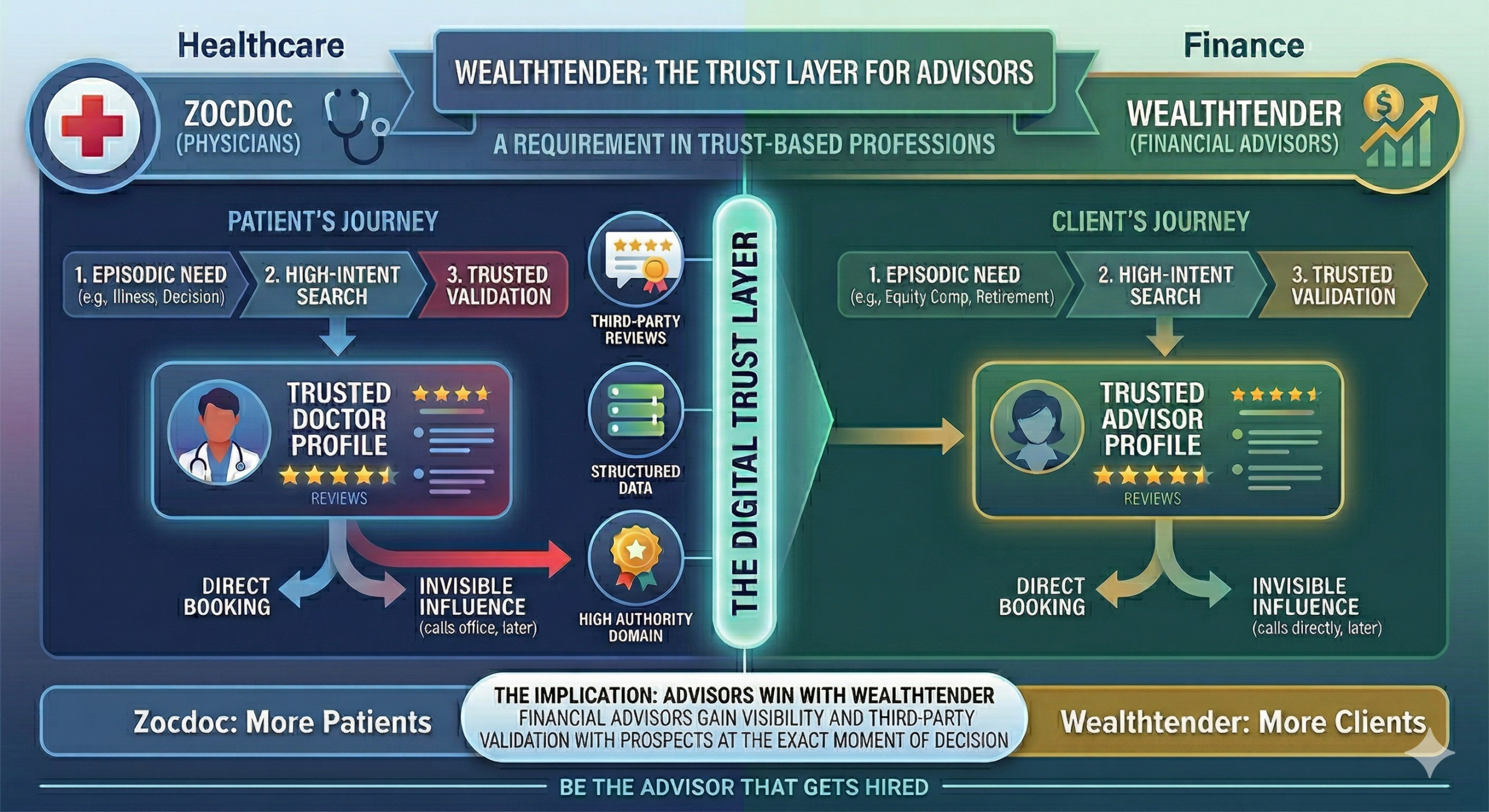

Wealthtender is to financial advisors what Zocdoc is to physicians: a trust-layer platform where high-intent prospects make their final decision.

Just as patients don’t choose a doctor based on a hospital’s brand alone, prospective clients don’t hire a financial advisor based on a firm’s marketing alone — they research individuals, read reviews, and validate trust before ever reaching out. Wealthtender positions you inside that decision moment: discoverable in Google and AI tools, credible through independently verified client reviews, and visible to prospects who are already motivated to act. That’s a fundamentally different point in the funnel than where traditional lead generation platforms operate.

Wealthtender delivers daily digital marketing ROI that increases visibility in Google and AI search, with a lead gen call option.

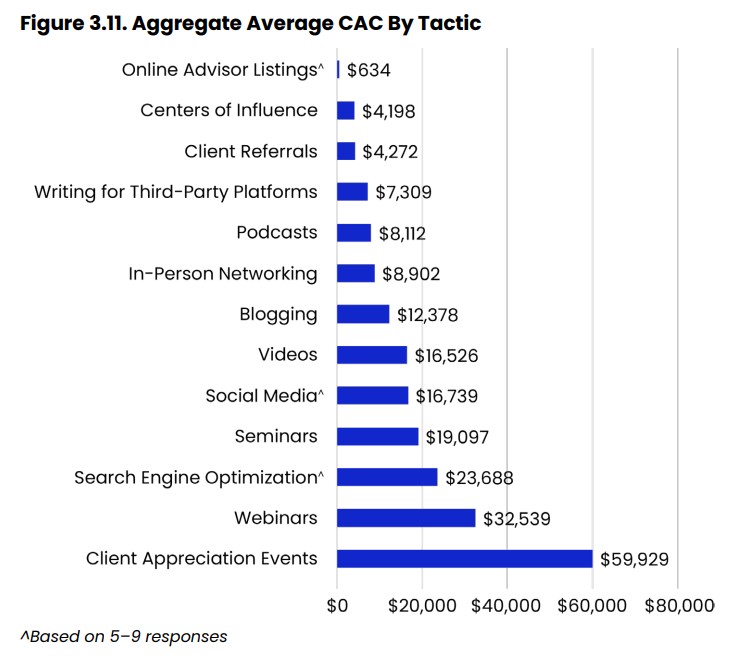

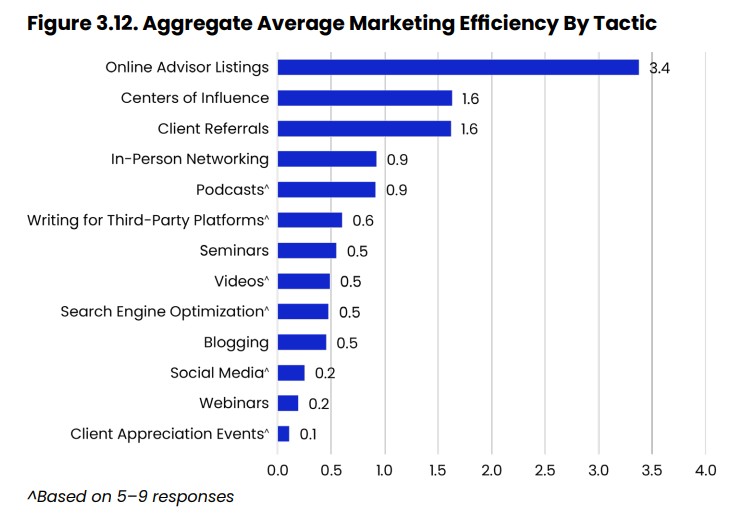

Think of your subscription as offering a call option: the monthly fee is the premium, and the intrinsic value is impactful — your profile indexed in Google and AI tools, your reviews differentiating you from the 90%+ of advisors who have none, your specializations surfacing in relevant searches every day. The option value (above and beyond intrinsic value) materializes when a qualified prospect discovers you on Wealthtender. Independent Kitces research found online advisor directory listings have the lowest client acquisition cost ($634) and highest marketing efficiency of any tactic studied across 14 categories.

Wealthtender influences more prospect decisions than advisors can directly measure.

Prospects may find you through AI-generated answers that cite Wealthtender content, see your reviews embedded on your website or compliantly promoted on social media, or discover you in a specialist directory or Q&A feature published on Wealthtender. And since 96% of referred prospects research advisors online before making contact, your Wealthtender profile is actively working on every referral you receive, not just the leads that originate directly through the platform.

Table of contents

- What Wealthtender Is (Before We Talk About What It Isn’t)

- What Wealthtender Isn’t

- What Wealthtender Delivers

- Think of Wealthtender as a Call Option on High-Quality Leads

- When the Option Is Exercised: Clicks That Become Clients

- Wealthtender Benefits You May Not Be Measuring

- The Wealthtender Ripple Effect: How Prospects Find You Without Ever Visiting Wealthtender

- See It for Yourself: AI Prompts to Try Right Now

- What to Do If You’re Not Showing Up — Yet

- What to Expect: A Realistic Timeline for Seeing Results

- Tips to Maximize Your Wealthtender Benefits

- A Note for Advisors on Legacy Wealthtender Plans

- A Powerful Complement to Other Marketing Strategies

- In Summary: Is Wealthtender Worth It for You?

- Frequently Asked Questions

- Even More FAQs

- Further Reading:

What Wealthtender Is (Before We Talk About What It Isn’t)

Let’s start with a comparison that may feel outside our industry, but arguably explains Wealthtender better than anything else:

Wealthtender is to financial advisors what Zocdoc is to physicians.

This comparison matters because both financial advisors and physicians operate in what are known as trust-based professions. Yes, credentials matter. Experience matters. Designations matter. But those are table stakes. When a consumer is deciding which doctor or financial advisor they will hire, the decision is ultimately driven by something else: trust.

Today, trust is built (and validated) online. That’s where platforms like Zocdoc (for physicians) and Wealthtender (for financial advisors) come in.

The Role of the “Trust Layer” & Bottom-of-Funnel Intent

Zocdoc is a popular tool used by people to find, compare and hire doctors. But patients don’t use Zocdoc every day, and doctors don’t sign up for Zocdoc with the expectation of receiving a steady stream of appointments. Usage is episodic. People use Zocdoc when they have a specific need (e.g., when something is wrong, when a decision needs to be made, when they’re ready to act). And when they show up, they’re not casually browsing. It’s bottom-of-funnel intent. They search for providers they can trust, compare profiles and specialties, read reviews carefully, and make a decision. Sometimes they book through Zocdoc. Sometimes they call the office directly. Sometimes they leave and come back later. And sometimes, they never visit Zocdoc at all.

How Zocdoc (and Wealthtender) Influence the Decision – Even If They’re Invisible

This is where many people misunderstand how platforms like Zocdoc – and Wealthtender – actually work. These platforms operate as part of the internet’s trust layer. Consumers today rely on third-party platforms for provider discovery, lean on reviews and profiles to evaluate credibility, and move through a multi-step journey before ever reaching out. And increasingly, that journey includes something new: AI-powered search.

When someone asks “Who is a good doctor in Los Angeles for an executive physical?” or “What do patients say about Dr. Smith?”, or, in the advisor world, “Who is a good financial advisor in Austin for Dell employees?” or “What do clients say about [advisor name]?”, AI tools like ChatGPT, Gemini, Perplexity, and others generate answers by pulling from trusted sources across the web. Platforms like Zocdoc and Wealthtender are among those sources, because each hosts independent third-party reviews, structure data in ways AI systems can interpret, and sit on high-authority domains that both search engines and AI tools trust. That means even if a consumer never visits Zocdoc or Wealthtender directly, their decision may still be shaped by information sourced from these platforms.

The Implication Some Advisors Miss

This leads to an important and often misunderstood aspect of the value these types of platforms can provide: Specifically, Wealthtender and Zocdoc can be highly valuable and influential even if consumer usage is episodic and attribution is imperfect. The value isn’t just in direct bookings. It’s in being visible in the right places, being validated by third-party credibility, and being trusted at the exact moment a decision is made. This is simply the nature of trust-layer marketplaces.

When a prospective client is ready to hire a financial advisor, they don’t start from scratch, and they don’t rely on a single source. They Google your name, ask AI tools like ChatGPT and Gemini for recommendations, look for reviews and third-party validation, and compare multiple advisors before reaching out. Even when receiving a glowing referral to an advisor from a friend or colleague, 83% of Americans who participated in a 2025 Wealthtender research study said the very next thing they will do is look online for reviews to learn if others feel the same way.

Wealthtender is designed to position you inside that decision process. So when the right prospect shows up, you’re discoverable, you’re credible, and you’re trusted. Sometimes that results in a direct introduction through Wealthtender. Other times, it results in a prospect calling you directly, booking time on your calendar, or reaching out after researching you elsewhere. In those cases, the influence is real, but the attribution isn’t always visible. And that’s okay. Because the goal isn’t constant activity. The goal is simple: be the advisor they choose when they’re ready to decide.

What Wealthtender Isn’t

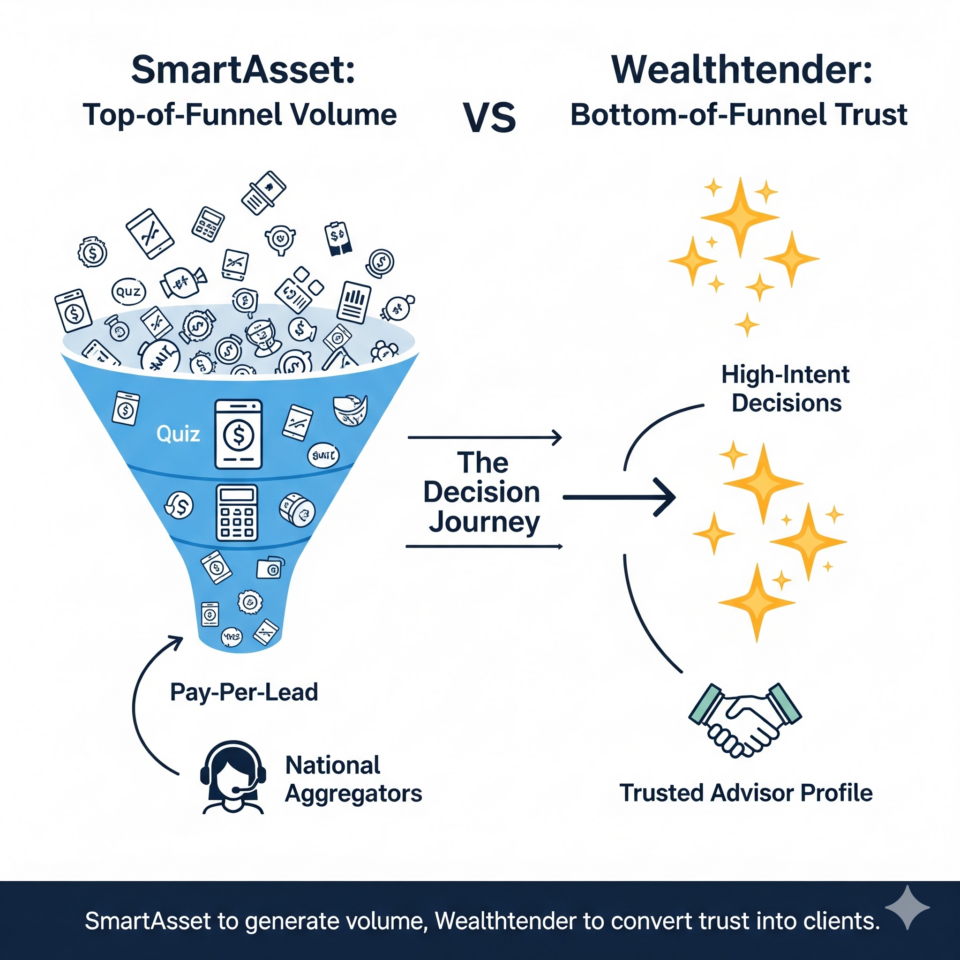

Now, with that framing in mind, let’s level-set clearly: Wealthtender is not a traditional lead generation platform, and we’re not trying to be.

Platforms like SmartAsset are built around a fundamentally different model. They generate a high volume of leads, typically through quizzes, calculators, and forms, and sell that information to advisors on a pay-per-lead basis, with advisors typically investing $2,000–$4,000+ per month to receive a steady stream of inbound contacts. Those leads can absolutely convert, but they come with real tradeoffs.

Prospects originating through SmartAsset are often early in their journey, they may be contacted by multiple advisors simultaneously, and success depends heavily on speed, persistence, and robust follow-up systems. Conversion rates are typically (very) low but scalable with volume. In other words: top-of-funnel intent. That model works well for firms with dedicated sales teams, structured follow-up processes, and the budget to operate at scale. There’s a reason the most successful firms utilizing SmartAsset are national aggregators like Creative Planning and Fisher Investments with call centers exclusively dedicated to working the leads.

Wealthtender operates at a completely different point in the journey. Instead of generating volume at the top of the funnel, Wealthtender positions you where decisions are made: when prospects are actively researching advisors, comparing credibility and fit, and when trust, not outreach, determines who they contact. Which is why lead flow is less frequent, but intent is significantly higher. And why many advisors might choose to use both: SmartAsset to generate volume, Wealthtender to convert trust into clients.

To learn more about how the two platforms compare and complement each other, check out our article on how advisors using SmartAsset can dramatically increase ROI by partnering with Wealthtender.

The slot machine problem

When it comes to traditional lead gen platforms like SmartAsset, here’s an analogy worth your consideration. Casinos have spent decades perfecting the science of the dopamine hit. Slot machines aren’t designed to make you rich, they’re designed to keep you playing. The ding of a near-miss, the flash of three matching symbols, the occasional modest payout just large enough to feel like validation: all of it is engineered to trigger a neurochemical response that makes it genuinely difficult to walk away. And the most sophisticated machines don’t just keep you at the same bet, they gradually encourage you to increase your wager for the prospect of a bigger reward. The cycle becomes self-reinforcing: the next pull might be the one, so you keep pulling.

Traditional lead generation platforms like SmartAsset understand this dynamic, even if they’d never describe it in those terms. The inbox notification of a new lead is a ding. The asset level in the prospect profile is the flashing symbol. The occasional conversion, the client who actually signs, is the payout that keeps you feeding the machine. And when a month goes by with nothing to show for it, the natural human response is not to question whether the machine is working, but to wonder if maybe you just need to increase your spend, improve your follow-up cadence, or try the next tier of the platform.

We’re not saying this analogy is perfectly accurate. Traditional lead gen can and does work for the right practices with the right commitment and resources, as we’ve acknowledged throughout this article. And unlike slot machines, it isn’t purely a game of chance. But the dopamine mechanism is real. It’s human nature to crave the feeling of something happening… a tangible, countable signal that your marketing investment is producing activity. Lead gen platforms like SmartAsset deliver that feeling reliably, which is part of why they’re so compelling even when the ROI math gets difficult to justify.

The honest question to ask yourself is whether that dopamine hit is actually informative signal or just psychological comfort. A lead notification feels like progress. But if that lead turns out to be someone who didn’t even intend to speak with a financial advisor, or who is simultaneously being called by two other advisors, or who stops returning calls after the first voicemail, was that ding actually telling you something useful? Or was it, like so many slot machine payouts, just enough of a reward to keep you in the game a little longer?

Inbound lead generation platforms like Wealthtender are simply not built to offer frequent dopamine hits. There’s no inbox ding when your profile shows up in a Google search. There’s no notification when an AI tool cites your reviews. There’s no alert when a prospect reads your testimonials and decides to reach out through your calendar link without mentioning Wealthtender. These things happen, and they influence real decisions, but they happen quietly. The tradeoff is that Wealthtender also poses no risk to your financial solvency with all plans below $100/month, is very unlikely to ever become your largest marketing expense, and doesn’t require you to talk yourself into another month of spend after a dry run. The downside is truly capped. The upside, when it materializes, tends to show up as exactly the kind of client you actually wanted.

What Wealthtender Delivers

Wealthtender is your long-term digital marketing partner for compliant online reviews and maximum visibility with prospects using AI search tools and Google to research and hire financial advisors, all for less than $100 per month (per advisor).

Each Wealthtender subscription covers a lot of ground. Your profile is built for organic visibility in AI tools like ChatGPT, Gemini, Claude, and Perplexity, in addition to traditional Google search. You get access to the industry’s first SEC/FINRA-compliant platform for collecting and publishing verified client reviews, hosted on a trusted, independent third-party website with industry-leading domain authority. Advisors on the Convert plan and above also receive weekly media quote opportunities in major publications that build authority and fuel AI citations, placement in local guides and specialist directories designed to surface you in the right searches, and the ability to be featured as a specialist in Large Employer Q&A discovery resources to get found and hired by employees and executives. And across all plans, when the right prospect finds you, they can reach out directly: no gatekeeping, no friction, no cost per lead.

Don’t just take our word for it. The 2024 Kitces Research Marketing Survey, arguably the most comprehensive independent study of financial advisor marketing effectiveness periodically conducted, found that online advisor directory listings have the lowest client acquisition cost of any marketing tactic studied, at just $634 per client, and the highest marketing efficiency of any tactic, with a score of 3.4. The Kitces researchers described online directory listings as one of the two “most underappreciated marketing tactics” in the industry.

“Using online directory listings (i.e., various ‘Find An Advisor’ platforms), along with cold calling or door knocking, are likely the 2 most underappreciated marketing tactics. With a solid rate of success and minimal cost to list in an advisor directory, listings have the highest marketing efficiency of any tactic.” — Kitces Report: How Financial Planners Actually Market Their Services (2024)

Think of Wealthtender as a Call Option on High-Quality Leads

Here’s the framework that best captures how Wealthtender works, and why the comparison to high-volume lead gen platforms misses the point entirely.

Joining Wealthtender is similar to purchasing a call option on the opportunity to attract your ideal clients. The monthly subscription (less than $100/month) is the premium you pay. And like any call option, it delivers two distinct types of value.

The first is intrinsic value: benefits you’re receiving every single day, regardless of whether you ever receive a direct inquiry. Your profile is continuously working to strengthen your visibility in Google, ChatGPT, Gemini, Perplexity, and other tools used by consumers to find and research advisors. Your independently-hosted reviews differentiate you from the 90%+ of advisors who have no online reviews at all. Your placement in local, specialist, and designation directories surfaces you in relevant searches. Backlinks from a high-domain-authority platform quietly strengthen your own website’s search ranking. And media quote opportunities build the kind of authority that compounds over time. None of this requires a prospect to contact you through Wealthtender for it to be valuable, though much of it can influence prospects to contact you without either of you ever knowing Wealthtender played a role.

The second is option value: realized when qualified prospects discover your profile and reach out to your directly through Wealthtender. And when that happens, the attributable ROI on your nominal monthly investment can be extraordinary – which is precisely what the Kitces research team calls out.

Just as call options provide asymmetric upside (e.g., limited downside, unlimited potential upside), Wealthtender works the same way. The downside is capped at your modest monthly subscription. The upside, when a single new client can generate thousands or tens of thousands in annual revenue, is uncapped.

This is why we say Wealthtender offers impactful digital marketing benefits as the core value proposition, with a call option on high-quality leads embedded at no additional cost. Not the other way around.

When the Option Is Exercised: Clicks That Become Clients

Prospect inquiries through Wealthtender are episodic: they don’t arrive with the predictable frequency (or cost) of a high-volume cold lead platform. But when they do arrive, they are categorically different from what most lead generation platforms deliver.

These prospects have already researched you. They’ve read your reviews, browsed your profile, confirmed you could be the right fit, and made a deliberate, self-directed decision to reach out to you specifically. They are not annoyed and standoffish, as we hear is often the case among consumers on the receiving end of three call center reps auto-dialing them after they click submit on a SmartAsset quiz. Rather, they are warm, self-qualified, and much further along in their decision-making process.

To illustrate what this looks like in practice, here’s a sample of real messages advisors have received through their Wealthtender profiles:

“We’re interested in learning more about your retirement planning services. Our portfolio is between $5–7M, we are 60 and 61, and live in…”

“My wife and I are looking for an advisor to help with equity and options. We are corporate professionals with options/RSUs in…”

“We are in Austin and retiring in a few weeks… selling our business. I would like to schedule a meeting with you and very likely proceed to…”

“I am currently with Edward Jones and wanted to look into a fiduciary or advisory financial planner…”

“I am an engineer at Google. I would appreciate the opportunity to schedule a brief introductory call…”

“I am a physician with investments in my hospital practice, retirement accounts, real estate, and…”

“We live in California and have a net worth around $5.5M. Please contact me if you are interested in working with us…”

“I came across your profile and would like to explore working with you for divorce-related financial planning…”

“I am looking for a flat fee financial advisor. I found your contact information on Wealthtender.”

We share these not because you should expect them regularly… you shouldn’t. But they do happen, and when they do, Wealthtender can instantly become the lowest cost-per-client acquisition channel of any platform you use. A single new client from one of these inquiries can deliver ROI that dwarfs years of monthly subscription fees. Again, we would point you back to the Kitces research.

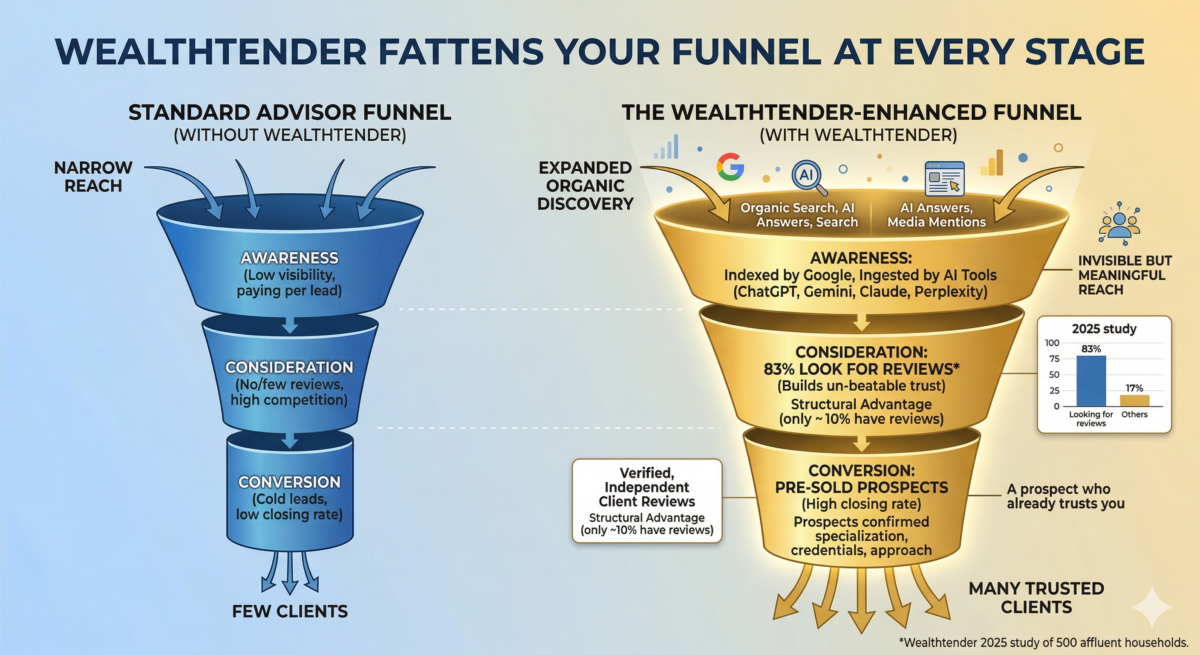

Wealthtender Fattens Your Funnel at Every Stage

This is perhaps the most important concept in this entire article: Wealthtender doesn’t just offer the potential to periodically add leads to the top of your funnel. It’s more important role is to make every stage of your funnel fatter (wider) and that compounds dramatically.

At the awareness stage, your Wealthtender profile is indexed by Google and ingested by AI tools like ChatGPT, Gemini, Claude, and Perplexity. More prospects discover you through organic search, AI-generated answers, directory listings, and media mentions without you paying-per-click or per lead. Your reach expands invisibly but meaningfully every day.

At the research and consideration stage, your client reviews create trust that most advisors simply cannot compete with. According to Wealthtender’s 2025 study of 500 affluent households planning to hire an advisor, 83% specifically look for online reviews before deciding whether to reach out. If you have verified, independently-hosted reviews on Wealthtender and your competitors don’t (and fewer than 10% of all advisors have any online reviews at all) you have a structural advantage at the exact moment the decision is being made.

At the conversion stage, consider what a prospect actually knows about you before they reach out through Wealthtender – They’ve read your reviews. They’ve confirmed your specializations match their situation. They’ve evaluated your credentials, your approach, and what real clients say about working with you. They chose you specifically, not because a call center rep from a national aggregator auto-dialed them, but because they did their homework and decided you were the right fit. Compare that to a cold lead who filled out a form and is now fielding calls from three advisors simultaneously. The conversion math isn’t complicated. A prospect who arrives already trusting you closes at a fundamentally different rate than one who has never heard your name.

Wealthtender Benefits You May Not Be Measuring

Here are three Wealthtender benefits with impactful ROI that many advisors dramatically underestimate:

1. You’re Showing Up in Google and AI Search, Whether You Know It or Not

When a consumer searches Google for “financial advisor specializing in equity compensation in Austin” or asks ChatGPT “Who is a good financial advisor for tech employees in Seattle?”, Wealthtender profiles with relevant specializations, client reviews, and well-structured content are increasingly surfacing in those results.

As covered by Barron’s in November 2025, platforms like Wealthtender are “designed to help make advisors discoverable by AI chatbots.” The article featured advisor Arielle Tucker of Connected Financial Planning, who received a new prospect inquiry that began simply: “I was searching for a U.S. expat advisor, and your name came up on ChatGPT.” Tucker’s specialized focus on U.S. expatriates, combined with her Wealthtender profile and client reviews, made her discoverable at the exact moment a highly qualified prospect was looking, without any paid advertising, cold outreach, or subscription to a lead generation platform.

The consumer behavior data behind that story is worth revisiting. According to Wealthtender’s 2025 consumer research study previously referenced, 50% of consumers begin their search for an advisor online through Google, and 25% (likely an even higher percentage today) are using AI tools like ChatGPT and Gemini to research advisors. Perhaps most importantly, 96% of people who receive a referral will still research the advisor online before making contact, and 83% specifically look for online reviews before deciding whether to reach out.

That last statistic carries significant implications. There is no such thing as a purely offline referral anymore. Even when a CPA refers a client to you, that prospect will Google you, ask ChatGPT about you, or look for your reviews before they ever pick up the phone or book a call on your calendar. Your Wealthtender presence is working for you at that exact moment, a moment that matters more than most, whether or not the prospect ever visits wealthtender.com directly.

2. Your Reviews Are Being Ingested by AI Tools

Client reviews published on Wealthtender don’t just live on your profile page. They are indexed by search engines and ingested by AI systems that use them to answer consumer queries. This means a prospect who has never visited Wealthtender.com may still be influenced by your Wealthtender presence, because when they ask ChatGPT or Perplexity what clients say about you, the answer is shaped by the content on your profile. Wealthtender’s structured data architecture, schema markup, and independent review infrastructure are specifically designed to maximize this effect. AI tools weight independent third-party review platforms more heavily than testimonials on advisor websites, which they recognize as self-curated rather than independently verified.

3. You’re Converting More Prospects Across Every Channel

Your Wealthtender profile builds trust that spills over into every other marketing channel you use. When a SmartAsset lead googles you or asks ChatGPT about you after receiving your call/email, your Wealthtender presence can be the difference between a callback and silence. When a seminar attendee goes home and researches you before your follow-up call, your reviews strengthen the likelihood they show up. When a referral researches you before reaching out, your independent third-party profile removes friction and your reviews accelerate their decision. Your profile is always working – 24/7, across all of these scenarios.

The Wealthtender Ripple Effect: How Prospects Find You Without Ever Visiting Wealthtender

One of the most counterintuitive benefits of Wealthtender is that we can influence a prospect’s decision to hire you even if they never visit wealthtender.com. There are three distinct ways this happens.

Through AI-generated answers. When prospects ask ChatGPT, Perplexity, Claude, or Gemini about financial advisors in their area or with a particular specialty, Wealthtender’s structured data and your client reviews surface your name and credentials in those answers more frequently and prominently, even when the prospect doesn’t search Wealthtender specifically. Advisors with complete profiles and verified reviews on the platform have a measurable advantage in AI-generated recommendations, because AI tools treat independently hosted third-party reviews as more authoritative than testimonials published on an advisor’s own website.

Through reviews embedded on your website. Every Wealthtender plan includes the ability to compliantly display your verified client reviews via a widget directly on your website. A prospect visiting your site sees verified third-party social proof without ever clicking to wealthtender.com.

Through specialist resources, like Wealthtender’s Large Employer Q&A content series. Advisors featured in Wealthtender’s Large Employer Q&A content series (available on the Convert plan and higher) can be discovered through highly targeted Google and AI searches by employees and executives of specific companies, with those employees never visiting Wealthtender’s homepage. One advisor in our community described her first experience with the feature this way: “I had a prospect reach out this week from one of the large companies that I did the Q&A on and he mentioned that he found me through a Google search using the keywords of ‘advisor, CFP and [the name of the $50B tech company where he works].’ Wow! These tools at Wealthtender are already working!!” She wasn’t found through Wealthtender’s homepage. She was found through Google, because Wealthtender’s content put her in exactly the right place at exactly the right moment.

The gist is this: Wealthtender’s reach is even greater than Wealthtender’s direct traffic. Our domain authority, structured data, and review infrastructure creates a ‘halo effect’ that extends your visibility across the internet everywhere prospects are looking to find and research advisors.

See It for Yourself: AI Prompts to Try Right Now

One of the most tangible ways to appreciate Wealthtender’s impact is to run a few searches yourself in the AI tools that prospects are already using. These prompts are designed to surface the type of information Wealthtender helps shape, specifically around your reviews and reputation, which are the areas most likely to return results influenced by your Wealthtender presence.

To see how your reviews appear to prospects researching you:

- “What do clients of [Your Name] say about their experience working with them?”

- “Are there reviews for financial advisor [Your Name]?”

- “What is [Your Name]’s reputation as a financial advisor?”

- “Can you summarize client feedback for [Your Name], CFP?”

To see how AI recommends you and/or competitors based on areas of specialization:

- “Who is a good financial advisor for [your niche] in [your city]?”

- “Can you recommend a financial advisor near [your city] who specializes in [your specialty]?”

- “I work at [large employer you serve]. What financial advisor would be a good fit for someone in my situation?”

To see how you appear when a prospect researches you by name:

- “Tell me about [Your Name], CFP. What are their areas of expertise?”

- “I was referred to [Your Name] as a financial advisor. What can you tell me about them?”

- “I’m looking for a financial advisor who specializes in [your specialty] near [your city]. Who comes up?”

If you have client reviews published on Wealthtender, you may be pleasantly surprised by what these queries return. If you haven’t yet collected reviews, these prompts will quickly illustrate how much more visible and credible you could be to prospects who are actively looking for someone exactly like you.

What to Do If You’re Not Showing Up — Yet

Don’t be discouraged if your name doesn’t immediately appear in every search. A few things are worth understanding before drawing conclusions, and a few concrete steps are worth taking.

First, understand how AI search actually works. Unlike a traditional Google search which often returns the same ranked list for a given query, AI tools like ChatGPT and Gemini are probabilistic, they don’t return identical answers every time. The same prompt entered twice in the same tool may surface different advisors on different occasions. So before drawing conclusions, run each prompt multiple times across multiple tools (ChatGPT, Gemini, Perplexity, Claude) and note both how often you appear and how consistently certain other advisors appear. You may show up more than you think, or you may identify a clear gap worth closing.

Second, flag the advisors who do appear more often for further analysis. When other advisors consistently appear in searches you want to own, look them up. Visit their website. Look at their Wealthtender profile. Count their reviews. Look for dedicated landing pages built for specific client segments. Check whether they’ve been quoted in media outlets or articles aligned to that topic, or whether they’re featured in YouTube videos or podcasts that could be elevating their AI visibility. Look at whether they’re publishing FAQs with schema markup on their site or profile. This isn’t about copying what they do, it’s about understanding what’s earning them visibility and honestly assessing where your own online presence has gaps you can fill.

Third, make sure the prompts you’re targeting actually match what your ideal clients are searching for. This is where advisors sometimes work hard on the wrong thing. If your ideal client is a Google employee navigating RSU vesting, the question worth asking is: are Google employees actually entering prompts like “financial advisor for Google employees with RSUs” into AI tools or Google itself? (Hint: we know at least some are.) A narrow niche can be extraordinarily powerful for establishing you as the recognized expert and elevating your visibility, but its smaller audience also means inbound interest will naturally be more episodic, even when your online presence is excellent. For niches like this, it’s worth pairing your inbound strategy (Wealthtender, reviews, website, Q&As) with outbound tactics that put you directly in front of your ideal audience: speaking to employee resource groups, writing content distributed in channels your ICP (Ideal Client Profile) frequents, or building relationships with HR teams and CPAs who work with those employees.

Fourth, remember that even referrals are influenced by your online presence. If you serve Amazon employees and a current client refers a colleague to you, that colleague is almost certainly going to Google your name, ask an AI tool about you, and look for reviews before scheduling a call. If your Wealthtender profile has reviews from other Amazon employees describing exactly the kind of help you provided them, a dedicated section on your website for Amazon employees, and FAQs built around their specific financial questions, that referral is very likely to convert. If none of those things exist, the referral may quietly choose someone else, or simply never reach out. This is one of the most underappreciated ways Wealthtender fattens your funnel: it doesn’t just generate new top-of-funnel interest, it helps convert the referrals and warm leads you’re already getting.

What to Expect: A Realistic Timeline for Seeing Results

Like any meaningful investment in organic digital marketing, Wealthtender rewards patience and consistency.

In the first 30–90 days, your profile is published, your specializations and credentials are indexed, and your digital presence begins strengthening. Consumers and AI tools start picking up your Wealthtender profile (typically within a day of signing up). You may not receive a direct inquiry in this early window, but your footprint is already expanding.

Over months 3–12, as you collect client reviews and your profile becomes richer, your visibility in Google and AI search grows. Each additional review is an independent piece of content indexed by search engines, a trust signal for AI tools, and a piece of social proof for any prospect researching you. The compounding effect of reviews accumulating over time is significant.

Over the long term, advisors with a strong presence on Wealthtender, particularly those who actively collect reviews, can expect the most meaningful impact on their business. And we’re grateful for the advisors who have consistently rated Wealthtender near the top of its category in the annual T3 Advisor Software Survey, reflecting strong advisor advocacy year after year. That recognition reflects long-term value, not overnight results.

The most successful Wealthtender advisors tend to share three habits: they keep their profile complete and up to date, they systematically invite clients to write reviews, and they pair their Wealthtender digital marketing benefits with their established sales and marketing tactics to attract and convert the right prospects at the right time.

Tips to Maximize Your Wealthtender Benefits

Knowing what Wealthtender does is one thing. Getting the most out of it is another. These are the habits and features that separate advisors who see compounding returns from those who wonder why the platform isn’t doing more for them.

Complete your profile thoroughly. AI tools strongly favor complete, detailed profiles. Fill in every section: specializations, credentials, geographic information, fee structures, a bio written in the language your ideal client uses, and a video if possible. A half-completed profile is a missed opportunity.

Could your Wealthtender profile be

working even harder for you?

Paste your profile URL below and get personalized, AI-powered tips in less than 2 minutes.

Of course, when it comes to artificial intelligence, it’s no replacement for OG AI: “Actual Intelligence”; We encourage you to speak with your marketing counterpart and your compliance officer before making updates to your profile.

📌 Important reminder

This analysis is AI-generated based on a review of your public profile page. While the guidance should prove helpful, please consider it directional and remember there’s a difference between “artificial intelligence” and “actual intelligence” (OG “AI”). For the best guidance and recommendations to improve your profile, please speak with your marketing counterpart or a qualified marketing consultant with experience serving financial advisors. And of course, always speak with your compliance officer for their guidance and approval before making any changes. Questions? yourfriends@wealthtender.com

Collect reviews consistently. This is the single highest-leverage action you can take. Set up a simple, repeatable process: 60–90 days after onboarding a new client, send them an invitation to write a Wealthtender review. Aim for at least 10 reviews in your first year. Even a handful of thoughtful, detailed testimonials can dramatically strengthen your visibility in both Google and AI search tools — and give you a structural competitive advantage over the 90%+ of advisors who have no online reviews at all.

Embed reviews on your website. Every plan includes the ability to display Wealthtender reviews on your website via a compliant widget. Use it. Prospects who land on your site should see social proof immediately, in an SEC-compliant format you can actively promote.

Participate in media opportunities (Convert and Command Plans). Being quoted in popular publications builds credibility, strengthens SEO, and sends trust signals to AI tools. These opportunities come to your inbox weekly — take advantage of them.

Use the FAQ feature strategically (Convert and Command Plans). AI-optimized FAQs with schema markup on your profile are among the most powerful tools for appearing in AI-generated answers. Write FAQs the way your ideal clients actually ask questions — “Does [Your Name] offer retirement planning services for Google employees in the Bay Area?” — rather than generic questions about what financial planning is. Wealthtender automatically applies schema markup so AI tools can extract and cite your answers directly.

Participate in Large Employer Q&As (Convert and Command Plans). If you serve employees of major companies, these features target highly specific, high-intent searches that can produce exceptional results — as the advisor story earlier in this article illustrates. The cost is built into your subscription. The payoff can be substantial.

A Note for Advisors on Legacy Wealthtender Plans

If you joined Wealthtender on one of our older subscription plans (e.g., Growth Essentials, Growth Premier, or Marketing Pro), here’s the most important thing to know: nothing changes unless you want it to. Your pricing and features are currently grandfathered, so you keep what you have at your current price.

In July 2026, we introduced three new plans and features reflecting how much the platform has grown and introducing more ways to show up in AI search and accelerate the trust-building process with prospects: Convert, Compound, and Command. The names describe a progression: convert prospects into clients, compound your reputation over time, then command your market or niche.

Convert ($59/month, or $54/month with annual billing) is the new foundation, and it includes benefits like weekly media quote opportunities and placement in up to four specialist directories, alongside your SEO and AI-optimized profile and Certified Advisor Reviews.

Compound ($79/month, or $73/month with annual billing) adds AI-Optimized FAQs with automatic schema markup, Testimonial Marketing Studio, and your first Large Employer Q&A participation.

Command ($99/month, or $92/month with annual billing) adds a professionally designed, AI-optimized Firm Focus Page built on Wealthtender’s domain authority, upgrades your Large Employer Q&A participation to Tier 1 employers, and includes 10% savings on all add-ons.

If you’d like access to any of these newer benefits, you can migrate at any time. As a thank-you for your early support, legacy subscribers receive a 15% loyalty discount off the new plan rate when choosing to migrate by December 31, 2026. And if your current plan still fits your practice, staying put is a perfectly good decision, too.

You can compare all plan features in detail on our pricing page, or email yourfriends@wealthtender.com and we’ll help you decide whether migrating makes sense for you. No pressure either way. The right plan is the one that matches where you are in your practice growth today.

A Powerful Complement to Other Marketing Strategies

Wealthtender works best as part of a broader marketing strategy, not as a replacement for one.

If you’re using SmartAsset or another lead generation platform, Wealthtender can make that investment significantly more productive. When those leads Google you or ask ChatGPT about you – and research shows 96% of prospects who receive a referral will research you online before reaching out – a credible, review-rich Wealthtender profile accelerates trust and increases conversion. A prospect who arrives already knowing you’re credible closes at a fundamentally different rate than one who finds nothing when they search your name.

If you’re building your practice through referrals, networking, and word of mouth, Wealthtender validates those relationships digitally at the exact moment it matters, when a prospect is doing their research before reaching out.

If you’re investing in content marketing, PR, or social media, Wealthtender’s directory placement and independent review platform reinforce your messaging with third-party credibility that your own content can’t provide alone.

And if AI-driven search is something you’re paying attention to (as it should be, given how rapidly consumer behavior is shifting) Wealthtender is currently the most purpose-built platform in our industry for ensuring you appear favorably in answers generated by ChatGPT, Perplexity, Claude, Gemini, and Google AI Overviews.

In Summary: Is Wealthtender Worth It for You?

If you’re wondering whether Wealthtender is working for you, here’s the honest answer: it’s almost certainly doing more than you can directly measure.

Your profile is being indexed. Your reviews are being read by prospects and AI tools alike. Your specializations are helping you get noticed by consumers looking for someone with your exact expertise. And when the right prospect is ready to reach out, you’re positioned to be found first and trusted immediately.

Direct inquiries that reference Wealthtender by name are a bonus, and a meaningful one when they occur, given the quality of prospects they represent and the extraordinary ROI a single new client can generate. But they represent only a fraction of the value Wealthtender delivers every day.

We’d love to offer the kind of recurring dopamine hits that pay-per-lead platforms deliver, but those hits come at a cost of $200 or more each, adding up to $25,000 to $50,000 a year. So while the full value of your Wealthtender subscription may not always be directly measurable, the money you’re not spending on frequent lead notifications absolutely is. That’s a dopamine hit worth savoring every time you look at your marketing budget.

The advisors who see the greatest returns are those who treat Wealthtender as the long-term investment it is and who give it the time and consistency to compound. If you’d like help assessing how your profile is set up or want to talk through your digital marketing strategy, we’re always happy to talk shop. Reach out to us anytime at yourfriends@wealthtender.com.

Frequently Asked Questions

Even More FAQs

Q: I hear what you’re saying, but it feels like you’re promoting Wealthtender as an elixir without showing real proof. What am I missing?

That’s a fair challenge, and we’d rather engage with it honestly than brush past it. Here’s what the evidence actually shows.

What independent research says. The 2024 Kitces Research Marketing Survey, a rigorous, independent study of financial advisor marketing tactics, found that online advisor directory listings have the lowest client acquisition cost ($634) and highest marketing efficiency (3.4) of any tactic studied across 14 categories (See report screenshots excerpted below). The Kitces team specifically called out directory listings as one of the two “most underappreciated marketing tactics” in the industry. Wealthtender is the most comprehensive advisor directory built specifically for the era of AI search and SEC-compliant reviews. That independent finding isn’t about Wealthtender specifically, it’s about the category. We happen to be the most purpose-built platform in that category.

The same study also noted that review sites (which Wealthtender combines with directory listings in a single platform) are seeing adoption grow rapidly since the SEC’s 2022 Marketing Rule update clarified advisors’ ability to use them and projected that their prominence will only increase. Wealthtender was specifically named as the most utilized industry-specific online review platform being monitored and used for marketing by advisors in the study.

What industry reports say. Wealthtender has consistently earned top ratings in the T3 Advisor Software Survey (Digital Marketing Tools – Lead Capture category). These ratings reflect feedback from advisors using the platform. A Barron’s article published in November 2025 covered how Wealthtender is helping financial advisors get found in AI search tools, featuring named advisors who received qualified inbound inquiries directly attributable to their Wealthtender presence. We have case studies like United Financial Planning Group, where reviews on Wealthtender directly influenced a prospect to choose an independent firm over a national wirehouse, a prospect who explicitly cited what they read on the platform as the reason they made contact. And we have lots of documented prospect messages from high-quality leads, physicians, Google engineers, retirees with multi-million-dollar portfolios, who found advisors specifically through their Wealthtender profiles.

The compliance credibility runs deep, too. After reviewing Wealthtender’s platform and review process, the Chief Compliance Officer of a Barron’s Top 100 RIA firm said simply: “I reviewed Wealthtender and their client review process, and I am good with it — I actually really like their process.” For advisors whose compliance teams need to sign off before joining, that kind of peer-level endorsement from a top-ranked firm’s CCO speaks volumes.

What we can’t offer is a SmartAsset-style guarantee of X leads per month. That’s not what Wealthtender is. If you need that kind of guaranteed volume, we’d genuinely tell you to look at a pay-per-lead platform (and then also join Wealthtender to make those leads convert better). But if the question is whether Wealthtender delivers measurable value beyond what most advisors expect when they sign up, the answer is yes, and both the independent research and 800+ advisors and firms who have chosen to partner with us bear that out. Read what financial professionals say about Wealthtender here.

How does the cost of Wealthtender compare to similar platforms for financial advisors?

Within the financial advisor industry, there are two meaningful comparison categories.

Category 1: Review collection tools designed to publish testimonials on your own website. Platforms like FMG Testimonials (FMG’s acquisition of Testimonial IQ, rebranded in early 2026) and Amplify Reviews are capable, well-built tools that do what they set out to do: collect compliant client testimonials and display them on your own website. We have a lot of respect for their founders and teams who share our passion for providing compliance-first solutions to collect and publish testimonials. If you’re using one of these tools, you’re already ahead of roughly 90% of advisors who use no testimonials in their marketing at all.

But there’s an important gap between collecting a testimonial and maximizing its impact, and that gap is exactly where Wealthtender comes in.

When a testimonial lives only on your website, it reaches people who have already found their way to you. Wealthtender functions as the amplification layer: your reviews are published on an independent, high-authority third-party platform that is indexed by Google, cited by AI tools, and visited by 500,000+ consumers annually. That means your testimonials are working to reach people who don’t yet know you exist.

There’s also a credibility dimension. AI tools explicitly weight reviews on independent third-party platforms more heavily than testimonials published on advisor websites, which they recognize as self-curated. Getting your reviews onto Wealthtender in addition to your own site doesn’t replace what FMG Testimonials or Amplify does, it dramatically extends its reach and impact.

Importantly, these review-only tools also carry no find-an-advisor consumer destination, no specialist or local directories, no media quote opportunities, and no Large Employer Q&A features. And notably, Wealthtender’s pricing is lower than some of these review-only tools despite offering substantially more. Advisors who use FMG Testimonials or a platform like Amplify Reviews can choose to pair it with Wealthtender specifically for the third-party amplification and consumer discovery that their existing tool can’t provide. Read more about how FMG Testimonials and Wealthtender work together.

Category 2: Third-party review platforms for financial advisors. Indyfin (now operating under WiserAdvisor following their 2025 acquisition) offers a more direct comparison in that it’s a third-party platform where advisors can collect and publish compliant reviews independent of their own website, similar to what Wealthtender does. That independent positioning is genuinely valuable, and we acknowledge it.

But the platforms are not equivalent, and the shortcomings of Indyfin relative to Wealthtender are significant. The key differences summarized below help explain why multiple advisors and wealth management firms have left Indyfin and migrated their online reviews to Wealthtender.

On pricing: Indyfin charges $99/month for a single advisor. Wealthtender’s Convert plan starts at $59/month, meaning Wealthtender’s entry-level plan costs significantly less than Indyfin. Advisors who choose Indyfin over Wealthtender are paying more for less.

On reach and discoverability: According to data from Ahrefs and Moz, Wealthtender receives approximately 63,700 monthly visitors compared to Indyfin’s 967, roughly 66 times more consumer traffic. Wealthtender’s domain authority is 42 versus Indyfin’s 18, meaning Wealthtender’s profile pages carry significantly more weight with Google and AI tools when surfacing your name in search results. (For the most current figures, see the data disclosures on our Indyfin comparison page.)

On features Indyfin doesn’t offer: The gap extends well beyond traffic. Wealthtender provides media quote opportunities, specialist and niche directories, Large Employer Q&A features, AI-optimized FAQs with schema markup, Voice of the Client Awards, the ability to convert Google Reviews to SEC-compliant testimonials, and Testimonial Marketing Studio for creating social media content from your reviews. None of these exist in Indyfin’s platform.

Read the full comparison of Indyfin vs. Wealthtender here.

What does independent industry data say? The T3 Technology Survey, one of the most widely cited independent assessments of advisor technology, has listed Wealthtender in its Digital Marketing Tools – Lead Capture category and consistently rated us among the highest in the category. In the 2025–2026 survey, Wealthtender earned an average user rating of 7.68 (2026) and 7.96 (2025) — among the highest scores in the category — and remains the only independent third-party directory and review platform in the category that combines a compliant review platform, a high-traffic consumer-facing find-an-advisor destination, and a full digital marketing suite in a single subscription. We’re proud of those ratings, which reflect feedback from advisors who use the platform, not from us.

The bottom line: for advisors who simply want a widget to display reviews on their own website, there are capable tools that do exactly that. For advisors who want their reviews, profile, and expertise to be discoverable by consumers and AI tools across the internet, and who want the credibility that comes from an independent third-party platform with real domain authority, Wealthtender stands in a category of its own within the financial services industry.

If my state regulator or home office doesn’t yet allow me to use online reviews, is Wealthtender still worth it?

We want to be completely honest with you here, because this is a question that deserves a straight answer: the inability to collect and publish client reviews does take away from one of the most powerful features Wealthtender offers. Reviews turbocharge the engine for AI visibility, SEO strength, and conversion-rate improvements we discuss throughout this article. We know that, and we don’t want to pretend otherwise.

We also know there are advisors who are waiting specifically for the green light on reviews before they sign up for Wealthtender, and we completely understand that position. If the reviews feature is the primary reason you’re interested in joining, it’s fair to wait until you have the ability to use it fully.

If you’re in this situation, we want you to know that we hear your frustration and we’re actively working on your behalf. Wealthtender has published research and engaged media coverage specifically to shine a light on the regulatory double standard that currently prohibits state-registered advisors in roughly 20 states from collecting and publishing client reviews, even as their SEC-registered counterparts and large national firms are free to do so. We’ve been engaged in ongoing conversations with state regulators, and we’ve found that our advocacy work and media efforts have been helpful in moving the needle. Several states have updated their rules in recent years, and we expect that progress to continue. We’re also in active, constructive conversations with a growing number of broker/dealer home offices, conversations that have increasingly proven fruitful, in part because we’ve built Wealthtender to be the “Boy Scout” of the industry when it comes to regulatory compliance. CCOs at firms including Barron’s Top 100 RIA practices have reviewed our platform and praised our approach. We’ll keep chipping away.

That said, a meaningful number of advisors are currently using Wealthtender even without reviews activated, and getting real value from it. Here’s why:

Your SEO/AEO-optimized profile begins working the moment it’s published, strengthening your visibility in Google searches and AI tools based on your specializations, credentials, location, and the overall authority of Wealthtender’s domain. Your placement in local, specialist, and designation directories puts you in front of consumers who are actively searching for someone like you. Media quote opportunities (Convert plan and higher) give you a consistent avenue to build credibility and gain backlinks from publications your prospects read. Large Employer Q&A features can make you discoverable through highly targeted searches by employees of specific companies in your area. And when your home office or state regulator does eventually grant approval for reviews, as we expect they will, your Wealthtender profile is already established, your profile traffic is already building, and you can activate the reviews feature immediately without starting from scratch.

For advisors in this position, we’d suggest thinking of Wealthtender the way you might think of planting a tree: the best time to have started was a year ago, and the second best time is today. The reviews feature, when available to you, will layer on top of a foundation that’s already working.

What if I want to cancel my Wealthtender subscription? Will I lose my reviews?

You can cancel at any time as there’s no long-term commitment on monthly plans. If you do choose to cancel, your Wealthtender profile is removed from public visibility and you’re no longer able to publicly display reviews or actively collect new reviews through the Wealthtender platform. However, the reviews that were published on Wealthtender are available for you to export and our team is always happy to assist you with the download. And if you decide to reactivate your Wealthtender subscription in the future, we’re happy to reinstate your reviews previously collected on Wealthtender to display on your profile.

Further Reading:

- How Financial Advisors Appear in ChatGPT & AI Search Tools

- How Advisors Using SmartAsset Can Drive Greater ROI with Wealthtender

- Answer Engine Optimization (AEO) for Financial Advisors

- How Financial Advisors Can Attract Large Company Employees

- Wealthtender Reviews vs. Google Reviews

- How FMG Testimonials and Wealthtender Work Together

- Indyfin (WiserAdvisor) vs. Wealthtender

- What Advisors Say About Wealthtender

- How Americans Will Choose Financial Advisors in 2026 and Beyond

- Compare Wealthtender Plan Options

- The Kitces Report, Volume 1, 2024: How Financial Planners Actually Market Their Services (Independent research — online advisor directory listings ranked #1 in marketing efficiency and lowest CAC of any tactic studied)

- 2026 T3/Inside Information Software Survey (Wealthtender featured in the Digital Marketing Tools – Lead Capture category, p. 71)

Want to see how individual advisors and leading wealth management firms are successfully using Wealthtender to grow their business? Visit Wealthtender.com/grow or schedule a demo to learn how you can start converting more prospects into clients with the industry’s first digital marketing platform for AI-optimization and compliant online reviews.

About the Author

Brian Thorp

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Book a Demo

Select a day in the calendar below to schedule a meeting

with Brian Thorp, Wealthtender founder and CEO.

Find financial advisors in Spartanburg, South Carolina ready to help with your financial planning needs so you can enjoy life more with less money stress.

Whether you have lived in Spartanburg for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Spartanburg featured on Wealthtender you may want to add to your shortlist.

Featured Spartanburg Financial Advisors

As you prepare to interview financial advisors in Spartanburg who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Spartanburg

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Spartanburg.

📍Double-click or pinch pins to view more.

The Benefits of Hiring a Financial Advisor in Spartanburg

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Spartanburg, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Spartanburg? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring a Spartanburg Financial Advisor

Before hiring a financial advisor in Spartanburg, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

- Budgeting and money management

- Debt management

- Insurance planning

- Retirement planning

- Other investment planning

- Inheritance planning

- Estate planning

- Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

- What services do you provide?

- What are all the ways you get paid? (fee transparency)

- What is your investment strategy?

- How do you measure investment performance?

- How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

How Much Does a Financial Advisor Cost?

➡️ How Much Does a Financial Advisor Cost? Read the Article

About the Author

About the Author

Brian Thorp

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

I recently attended the Basis Northwest Conference in Seattle, which centered around tax-aware investments and how the landscape is changing. About 30 years ago, ETFs were the hot new thing. But as wealth continues growing and incomes rise, they’re not enough to meet the demands of high-net-worth investors. More often, clients are coming to me focused on achieving greater after-tax return through more sophisticated tax strategies, and a few potential strategies stand out.

What Tax Strategies Are Gaining Traction?

Traditionally, certain tax-aware investing tools were limited to institutional investors and the ultra-wealthy. However, many of those have recently become accessible to individual investors. While the following approaches won’t work for everyone, these strategies are worth considering:

Tax-aware long/short: Tax-aware long/short strategies aim to generate losses used to offset realized gains while maintaining market exposure.

351 exchanges: Investors contribute appreciated securities into a diversified investment vehicle without immediately triggering capital gains taxes. For those with a large position in a single stock, a 351 exchange offers diversification while deferring the tax consequences of a sale.

Tax-aware hedge funds: Certain hedge fund structures try to generate losses or deductions that can offset other sources of taxable income (including W-2 income or Roth conversions).

Oil and gas exploration: Direct investments in oil and gas exploration can provide substantial tax deductions, often allowing investors to deduct a significant portion of their investment in the early years.

Real estate depreciation: Real estate investors benefit from depreciation deductions, which reduce taxable income even as the underlying property potentially increases in value.

Box-spread loans: A relatively new strategy, box-spread loans use your existing investments as collateral to offer reduced interest rates on loans. Box-spread loans tend to benefit those who need liquidity but prefer not to sell appreciated investments outright.

Incorporating Tax-Aware Strategies Into Your Portfolio

Many of the strategies shared above are beyond what’s available through a standard custodial platform or typical advisor relationship. Because they lack accessibility, the number of investors able to implement these more sophisticated tax-aware strategies is limited.

But for those who are able and willing to try, the next hurdle is understanding how these strategies fit together and when they make sense.

Let’s take, for example, an investor with a substantial amount of concentrated single company stock they’ve accumulated over many years. Selling this highly appreciated stock outright to reduce concentration would create a significant tax bill. Instead, they may pursue a tax-aware long/short strategy, which would generate potential losses that help offset future gains. At the same time, they might explore a 351 exchange that would help diversify some of those concentrated holdings without triggering capital gains tax.

Or, consider a business owner preparing to sell their business. Negotiating the highest sale price is important to them, but so is preserving as much after-tax proceeds as they’re able. Again, tax-aware long/short strategies could help offset a portion of that eventual gain and improve the overall after-tax outcome.

Investors with large 401(k) balances or cash balance plans may want to pursue Roth conversions during favorable tax years. Tax-aware hedge fund strategies aim to create deductions or losses that make those conversions more tax-efficient.

An investor with a need for liquidity — for example, if they’re purchasing a new home — may not want to liquidate appreciated investments to access cash. Similarly, an investor committing capital to a private equity opportunity may prefer to leave an existing portfolio intact. In those situations, a box-spread loan can bridge the gap, providing access to capital while allowing the underlying investments to remain invested.

Keep More of What You Earn

What you keep matters as much as what you earn. The investors who understand that plan for taxes year-round, not just in April. It takes strategic planning and careful consideration to find the right mix of tax-aware tools for your specific needs.

This article was originally published here and is republished on Wealthtender with permission.

About the Author

Sean Gerlin, CFP®, CPWA®, ChFC®, CLU® | Envision Wealth Planners

IPOs and the excitement surrounding them tend to bring out investors’ emotional biases. Fear of missing out on big potential gains, excitement over the “hot stock” everyone’s talking about, or the optimistic belief that a company’s recent growth means more is coming—these can all influence an investor’s decision-making process.

When a well-known company finally goes public, investors are presented with an opportunity to participate in a story they’ve likely been following for years. Recently, SpaceX and other big names have generated significant attention, with many investors eager to gain exposure before the next potential chapter of growth unfolds.

If you do decide to buy, it’s worth understanding the mechanics behind an IPO and the volatility that tends to come with it. There are ways to both participate in an exciting event like an IPO and consider your long-term financial well-being at the same time. The key is to be strategic, think with a clear head, and keep the potential tax consequences of large gains in mind.

The Nature of IPO Pricing

When a company goes public, it establishes an initial offer price for its shares. That’s all well and good. But once public trading begins, the market ultimately determines what investors are willing to pay. Shares often begin trading at a different price from the original IPO offering price.

A highly anticipated IPO might surge immediately. Other times, shares open flat or even decline. While there’s plenty of excitement surrounding a new public offering, no one knows exactly how the market will respond once trading begins.

Remember, recently IPO’d companies are still relatively early-stage businesses. They’ve demonstrated impressive growth, but they haven’t yet established a consistent path to profitability.

Take Uber as an example. Despite being one of the most recognizable companies to go public in recent years, the stock initially struggled to meet expectations. It took roughly five years after its IPO to achieve profitability. Since going public, it’s actually lagged behind the S&P 500.

Even exciting companies can experience significant volatility and long periods of uncertainty before their business results fully catch up to investor expectations (though there’s no guarantee they ever will).

Preparing for IPO Volatility with Strategic Asset Location

Considering where an investment should live within your portfolio is a commonly overlooked strategy called “asset location.” Different types of accounts carry different tax treatments and consequences. Investors can pair tax-efficient or inefficient assets with the accounts that will best complement their attributes.

For example, a Roth IRA allows qualified growth and withdrawals to occur tax-free. Tax-deferred accounts, such as traditional IRAs, generally allow investments to grow without immediate taxation, with taxes deferred until funds are withdrawn.

Investments with the potential for substantial appreciation are often well-suited for these types of accounts. If an IPO investment performs well, future gains may be shielded from current taxation or deferred for years, depending on the account structure.

When capital gains are realized in a taxable account, they can create an immediate, sizable tax bill. Frequent trades may also be considered taxable events and reduce after-tax return.

Tax-sheltered accounts mitigate tax drag and allow more of the investment’s potential growth to remain invested over time.

That said, an asset location strategy doesn’t make the investment itself safer for your portfolio. Risk and volatility still exist regardless of what account the investment lives in. A company can still disappoint investors, miss expectations, or experience sharp price swings. Rather, considering different account types and their tax characteristics gives you the ability to better control the eventual tax outcome.

When Do Taxable Accounts Make Sense?

Taxable accounts may still be suitable in certain situations, especially if you have access to a tax-reduction wrapper plan such as a long/short strategy.

A long/short strategy can be used to offset gains by intentionally realizing losses elsewhere in the portfolio. Tax-management strategies like this give investors greater flexibility when deciding where to hold a high-growth IPO allocation.

Want to Take Part in the Next IPO?

Investment performance impacts returns, naturally. So does the tax treatment, which can differ depending on where you choose to house investments with significant growth potential.

If you’re tempted to take part in a recent or soon-to-come IPO, consider both the investment opportunity and the tax implications. Strategic decisions, including asset location, can help position your portfolio to keep more of what you earn, especially if the investment succeeds.

This article was originally published here and is republished on Wealthtender with permission.

About the Author

Sean Gerlin, CFP®, CPWA®, ChFC®, CLU® | Envision Wealth Planners

Discover financial advisors trusted by residents of Aspen, Colorado in the only local directory featuring 5-Star Certified Advisor Review™ recipients and Wealthtender Voice of the Client Award™ winners—recognition earned for exceptional client feedback. Compare fiduciary, fee-only advisors, CFP® professionals, and specialists to find the right fit for your unique financial needs.

Whether you have lived in Aspen for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Aspen featured on Wealthtender you may want to add to your shortlist.

Featured Aspen Financial Advisors

As you prepare to interview financial advisors in Aspen who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Aspen

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Aspen.

📍Double-click or pinch pins to view more.

The Benefits of Hiring a Financial Advisor in Aspen

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Aspen, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.