Do you work at Microsoft? Get the resources you need and expert insights from financial professionals who specialize in helping Microsoft employees make the most of their compensation package and benefits.

Whether you’re a new Microsoft employee or you’ve moved up the ranks into a management or executive leadership role over a multi-year career, it’s important to make smart money moves with your income and employee benefits. For example:

✅ Do you know the right moves to make to get the greatest value from the Microsoft benefits available to you?

✅If you’re thinking about leaving Microsoft for another job or planning to retire from the company in a few years, are you taking the right steps today to ensure you will receive all of the compensation and benefits that you’ve earned?

Get the Most Value from Your Microsoft Benefits and Compensation Package

Throughout the year, Microsoft provides its employees and executives with updates about their benefits ranging from health insurance and health savings plans to retirement plans like a 401(k), deferred compensation plans, and stock options. While the company offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Microsoft who specialize in helping Microsoft employees make the most of their income and benefits.

Whether you work in the Microsoft headquarters in Redmond, Washington, another office location around the country, or remotely from home, you may have questions about your compensation package and benefits better suited for a financial professional who can offer unbiased advice and guidance.

For example, sensitive topics like discussing the steps you should take before quitting your job at Microsoft to work elsewhere, protecting yourself in advance of a corporate layoff, or deciding when you should plan to retire are all conversations that may be more comfortable with a trusted financial advisor.

Should you hire a Microsoft specialist financial advisor or an advisor close to home?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in serving Microsoft employees.

Fortunately, many financial advisors offer virtual services so you can meet online no matter where you (or they) live.

This means you can choose to hire a specialist financial advisor who lives hundreds of miles away if you decide their knowledge and experience working with Microsoft employees is a better fit to help with your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Microsoft employees to help them make smart decisions to get the most value from their compensation and benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Do you have questions not yet answered? Use the form below to submit questions anonymously and watch this article for updates with answers to your questions. You can also reach out to the financial advisors below to set up an introductory call or contact them with your questions by email.

Find Financial Advisors for Microsoft Employees

📍 Click on a pin in the map view below for a preview of financial advisors who specialize in serving Microsoft employees. Or choose the grid view to search our directory of financial advisors with additional filtering options.

📍Double-click or pinch pins to view more.

💸 Smart Money Insights for Microsoft Employees & Executives

This page is organized into sections to help you quickly find the information you need and get answers to your questions:

- Q&A: Financial Planning Tips for Microsoft Employees & Executives

- Get Answers to Your Questions About Your Microsoft Benefits and Career

- Quick Facts & Resources for Microsoft Employees

- Browse Related Articles

Q&A: Financial Planning Tips for Microsoft Employees & Executives

Get to Know:

↗️ Emily Rassam (Charlotte, North Carolina) and Richard Archer (Austin, Texas)

↗️ Noah Schwab (Spokane, Washington)

Answers to Microsoft Employee Questions with Emily Rassam and Richard Archer (Archer Investment Management)

Q: As a financial advisor with experience helping Microsoft employees save for their retirement, how do you help them make the most of their employee benefits?

Emily: At Archer Investment Management, we specialize in working with mid-career technology professionals. We have several Microsoft employees as clients and are familiar with the company’s employee benefit plans, retirement plans, equity compensation packages, and ancillary benefits. More importantly, we are acutely aware of the financial planning needs of technology professionals and how their Microsoft benefits fit into an overall financial plan, including long-term planning, goal setting, tax planning, and estate planning. We start by building a financial personality profile and risk tolerance assessment to understand your relationship with money and your comfort level with risk.

Q: When you first speak with a Microsoft employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

Richard: Our detailed onboarding process includes conversations about your life goals, how your finances play a role in maximizing happiness, and what it means to be intentional with money. We gather information about your benefits and compensation package, spending plan, short-term and long-term goals, taxes, estate plans, and insurance. This detailed planning process allows us to build a comprehensive picture of your financial life and how each piece of the puzzle fits together. You cannot make recommendations without examining the whole picture.

Q: Is there a particular benefit available to Microsoft employees you feel isn’t as well utilized or understood by employees as it should be?

Richard: The opportunity to do a Mega Backdoor Roth Conversion with after-tax 401(k) dollars is regularly underutilized. Employees often focus on contributing to their pre-tax or Roth 401(k) without realizing the power of after-tax contributions that can be converted to a Roth as soon as the contribution is made. The Mega Backdoor Roth Conversion strategy can be a way to fast-track your journey to financial independence.

Q: Beyond Microsoft employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients (e.g., stock, education savings, health savings)?

Emily: Microsoft offers an Employee Stock Purchase Plan (ESPP) within which they can receive a 10% discount on Microsoft stock. Employees at Level 67 or higher have a great opportunity to defer part of their bonus and salary and use vesting Restricted Stock Units (RSUs) as cash flow. A nice perk that employees may miss is the $1,500/year reimbursement for wellness-related expenses.

We applaud Microsoft for offering generous parental leave including 20 weeks of paid time away for mothers and 12 weeks of fully paid parental leave for all other new parents, including adoptions and foster placements. Fully paid family leave is also available for up to twelve weeks if an immediate family member is diagnosed with a serious health condition and requires care.

Get to Know Emily Rassam, Financial Advisor for Microsoft Employees:

View Emily’s profile page on Wealthtender or visit her website to learn more.

Q: For Microsoft employees thinking about leaving the company to accept a job elsewhere, what actions do you recommend they take before resigning and shortly thereafter?

Emily: Your matched 401(k) dollars are 100% vested from day one. However, you may have received employee stock options or RSUs that are unvested. Look carefully at the dates on your grants and vesting schedules to determine when each RSU grant vests; this may impact your timing to leave Microsoft – you don’t want to leave any money on the table! You have 90 days after departing the company to exercise your stock options. Work with an advisor to determine which grants to exercise and the best way to fund this purchase.

Q: For Microsoft employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

Richard: Our detailed retirement planning process includes:

- A spending strategy tailored to your income goals

- Social Security timing recommendations

- Coordination of health care benefits

- Discussion around how your spending will change throughout retirement

- Stress-testing your retirement projection with many what-if scenarios

- Timing your exit to maximize any unvested incentive stock options (ISOs), non-qualified stock options (NSOs), or RSUs

Q: For Microsoft employees who have managed their finances on their own to this point, what would you suggest they consider to help them decide if they should begin working with a financial advisor at this stage in their lives?

Emily: There are many online tools and calculators. Where we find Microsoft employees get stuck is understanding how to prioritize goals and seeing the big picture. We help Microsoft employees organize their financial lives and provide accountability for reaching goals. Understanding whether you should use surplus dollars to pay down debt, save towards a short-term goal, or work towards a long-term aspiration (such as retirement or college education savings) can be challenging. For Microsoft employees planning with a spouse or partner, an advisor helps facilitate difficult conversations and moves the ball forward in your planning process.

Q: What are some of the unique financial planning challenges you commonly see among your clients who are Microsoft employees and how do you help them overcome these obstacles?

Richard: One common obstacle we find is knowing when to diversify away from the concentration risk of holding a high percentage of your net worth in one company’s shares. Many of our Microsoft employee clients struggle with selling positions; it requires coaching, recognizing natural human biases, an evaluation of the risks, and careful diversification away from an outsized position.

Get to Know Richard Archer, Financial Advisor for Microsoft Employees:

View Richard’s profile page on Wealthtender or visit his website to learn more.

Q: What questions do you recommend Microsoft employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

Richard: If you were granted ISOs or RSUs, be sure to work with an advisor who understands how to incorporate those into your overall picture. Seek an advisor who can model the alternative minimum tax (AMT), understands the rules around qualifying and disqualifying dispositions, and knows how and when to diversify away from sizeable single stock positions, if appropriate.

Q: Is there anything that comes up frequently in your initial meeting with Microsoft employees that surprises you?

Richard: Employees don’t always understand the full realm of benefits – both big and small – available to them. Be sure to carefully review the benefits available to you! For some employees, this may be the first time they have received an equity compensation package. They often need our guidance to fully understand the type of grant they received and potential tax impacts. We enjoy helping people with strategies to ensure they fully benefit from their entire compensation package.

Q: For highly compensated Microsoft employees and executives, are there any special benefits you believe it’s important to take into consideration when preparing their financial plan?

Emily: The Microsoft Deferred Compensation Plan (DCP) is available to employees at Level 67 or higher. This enables employees to save and invest up to 100% of their annual cash bonus and up to 75% of their salary. Importantly, contributions to the DCP reduce your annual taxable income. By reviewing the full picture of your salary, bonus, and equity compensation, we can identify key strategies to help you maximize the DCP benefit.

Q: Is there a particularly memorable experience or a moment you recall with a client who worked at Microsoft when you realized they have unique opportunities and circumstances when it comes to their financial planning needs?

Emily: One of our clients is an executive at Microsoft, and he was unfamiliar with the after-tax savings and daily Mega Backdoor Roth Conversion opportunities. We reviewed the plan documents and rules to guide him during the enrollment process and showed him how to use ongoing vesting RSUs for cash flow while maximizing after-tax savings to quickly build his Roth accounts. The executive and his wife are in their 50s, and the strategy was especially beneficial for their goal of retiring early in a lower tax bracket. We have also helped our clients utilize the College Coach program which helps parents navigate through college admissions and financial aid processes.

Answers to Microsoft Employee Questions with Noah Schwab, CFP®

Noah Schwab is a financial advisor based in Spokane, Washington who specializes in offering financial planning services to Microsoft employees. Noah helps his clients get the most value from their Microsoft benefits and compensation package so they can enjoy life and feel confident about their financial future.

Q: As a financial advisor with experience helping Microsoft employees save for their retirement, how do you help them make the most of their employee benefits?

Noah: Working with Microsoft employees means navigating one of the most generous and complex benefit packages in the tech industry. My goal is to make sure clients take full advantage of what is available, especially when it comes to retirement planning, tax efficiency, and managing equity compensation. Here are some of the key areas where I help Microsoft employees get the most value:

401(k) and Mega Backdoor Roth Contributions

Microsoft offers a strong 50% 401(k) match up to the federal limit. But on top of that, Microsoft’s plan allows after-tax contributions up to the full IRS limit (up to $77,500 if age 50+ in 2025). That can be converted into a Roth 401(k) or Roth IRA for years of tax-free growth if implemented correctly. This allows employees to circumvent the normal income limits of a Roth IRA and get a massive amount of money into tax-free growth.

Employee Stock Purchase Plan (ESPP)

Microsoft’s ESPP allows employees to buy MSFT stock at a 10 percent discount with contributions deducted from each paycheck and purchases made quarterly. I work with clients to evaluate how much they should contribute, when they should sell shares to avoid becoming too concentrated in a single stock, and how to manage the tax implications based on the length of time the shares are held.

Restricted Stock Units (RSUs)

RSUs comprise a significant portion of Microsoft’s compensation. I help clients create a strategy around when to sell, how to set aside funds for the taxes due at vesting, and how to diversify, and potentially consider a direct indexing strategy. This becomes especially important for those approaching retirement.

Deferred Compensation Plan (for Level 67 and above)

For senior-level employees, Microsoft offers a Deferred Compensation Plan. This benefit allows employees to defer a portion of their salary and bonuses to future years, which can result in significant tax savings if done correctly. I help clients decide how much to defer and when to receive distributions in a way that aligns with their retirement income needs and tax bracket planning.

Health Savings Account (HSA)

Microsoft offers a high-deductible health plan that is eligible for an HSA, and the company makes generous annual contributions to the account. I encourage clients to utilize this account as a long-term retirement savings tool by investing the funds and making withdrawals only when necessary. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free.

Charitable Giving and Matching

Microsoft matches employee charitable contributions up to $15,000 per year. For charitably inclined clients, I help them maximize this benefit while also utilizing advanced strategies, such as Donor-Advised Funds. This can create a bigger impact and reduce taxes, especially during high-income years when RSUs are vesting.

Q: When you first speak with a Microsoft employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

Noah: When I first talk with a Microsoft employee, I focus on understanding their current use of Microsoft benefits and their financial goals. I ask about their level and tenure to determine which benefits they are eligible for, such as the Deferred Compensation Plan or pension. I check if they are maximizing their 401(k) contributions, including after-tax options for the Mega Backdoor Roth.

I also ask about their approach to Microsoft stock through the ESPP and RSUs to assess risk and tax planning. Understanding their career plans helps with timing strategies around equity and benefits. I inquire about their Health Savings Account usage and charitable giving to identify additional tax-smart opportunities. Finally, I learn about their personal goals to tailor a plan that fits their life, not just their finances.

This helps me create a clear, customized strategy that aligns their Microsoft benefits with their long-term goals.

Q: Is there a particular benefit available to Microsoft employees you feel isn’t as well utilized or understood by employees as it should be?

Noah: Yes, the Mega Backdoor Roth is often overlooked. Many employees are familiar with the standard 401(k) match but may not be aware that they can make large after-tax contributions and then convert those to a Roth account.

Q: Beyond Microsoft employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients (e.g., stock, education savings, health savings)?

Noah: Absolutely. Microsoft offers several valuable benefits beyond retirement savings that I always review with clients. The Employee Stock Purchase Plan lets employees buy stock at a discount, which can be a great way to build wealth if managed carefully. The Health Savings Account is another powerful tool. I also discuss charitable giving options for those who are inclined to give charitably. With Microsoft’s matching program, it can create a meaningful impact while providing tax benefits.

Q: For Microsoft employees thinking about leaving the company to accept a job elsewhere, what actions do you recommend they take before resigning and shortly thereafter?

Noah: Before leaving Microsoft, it is important to review key benefits and plan ahead. I recommend confirming RSU vesting dates so you do not forfeit valuable stock by leaving too early. Look at your 401(k) contributions and the status of any after-tax amounts that could still be converted to Roth. If you are eligible for the Deferred Compensation Plan, make sure you understand how your deferral and payout schedule will be affected.

Shortly after leaving, review your healthcare coverage options, decide what to do with your 401(k), and create a plan for your Microsoft stock. It is also a good time to revisit your overall financial goals and adjust your plan for the new role, compensation, and benefits you will be receiving.

Leaving Microsoft is a big transition, and taking a few smart steps before and after can protect the benefits you worked hard to earn.

Q: For Microsoft employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

Noah: The first step is to determine how much you will need to spend each year in retirement. This typically begins by either creating a retirement budget or working backward from your current income to estimate the yearly spending required to support your lifestyle, then accounting for future inflation.

Next, I help Microsoft employees map out where their income will come from. This includes 401(k) plans, Roth accounts, RSUs, deferred compensation, Social Security, and any other savings. From there, we create a plan for how and when to draw from these sources in a tax-efficient way. We also run projections to assess the likelihood that their savings will last through retirement while still supporting their goals, such as travel, family, or leaving a legacy.

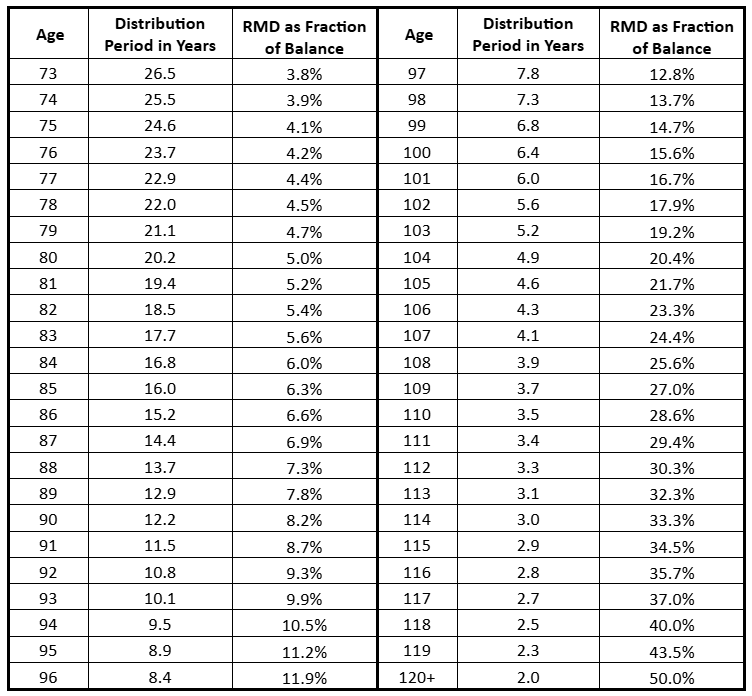

A major area we focus on is planning for required minimum distributions (RMDs) from tax-deferred accounts. If someone has over one million dollars in a 401(k), RMDs can push them into a higher tax bracket. In such cases, we often explore Roth conversions in lower-income years or qualified charitable distributions (QCDs) starting at age 70.5 to reduce or eliminate the tax burden.

We also review their Microsoft stock holdings to see if it makes sense to diversify and reduce risk. Healthcare planning is another important part of the transition. We examine coverage options after Microsoft ends and consider whether an HSA or other savings can help cover the costs.

All of this comes together in a clear income and tax strategy, so they can step into retirement with confidence, knowing their money is working toward the life they want to live.

Q: For Microsoft employees who have managed their finances on their own to this point, what would you suggest they consider to help them decide if they should begin working with a financial advisor at this stage in their lives?

Noah: If you have done a great job managing your finances on your own, that is a strong foundation. However, as you approach retirement, the decisions become more complex and the stakes are higher. At this stage, it is not just about saving and investing. It is about turning those savings into a reliable income stream, managing taxes, and avoiding costly mistakes.

I encourage Microsoft employees to ask themselves a few questions. Do you have a clear plan for when to start Social Security and how to draw from different accounts in a tax-efficient way? Have you mapped out what your RSUs, deferred compensation, or 401(k) will look like in retirement? Are you prepared for required minimum distributions and how they will affect your taxes? Do you feel confident about your healthcare and estate planning?

If any of those questions feel unclear or overwhelming, it may be the right time to work with a financial advisor. The value often comes not from doing something you could not do yourself, but from having someone help you avoid mistakes, find better strategies, and give you peace of mind.

Q: What are some of the unique financial planning challenges you commonly see among your clients who are Microsoft employees and how do you help them overcome these obstacles?

Noah: One of the biggest challenges is managing the complexity of compensation, which often involves a combination of salary, bonuses, RSUs, ESPP, and, in some cases, deferred compensation. I help clients develop a clear strategy to manage cash flow, reduce taxes, and maximize the benefits they receive.

Another common issue is future required minimum distributions. We create a long-term tax plan utilizing strategies such as Roth conversions and charitable giving to help reduce future tax burdens.

Many clients also hold excessive amounts of Microsoft stock without realizing the associated concentration risk. I help them create a plan to gradually diversify in a way that fits their goals and comfort level.

Lastly, preparing for retirement involves important decisions about income, healthcare, and Social Security. I work with clients to create a plan that brings clarity and confidence as they shift from saving to spending.

Q: What questions do you recommend Microsoft employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

Noah: Choosing the right advisor is an important decision. I recommend asking a few key questions to help you find someone who understands your situation and can provide real value.

Start by asking, Have you worked with other Microsoft employees before? The benefits and compensation can be complex, so experience matters.

Then ask, How do you get paid? Look for transparency. Fee-only advisors are paid directly by you, not through commissions, so their advice is more likely to be in your best interest.

Another helpful question is, Will you create a tax plan as part of the financial plan? With RSUs, deferred compensation, and substantial 401(k) balances, an effective tax strategy is crucial.

Finally, ask: Who will I be working with on a day-to-day basis, and how often will we meet? You want someone who is accessible and proactive, not just someone who shows up once a year.

The right advisor should not only manage your investments but also help you make informed decisions with all aspects of your financial picture.

Q: Is there anything that comes up frequently in your initial meeting with Microsoft employees that surprises you?

Noah: Yes, I’m often surprised by how many Microsoft employees are not fully using some of the most powerful benefits available to them. For example, many people are unaware that they can make after-tax contributions to their 401(k) and convert them to a Roth account. This Mega Backdoor Roth strategy can significantly boost long-term, tax-free retirement savings.

Another common surprise is the amount of Microsoft stock people have accumulated without a clear plan. It is easy to let RSUs accumulate over time, but that can create unnecessary risk concentrated in one stock if left unchecked, especially if you’re close to retirement.

Lastly, many employees are not sure how all the pieces of their compensation fit together. Salary, bonuses, RSUs, ESPP, and deferred comp often feel disconnected. One of the first things I do is help organize everything into one clear plan so they can see how each part works toward their long-term goals.

Q: For highly compensated Microsoft employees and executives, are there any special benefits you believe it’s important to take into consideration when preparing their financial plan?

Noah: Yes, for senior-level employees and executives at Microsoft, several key benefits deserve special attention in the financial planning process.

One of the most important is the Deferred Compensation Plan, which allows eligible employees to defer a portion of their salary and bonus into future years. This can be a powerful tax planning tool, but it also requires careful coordination with other income sources and future cash flow needs.

Another area to focus on is RSU and stock concentration. High earners often receive a large portion of their compensation in Microsoft stock, which can lead to an outsized exposure. I help clients create a plan to diversify their investments over time while managing their taxes through effective tax strategies, such as direct indexing.

Many executives also face higher tax exposure, so we look closely at Roth conversion strategies, charitable giving through Donor-Advised Funds, and long-term planning for required minimum distributions.

Q: Is there a particularly memorable experience or a moment you recall with a client who worked at Microsoft when you realized they have unique opportunities and circumstances when it comes to their financial planning needs?

Noah: Yes, I remember working with a Microsoft employee who was approaching retirement with a sizable portfolio of RSUs, a large 401(k), and access to the Deferred Compensation Plan. What stood out was how many options they had to shape their retirement through timing and tax strategies.

Together, we developed a plan that leveraged Roth conversions during lower-income years and employed a charitable giving strategy to manage required minimum distributions. We also created a clear roadmap for diversifying their Microsoft stock holdings while balancing their risk.

That experience highlighted how Microsoft employees have access to powerful tools but also face complexity that requires careful planning. It reinforced the importance of helping them see the big picture and create a plan tailored to their specific circumstances.

Get to Know Noah Schwab, Financial Advisor for Microsoft Employees:

View Noah’s profile page on Wealthtender or visit his website to learn more.

Are you a financial advisor who specializes in working with employees at Microsoft or another large company?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with employees at Microsoft or another large company. (Subject to availability and terms.)

✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender

✅ Or request more information by email:

Quick Facts & Resources for Microsoft Employees

🙋♀️ Have Questions About Your Microsoft Benefits or Career?

📰 Browse Related Articles

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

About the Author

Brian Thorp

Founder and CEO, Wealthtender

Brian and his wife live in Texas, enjoying the diversity of Houston and the vibrancy of Austin.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Connect with Brian on LinkedIn