If you’re a confident, self-directed investor, you may not want a financial advisor who takes over management of your portfolio — but you might still want expert guidance on the decisions that really matter. Advice-only financial advisors offer exactly that: professional financial planning and investment guidance without managing your assets or earning commissions, at a cost that’s typically far lower than traditional advisory fees. This guide explains what advice-only services are, how they compare to traditional advisory relationships, what questions to ask before hiring one, and where to find advice-only financial advisors on Wealthtender.

If you consider yourself a DIY (do it yourself) kind of person, you’re not alone. Millions of Americans successfully start and complete DIY projects every day.

But just because you decide to do a project yourself doesn’t mean you have to learn how to do the task on your own. In fact, most DIY projects start with education in the form of instructional videos, articles, books, or even live demonstrations.

The same holds when it comes to managing your personal finances and investing. If you consider yourself a DIY investor and are comfortable managing your own money, you may not want to hire a traditional financial advisor and turn over financial decision-making to someone else.

Fortunately, a new breed offinancial advisors offering advice-only services has emerged as a popular choice among DIY investors interested in professional guidance at a very attractive cost.

Key Takeaways

1

An advice-only financial advisor provides professional guidance and a financial plan — but you, not the advisor, implement the recommendations. This is fundamentally different from traditional advisory relationships where the advisor manages your investments.

Because advice-only advisors don’t manage assets or earn commissions, their compensation isn’t tied to any product outcome — which means their guidance can go anywhere your financial situation requires without the constraints or conflicts that come from managing a portfolio. Most charge an hourly or flat fee, and many are SEC-registered RIAs who hold the CFP designation. The tradeoff: you’re responsible for executing the plan yourself, which requires a level of financial confidence and follow-through that not every investor has.

2

There’s an important distinction between “advice-only advisors” who exclusively operate this way and traditional advisors who offer advice-only as one option among several — and that distinction matters when evaluating conflicts of interest.

A dedicated advice-only advisor has structured their entire practice around not managing assets or earning commissions — eliminating the most common conflicts that arise in financial advisory relationships. An advisor who offers advice-only as one of several service options may still have business incentives that subtly favor other arrangements. Both can provide legitimate advice-only services, but understanding which type you’re working with helps you evaluate the advice you receive more accurately.

3

Advice-only services are best suited to DIY investors, high-asset clients who want to avoid percentage-based AUM fees, and anyone seeking a second opinion on a financial plan they’ve already developed.

For a self-directed investor managing a large portfolio, the savings from avoiding a 1% AUM fee can be substantial — on a $2 million portfolio, that’s $20,000 per year that stays invested instead of going to an advisor. Advice-only services are also well-suited to one-time planning engagements: reviewing a retirement plan, evaluating a job offer’s equity compensation, or stress-testing a financial strategy before a major decision. The key question to ask any advice-only advisor: do they provide tools or technology to help you implement their recommendations independently?

Advisors Who Offer “Advice-Only Services” vs. “Advice-Only Advisors”

As you evaluate financial advisors who offer “advice-only” services, it’s worth noting a distinction between advisors who may offer multiple compensation models for their services, with “advice-only” among them vs. advisors who hold themselves out as “advice-only advisors” and exclusively act in an advice-only capacity.

When financial advisors provide advice-only financial planning services and investment guidance, it’s their clients, not the advisors, who are responsible for implementing the recommendations independently. Because these advisors do not manage your investments for you, the cost of hiring a financial advisor offering advice-only services is often considerably less than hiring a financial advisor and paying a percentage of assets under management, especially for people with large investment portfolios.

“Advice-only advisors” are Registered Investment Advisors (RIAs) regulated by the Securities and Exchange Commission (SEC) or by state regulators where their services are available. Many advice-only financial advisors will hold their Certified Financial Planner certification and will likely charge an hourly or flat fee for their services.

While you’ll be responsible for implementing recommendations on your own, some advice-only financial advisors offer technology and tools to make it easier for you to follow their guidance. Before hiring an advice-only advisor or an advisor who offers advice-only services, be sure to ask if they offer resources to help streamline your DIY efforts.

Should I Hire a Financial Advisor Who Offers Advice-Only Services?

If you consider yourself a DIY investor, you may still desire the benefit of professional guidance a financial advisor who offers advice-only services can provide to help you make smart decisions with your money. Or, if you’re looking for a second opinion regarding investment decisions or a financial plan you’ve prepared on your own, an advice-only financial advisor can review your work and offer feedback and recommendations to help ensure you’re on track to achieve your financial goals.

How to Find Financial Advisors Who Offer Advice-Only Services

📍 Click on a pin in the map view below to discover financial advisors who offer advice-only services and can work with you to develop a personalized financial plan. Or click the Grid option to view these advisors in a directory.

What Questions Should You Ask Before Seeking Advice-Only Services?

To help you find the right financial advisor who offers advice-only services for your individual needs, it’s best to ask the right questions to determine if you’re a good fit to work together.

We asked financial advisors who offer advice-only services in the Wealthtender community for their thoughts on good questions to ask.

Eric Simonson, CFP®, CRPC®, CLTC®Advice-Only Financial Planning For Everyone

With an advice-only advisor, you fortunately do not need to ask them the usual questions you would a typical advisor such as 1) What hidden fees do you charge? 2) Do you sell products and make commissions? 3) Are you a fiduciary?

You can rest assured that with an advice-only model, you are receiving some of the fairest, most transparent advice available in our industry. So, the questions you should ask should be tailored more towards your specific situation.

For example, if you have student loans, ask them about their knowledge around student loans and typical strategy for how to tackle that debt. Or, if you own rental properties, how familiar are they with them and what recommendations do they usually provide there? Also make sure it is a good personality fit so ask about hobbies, communication style, etc.

Andrew Dressel, CFP®, CRPC®, APMA®Advice-Only Financial Planning For Everyone

What range of subjects do you work on with your clients? Do those areas of advice align with the needs that you are trying to address? How are your fees determined?

How Does an Advice-Only Financial Advisor Compare to a Traditional Financial Advisor?

Beyond not managing their clients’ investments and earning a fee for this service, how else do advice-only financial advisors differ from traditional advisors? Should you expect the same services other than investment management? We asked advice only financial advisors what they think.

Andrew Dressel, CFP®, CRPC®, APMA®Advice-Only Financial Planning For Everyone

I would say that you should get the same if not more advice from an advice-only financial advisor than you would from a fee-only or commission-based financial advisor. This is because an advice-only financial advisor isn’t tied to a product outcome.

Traditional Financial advisors use financial advice to drive to certain outcomes or products that they receive a benefit or compensation from. The scope of the relationship with and advice-only advisor is based on depth and breadth of the advice that you get.

Eric Simonson, CFP®, CRPC®, CLTC®Advice-Only Financial Planning For Everyone

Every advisor is going to be a little unique in terms of their service offering, but on the whole you can expect advice-only advisors to be much more comprehensive with their advice since their income is in no way tied to the advice they provide. So, they are really free to ‘go anywhere’ with their guidance/advice.

Expert Insights: Should I Hire an Advice-Only Financial Advisor or a Traditional Advisor?

Danielle Miura, CFP®

Spark Financials

“Advice-Only firms ensure transparency of compensation and minimize conflicts of interest. At Spark Financials, we provide financial advice to empower our clients to be self-reliant and visualize their financial future. We are the navigator, and our clients are the driver.

Our firm is set up to not hold or have access to our client’s assets; therefore, our clients are protected from hidden fees. When a financial advisor manages assets, many clients are not able to see the direct impact of fees taken out of their accounts over time.

We also do not refer clients to someone who can manage their assets, preventing any kickback or markup compensation. We minimize conflicts of interest and fees for our clients so they can reach their goals faster and safer. Instead of managing our client’s assets to make them rely on us, we educate our clients so they can eventually be independent. Our goal is to be as transparent as possible; this means no commission and no hidden fees.”

Are You a Financial Advisor Who Offers Advice-Only Services?

👋 Hi there! We’re excited to help more people understand the benefits of working with advice-only financial advisors and advisors who offer advice-only services. And we want to help connect people to the best financial advisors for their individual needs. If you offer advice-only services, we encourage you to join our growing community of financial advisors featured on Wealthtender so we can add you to this guide soon. Click here to learn more and get started.

About the Author

About the Author

Brian Thorp

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Are you among the 400,000 Oregon public employees and retirees who are members of the Oregon Public Employees Retirement System? Get the resources you need and expert insights from financial professionals who specialize in helping Oregon PERSmembers make the most of their benefits.

Whether you’re a new public employee in Oregon, nearing retirement, or enjoying your golden years, it’s important to make smart money moves with your Oregon Public Employees Retirement System (PERS) benefits. For example:

✅ Do you know the right moves to make to get the greatest value from the Oregon PERS benefits available to you?

✅If you’re thinking about leaving pubic employment for a corporate position or planning to retire in a few years, are you taking the right steps today to ensure you will receive all of the compensation and benefits that you’ve earned?

Get the Most Value from Your Oregon PERS Benefits

Throughout the year, Oregon PERS provides its members with updates about their benefits, including health insurance, pension, and defined contribution retirement plans. While Oregon PERS offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Oregon PERS who specialize in helping Oregon PERS members make the most of their benefits.

As an Oregon PERS member, you may have questions about your benefits better suited for a financial professional who can offer unbiased advice and guidance.

For example, sensitive topics like discussing the steps you should take before quitting your job as a public employee to work elsewhere or deciding when you should plan to retire are all conversations that may be more comfortable with a trusted financial advisor.

Should you hire an Oregon PERS specialist financial advisor or an advisor close to home?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in serving Oregon PERS members.

Fortunately, many financial advisors offer virtual services so you can meet online no matter where you (or they) live.

This means you can choose to hire a specialist financial advisor who lives on the other side of the state if you decide their knowledge and experience working with Oregon PERS members is a better fit to help with your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Oregon PERS members to help them make smart decisions to get the most value from their benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Do you have questions not yet answered? Use the form below to submit questions anonymously and watch this article for updates with answers to your questions. You can also reach out to the financial advisors below to set up an introductory call or contact them with your questions by email.

💸 Smart Money Insights for Oregon PERS Members

This page is organized into sections to help you quickly find the information you need and get answers to your questions:

Q&A: Financial Planning Tips for Oregon PERSMembers

Get Answers to Your Questions About Your Oregon PERSBenefits

Browse Related Articles

Q&A: Financial Planning Tips for Oregon PERS Members

Answers to Employee Questions with Steven Jamison, CFP®, CPA

Steven Jamison is a financial advisor based in Salem, Oregon who specializes in offering financial planning services to State of Oregon Public Employees (PERS) employees. Steven helps his clients get the most value from their State of Oregon Public Employees (PERS) benefits and compensation package so they can enjoy life and feel confident about their financial future.

Q: As a financial advisor with experience helping State of Oregon Public Employees (PERS) employees save for their retirement, how do you help them make the most of their employee benefits?

Steven: We help navigate decisions regarding tax deferred retirement savings, life insurance, long term care insurance, retiree health insurance, and other benefits, including tax and financial implications during an employee’s employment. We then help with decision making regarding PERS, IAP and OSGP payouts at retirement.

Q: When you first speak with a State of Oregon Public Employees (PERS) employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

Steven: When were you first hired? When do you plan to retire? What benefits are you currently using? Do you have a spouse you would like to provide for in case of death? What insurance do you have outside of your employee benefits?

Q: Is there a particular benefit available to State of Oregon Public Employees (PERS) employees you feel isn’t as well utilized or understood by employees as it should be?

Steven: The Oregon Savings Growth Plan (OSGP) allows for a 3 year catchup (PDF) beyond the catch up contributions permitted for savers over age 50. For three years prior to the employee’s defined full retirement age the employee can contribute extra amounts if they did not historically maximize their deferrals. I’ve attached a document about this.

Q: Beyond State of Oregon Public Employees (PERS) employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients (e.g., stock, education savings, health savings)?

Steven: Long term care insurance. Life insurance. Retiree health insurance.

Q: For State of Oregon Public Employees (PERS) employees thinking about leaving the company to accept a job elsewhere, what actions do you recommend they take before resigning and shortly thereafter?

Steven: Maximizing available retirement contributions, cash flow permitting.

Q: For State of Oregon Public Employees (PERS) employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

Steven: Prepare a personal budget for retirement. Evaluate available PERS, OSGP, IAP and other retirement benefits to assess the best spend down strategy, especially for tax efficiency. Consider service buy back options using IAP funds as a potentially tax efficient way to increase the PERS pension payout.

Q: Is there a particularly memorable experience or a moment you recall with a client who worked at State of Oregon Public Employees (PERS) when you realized they have unique opportunities and circumstances when it comes to their financial planning needs?

Steven: We had a client who had been unable to save for retirement for a number of years but found himself inheriting wealth. With the newly available cash he was able to take advantage of the tax benefits associated with the 3 year catchup contributions and make significant progress towards his retirement goals.

Get to Know Steven Jamison Financial Advisor for State of Oregon Public Employees (PERS) Employees:

Are you a financial advisor who specializes in working with Oregon PERS members or a large employer?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with Oregon PERS members or another large company. (Subject to availability and terms.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender ✅ Or request more information by email:

🙋♀️ Have Questions About Your Oregon PERSBenefits?

Get answers from the Wealthtender network of financial professionals and educators.

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

About the Author

Brian Thorp

Founder and CEO, Wealthtender

Brian and his wife live in Texas, enjoying the diversity of Houston and the vibrancy of Austin.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Like most writers I have a lot of reservations around generative AI. It’s already stolen part of my job, and I’m concerned it’s coming for the rest of it. But burying your head in the sand is probably not the way to go right now if you’re a freelancer.

AI is here to stay. Like most intelligent people, I’m hoping we’re going to be able to find ways to make it ethical and useful, while still retaining and valuing human creativity.

I’m also aware that there are many ways that freelancers like me can use AI tools to increase efficiency, find more clients, and therefore boost profits. Here are some of the ways AI can help you as a freelancer.

Content Creation

Many people are using ChatGPT or similar tools to give them ideas for products, services, blog posts, YouTube videos and social media posts. Some are also using them to write blog posts or video scripts.

I’m not an advocate for getting AI to write these things for you, but it can be used to give you an outline of what people want to know about a particular topic, or what the key points are that you should include.

It’s also great for helping with headlines. AI tools like The Coschedule Headline Analyser and the Capitalize My Title tool, can be used to rewrite your headline, in a specific style and for a specific type of content. This can be really useful given that the headline is always one of the most important elements of any piece of content you put out.

AI can also help with producing visual content. Tools like Canva AI, Napkin, and Kittl can help you design and produce eye-catching visuals and graphics for social media, your website, or your sales pages.

Project Management

I’m a fan of Notion for general, AI-powered project management. It lets me automate repetitive tasks, create deadlines, and set reminders so I can manage the small but complex set of projects that are always on my to-do list as a busy freelancer.

I like that it lets me create a reading/research list for each project I’m working on, letting me switch back and forth between my book, the digital product I’m working on, and day-to-day work like essays, articles and newsletters.

It also lets me manage personal stuff too, from exercise goals to my reading-for-pleasure list, effectively letting me plan out most aspects of my life — from one dashboard.

Finding Freelance Clients

Apob AI is a new tool I’m still finding my way around, but it was recommended to me after something I mentioned in one of my online freelancing forums.

Basically, I lack the video filming and editing skills to make the short videos that are needed to help freelancers stand out on platforms like Upwork, Freelancer.com, and Fiverr.

This one allows you to create professional looking videos in minutes, including ‘talking avatar’ videos, image-to-video, and text-to-video: useful if actually filming and editing videos is outside of your wheelhouse.

It also allows you to find new clients, by offering a broader range of services. Apob AI allows you to easily make things like explainer videos, which are really popular with some clients, or convert written content to video, allowing a broader reach online, across a larger number of platforms, for you and your clients.

These types of videos don’t aim to replace authentic, real-life vloggers, who will likely always be popular on platforms like YouTube or TikTok. They fill a totally different gap in the market for brands and professionals who need quick video content for very specific purposes.

As I say, I’m brand new to this one so can’t delve into any details right now, but I’ll be playing with it a lot in the coming weeks to see if it’s something that can be incorporated into my business.

Extra Tip: Don’t Hide Your AI Skills

One of the reasons AI already has a bad reputation among creatives is that people are using AI to create stuff that they then claim as their own and sell to clients. I can’t stress enough that this is not the way to do it.

Instead, make your ability to use specific AI tools to achieve desirable metrics part of your sales pitch. Many of these tools are simple to use once you’ve learned how, but most freelancers simply don’t know how to use them.

It’s fine to be the freelancer that offers to make “simple, high-quality, explainer videos using cutting edge AI tools”.

It’s fine to be the virtual assistant that can “manage multiple projects via one simple Notion AI dashboard, where I’ll track and organise every task and every deadline, for up to 20 projects at a time.”

Learn how to use a specific AI tool efficiently, creatively and ethically. Then make your AI knowledge and expertise your freelancing superpower, not your dirty secret.

About the Author

Karen Banes is a freelance writer specializing in entrepreneurship, parenting and lifestyle. She writes articles, website content, ebooks and the occasional award winning short story. Her work has appeared in a range of publications both online and off, including The Washington Post, Life Info Magazine, Transitions Abroad, Brave New Traveler, Natural Parenting Group, and Copia Magazine.

Learn More About Karen

Do you work at Raytheon Technologies (RTX)? Get the resources you need and expert insights from financial professionals who specialize in helping Raytheon Technologiesemployees make the most of their compensation package and benefits.

Whether you’re a new Raytheon Technologies employee or you’ve moved up the ranks into a management or executive leadership role over a multi-year career, it’s important to make smart money moves with your income and employee benefits. For example:

✅ Do you know the right moves to make to get the greatest value from the Raytheon Technologies benefits available to you?

✅If you’re thinking about leaving Raytheon Technologies for another job or planning to retire from the company in a few years, are you taking the right steps today to ensure you will receive all of the compensation and benefits that you’ve earned?

Get the Most Value from Your Raytheon Technologies Benefits and Compensation Package

Throughout the year, Raytheon Technologies provides its employees and executives with updates about their benefits ranging from health insurance and health savings plans to retirement plans like a 401(k), deferred compensation plans, and stock options. While the company offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Raytheon Technologies who specialize in helping Raytheon Technologies employees make the most of their income and benefits.

Whether you work in the Raytheon Technologies headquarters in Arlington, Virginia, another office location around the country, or remotely from home, you may have questions about your compensation package and benefits better suited for a financial professional who can offer unbiased advice and guidance.

For example, sensitive topics like discussing the steps you should take before quitting your job at Raytheon Technologies to work elsewhere, protecting yourself in advance of a corporate layoff, or deciding when you should plan to retire are all conversations that may be more comfortable with a trusted financial advisor.

Should you hire a Raytheon Technologies (RTX) specialist financial advisor or an advisor close to home?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it may be more difficult to find a financial advisor who specializes in serving Raytheon Technologies employees.

Fortunately, many financial advisors offer virtual services so you can meet online no matter where you (or they) live.

This means you can choose to hire a specialist financial advisor who lives hundreds of miles away if you decide their knowledge and experience working with Raytheon Technologies employees is a better fit to help with your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Raytheon Technologies employees to help them make smart decisions to get the most value from their compensation and benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Do you have questions not yet answered? Use the form below to submit questions anonymously and watch this article for updates with answers to your questions. You can also reach out to the financial advisors below to set up an introductory call or contact them with your questions by email.

Answers to RTX Employee Questions with Allen Mueller, CFA, MBA

Allen Mueller is a financial advisor based in Richardson, Texas, who specializes in offering financial planning services to Raytheon Technologies (RTX) employees. Allen helps his clients get the most value from their Raytheon Technologies benefits and compensation package so they can enjoy life and feel confident about their financial future.

Q: Is there a particular benefit available to Raytheon Technologies employees you feel isn’t as well utilized or understood by employees as it should be?

Allen: A huge benefit to Raytheon employees is the RAYSIP retirement plan which allows pre-tax, Roth, or after-tax contributions. In 2022, a high saver who wants to maximize their tax-advantaged accounts can contribute $20,500 to their pre-tax 401(k) ($27,000 if over age 50). On top of that, they can contribute about $40,000 to the after-tax 401(k) and convert that amount to Roth with an in-service conversion. This strategy, also known as the “Mega Backdoor Roth”, is popular among those who are above the income threshold to contribute to a Roth IRA.

Q: Beyond Raytheon Technologies employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients?

Allen: Raytheon healthcare plans are typically HSA eligible which means maximum account contributions of $3,650 for individuals or $7,300 for families (2022 values). The HSA is a fantastic way to lower taxable income at contribution, the money can be invested to grow tax-free, and withdrawals are tax-free if used for eligible medical expenses. Bonus points – the contributions to an HSA get to dodge Social Security and Medicare taxes if funded through payroll contributions. Building up a massive HSA balance can be an effective way to pay for Medicare premiums in retirement or self-insure for long-term care (LTC).

Another fantastic benefit is the group legal plan – a very cost-effective way to get estate planning documents like wills and trusts drafted for about $240. Normally, these documents cost several thousand dollars. Employees can choose the plan during open enrollment, pay for a year of the service, get documents created, and decline coverage during the next year’s open enrollment.

Q: What are some of the unique financial planning challenges you commonly see among your clients who are Raytheon Technologies employees, and how do you help them overcome these obstacles?

Allen: A common challenge among Raytheon employees, particularly those who are entering retirement, is the large tax-deferred balances in their 401(k) plans. If not mitigated, Required Minimum Distributions (RMDs) can cause a massive tax bill after age 72.

It’s important for retirees to work with a competent financial planner and develop a strategy to get ahead of RMDs during lower-income years. Typically implemented in the “tax planning window” between retirement and age 72, tools can include Roth conversions, delaying Social Security, and withdrawing from taxable accounts.

Q: What questions do you recommend Raytheon Technologies employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

Allen: Questions to ask a potential advisor include:

Do you act as a fiduciary (in my best interest) at all times?

How are you compensated? Do you sell any products?

How much (in dollars) can I expect to pay now and in the future?

Do you require me to move my assets, or can you provide advice only without investment management?

Do you focus solely on investments, or do you also advise on other important areas like tax planning, estate, retirement, debt/cash flow management, and insurance?

What is your investment philosophy?

What professional credentials do you hold?

Get to Know Allen Mueller, Financial Advisor for Raytheon Technologies Employees:

Answers to RTX Employee Questions with Jeffrey Davis, AAMS®

Jeffrey Davis is a financial advisor based in Santa Barbara, California who specializes in offering financial planning services to Raytheon employees. Jeffrey helps his clients get the most value from their Raytheon benefits and compensation package so they can enjoy life and feel confident about their financial future.

Q: As a financial advisor with experience helping Raytheon employees save for their retirement, how do you help them make the most of their employee benefits?

Jeffrey: When working with Raytheon employees, I start by helping them understand the full scope of their benefits package—because maximizing retirement readiness begins with leveraging what’s already available. I focus on strategies that integrate the Raytheon savings plan (such as the RTX 401(k) with potential employer match), as well as supplemental benefits like the Employee Stock Purchase Plan, all within a broader financial plan.

We explore contribution limits, Roth versus traditional deferrals, and tax-efficient withdrawal strategies to enhance long-term growth potential. I also guide clients through decisions around pension options and deferred compensation, ensuring they align with their broader retirement goals and cash flow needs. Ultimately, I tailor each strategy to the individual’s career stage and life priorities, bringing clarity to complex choices and helping them confidently move toward financial independence.

Q: When you first speak with a Raytheon employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

Jeffrey: When I first meet with a Raytheon employee, my goal is to understand both their financial picture and what truly matters to them—because a great plan is built around purpose, not just numbers.

I typically start with questions like:

What areyour short-term and long-term goals—both personally and financially?

How confident do you feel about your current retirement strategy?

Are you aware of all the benefits available to you through Raytheon, and are you using them to their full advantage?

Do you have other financial priorities right now, like college savings, buying a home, or reducing taxes?

I also want to understand any life transitions on the horizon—whether it’s a career change, relocation, or family event—so we can anticipate and plan proactively.

These conversations often uncover opportunities to optimize their current benefit elections, adjust savings strategies, or build in tax-efficient planning. Ultimately, it’s about crafting a plan that’s aligned with their values, evolves with their life, and gives them peace of mind.

Q: Is there a particular benefit available to Raytheon employees you feel isn’t as well utilized or understood by employees as it should be?

Jeffrey: One particularly powerful but underutilized benefit available to Raytheon employees in 2025 is the ability to implement a backdoor Roth strategy through the RTX 401(k) Plan (RAYSIP).

Raytheon allows employees to make after-tax contributions beyond the standard pre-tax and Roth limits—up to the 2025 total contribution cap of $70,000 (or $81,250 for ages 60–63 with catch-ups). These after-tax dollars can then be converted to Roth within the plan, creating a significant opportunity for long-term, tax-free retirement growth. Despite its potential, many employees overlook this option due to its complexity or lack of awareness.

Another valuable and often overlooked benefit is the MetLife Group Legal Plan, still available in 2025. For a modest monthly payroll deduction (typically $16–$20/month), Raytheon employees can access estate planning services like wills, trusts, and powers of attorney at no additional cost. It also covers a wide range of personal legal matters—without deductibles or copays when using in-network attorneys.

Both benefits can make a meaningful difference when incorporated into a thoughtful, comprehensive financial strategy. Helping employees understand and confidently navigate these opportunities is a key part of the work I do.

Q: Beyond Raytheon employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients?

Jeffrey: Absolutely—beyond retirement savings, Raytheon offers several benefits that can significantly enhance a client’s financial well-being when integrated into a broader plan.

One standout is the Employee Stock Purchase Plan (ESPP), which allows employees to purchase RTX stock at a 15% discount through payroll deductions. This can be a powerful tool for long-term wealth accumulation, especially when paired with a disciplined diversification strategy.

Raytheon’s Employee Scholar Program is another exceptional benefit. It provides 100% reimbursement for tuition, books, and fees for approved degree programs—with no cap on the number of degrees. For clients looking to advance their careers or pivot professionally, this is a tremendous value.

The Health Savings Account (HSA), available with Raytheon’s high-deductible health plans, is also worth highlighting. Contributions are triple tax-advantaged, and Raytheon contributes to the account as well. For clients who can afford to pay current medical expenses out of pocket, the HSA becomes a stealth retirement account for future healthcare costs.

Lastly, the MetLife Group Legal Plan continues to be a cost-effective way for employees to access estate planning services like wills and trusts—services that are often overlooked but critically important.

These benefits often go underutilized simply because they’re not well understood. I help clients evaluate which ones align with their goals—whether that’s reducing taxes, funding education, or protecting their family’s future.

Q: For Raytheon employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

Jeffrey: For Raytheon employees nearing retirement, the transition from a steady paycheck to drawing income from various sources requires careful planning and coordination. I guide clients through a multi-step process that helps them feel confident and in control of this next chapter.

We start by mapping out all available income streams—401(k), pension (lump sum or annuity), Social Security, brokerage accounts, and any deferred compensation. From there, we build a tax-efficient withdrawal strategy that balances income needs with long-term sustainability.

One key opportunity is to take advantage of the ‘income valley’—the window between retirement and the start of required minimum distributions (RMDs). During this period, we often implement Roth conversions, harvest capital gains at favorable rates, or draw down taxable assets to manage future tax brackets.

We also evaluate healthcare coverage, including retiree medical benefits and Medicare timing, and ensure estate planning documents are up to date.

Ultimately, it’s about replacing the predictability of a paycheck with a well-structured income plan that aligns with their lifestyle, values, and legacy goals. I help clients make this shift with clarity and confidence—so they can focus on enjoying the freedom they’ve worked so hard to earn.

Q: For Raytheon employees who have managed their finances on their own to this point, what would you suggest they consider to help them decide if they should begin working with a financial advisor at this stage in their lives?

Jeffrey: For Raytheon employees who’ve done a great job managing their finances independently, the decision to work with a financial advisor often comes down to complexity and confidence. As they near retirement or experience major life transitions, the stakes get higher—and so does the value of having a second set of eyes.

I encourage them to consider a few key questions:

Are you confident in your retirement income strategy—including how and when to draw from your 401(k), pension, and Social Security?

Have you evaluated the tax impact of your decisions, including Roth conversions, RMDs, and capital gains?

Do you have a plan for healthcare costs, estate planning, and legacy goals?

Are you making the most of Raytheon’s more advanced benefits—like deferred compensation, the backdoor Roth strategy, or the ESPP?

Q: What are some of the unique financial planning challenges you commonly see among your clients who are Raytheon employees and how do you help them overcome these obstacles?

Jeffrey: Raytheon employees often encounter unique planning challenges that stem from the structure of their compensation, evolving retirement benefits, and the tax implications of various elections. One common issue is navigating the transition from legacy pension plans to cash balance plans following the merger with United Technologies. Many employees are unsure how to weigh lump sum versus annuity options, or how these fit into their broader retirement income strategy.

Another challenge is the underutilization—or mismanagement—of advanced savings opportunities like after-tax 401(k) contributions and in-plan Roth conversions. While Raytheon offers the ability to implement a backdoor Roth strategy, many employees either miss the conversion step or don’t understand the tax implications, which can lead to missed opportunities or unintended tax bills.

Deferred compensation planning is also a key area of concern, especially for higher-level employees. Elections must be made well in advance and are irrevocable, so aligning those decisions with future cash flow needs and tax brackets is critical.

Finally, equity compensation—such as RSUs and ESPP participation—can create concentrated stock risk and unexpected tax consequences if not managed proactively.

I help clients overcome these challenges by building integrated plans that coordinate all these moving parts. We model different scenarios, optimize tax strategies, and ensure that each decision—from pension elections to stock diversification—is aligned with their long-term goals. The goal is to bring clarity to complexity and help them make confident, informed choices.

Q: What questions do you recommend Raytheon employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

Jeffrey: I always encourage Raytheon employees to ask prospective financial advisors questions that go beyond investment performance. The goal is to find someone who understands the nuances of Raytheon’s benefits and can provide truly personalized guidance. Here are a few key questions to consider:

Do you have experience working with Raytheon employees or are you familiar with the RTX Savings Plan, pension options, and deferred compensation?

Do you act as a fiduciary at all times—and can you explain what that means in practice?

How are you compensated? Are there any commissions or product sales involved?

Can you help me with more than just investments—like tax planning, estate strategies, and benefit elections?

What is your process for building a retirement income plan that includes my 401(k), pension, Social Security, and other assets?

How do you stay up to date on changes to Raytheon’s benefits and the broader financial landscape?

What kind of ongoing support and communication can I expect from you?

These questions help uncover whether an advisor is not only technically competent but also aligned with your values, communication style, and long-term goals. It’s about finding a partner—not just a portfolio manager.

Q: Is there anything that comes up frequently in your initial meeting with Raytheon employees that surprises you?

Jeffrey: One thing that frequently comes up—and surprises both me and the Raytheon employees I meet with—is just how underutilized and complex their benefits package can be, especially for those who’ve spent years with the company.

Many are unaware of advanced planning opportunities like after-tax 401(k) contributions and in-plan Roth conversions (a backdoor Roth strategy), or they haven’t evaluated deferred compensation elections, which require early, irrevocable decisions that can significantly impact future cash flow and taxes.

Pension decisions are another common challenge—particularly for employees navigating the transition from legacy defined benefit plans to cash balance formats after the Raytheon–UTC merger. Choosing between lump sum and annuity options often comes with uncertainty and wide-ranging financial implications.

It’s also surprising how many employees have accumulated substantial retirement savings but haven’t yet mapped out a coordinated withdrawal strategy—one that aligns income sources like 401(k), pension, and Social Security while managing taxes across retirement.

Lastly, I often discover that clients are paying into the MetLife Legal Plan but haven’t taken advantage of the included estate planning services such as wills, trusts, and powers of attorney.

These realizations can be eye-opening—and they reinforce how valuable it is to work with someone who can integrate all these moving parts into a cohesive, personalized strategy.

Q: For highly compensated Raytheon employees and executives, are there any special benefits you believe it’s important to take into consideration when preparing their financial plan?

Jeffrey: For highly compensated Raytheon employees and executives, there are several specialized benefits that warrant close attention when building a comprehensive financial plan.

One of the most impactful is the RTX Compensation Deferral Plan, which allows eligible employees to defer salary, bonuses, and other compensation beyond IRS limits. This can be a powerful tool for managing taxable income and aligning cash flow with future retirement needs. Timing and structure are critical, as elections must be made in advance and are irrevocable.

Executives may also receive Performance Share Units (PSUs), Restricted Stock Units (RSUs), and Stock Appreciation Rights (SARs) through Raytheon’s Long-Term Incentive Plans. These awards come with vesting schedules, tax implications, and concentration risk—especially when combined with 401(k) holdings and ESPP participation. I help clients evaluate when to exercise, diversify, or hold based on their broader portfolio and tax strategy.

Additionally, Raytheon offers a Lifetime Income Strategy (LIS) within the 401(k) plan, which provides guaranteed income options. While this can be attractive for some, it may limit flexibility and preclude strategies like Net Unrealized Appreciation (NUA), so it’s important to assess fit on a case-by-case basis.

Finally, executives should consider supplemental disability insurance and legal benefits that go beyond standard offerings, especially given income levels that exceed base policy caps.

These benefits can be incredibly valuable—but only when integrated thoughtfully into a broader plan that considers taxes, timing, and long-term goals.

Q: Is there a particularly memorable experience or a moment you recall with a client who worked at Raytheon when you realized they have unique opportunities and circumstances when it comes to their financial planning needs?

Jeffrey: One particularly memorable experience was working with a long-tenured Raytheon engineer who was approaching retirement and had accumulated a significant balance across multiple benefit plans—including a legacy pension, after-tax 401(k) contributions, deferred compensation, and unexercised stock options.

What stood out was how unaware he was of the tax implications tied to each of these accounts. For example, he hadn’t yet initiated in-plan Roth conversions on his after-tax 401(k) contributions, which meant he was missing out on a powerful backdoor Roth opportunity. He also hadn’t considered how his deferred compensation payouts would overlap with required minimum distributions, potentially pushing him into a much higher tax bracket.

Through our planning process, we were able to model different income scenarios, optimize the timing of his pension election, and implement a multi-year Roth conversion strategy during his lower-income retirement window. We also helped him diversify out of concentrated RTX stock positions and take advantage of the MetLife Legal Plan to update his estate documents.

That experience reinforced how uniquely complex—and potentially rewarding—Raytheon’s benefits can be when integrated thoughtfully. It also highlighted the value of proactive planning, especially for employees who’ve done a great job accumulating assets but haven’t yet mapped out how to turn them into a sustainable, tax-efficient retirement income.

Get to Know Jeffrey Davis Financial Advisor for Raytheon Employees:

Are you a financial advisor who specializes in working with employees at Raytheon Technologies or another large company?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with employees at Raytheon Technologies or another large company. (Subject to availability and terms.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender ✅ Or request more information by email:

Quick Facts & Resources for Raytheon Technologies Employees

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

About the Author

Brian Thorp

Founder and CEO, Wealthtender

Brian and his wife live in Texas, enjoying the diversity of Houston and the vibrancy of Austin.

With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress.

Alyssa Dalbey, CPWA®, CFP® and Wealth Manager at Schultz Financial Group | Image Credit: Institute for Innovation Development

[While the history of single family offices take us from the major domus of ancient Rome, to the major-domo of great households in the Middle Ages, to the “superintendent” of rich families from the 14th to 18th centuries, it was not until 1838 that the House of Morgan ushered in the formation of one of the first modern family offices. This model was then also applied by the Guggenheim, Dupont, and Vanderbilt families.

Since the purpose of the family office was to serve the specific needs of a particular family’s wealth that could comprise multiple businesses, global properties, and complex assets, it is safe to say that there were as many different family offices as there were families that needed them. Some single-family offices became so well structured and effectively managed that they offered their services to a few other rich families creating the first multi-family office and providing an outsourced option versus building your own family office. But this was a very limited option among the wealthiest families.

Today’s technological and innovation revolutions have similarly created substantial wealth across many industries. Most maybe not to the extent of the dominating families of previous centuries that necessitated the uber-wealthy’s single family office haven. But an interesting evolution – driven by a comprehensive or holistic financial planning advisor movement – is driving the formation and growing access of multi-family office services from ultra-high-net-worth to high-net-worth clients and successful business owners.

To better understand this comprehensive financial planning movement and its emerging family office business structure, we reached out to Alyssa Dalbey, CPWA®, CFP® and Wealth Manager at Schultz Financial Group (SFG) – an independent RIA firm with a decades-long commitment to deepening client relationships by offering a unique integrated package of services to create a working partnership with their clients. This belief shaped their conscious firm development decisions to provide their clients with a more holistic and carefully integrated family and business wealth planning approach that covers what they term as the “Four Capitals of Wealth” – Financial Matters, Physical Well-being, Intellectual Engagement, and Psychological Space.

We asked her questions from a practice management and business development perspective to learn from the firm’s leadership mindset and experience on how they built their firm for stronger and more extensive wealth management engagements with their clients that go beyond just asset management.]

Hortz: Did the concept of a multi-family office structure come to mind as you were consciously choosing to expand the range of your services and working relationships with clients? When did you realize you were approaching a multi-family office structure?

Dalbey: Early on, we found ourselves working with high-net-worth individuals and business owners who started families. As these families and their businesses grew and expanded, the complexities of our wealth management relationships with them increased.

The decision to expand our range of services and working relationships was driven by the need to offer more holistic and integrated wealth management solutions, ultimately leading us to adopt a more comprehensive wealth management model. There was not a single moment in time that we realized we were operating under a multi-family office model. This growth and expansion of our services happened organically.

Hortz: From your experience, why do high-net-worth and successful business owners need a more comprehensive family office structure than traditional wealth management services?

Dalbey: In working with our clients, it became clear to us that high-net-worth (“HNW”) families, not just billionaires, require a family office service structure to manage the complexities of their wealth and ensure long-term financial security and well-being. A family office provides a centralized approach to wealth management, offering personalized services that address the unique needs of HNW individuals beyond just money. By consolidating these services, a family office helps streamline decision-making and enhances the efficiency of managing wealth.

Additionally, a family office offers confidentiality and security, compiling and protecting sensitive financial information. It provides continuity and stability, ensuring that wealth is preserved and transferred across generations. For families with diverse assets and interests, a family office acts as a trusted advisor, guiding them through financial and business decisions and helping them achieve their goals across time and generations.

Hortz: What services did you determine that a family office approach should provide?

Dalbey: By asking a lot of probing questions and listening intently to our clients, many made it clear that their goals were not solely about money. Over time we learned and compiled client concerns to a more expansive redefinition of wealth and a new client dialogue into the “Four Capitals of Wealth” – Financial Matters, Physical Well-being, Intellectual Engagement, and Psychological Space – which offer the following:

Financial Matters – we gather and analyze information from the client and their other advisors (such as their CPA, estate planning attorney, etc.), to develop customized investment strategies that incorporates investments (including alternative investments), detailed financial planning, thorough tax planning and optimization coordinated with the client’s CPA, estate planning, legal advisory relating to estate and business issues, risk management mitigated through insurance and other protective measures, and philanthropic advisory. Furthermore, we can share those plans with the next generation so that their children and grandchildren may be good stewards of the family’s wealth.

Physical Well-being – we provide clients with a subscription to the Tufts Health & Nutrition Letter, which has prompted clients to engage deeper in health-related discussions with our Physical Capital Resource Manager. We also provide access to articles and resources on diet & nutrition, health & fitness, and healthy recipes, and guide clients to the information that relates specifically to their Physical Well-being goals.

Intellectual Capital – is an invaluable asset, and we recognize that it evolves throughout life. As such, we help clients identify opportunities and resources to harness their natural desires and maximize their intellectual capital during their high-earning years. Then, we help them transform it to their next career, avocation or hobby using their personal skills and experience to positively impact their future.

Psychological Space – we work with clients to identify what brings them joy and how they can share that with others, whether that be family, friends, or their community. We also help clients identify how they want to contribute to society, as giving back can enhance psychological well-being. Legacy planning is another important pillar of our Psychological Space family office services.

Most importantly, we learned that the key differentiating service we could provide HNW clients was in carefully integrating all aspects of a family’s needs and goals which informed all our decisions and recommendations. Thereby, we were given the ability to truly go beyond the traditional euphemisms of “personalized” services into uniquely tailored and bespoke solutions. The resulting Four Capitals Plan we develop together with our clients serves as the foundation for an ongoing, interactive, and personal relationship. It helps us understand our clients holistically and serve them in a meaningful way.

Hortz: How are family office services different for business owner clients?

Dalbey: While there are many areas of need for HNW families, this can be heightened for the business owner that carries the weight of the business and family livelihood on his or her back. The emotional, motivational, physical, and psychological forces need to be aligned and managed as well as the financial cash flow.

This entails even more in-depth “Four Capitals of Wealth” management and a family office structure to handle complex business needs that can also include human capital management, property management, diverse business assets, intellectual property/trademark protections, retirement/benefits programs, business/personal tax planning optimization, succession planning, eventual business sale, family/business balance, etc.

Family office services can bring together a team of highly skilled professionals, including tax specialists, legal experts, and investment bankers. Business owners benefit from this diverse range of expertise, receiving comprehensive and informed advice.

Hortz: How is investment management different for family office clients?

Dalbey: Investment management for a family office differs significantly from traditional investment management due to the unique needs and goals of high-net-worth families. Here are some key distinctions:

Family offices tailor investment strategies to the specific objectives, risk tolerance, and time horizons of the family. This personalized approach ensures that the investment portfolio aligns with the family’s overall financial plans and legacy goals. This may include separating the portfolio out into different sub-portfolios, each with their own goals and objectives.

One of the significant differences in investment management for family offices is the inclusion of alternative investments including private equity, private credit, hedge funds, commodities, real estate, art and collectibles. HNW individuals can also access exclusive investment opportunities that may not be available to the general public. This includes private deals, co-investments, and bespoke investment vehicles tailored to the family’s needs.

Family offices can also play a crucial role in educating family members about investment principles and involving them in the decision-making process. This helps ensure that future generations are prepared to manage and preserve the family’s wealth while also carrying on the family’s mission and values. We find great joy in working with the multiple generations of our clients’ families.

Hortz: Can you share with us a brief client case study that demonstrates the power of holistic financial planning and the family office model?

Dalbey: We have a business-owner client that was referred to our firm for our wealth management and business consulting services by an existing client. This business owner is single and owns and operates a successful business that is cash flow positive and has been in existence for over ten years.

Despite receiving a few million dollars of cash flow every year, this client lacked a personal investment portfolio, retirement savings, and college savings for his children. Additionally, his business had no formal operational procedures, career paths, or incentive plans. We worked with the client to develop a cash flow management plan that would satisfy both business and personal goals by accumulating investment savings in accounts for his own future, the future expansion of his business, and his children’s college education.

We also consulted with him and his management team to write job descriptions, create career paths, develop a new employee training program, put together an incentive plan, and implement an operational checklist for ensuring the business consistently delivers the quality of goods and services customers have come to expect.

We have brought in personal and business attorneys to address business succession issues and estate planning. We have consulted with bankers to establish long-term banking relationships and secure financing for business expansion. We also coordinated tax planning with both his CPA and bookkeeper.

Hortz: Are prospects that you are seeing aware of and seeking family office services or is there more education needed to explain this service model?

Dalbey: There are several reasons why many HNW clients might not be aware of family office services:

Lack of Awareness and Education – Family office services are often not widely advertised or discussed in mainstream financial education. Many HNW individuals may not be aware of the existence or benefits of family offices simply because they have not been exposed to this information. Family office services are still relatively new in being accessible for the HNW individuals and business owners as these services were exclusive to the ultra HNW families for a long time.

Traditional Financial Services – Many HNW individuals rely on traditional financial services provided by banks, brokerage firms, and independent financial advisors. These traditional services may meet their needs to a certain extent. However, once a family’s net worth starts to exceed $10-$15 million and they start prioritizing things like family legacy and business succession, family office services are critical to meeting their needs.

Limited Marketing and Outreach – Family offices often operate with a low profile and rely on word-of-mouth referrals rather than extensive marketing campaigns. This limited outreach means that potential clients may not come across family office services unless they are specifically looking for them or are referred by someone in their network.

Focus on Business Interests – For business owners, the primary focus is often on managing and growing their business. They may not prioritize or even consider the additional benefits that a family office can provide in terms of personal wealth management, succession planning, and risk management.

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.

You’re working hard, saving for retirement, and maybe even helping your kids launch—but now your parents need help, too. For many couples in their forties and fifties, the financial squeeze is real.

It’s a season of life that can feel both meaningful and overwhelming. You want to be there for your parents, to honor everything they’ve done for you. At the same time, you’re navigating your own financial goals, career demands, and family responsibilities. It’s not about choosing one priority over another—it’s about finding a path forward that supports your loved ones across generations with compassion and clarity.

When you’re balancing elder care and retirement planning, it’s easy to feel stretched thin—financially and emotionally. The good news? With thoughtful planning, you can care for your family and stay on track for the future you’ve worked so hard to build.

Remember to Put Your Oxygen Mask on First

This isn’t just about the rising cost of care; it’s also about the emotional weight of setting financial boundaries with the people who raised you. That can be hard, even when you know it’s what’s best for everyone in the long run.

Supporting your parents doesn’t mean covering every cost yourself. Instead, look for ways to help them make the most of the resources they already have, whether that’s retirement income, home equity, or other assets. The goal is to preserve their dignity and quality of life while protecting your own financial stability.

As the saying goes, you need to put your own oxygen mask on first. Prioritizing your financial well-being isn’t selfish. It’s a necessary step toward being able to care for others with confidence and resilience, both now and in the years ahead.

Consider a Rental Setup That Works for Everyone

There often comes a time when the family home simply doesn’t fit anymore. Perhaps it has stairs that have become difficult to navigate or bathrooms and entryways that aren’t designed for changing mobility needs. The yard and upkeep may have once been a source of pride, but now feel overwhelming or even unsafe. And if your parents live far from family, especially potential caregivers, distance can add layers of stress and complication during an already challenging season of life.

In these situations, a move may be the best solution, whether to bring your parents closer to family or simply to place them in a home that better suits their needs. One option to consider: purchasing a small condo or townhouse and setting it up as a rental. Rather than gifting the home outright, you can charge fair market rent, ideally covered by your parents’ Social Security or other retirement income. This approach helps maintain their independence, eases day-to-day challenges, and gives you a long-term asset that may come with potential tax benefits.

Use Existing Home Equity Wisely

If your parents already own a home, you may be able to strategically leverage the equity it’s built up over time (especially considering the rapid rise in home valuations in recent years). As they age, consider how the equity in that home can be used to provide for their future care needs.

With your parents and the help of an advisor, explore potential options including:

Home equity loan or line of credit (HELOC)

Selling and downsizing

Possibly moving and renting the home for extra income.

Home equity can be used to fund part-time care, pay for home modifications, or cover other expenses.

Tapping into your parents’ existing equity also helps preserve more of your own savings. Rather than covering care costs out-of-pocket, you’re using the assets your parents have already built to support their quality of life.

Use Other Resources Strategically

When deciding which funds to draw from first, try to follow a thoughtful order that balances tax efficiency with long-term planning.

For example, start by making full use of your parents’ guaranteed income sources, such as Social Security or pension payments. These benefits typically can’t be passed on and are meant to support their needs during retirement, so it makes sense to use them first before tapping into other savings or investments.

Withdrawals from retirement accounts like IRAs or 401(k)s are taxed as ordinary income. However, depending on your parents’ overall income in retirement, they may fall into a lower tax bracket than you, especially if you’re still working. Strategically drawing from their accounts now could reduce the long-term tax burden on your family and preserve more of your own assets.

If you eventually inherit your parents’ tax-deferred retirement accounts, you could face a significant tax bill. Under current rules, most non-spouse beneficiaries must empty inherited IRAs or 401(k)s within 10 years—and all withdrawals are treated as taxable income. If you’re in your peak earning years when this happens, those extra distributions could push you into a higher tax bracket.

Rather, it may be a more tax-efficient option for your parents to spend those funds on their own needs now. Meanwhile, other assets—like taxable investment accounts or real estate—that may qualify for a step-up in basis at death can be preserved as part of a more tax-efficient legacy plan.

What to Do When Assets Are Limited

Not every parent enters retirement with a cushion of savings, home equity, or reliable income beyond Social Security. When resources are tight, it’s important to explore alternative strategies that can still provide the care and support they need.

In some cases, Medicaid may offer essential help with long-term care costs. However, eligibility comes with strict income and asset limits. To navigate this, families sometimes use tools like irrevocable trusts to preserve assets while still allowing parents to qualify for benefits. The key is timing: these strategies often need to be in place at least five years before care is required, due to Medicaid’s look-back rules.

If your family is in this situation, consider consulting a financial advisor or elder law attorney. With the right guidance and early planning, you can help ensure your parents receive the support they need, without creating additional financial strain on yourself or your family.

Don’t Neglect Your Own Needs

It’s easy to fall into the mindset that you need to do it all, especially when you’re caring for an aging loved one. But if supporting your parents starts to derail your retirement savings, the entire family could end up with fewer options down the road. You’re not helping anyone if you end up financially vulnerable in your own later years.

Keep contributing to your own investment accounts. Have enough cash on hand for upcoming needs. And whenever possible, rely on your parents’ resources, rather than your own, to cover their expenses. Protecting your financial future is part of protecting your family’s stability.

Remember, You Don’t Have to Do It Alone

Balancing your own goals with the needs of aging parents is no small task. It takes time, heart, and a plan.

Congratulations! Earning a Wealthtender Voice of the Client Award™ is an achievement worth celebrating. We created this guide to help you maximize the value of your award.

Increase visibility in AI tools (Answer Engine Optimization)

Reinforce client loyalty

Achieve a higher business valuation

Your award offers more benefits than you think

Consumers preparing to hire financial advisors are looking for signs that they can trust the advisors they hire. When they look beneath the surface of your Voice of the Client Award to discover how your recognition was earned, they will find real clients sharing stories about their experiences working with you. Unlike other award programs with criteria heavily weighted on a firm’s size or revenue growth that could raise eyebrows among skeptical consumers, even the name of your “Voice of the Client” award conveys that this award is special.

Increasing Client Loyalty & Referability

Beyond the impression your Voice of the Client Award makes in the minds of prospects, your award also reminds your current clients that they’re in good hands. Especially among clients who took the time to write a review about their experience working with you, they will take pride in knowing the feedback they shared contributed to your recognition for an award they believe you deserve.

Other clients who haven’t yet written a review may be more inclined to do so as they learn of your award and feel greater validation that choosing you as their advisor was a smart move. Ultimately, your award reinforces to all of your clients that they made a wise choice in hiring you, increasing their loyalty as well as the likelihood that they will refer you to family, friends and others in their network.

Enhancing Your Visibility in Search Engines and AI Tools

Another benefit of receiving a Voice of the Client Award includes strengthening your SEO (Search Engine Optimization) to rank higher in traditional search engines like Google, improving your AEO (Answer Engine Optimization) to raise your visibility in AI tools like ChatGPT, Perplexity, and Gemini, and even aiding your ZCO (Zero-Click Optimization) efforts where traditional search engines display AI summaries above all other search results.

Motivating Your Team and Boosting Morale

Your award also helps you recruit and retain top-caliber employees who prefer to work for an organization that’s been recognized for exceptional client service and where they feel they’re part of a winning team. Celebrating your award as a team boosts morale and motivates your staff to continue delivering a client experience that sets your firm apart.

For a more complete discussion regarding the regulatory disclosures required when promoting third-party ratings, please read this article.

Please remember, you must first sign a licensing agreement with Wealthtender and agree to the terms of use to display the Wealthtender award logo in digital or print format beyond your Wealthtender profile page. This article is provided for educational purposes and is not intended to replace the guidance of your compliance officer/consultant. Please speak with your compliance counterpart before getting started promoting your award. Questions? Contact yourfriends@wealthtender.com. We’re always happy to help.

Impactful Ways to Promote Your Voice of the Client Award™

Just below, you will discover several practical ways you can promote your award to convert more prospects into clients, improve client retention, strengthen your visibility online, enhance your company culture, and ultimately increase the value of your business.

1. Display Award on Your Wealthtender Profile

Shortly after accepting your award from Wealthtender, your Wealthtender profile will display the award logo with the disclosures necessary to satisfy SEC and FINRA requirements. Your award is displayed with coding that helps search engines and AI tools validate your status as an award recipient. This can lead to you appearing more prominently and frequently when prospects are searching for advisors or evaluating the advisor names on their short list. No action is required on your part. Wealthtender staff will set this up automatically for you.

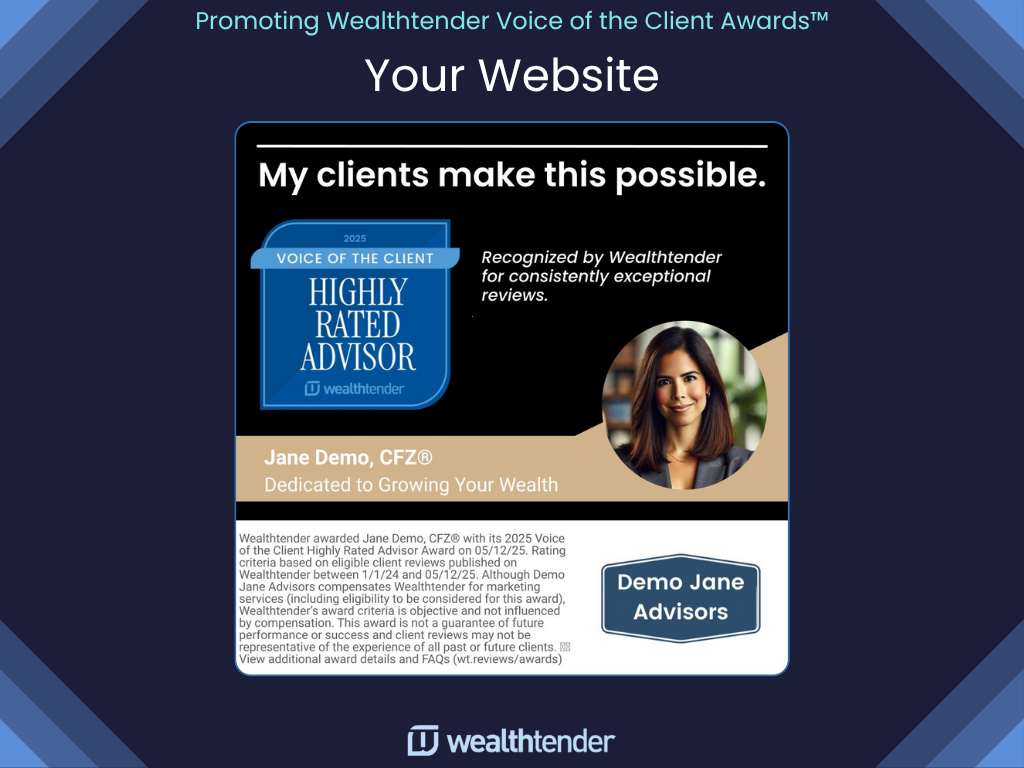

2. Display Award on Your Website

Your Wealthtender Voice of the Client Award is not only a meaningful recognition of the outstanding client experience you deliver, it’s also a highly effective trust signal that can influence prospects at “moments that matter” when they’re deciding if they should contact you or another advisor. Your website is often one of the final touchpoints for prospects deciding whether you are the right financial advisor or firm that can meet their needs. Prominently displaying your award on your website can help strengthen your credibility and differentiate you from competitors.

➡️ Why This Is Important:

Builds Immediate Trust: Awards based on authentic client feedback resonate strongly with prospects. Seeing your Wealthtender recognition demonstrates that your clients have enjoyed their experience, reinforcing confidence among prospects in choosing you over other advisors.

Enhances First Impressions: Among many prospects, your website serves as a digital billboard they will quickly scan upon their initial visit. The inclusion of third-party recognition instantly elevates your credibility, places prospects at ease, and helps ensure you land on their short list.

Supports SEO & AI Discovery: As search engines and AI-powered tools like ChatGPT and Gemini increasingly look for professional credentials, online reviews and awards when deciding which advisors to show in search results, displaying your award on your homepage, bio page and contact pages may increase how frequently and prominently you appear in search results.

➡️ How to Implement:

Compliance Tip: When displaying the award logo on your website, remember to include the disclosures required for regulatory compliance. These disclosures can be added as a text block near the award logo, or consider using an image design (like the example below) that incorporates disclosures alongside the award logo.

Homepage Feature: If you have earned a Highly Rated Firm award, place the Wealthtender Voice of the Client Award logo prominently on your home page where visitors will see it as they scan to learn more about your firm and services. Or add a section to your homepage featuring the advisors who have received a Highly Rated Advisor award. Consider adding a link to your Wealthtender profile or the testimonials page on your website where prospects can “Read the client reviews that helped us earn this award“.

Sample design created in Canva that includes regulatory disclosures.