Discover financial advisors trusted by residents of Bellingham, Washington in the only local directory featuring 5-Star Certified Advisor Review™ recipients and Wealthtender Voice of the Client Award™ winners—recognition earned for exceptional client feedback. Compare fiduciary, fee-only advisors, CFP® professionals, and specialists to find the right fit for your unique financial needs.

Whether you have lived in Bellingham for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Bellingham featured on Wealthtender you may want to add to your shortlist.

Featured Bellingham Financial Advisors

As you prepare to interview financial advisors in Bellingham who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Bellingham

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Bellingham.

The Benefits of Hiring a Financial Advisor in Bellingham

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Bellingham, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Bellingham? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Bellingham Financial Advisor

Before hiring a financial advisor in Bellingham, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

You work hard to earn money, save diligently, and invest for the future. But do you actually know what your financial picture looks like right now, across every account you own?

Knowing your net worth in real time isn’t just satisfying; research consistently shows that people who actively track their wealth make better financial decisions, stay on budget more reliably, and build toward financial goals faster. Whether you’re just starting out or managing a complex portfolio across multiple brokerages, the right wealth tracker can be the single tool that brings everything into focus.

Pearson’s Law states: “When performance is measured, performance improves. When performance is measured and reported back, the rate of improvement accelerates.”

So, if you’re working toward a financial goal, tracking your progress will help you achieve it quicker! The hard part is finding an efficient way to do it.

That’s where wealth tracker apps and websites come in to help you know your net worth and achieve your goals. These useful tools aggregate info from your various accounts and allow you to monitor (and manage) everything from your income and expenses to your investments – all from a single dashboard. Making informed financial decisions and hitting those big money goals becomes much easier as a result.

Want to find one that’s right for you? Keep reading to discover 7 of the best wealth trackers available today.

Key Takeaways

1

Tracking your net worth accelerates wealth-building — not just awareness.

Research supports what Pearson’s Law describes: when you measure financial performance and regularly review it, improvement accelerates. Wealth tracker apps automate the aggregation of your accounts into a single dashboard, making consistent monitoring effortless rather than a manual chore.

2

The best wealth tracker depends on what financial visibility you actually need.

Beginners benefit most from budgeting-first tools like YNAB, while those who want a comprehensive view of spending and net worth together will find all-in-one platforms like Monarch Money or Empower ideal. Advanced investors with complex, diverse portfolios may prefer the deeper tracking capabilities of Kubera. Knowing what you need most — budgeting, net worth tracking, investment analytics, or all three — is the right starting point for choosing a tool.

3

Free tools can get you started, but paid options deliver meaningfully more insight.

Several apps on this list offer free tiers — including Empower and PocketSmith — but their most powerful features (investment analytics, multi-account sync, long-range financial projections) typically require a paid plan. Given that most premium wealth trackers cost less than $150/year, the ROI on better financial decisions usually far outweighs the subscription cost.

What Is a Wealth Tracker App and Why Does It Matter?

A wealth tracker app is a digital tool that connects to your financial accounts (e.g., bank accounts, investment portfolios, retirement funds, loans, and more) and aggregates everything into a single, unified dashboard. Instead of logging into five different apps or building a spreadsheet from scratch, you get a real-time snapshot of where you stand financially, including your total assets, liabilities, and net worth.

Net worth is one of the most important numbers in your financial life, yet most people have only a vague sense of what it actually is. Your net worth, the difference between everything you own and everything you owe, is the clearest measure of whether your financial life is moving in the right direction. Wealth tracker apps make that number visible, trackable, and actionable rather than something you calculate once a year (if at all).

Beyond the snapshot, the best wealth tracker apps and websites reveal patterns you’d otherwise miss: spending categories quietly eating into your savings, investment accounts drifting out of alignment with your goals, or retirement projections that suggest you need to course-correct sooner than you thought. Used consistently, these tools don’t just tell you where you are, they help you get to where you want to be.

Want to track your wealth and invest at the same time? Try Betterment, the “all-on-one financial dashboard.” The app’s a roboadvisor – a digital financial advisor that manages your investing accounts (Betterment restricts you to investing in exchange-traded funds, or ETFs) depending on your goals and risk tolerance. However, you can also sync your bank accounts to enjoy a birds-eye view of your finances, set goals, and track your saving/investing progress.

There are two service tiers: Digital and Premium. Choose the former if you’re on a budget and investing less than $100k. There’s no minimum to get started, and the annual advisory fee is 0.25%.

2. Empower

Empower (previously called Personal Capital) is another popular and widely-used wealth tracker that comes highly recommended online. Empower is powerful, versatile, and has many impressive free-to-use tools – as well as a paid wealth management service for those who need/want it.

After signing up, you can link your financial accounts (e.g., bank, credit cards, savings, loans, investing, retirement, etc.) to get a real-time look at your net worth. You can then monitor cash flow, set budgets, and leverage many other special tools, including a Savings Planner, Retirement Planner, and Fee Analyzer. The fact you get so much for free is a huge selling point.

EmpowerWhatever your financial happiness looks like, let’s help get you there.

Self-billed as “the world’s most modern wealth tracker,” Kubera is an advanced portfolio-tracking app that offers a near-limitless number of bank connections and detailed insights on your investments.

It’d be ideal for someone with a large and diverse portfolio – even if it includes international holdings. Kubera tracks all of your assets in one place and shows their current and estimated resale value, making monitoring your net worth over time straightforward.

Take note, though: unlike other wealth trackers with a diverse range of tools, Kubera has a heavy investment focus. Likewise, there’s no free plan. Once the 14-day $1 trial is over, you’ll pay $150 per year.

4. Monarch Money

If Mint’s shutdown left a gap in your financial toolkit, or if you’ve never found a personal finance app that truly brings everything together, Monarch Money may be exactly what you’re looking for. Launched in 2021 and now widely regarded as the leading all-in-one personal finance platform in the post-Mint era, Monarch combines account aggregation, net worth tracking, budgeting, and investment monitoring in a single, polished dashboard.

What sets Monarch apart is its balance of depth and usability. Connect your bank accounts, credit cards, investment portfolios, loans, and retirement accounts, and you get a real-time picture of your complete financial life, not just one slice of it. The budgeting tools are intuitive without being rigid, the net worth tracker updates automatically as balances change, and a collaborative feature makes it particularly well-suited for couples managing finances together.

Monarch is available on both iOS and Android and is priced at $99.99 per year (or $14.99 per month billed monthly). There’s no permanent free tier, but a 30-day free trial gives you time to evaluate it before committing. For anyone who wants a comprehensive, beautifully designed tool that moves beyond basic budgeting into genuine wealth visibility, Monarch Money belongs near the top of your list.

5. PocketSmith

PocketSmith is an easy-to-use personal finance software that helps users with money management, cash flow forecasting, and personal budgeting.

There’s a lot to like, but one highlight is the info it provides on your future financial situation based on your current spending habits and earnings. This glimpse of what’s to come should compel positive financial action in the present.

The fact that PocketSmith offers a free plan is a bonus, although its features are quite limited. If you wish to connect your accounts to a single dashboard (for the most accurate wealth tracking) and enjoy financial projections well into the future, you’ll need to pay for a premium plan.

Image Credit: Depositphotos.

6. Tiller

Calling all spreadsheet fans and aficionados! Tiller could be the best wealth tracker for your needs. Like Microsoft Excel on steroids, this tool syncs to your financial accounts and imports real-time data to robust, highly customizable spreadsheet templates. That means no more manual data entry – unless you choose to edit certain fields or set custom rules!

Among other elements, the basic template offers a net worth tracker and a breakdown of your annual budget. However, many others are available, such as a template for retirement planning and another for debt reduction. Try Tiller for free on a 30-day trial, after which you’ll pay $79 annually.

7. YNAB

Short for “You Need a Budget,” YNAB is a fantastic tool that helps users budget, pay down debt, and manage money more effectively. It’s a great wealth tracker for beginners, with a program that revolves around four basic rules:

Give every dollar a job – be intentional with money, allocating everything you earn to specific expenses based on your financial priorities.

Embrace your true expenses – handle larger but less frequent expenses more easily by breaking them into smaller bills that you save for each month.

Roll with the punches – forget rigid budgets and simply move money from less important budgeting categories when you overspend elsewhere.

Age your money – spend less than you earn, watch your money accumulate, and start buying things today with money you earned in the past.

After a ~30-day free trial, you’ll need to pay for a subscription. This costs $14.99 per month or $98.99 per year.

Choose From This List of the Best Wealth Trackers to Know Your Net Worth

As Pearson’s Law points out so eloquently, tracking your progress is crucial to moving in the right direction and achieving goals sooner rather than later. That’s why it pays serious dividends – sometimes quite literally – to use a wealth tracker in your bid to budget, save, and invest as effectively as possible!

If you’ve been hunting for the best tracking tool, we hope this list has helped. Whether you’re an advanced investor with a vast and diverse portfolio or someone brand new to the pursuit, there should be a service here to suit your needs.

Author Bio

Danny Newman is a nationally syndicated freelance writer with a focus on travel. MSN feed and Associated Press bylines. Danny is a digital nomad from the UK who’s been traveling full-time since 2018. Learn More About Danny.

Find Financial Advisors on Wealthtender

📍 Click on a pin in the map view below for a preview of financial advisors who can help you reach your money goals and enjoy a comfortable retirement with a personalized plan. Or choose the grid view to search our directory of financial advisors with additional filtering options.

Do you have questions about your financial future? Find a financial advisor who can help you enjoy life with less money stress by visiting Wealthtender’s free advisor directory.

Whether you’re looking for a specialist advisor who can meet with you online, or you prefer to find a nearby financial planner, you deserve to work with a professional who understands your unique circumstances.

Have a question to ask a financial advisor?Submit your question and it may be answered by a Wealthtender community financial advisor in an upcoming article.

–

Do you already work with a financial advisor? You could earn a $50 Amazon Gift Card in less than 5 minutes. Learn more and view terms.

This article originally appeared on Wealthtender. To make Wealthtender free for our readers, we earn money from advertisers, including financial professionals and firms that pay to be featured. This creates a natural conflict of interest when we favor their promotion over others. Wealthtender is not a client of these financial services providers.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

April 20, 2026

If you’ve been watching AI dominate headlines and wondering whether you’re positioned to actually benefit from it, you’re not alone. Most high-income investors have exposure to AI through a handful of large-cap tech stocks. That’s a start, but it’s a narrow slice of one of the most significant economic expansions of our lifetime. The global AI market is on track to grow from roughly $376 billion this year to more than $2.4 trillion by 2034. The opportunity isn’t just in the companies everyone already owns.

Most investors are still playing the same crowded trade. NVIDIA, the dominant force in AI computing, has become the default bet, with Wall Street analysts continuing to raise the ceiling. Consensus estimates project Nvidia’s revenue to jump roughly 48% in fiscal 2027, and some analysts believe the stock could approach double its current price if earnings growth accelerates as expected. The enthusiasm is understandable. North America alone captured nearly one-third of the global AI market in 2025, and this giant sits squarely at its center.

But here’s the question serious investors should be asking: if enthusiasts already own Nvidia, where’s the edge?

For example, cloud deployment now accounts for more than 71% of the AI market share, growing at a projected rate of 30.7% annually. And the infrastructure powering that cloud buildout is where the real leverage may lie. The AI opportunity goes beyond computing itself. It’s the physical and digital backbone that makes an entire ecosystem operate at scale: data centers, power supply, networking, and cooling. These are the unsexy picks that investors aren’t always talking about at dinner parties, which might be exactly why they’re worth a closer look.

AI Runs on Power, and That’s a Problem

Once you start looking beyond the headlines, one constraint becomes hard to ignore: AI doesn’t just run on innovation; it runs on electricity.

Every query, model, and automation tool relies on data centers working around the clock. And those facilities are power-hungry in ways most people haven’t thought about. A typical AI-focused data center consumes as much electricity as 100,000 households annually, and the largest ones currently under construction are expected to use 20 times that amount. U.S. data centers consumed 183 terawatt-hours of electricity in 2024, more than 4% of the country’s total, and that figure is projected to more than double by 2030.

According to Bloomberg, a confluence of factors is placing significant strain on power grids worldwide, creating a tangible drag on economic growth. And according to Pew Research, everyday Americans are shouldering the cost in their power bills. In the PJM electricity market, which stretches from Illinois to North Carolina, data centers contributed to an estimated $9.3 billion increase in capacity market pricing.

I’ve been paying attention to this for a while.

There’s genuine debate about how to solve the energy problem, and some of it gets political fast. But set the politics aside, and the underlying dynamic is straightforward: demand for a critical resource is outpacing the infrastructure supporting it. That gap is where investment opportunities tend to emerge.

What “Investing in the Grid” Actually Means

When I talk about investing in the grid, I’m not talking about chasing a theme or picking the next AI stock. I’m talking about owning the assets that make AI possible. That includes data centers, power generation, transmission infrastructure, and fiber networks.

These are physical, capital-intensive assets built to support sustained, long-term demand. And the scale of that demand is hard to overstate.

McKinsey estimates that by 2030, data centers will require $6.7 trillion in cumulative capital investment worldwide to keep pace with AI-driven compute needs, spread across real estate developers, energy providers, semiconductor firms, and cloud operators. Utilities and energy providers alone face an estimated $1.3 trillion in AI-related capital requirements.

If you’ve invested in commercial real estate, this asset class should feel familiar. Data centers are increasingly treated as a specialized form of real estate — physical buildings with long-term leases, mission-critical tenants, and predictable cash flows. A 2025 survey by CBRE found that 95% of major investors worldwide plan to increase their allocations to data centers, with 41% planning to commit $500 million or more in equity, up from 30% the year prior. Vacancy rates in the sector finished 2025 at a historic low of 1% for the second consecutive year, with 92% of capacity currently under construction already pre-committed by tenants.

The appeal is structural. These are long-duration, hard assets — the kind where demand isn’t speculative but is driven by an accelerating, durable tailwind. AI doesn’t run on software alone. It runs on land, steel, power lines, and cooling systems. That’s the investment conversation worth having.

I encourage clients to take a disciplined approach and acknowledge what we don’t know. Researchers at the World Resources Institute point out that modeled projections for data center energy use by 2030 range from 200 to over 1,050 terawatt-hours per year, which is a pretty staggering spread. Some experts have also warned that utilities are being flooded with speculative grid connection requests, which may be distorting load forecasts.

The investment case for infrastructure isn’t built on assuming the most aggressive projections are right, but on recognizing that even the conservative ones point to a significant and sustained build-out, and that the physical assets required to support it will need to exist regardless.

Why the Real Action Is in Private Markets

These opportunities aren’t readily accessible to everyone. Most of the meaningful investment in AI infrastructure isn’t happening in the public markets, and there’s a structural reason for that.

Large-scale data centers, energy systems, and digital networks require significant capital, long development timelines, and patient ownership. These are conditions private markets are built for, and institutional conviction is growing.

The World Economic Forum puts the scale of opportunity in sharp focus. Meeting the world’s infrastructure demand will require $106 trillion in investment by 2040, spanning energy, digital, and transportation systems. Private investment plays a critical role, as public funding alone falls well short.

For high-income investors, access to these markets has improved meaningfully in recent years. But access isn’t the strategy. As I’ve written before, private credit and infrastructure funds can generate steady cash flow even when public markets struggle, and that’s exactly the kind of characteristic that belongs in a long-term, disciplined wealth plan. The trade-offs around liquidity, structure, and complexity are real, and they deserve a direct conversation. That’s always where we start.

What to Watch Out For

This is where I usually slow things down.

Private infrastructure and similar investments can be a good fit, but they come with real trade-offs.

Liquidity is one of the biggest. You’re not buying something you can sell tomorrow; you’re committing capital for years, and that needs to align with your broader plan. As I’ve noted in past articles on private investments, these structures often involve lock-up periods and limited access to funds, which can be challenging when flexibility is needed.

Manager selection is just as important. Two funds may both be labeled “infrastructure,” but have very different strategies, risk profiles, and outcomes depending on how they’re built and managed. Not all opportunities are created equal.

I’ve seen investors get pulled in by a compelling theme without fully understanding how the investment works — how returns are generated, what assumptions are being made, and how long capital is tied up. That’s why the focus should always be on fundamentals. If we can’t clearly answer those questions, we don’t move forward.

A Different Way to Think About AI Investing

This isn’t about chasing AI hype or trying to pick the next winner. It’s about understanding where durable, long-term value is being built and whether those opportunities belong in your portfolio. If you’re curious how this type of investment could fit into your broader plan, that’s a conversation worth having.

You’ve both managed money successfully before. You’re professionals, homeowners, and financially stable. So why does talking about money together feel so much harder than it should?

In blended families, money isn’t just financial—it’s relational. Each of you brings financial beliefs shaped by different experiences: how you were raised, what your first marriage taught you, what felt safe or risky during the years you were on your own. These beliefs run deep, and they don’t always surface until you’re making decisions together.

The challenge isn’t that one person’s approach is right, and the other’s is wrong. It’s those assumptions about fairness, responsibility, and what money should do that often go unspoken until a decision forces them into the open. When that happens, what looks like a disagreement about numbers is actually a clash of unexamined values.

Traditional financial planning assumes alignment and moves quickly to strategy. But in blended families, that sequence gets it backward. The hard part isn’t the math—it’s the conversations that clarify what you’re building together. When those conversations happen first, the financial decisions become clearer because you’ve defined the direction.

Understanding What Drives Your Financial Choices

In any relationship, you don’t want to lose sight of who you are as an individual. While marriage calls two people to come together as a strong partnership, it also requires honoring each person’s unique experiences, perspectives, and priorities.

Examining your money values helps you do exactly that. It clarifies what drives you financially and reveals the motivations behind both your best decisions and your most challenging ones. Someone who experienced financial instability in their first marriage might prioritize emergency savings above everything else. Another person who managed fine as a single parent might feel more comfortable taking calculated risks or spending on experiences today.

Neither perspective is right or wrong. They’re protective responses to different stories.

But in blended families, those protective instincts can collide in unexpected ways. What feels like financial caution to one spouse can feel like resistance to the other. What looks like generosity might feel like favoritism. Understanding your own values gives you the language to explain what’s driving a decision and helps your spouse see it as protection, not rejection.

When you can name what money means to you, conversations shift from defending positions to understanding each other.

Bringing Your Money Values Into the Open

Once you understand what drives your own financial choices, the next step is harder: sharing those beliefs with your spouse, and creating space to hear theirs.

In blended families, this isn’t a conversation about budgets or account structures. It’s about surfacing the assumptions you’ve both been carrying: what feels fair, what feels threatening, what you’re protecting, and what you’re afraid of repeating from your first marriage.

You’re navigating questions with no easy answers: How do we balance supporting your kids and mine fairly? What happens to assets you brought into the marriage? Should inheritance stay separate or become shared? What feels like protection to you but feels like distrust to me?

There’s emotional math at play—invisible calculations about loyalty, fairness, and what each of you promised yourself you’d never do again. These don’t show up on a spreadsheet, but they shape every financial decision you make together.

Traditional financial planning skips this step. It assumes alignment and moves straight to strategy. But in blended families, when assumptions go unspoken, they don’t disappear. They build consequences that surface years later as conflict or unintended outcomes.

Start by naming what money means to you and what shaped that belief—not what you think you should say, but what’s actually true. Maybe you’re still carrying fear from your first marriage. Maybe you feel protective of your kids in ways that are hard to explain. Your spouse’s perspective will be different, and that’s not a problem to solve immediately. The work here is to understand, not to convince.

Money conversations can get emotional. It’s tempting to label one partner as “bad with money” or overly cautious. But those labels shut down understanding. Don’t assume you know what drives your spouse’s choices without asking. And don’t treat your own perspective as fact while dismissing theirs as opinion.

Where you find common ground, acknowledge it. Where you see differences, don’t ignore them. The danger isn’t disagreeing—it’s leaving assumptions unspoken.

This conversation is how you move from two separate money stories to one shared direction. When you surface what you’re each building toward, the financial decisions become clearer because you’ve defined where you’re going first.

Start Creating Intentional Alignment

You don’t have to agree on every financial detail throughout your marriage. Rather than aim for perfection, build a shared understanding of how your values will be expressed in real life.

For example, you might need to clarify expectations around spending, saving, supporting children, and charitable giving. As a blended family, you may need to think deeper about inheritance planning, financial responsibilities for children from previous relationships, or how household expenses will be shared.

Understand that you won’t be perfectly aligned at every step, and that’s okay. The point is to be more intentional with your decisions and come from a place of understanding. When you know how you both feel about money and what shaped those perspectives, you create a shared sense of direction. That direction becomes your North Star. It won’t eliminate every disagreement, but it gives you a framework for making decisions together.

Knowing what you’re building together helps you measure individual choices against a bigger picture. That’s what alignment actually looks like: not identical opinions on every detail, but clarity about where you’re going and why.

Ready to Go Deeper?

Navigating money conversations in a blended family is complex, but it’s also an opportunity to build deeper understanding and alignment within your marriage.

California’s top state income tax rate of 13.3% doesn’t discriminate — it applies to wages, bonuses, investment gains, and business sale proceeds alike. But while every high earner in California faces the same tax code, not all of them pay the same amount. The ones who keep more aren’t doing anything illegal, and they don’t have access to secret strategies unavailable to others. What they do have is a deliberate, multi-year approach built around three core levers: controlling when income is recognized, structuring investments for state-level tax efficiency, and making coordinated financial decisions with long-term tax consequences in mind. Here’s how it works and why waiting until tax season to think about any of this is one of the most expensive habits a high earner in California can have.

California taxes are high. In fact, according to the Tax Foundation, Fiscal Year 2022 data show they’re second only to New York. Overall, California tax collections per capita were about $10,319, compared to a US average of $7,109.

But if you’re a high earner there, doubtless you already know this.

You may be less aware that even within the same tax system, people earning similar amounts can pay different amounts of taxes. Some even make more than others while paying less in state taxes, sometimes significantly so.

This isn’t about tax evasion, which is illegal, nor do these people try to avoid California taxes altogether, which is next to impossible for California residents. Instead, they focus on optimizing when and where income shows up, and on how different financial decisions interact and affect outcomes.

Implementing these strategies won’t let you eliminate your taxes, but it can make a big difference in how much you get to keep over a lifetime.

Key Takeaways

1

California taxes long-term capital gains the same as ordinary income — making federal tax strategies unreliable at the state level.

Unlike the federal tax code, California offers no preferential rate for long-term capital gains, which means strategies specifically designed to minimize federal taxes can fall flat — or even backfire — for California residents. High earners need a California-specific tax framework, not a one-size-fits-all approach borrowed from federal planning.

2

Stacking income events in a single tax year is one of the most expensive mistakes high earners in California make.

Bonuses, stock option exercises, RSU sales, and business sale proceeds hitting in the same calendar year can push high earners into California’s steepest marginal tax brackets — a self-inflicted tax problem that proactive income timing can often prevent. Spreading these events across multiple years, when feasible, can meaningfully reduce the effective rate paid on that income.

3

The highest-impact California tax strategies — including direct indexing, municipal bonds, and multi-year deferral planning — require ongoing coordination, not a once-a-year tax filing mindset.

Tools like direct indexing (which harvests losses even in up markets), California municipal bonds (exempt from both federal and state taxes), and long-term deferral vehicles such as cash balance plans and deferred compensation can dramatically reduce lifetime tax drag — but only when implemented consistently and coordinated across your financial advisor and CPA well before year-end.

Why California Tax Strategies Are Different and Why That Matters for High Earners

Not only are California taxes higher than almost any other state’s, but they’re also broader than most. For example, there are no preferential tax rates for long-term capital gains (LTCG).

When

marginal rates are high,

income is broadly taxed, and

there’s limited preferential treatment,

many common tax-reduction strategies stop working. In fact, some can even backfire. This is why the gap between managing and optimizing taxes vs. just paying them tends to be wider in California than in most other states.

The Most Common California Tax Mistakes High Earners Make

So, if it isn’t about tax evasion, generic tax tips, or access to some secret tools, how do certain high earners optimize their taxes better than others?

First, most high earners don’t ignore taxes, but they do tend to focus mostly on maximizing their earnings. They evaluate compensation, bonuses, and business-sale windfalls based on how large they are.

They think of taxes, but often as a secondary consideration.

In California, as in other high-tax states, income timing can be crucial. Having multiple one-time income spikes in a single year can push you into higher tax brackets.

That makes your taxes more expensive.

Second, many assume that the same strategies they use to optimize federal taxes work equally well for state taxes.

In California, some, but not all, do.

Here’s one example that doesn’t.

If you’re a high earner, concentrating long-term capital gains in a taxable portfolio lets you pay significantly lower federal income tax on them than placing them in a tax-deferred account, such as a traditional IRA.

California, however, taxes long-term capital gains the same as wage income, so strategies built around long-term holding periods for federal purposes don’t carry the same state-level benefit.

Third, people only think about taxes when it’s time to file, when it’s already too late to do much optimizing. Or, at best, they think about them one year at a time.

That’s understandable, since that’s how we report our income and pay our taxes.

But this is far less powerful than multi-year tax planning. If you have an especially high income in a single year, you’ll get pushed into the higher tax brackets of California’s progressive tax system, which would extract much higher taxes than if you could spread the excess income over two or more years.

While these patterns are understandable, not evidence of carelessness, they won’t let you achieve the optimal results you want.

You need a different approach for that.

3 Proven Strategies High Earners Use to Reduce California State Taxes

In California, there are 3 main ways you can optimize your lifetime taxes.

Time Your Income to Avoid California’s Highest Tax Brackets

Build State Tax Efficiency Into Your Investment Portfolio

Plan Taxes Across Years, Not Just Tax Seasons

Here’s how they work.

1. Time Your Income to Avoid California’s Highest Tax Brackets

Here, your power move is combining two ideas, income timing and the resulting tax rates.

In a high-tax state like California, this is connected even more tightly than in other states.

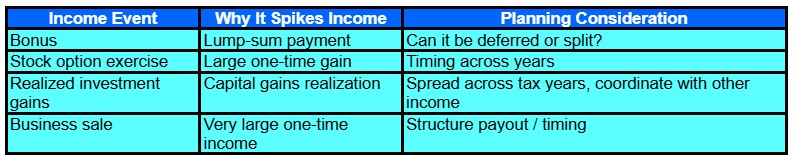

Beyond “base” income, high earners often have other large compensation sources (Table 1).

Bonuses.

Exercised stock options.

Significant realized investment gains, e.g., when selling Restricted Stock Units (RSUs) at highly appreciated prices.

Selling (part or all of) a business.

Table 1. Events that can spike your income and what you can consider doing about them.

When several of these get stacked in a single tax year, you may get pushed into higher marginal tax brackets, forcing you to pay a larger fraction of your income in taxes.

Dr. Steven Crane, Founder of Financial Legacy Builders, agrees, “The biggest mistake I see is people focusing only on how much they make, not when and where it’s taxed. California is aggressive, and if you stack income in one year, bonuses, stock sales, and business income, you can get hit far harder than expected. A lot of high earners don’t realize they’re creating their own tax problem just through timing.

“The people who plan ahead keep more. The ones who react usually pay more. California taxes success aggressively, but it doesn’t mean you’re stuck. The key is realizing that taxes aren’t just something that happens to you; they’re something you can plan around. Most of the damage I see isn’t from bad investments, it’s from unplanned tax events that could have been managed with a little foresight.”

That’s why smart high earners try, when they can, to spread these events across multiple years. This doesn’t let them avoid the tax, but it does let them pay at least somewhat lower taxes on the same income.

A similar notion shows up in picking what retirement accounts to contribute to.

Roth accounts, both IRA and 401(k), are attractive because they let you pay taxes now on your contributions, but avoid paying any taxes on withdrawals, even when the majority of the withdrawn money is investment gains.

That makes sense in some situations.

But when your current marginal tax rates are very high, that’s an expensive choice. One that doesn’t usually optimize your long-term results.

As Joe Stabile, Founder at Coast Financial, explains, “A common mistake I see many high earners in California make is blindly choosing to fund Roth retirement accounts. While Roth accounts have their benefits, it’s important to realize that your top marginal tax rate in California, between federal and state, can be 50.3%, which means any income you can defer at this level to future years, where your effective rate is lower, is extremely powerful. Deferral strategies can include 401(k) plans, HSAs, deferred compensation plans, cash balance plans for business owners, and more.”

The key here is that by contributing to a tax-deferred account, rather than a tax-now account like a Roth, you can pay taxes later, when your marginal tax bracket may be lower.

This will often reduce your lifetime taxes, even with the same lifetime income.

If, like me, you’ve put most of your long-term savings into such tax-deferred accounts, you may be unhappy that all withdrawals, including money that originated from long-term capital gains, get taxed at regular income tax rates, rather than at preferential LTCG rates.

In states like California, where LTCG is taxed the same as regular income, the negative impact of this is smaller than in states that treat LTCG preferentially, as do federal taxes.

Tushar Kumar, Founder, Twin Peaks Wealth Advisors, has a different perspective, “The number one mistake I see high taxpayers in California making is not maxing out all of the tax-advantaged buckets at their disposal. Most of my clients max out their 401(k) contributions, but many overlook the Mega Back Door Roth 401(k) option. Most of my clients make some contributions to 529 accounts, but many don’t max them out or don’t take advantage of the super-funding rules. Most people don’t understand how much money they are leaving on the table by not maxing out these accounts.”

How California treats the 529 college savings plan is different from many other states. There is no state tax deduction for contributions made to these plans, but qualified withdrawals are tax-free.

Ajay Vadukul, CFP®, EA, Vice President of Endeavor Advisors, also sees Roth accounts as a useful tool, “Roth conversions are a conversation we start early, too, since California offers no special treatment for retirement distributions. Converting in lower-income years before Required Minimum Distributions (RMDs) kick in reduces your long-term burden at both levels.”

2. Build State Tax Efficiency Into Your Investment Portfolio

Next up is how you structure your investments.

Not all income sources get taxed the same, which you can use to your benefit.

For example, as Ray Prospero, Partner Advisor, AdvicePeriod, details, “My practice is geared toward the high-net-worth space, and two of the tax-mitigation strategies I like to explore for my high-income California clients are municipal bond ladders and direct indexing.

“Municipal bond ladders can generate consistent, tax-advantaged income while managing interest rate risk by holding individual bonds with staggered maturities. On the equity side, direct indexing gives us more control. By owning the individual stocks within an index, we’re able to harvest losses throughout the year, even in up markets, while staying broadly aligned with overall market performance. Those losses can then be used to offset capital gains and potentially reduce a portion of taxable income.

“When combined, it can be an effective way to potentially enhance tax efficiency while maintaining a disciplined, long-term investment strategy.”

Kumar agrees, “I see many California residents sitting on cash in high-yield savings accounts or money market funds when they could be considering California muni bonds for tax-free yield. Of course, there is a risk trade-off there.”

As this demonstrates, you can and should build tax efficiency, especially at the state level, into your portfolio structure.

Income from municipal bonds is exempt from federal and, for bonds issued by California public agencies, state taxes.

Direct indexing lets you harvest losses even when the index is up. That’s because there are almost always some companies in the index with depressed prices, even in a bull market. This means you can sell those shares to capture a loss, without selling the entire index, which may be at a higher price point than when you bought in.

Then, when enough time has gone by so it isn’t a wash sale, you can buy back those shares to reestablish the full index.

Doing this consistently, not as a once-and-done exercise, provides long-term tax benefits. That’s why you should make a point of it, even if you’re busy.

3. Plan Taxes Across Years, Not Just Tax Seasons

Yes, income is reported, and taxes are paid on an annual basis.

But that doesn’t mean that’s the optimal way to plan. The most effective tax strategies play out over years or even decades and help guide and coordinate decisions across multiple aspects of your financial life.

As James Selu, CFP®, CEPA®, CBDA®, President & Founder of Palm Coast Wealth Management, says, “One of the biggest mistakes high earners make is waiting until tax season to think about taxes. By the time you’re preparing a return in March or April, the tax year is already over, and many of the best planning opportunities are gone. At that point, you’re often limited to reporting what happened rather than improving it.”

This is where long-term planning becomes critical.

Advanced tax planning for higher-net-worth households looks five, ten, twenty, or even more years into the future, rather than focusing on the next Tax Day.

These strategies include various trusts, permanent insurance, annuities, charitable giving vehicles, and more, with each family’s situation calling for a different set of tools, implemented in a tailored way.

Selu again, “Depending on the client’s situation, strategies may include maximizing retirement plan contributions, Roth conversions in lower-income years, tax-loss harvesting, charitable giving, municipal bond strategies, deferred compensation planning, or repositioning assets into more tax-efficient investments. The right strategy depends on how someone earns income: W-2 wages, business income, stock compensation, real estate, or investments.”

Vadukul expands, “The biggest mistake high-earning Californians make is treating state taxes as a fixed cost instead of a planning opportunity. With California’s 13.3% top rate, there’s real leverage available. You just have to use it.

“For clients who are charitably inclined and over 70½, qualified charitable distributions from your IRA are one of the cleanest tools available, reducing your Adjusted Gross Income (AGI) at both the federal and state level in one move. If you’re sitting on appreciated stock, gifting shares to children in a lower bracket rather than selling yourself can dramatically cut the capital gains bill.

“On the deferral side, maxing your 401(k) is table stakes, but self-employed clients and business owners should be looking at solo 401(k) plans or cash balance plans, which can shelter hundreds of thousands annually. An S-corp election is also worth revisiting for the right business owner. And for clients facing a large capital gains event, Qualified Opportunity Zone investments can defer and potentially reduce that exposure in ways most people haven’t considered.”

None of this implies that you, or even a financial advisor, can predict the future with any guaranteed accuracy.

However, planning over the long term gives you a better chance of success than focusing on the current tax year, or worse, on the previous one.

Taken together, these three levers don’t eliminate state taxes, but they do let you optimize how you position yourself, which determines how efficiently you can maximize your lifetime take-home money.

The Bottom Line: California Taxes Are High, But Your Lifetime Tax Bill Isn’t Fixed

Whatever you think or feel about California’s high state income taxes, if you live there and earn a high income, they’re a major, unavoidable factor in your financial picture.

Some people suggest moving out of California because of this.

Moving to a lower-tax state can indeed reduce your tax burden, but you should only consider it if it makes sense for your overall life. And even then, California’s residency rules mean the timing and structure of that move matter. If it looks temporary or primarily tax-driven, you may not achieve the outcome you expect.

Vadukul agrees, “Something I only half-joke about with clients: one of the most effective California tax strategies is leaving California. Texas, Nevada, Florida, Arizona. The savings can be $50,000 a year or more for a high earner. But there are things money can’t buy. Family, community, California’s business ecosystem. I’ve had clients look at that number and say, ‘still worth it to stay,’ and that’s a completely legitimate answer. The goal is to make sure the decision is informed, not to let the tax tail wag the life dog.”

For most people, you can get the results you want from planning, without needing to relocate. From not treating taxes as something you deal with once a year for a few weeks, but rather planning and managing them continuously, even if you’re busy with your career and family.

As Selu puts it, “Successful professionals are so busy building careers or businesses that tax planning gets pushed aside. Unfortunately, California’s high state tax rates can make procrastination expensive. Without proactive planning, people often miss opportunities to manage income timing, harvest losses, maximize retirement contributions, or structure investments more efficiently.

“Tax planning should be ongoing, not seasonal. The earlier you plan, the more options you tend to have. The most valuable habit a high earner can have in this regard is scheduling a coordinated year-end tax planning meeting with both their financial advisor and CPA before December 31. That gives you time to evaluate what happened during the year and make adjustments while there’s still time to act.

“California taxes may be high, but with proactive planning, coordination, and discipline, you can often reduce unnecessary tax drag and keep more of what you earn.”

Crane sums it up, “The most effective strategies usually come down to control. Control when income hits, diversify how it’s taxed, and be intentional about where you live and work. That might mean spreading income across years, using tax-deferred and tax-free buckets, or even thinking seriously about residency if it aligns with your life.”

It’s simple, but not necessarily easy to implement:

Taxes aren’t just something you file. They’re something you manage.

Ongoingly.

And in a high-tax state like California, small, consistent improvements in how you manage them can add up to a noticeable difference in what you keep over a lifetime.

Are You Ready to Hire a Financial Advisor?

You’ll find a growing number of financial advisors featured on Wealthtender. You can search based on the areas of specialization most important to you and where they’re located, or browse our financial advisor directory for more search options to find advisors who may be a good fit for you.

Find Your Next Financial Advisor on Wealthtender

📍 Click on a pin in the map view below for a preview of financial advisors who can help you reach your money goals with a personalized plan. Or choose the grid view to search our directory of financial advisors with additional filtering options.

Disclaimer: This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel, Ph.D.

My career has had many unpredictable twists and turns. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research position in experimental cosmic-ray physics (including a couple of visits to Antarctica), a brief stint at a small engineering services company supporting NASA, followed by starting my own small consulting practice supporting NASA projects and programs. Along the way, I started other micro businesses and helped my wife start and grow her own Marriage and Family Therapy practice. Now, I use all these experiences to also offer financial strategy services to help independent professionals achieve their personal and business finance goals. Connect with me on my own site: OpherGanel.com and/or follow my Medium publication: medium.com/financial-strategy/.

Divorce is one of the most significant financial transitions you’ll ever navigate. While the emotional weight of ending a marriage can feel overwhelming, the financial decisions you make in the months before filing can shape your security and independence for decades to come.

If you’re contemplating divorce or know it’s inevitable, taking strategic financial steps now, before you file, can protect your interests, clarify your options, and position you for a more stable future.

This guide will walk you through the essential actions to take during this critical window, helping you move forward with clarity, confidence, and control.

Why “Before You File for Divorce” Matters

The period before you officially file for divorce is uniquely important. During this time:

You still have full access to financial accounts and records

Your spouse may be less guarded or defensive about finances

You have time to gather documentation without court-imposed deadlines

You can consult professionals privately and develop a strategy

You can take steps to protect yourself financially without triggering immediate conflict

Once divorce proceedings begin, access to information may become restricted, emotions may escalate, and decisions are often made under pressure or court deadlines. Preparing in advance gives you leverage, clarity, and peace of mind.

Step 1: Gather and Organize Financial Documents

The foundation of any divorce settlement is a clear understanding of your family’s financial picture. Before you file, quietly and methodically gather copies of all important financial documents.

What to Collect:

Income documentation:

Tax returns (federal and state) for the past 3–5 years

Recent pay stubs for both spouses

W-2s, 1099s, K-1s, and other income statements

Business financial statements if you or your spouse own a business

Asset records:

Bank account statements (checking, savings, money market) for the past 12 months

Real estate records (deeds, mortgage statements, recent appraisals)

Vehicle titles and loan statements

Business ownership documents and valuations

Cryptocurrency account statements

Life insurance policies (cash value and beneficiary information)

Debt records:

Credit card statements for all accounts

Mortgage statements

Auto loan statements

Student loan statements

Personal loan or line of credit statements

Any judgments, liens, or other obligations

Other important documents:

Estate planning documents (wills, trusts, powers of attorney)

Prenuptial or postnuptial agreements

Social Security statements

Health insurance policies

Recent credit reports for both spouses

Why this matters: Complete documentation prevents your spouse from hiding assets, underreporting income, or claiming ignorance about financial details. It also allows your attorney and financial advisor to build an accurate picture of what’s at stake.

How to do it discreetly: Make copies or take photos of documents. Download statements from online accounts. Store everything securely, either digitally (encrypted cloud storage, password-protected files) or physically (safe deposit box in your name, trusted friend or family member’s home). Don’t leave copies where your spouse can find them.

Step 2: Understand Your Current Standard of Living

Courts often use “marital standard of living” as a benchmark for spousal support and division of assets. Before filing, document your family’s spending patterns and lifestyle.

It helps establish what you’ll need to maintain a similar lifestyle post-divorce

It supports arguments for spousal or child support

It provides a reality check for budgeting your post-divorce life

Pro tip: Review credit card and bank statements to build this picture. If you don’t have direct access, gather what you can before filing.

Step 3: Open Individual Accounts in Your Name

If you don’t already have financial accounts solely in your name, now is the time to establish them.

What to open:

Individual checking account: Deposit your paycheck here going forward. This protects your income from being drained by your spouse.

Individual savings account: Build an emergency fund to cover 3–6 months of post-divorce living expenses.

Individual credit card: Establish credit in your own name if you don’t already have it. This is essential for rebuilding your financial independence.

Important: Don’t drain joint accounts or transfer large sums without legal advice, this can be seen as dissipation of marital assets and may hurt you in court. Instead, open new accounts and begin directing income there going forward.

Step 4: Check and Monitor Your Credit

Your credit report contains critical information about your financial life and may reveal debts or accounts you didn’t know existed.

What to do:

Pull your credit report from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com

Review it carefully for:

Joint accounts or debts

Accounts you’re listed as an authorized user

Unknown or fraudulent accounts

Your credit score and history

Consider placing a credit freeze or fraud alert if you’re concerned your spouse may open accounts in your name

Monitor your credit regularly during the divorce process

Why this matters: You’re responsible for joint debts even after divorce unless explicitly addressed in your settlement. Knowing what’s out there allows you to negotiate who assumes which debts.

Step 5: Determine the Value of Major Assets

Some assets are easy to value (bank accounts, publicly traded stocks), while others require professional appraisals.

Assets that may need valuation:

Real estate: Get a current market appraisal or at least a comparative market analysis from a realtor

Business interests: If you or your spouse own a business, a formal business valuation may be necessary

Retirement accounts: Obtain recent statements showing current balances

Pensions: Understand the present value of any defined benefit pensions

Personal property: High-value items like art, jewelry, collectibles, or antiques

Stock options or restricted stock units (RSUs): Determine vesting schedules and current value

Pro tip: Don’t tip your hand by suddenly requesting appraisals if it seems unusual. If possible, gather comparable sales data or informal estimates first, and save formal appraisals for when you have legal representation.

Step 6: Understand Your Spouse’s Income and Benefits

In many marriages, one spouse handles most of the finances while the other has limited visibility. If that’s your situation, now is the time to educate yourself.

Key questions to answer:

What is your spouse’s exact income (salary, bonuses, commissions, business income)?

What benefits does your spouse receive (health insurance, stock options, retirement contributions, company car, expense accounts)?

Does your spouse have access to hidden income or unreported cash?

Are there deferred compensation plans, stock awards, or other future income?

Why this matters: Spousal support and child support calculations depend on accurate income information. Underreported income means you may receive less than you’re entitled to.

Step 7: Assess Your Own Earning Potential

If you’ve been out of the workforce, working part-time, or earning significantly less than your spouse, understanding your earning potential is critical.

Ask yourself:

What are my current job skills and qualifications?

What is the job market like in my field?

Do I need additional training, certification, or education to re-enter the workforce or increase my earnings?

What is a realistic income I can expect to earn post-divorce?

This assessment influences:

Whether you’ll seek spousal support (and for how long)

Your post-divorce budget and lifestyle

Decisions about returning to school or career development

Pro tip: If you’ve been a stay-at-home parent or out of the workforce for years, courts may award rehabilitative spousal support to help you gain skills and become self-supporting. Document your career sacrifices and the gap in your resume.

Step 8: Consider the Tax Implications of Asset Division

Not all assets are created equal when it comes to taxes. A $100,000 retirement account is not the same as $100,000 in cash or home equity.

Key tax considerations:

Retirement accounts (401(k)s, IRAs): Withdrawals are taxable as ordinary income. Dividing them requires a Qualified Domestic Relations Order (QDRO).

Roth accounts: Qualified withdrawals are tax-free, making them more valuable than traditional retirement accounts.

Home equity: Generally not taxable when sold as part of a divorce, up to certain limits.

Taxable investment accounts: May have embedded capital gains that will trigger taxes when sold.

Stock options and RSUs: Tax treatment varies depending on type and vesting schedule.

Why this matters: Accepting an equal dollar split without considering tax consequences can leave you with less after-tax value. Work with a financial advisor or Certified Divorce Financial Analyst (CDFA) to model different scenarios.

Step 9: Understand Health Insurance Options

If you’re covered under your spouse’s employer health insurance, you’ll lose that coverage after divorce.

What to explore now:

COBRA: You can continue your spouse’s employer coverage for up to 36 months, but you’ll pay the full premium (often expensive).

Marketplace plans: Explore health insurance options through the Affordable Care Act marketplace.

Your own employer coverage: If you work, check your employer’s plan and costs.

Medicaid: Depending on your income, you may qualify for Medicaid post-divorce.

Pro tip: Health insurance costs should be factored into your post-divorce budget and may influence spousal support negotiations.

Step 10: Consult with Professionals Before Filing

Divorce is not a DIY project, especially when significant assets, businesses, or complex financial situations are involved.

Who to consult:

Divorce attorney: Interview several before choosing. Look for someone experienced in cases like yours (high-net-worth, business ownership, child custody, etc.).

Certified Divorce Financial Analyst (CDFA): A CDFA can model different settlement scenarios, analyze tax implications, and help you understand the long-term financial impact of decisions.

Therapist or counselor: Emotional support is critical. Divorce is a major life transition, and having professional support helps you make clearer, less reactive decisions.

CPA or tax advisor: Understand the tax consequences of asset division, spousal support, and filing status changes.

Financial advisor: Work with someone who understands divorce planning and can help you create a post-divorce financial plan.

Important: Consultations before filing are often confidential and protected. Once you file, certain communications may become discoverable in court.

Step 11: Protect Yourself from Financial Abuse

In some marriages, one spouse controls all the money, monitors spending, or limits the other’s access to financial resources. If this describes your situation, take steps to protect yourself.

What to do:

Open accounts your spouse doesn’t know about (at a different bank)

Redirect a portion of your paycheck to your individual account

Document any financial abuse or controlling behavior

Keep cash in a safe place

Change passwords on your personal accounts

Consider a restraining order if there’s a threat of financial retaliation

Why this matters: Financial abuse is a form of domestic abuse. Courts take it seriously, and documenting it can strengthen your case.

Step 12: Think About Your Post-Divorce Life

Finally, take time to envision what you want your life to look like after divorce.

Questions to consider:

Where do you want to live? (Keep the house? Move? Downsize?)

What are your financial priorities? (Stability? Independence? Funding your children’s education?)

What does financial security look like for you?

What are your non-negotiables in the settlement?

Having clarity about your goals helps you and your legal team negotiate more effectively.

Final Thoughts

Divorce is undeniably difficult, but it doesn’t have to leave you financially devastated or unprepared. By taking strategic steps before you file, you give yourself the best possible foundation for a fair settlement and a secure future.

You don’t have to navigate this alone. At Life Story Financial, we specialize in helping women through major life transitions, including divorce. We provide clarity, guidance, and support so you can move forward with confidence.

Frequently Asked Questions

Should I close joint credit cards before filing for divorce?

Generally, no. Closing accounts can hurt your credit score. Instead, contact the creditor to remove your liability or freeze the account from new charges. Discuss strategy with your attorney.

Can my spouse drain our joint accounts before I file?

Yes, unless there’s a court order preventing it. This is why opening individual accounts and redirecting income is important. If your spouse does drain accounts, document it, this may be considered dissipation of marital assets.

What if my spouse owns a business and I suspect hidden income?

Work with a CDFA or forensic accountant who can analyze business records, tax returns, and cash flow to uncover unreported income or undervalued business assets.

How soon should I start gathering documents?

As soon as you’re seriously considering divorce. The earlier you start, the more complete your documentation will be.

Do I need to tell my spouse I’m preparing for divorce?

That depends on your situation. If there’s a risk of retaliation, financial abuse, or asset hiding, it may be safer to prepare quietly. Consult with an attorney before disclosing your intentions.

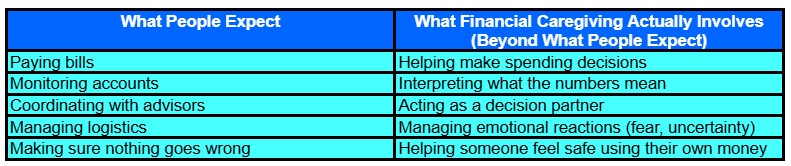

Most people don’t think of themselves as a financial caregiver until suddenly they are one. Whether it’s a parent who can no longer manage investments after losing a spouse, or a sibling whose finances have quietly become unmanageable, stepping into this role is rarely something families plan for. And that’s exactly the problem. What looks from the outside like a straightforward task — helping Mom pay her bills and stay on budget — turns out to involve legal authority you may not have, emotional dynamics no one warned you about, and decisions that require expertise most of us simply don’t have. Financial advisors who regularly work with families in this situation say the gap between what people expect and what they actually face is the single biggest source of costly mistakes. Here’s what they consistently say families miss and what you can do now, before you need to.

“Mom?” I asked, “Have you and Dad set things up so you’d be financially secure if he passed away before you?”

It was 2014.

My concern was that Dad had always handled all their finances. Worse, he was three years older than she was, in poorer health, and, as a male, statistically likely to pass away younger anyway.

Her response was resounding, emotionally driven, and reality-denying: “That won’t happen!“. And that was the end of the conversation.

I didn’t push and never brought it up again. Obviously, neither did she. Like most families, we just left it there.

Two years later, in 2016, what I expected to happen did. Dad passed away, leaving Mom to deal with life on her own for the first time in over 70 years.

In her late 80s, Mom was still perfectly able to handle the day-to-day stuff. She could use credit cards, withdraw cash from the ATM, order groceries, use the phone, and talk with people (though often with less of a filter than appropriate).

Unfortunately, she was woefully unprepared and felt unable to learn how to understand and manage investments, budget appropriately for her situation, or even see how all the moving pieces of her finances fit together. So, I offered to help with managing her finances in Dad’s place.

Given her personality, her experience, and her fears, she didn’t easily trust anyone, not even my sisters or me, to do this. She was afraid that whoever she let in might behave inappropriately with her money, or at least judge her for how she spent it.

So I asked her, “Do you see any situation in this universe in which I would cheat you, steal from you, or even judge you?”

She went silent for a few loaded seconds, then said simply, “No. Never.”

With that acceptance, I stepped in. I thought I knew what to expect. I’d organize things, review her accounts, pensions, and bills; communicate with her investment manager; and make sure she didn’t spend beyond her means. And I did all those things.

Thankfully, Dad had set up the investment management relationship decades earlier, and the CEO there was my oldest childhood friend, so I knew I could trust him. Dad had also set up their credit cards and utility bills to all be paid automatically, so I didn’t have to go too far into the weeds. Not everyone is that prepared and that fortunate.

Mom insisted that she didn’t want to stay in a home that was too big and old for her to manage, where everywhere she turned, there were 60+ years of memories of Dad, and where she’d be alone, with nobody knocking at her door for days at a time.

So, my sisters and I helped her sell her house and move into an independent living facility a few miles down the road, so she knew the area like the back of her hand. This meant that her housing and food expenses were known, predictable, and easily within her means. All that wasn’t the hard part.

One of the harder things was when she couldn’t tell me what various transactions were for, so I couldn’t necessarily separate legitimate expenses from things she’d been talked into inappropriately, let alone outright fraud. Here, too, we were fortunate, and nothing really bad of that sort happened. Much worse, though, was helping her feel comfortable spending her money.

She constantly worried about “Spending my kids’ inheritance.” This, to the point that she wasn’t sure it was ok to buy a few pairs of panties!

This, even though I repeatedly reassured her that she was better than fine, and that I would alert her promptly if I ever saw that she was on an unsustainable path, long before it became too late.

I also had to keep reassuring her that this was her money, that it was there for exactly this reason, that she could spend it as she chose, and that, however much or little remained when she passed away, we’d be happy that she had a comfortable retirement, and grateful for whatever we received.

None of this seemed to stick. She’d say she understood and was ok with it, but as soon as we hung up the phone (I was over 5,000 miles away), she lost the confidence that she could spend whatever she wanted.

In the final analysis, repeatedly giving her “permission” to spend more than she allowed herself, reassuring her that it was appropriate because it was her money and it was there to support her, was more valuable than anything technical I did for her.

Key Takeaways

1

Financial caregiving is far more than paying bills and monitoring accounts.

Most people stepping into a financial caregiving role expect to handle logistics — paying bills, reviewing statements, coordinating with investment managers. What they don’t anticipate is the emotional weight: helping an aging parent feel comfortable spending their own money, navigating family disagreements, and making high-stakes decisions under pressure with incomplete information and no formal training.

2

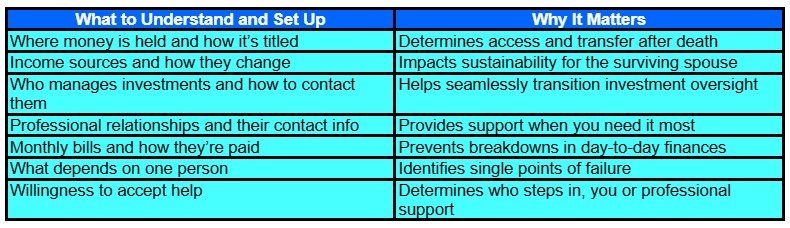

Without legal authority and full financial visibility already in place, families can be locked out when it matters most.

A durable power of attorney, updated beneficiary designations, and a clear record of accounts, income sources, and professional relationships aren’t just paperwork — they’re the infrastructure that determines whether a caregiver can actually act. Families who assume they’ll figure it out when the time comes often discover they’re legally blocked from accessing accounts at exactly the moment their parent needs them most.

3

The best time to prepare for financial caregiving is long before you need to step in.

Having the uncomfortable conversation while everyone is still healthy — covering where accounts are held, how bills are paid, who the professional contacts are, and what role each family member will play — is worth far more than any planning done during a health crisis. Financial advisors consistently find that the families who navigate caregiving most successfully aren’t the wealthiest ones; they’re the ones who talked about it early and put the right structure in place ahead of time.

The Emotional Side of Financial Caregiving Most People Don’t See Coming

That wasn’t the role I expected to play.

And it’s not a role most people expect when they have to step in to help a parent or sibling manage their finances.

But that, or the reverse, reining in unsustainable spending, may be the most important part of what financial caregiving often entails.