Introducing Certified Advisor Reviews™: The first advisor review platform built for SEC Marketing Rule compliance

Certified Advisor Reviews™ help consumers make smarter hiring decisions, and help financial advisors turn client trust into growth, compliantly, on the web and in AI search.

Scroll to explore, or jump to what matters to you ↓

What it is

Certified Advisor Reviews™ help consumers choose with confidence

And help advisors build trust and get found, without the compliance worry that kept testimonials off-limits for decades.

Collect & display compliantly

Unlike sites like Google and Yelp, every review on Wealthtender includes the disclosures that satisfy regulatory and firm requirements, with admin tools to protect client privacy and a Google Reviews import tool.

Build trust more quickly

Reviews written by your clients create an emotional connection that helps prospects feel confident about hiring you, going beyond your experience and credentials alone.

Rank higher and get found

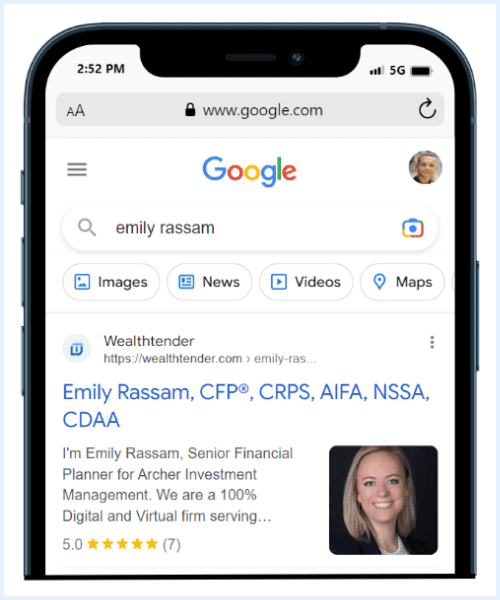

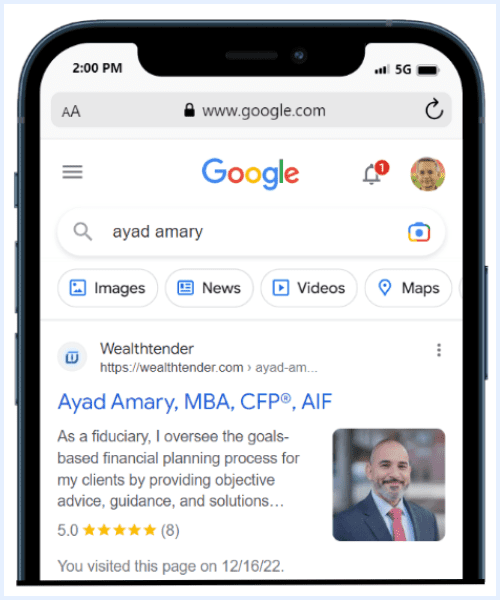

Your reviews live on a domain visited by nearly 500,000 consumers a year, send positive trust signals to Google and AI tools, and make your gold stars shine in search results.

Positive trust signals

Your reviews on Wealthtender show up where prospects search

Collect reviews compliantly, rank higher in search results, and accelerate the trust-building process with prospects.

See it in action

Take an interactive tour of Wealthtender

Get hands-on and discover why 900+ advisors and wealth management firms choose Wealthtender as their digital marketing partner and online reviews platform.

Find your path

Jump to what matters to you

Advisors

Benefits, how it works, displaying reviews on your site, getting started.

Explore →Compliance

SEC Marketing Rule & FINRA 2210, disclosures, certification, removals.

Explore →Firms & enterprise

Review amplification, firm profiles, the case study, and how we compare.

Explore →Media

The industry-first story, the data, coverage, and an SME to quote.

Explore →Consumers

What a certified review means, the ratings map, why reviews matter.

Explore →Put client reviews to work, without the compliance worry

Everything you need to collect, certify, display, and promote reviews that build trust and help you get found.

The benefits

- Reviews accelerate trust and create an emotional connection with prospects.

- Your reviews appear on wealthtender.com and send positive trust signals to Google and AI tools.

- Gold stars in search results help you stand apart from advisors without reviews.

- Easy to display on your own website, with tips to promote compliantly on social.

Get started, on your timeline

The SEC Marketing Rule opens the door to new opportunities, and new risks. Grab the free playbook and education series, then move when your compliance team gives the green light.

Not ready yet? That is ok, you are not alone. When you are ready, we will be here to help you get started.

Clients and other acquaintances write a review on the Wealthtender profile of an advisor who has turned the reviews feature on. Before a review is publicly displayed, the advisor provides Wealthtender with important information about their relationship with the reviewer, so consumers gain the transparency they deserve when their life savings could be at stake. These disclosures also help advisors satisfy compliance with industry regulations.

Once Wealthtender receives the requested information, we complete the certification process and publish the review with the Certified Advisor Review™ mark. Advisors in good standing are authorized to display the Certified Advisor Reviews™ badge on their website, email signature, and social media accounts.

There are two easy, compliant ways to display reviews on your site.

1) A rotating carousel. This is how Abundo Wealth, an SEC-registered investment advisor, publishes reviews on its homepage. To stay compliant they display the three required disclosures clearly and prominently (client or non-client, compensated or not, any material conflicts), and because only a sample of reviews is shown, they link to their Wealthtender profile where every review is available. Since each rotating review shares the same disclosures (each reviewer is a current client, not compensated, no conflicts), the disclosure can be written once and applied to the set.

2) An embeddable widget. Wealthtender can provide simple HTML you can place anywhere on your site, below your bio, within an article, or on your homepage. Each review is packaged with its required disclosures, so nothing extra needs to be coded. You can see a live example on the Abundo Wealth article. Learn how to display testimonials on advisor websites.

Editing: if a review contains language not permissible by the SEC or another regulator, Wealthtender works with the advisor and, or their compliance officer to redact the disallowed language (or remove it if doing so does not affect the integrity of the review).

Anonymity: all reviewers must provide a valid email address, shared only with the reviewed advisor to confirm identity. Reviewers may choose to display their full name, an abbreviated name, or remain anonymous.

Removal: advisors may request a review be removed or not published if it is disallowed by a regulator, for example if the reviewer meets the SEC definition of a bad actor. Wealthtender also removes spam automatically and may remove profane or indiscernible reviews lacking substance.

Optional: reviews are always optional. Advisors can turn them on or off at any time and still enjoy all other platform benefits.

For doctors and lawyers, online reviews are already a fact of doing business, a useful preview of where advisor reviews are heading. In a BrightLocal survey, 89% of consumers said they look at reviews of medical professionals and 81% look at lawyer reviews. A 2018 NRC Health study of 3,000+ patients found 37% used online reviews as their very first step in finding a new doctor, 83% trust online ratings more than personal recommendations, 75% want to see at least 7 ratings, and 60% are suspicious of only-positive reviews. A 2018 Martindale-Avvo survey of 6,300 consumers found 47% used review sites and directories to find an attorney, more than any other resource.

We also asked several doctors, lawyers, and review experts what they would tell a financial advisor getting started:

Max Meinerz, DDS

Honest Teeth Dentistry“Most patients are happy to write reviews and love sharing their chosen professional with others. You simply have to make a practice to ask. And spread your reviews across multiple platforms; only focusing on Google can hurt you if their algorithm changes.”

Jason Stern

Law Offices of Jason Stern“Online reviews are critical in this digital age. They provide marketing support, differentiation, and validation before a client ever calls. But have a strategy: when I declined to advertise, Yelp buried all of my five-star reviews under ‘Reviews Not Recommended.’”

Melanie Jayashankar

Owner, MJ Law Firm“I always ask prospective clients to Google me and form their own opinions. My reviews speak for themselves, and most feel more comfortable hiring me after seeing them. Your former clients can sell you better than you can sell yourself.”

Kris Ruby

CEO, Ruby Media Group“Google is now your digital front door. How you respond to reviews matters more than the reviews themselves: make the person feel heard, validate with genuine empathy, and know when to stop. People measure a business by how the owner replies.”

David Reischer, Esq.

Attorney & CEO, LegalAdvice.com“My most important advice is to work hard to prevent bad reviews before they happen. Consumers scan reviews looking for consistency; a mostly-negative pattern signals a problem. Be proactive: ask what can be done to satisfy a client before they post a negative review.”

E-E-A-T is Google’s shorthand for Experience, Expertise, Authoritativeness, and Trustworthiness (Google added the extra “Experience” to its Quality Rater guidelines in late 2022). YMYL refers to “Your Money or Your Life” topics that could affect a person’s financial stability, health, or safety. Financial advisor websites are already held to higher E-E-A-T and YMYL standards.

Google’s guidelines instruct raters to look for independent reputation information: “When the website says one thing about itself, but reputable external sources disagree, trust the external sources.” By earning reviews on a high-authority third-party platform like Wealthtender, you strengthen those signals and can improve how prominently you appear in search and AI answers.

Wealthtender’s 2025 study of 500 U.S. adults earning $100K+ found that 96% will research an advisor online even after a referral, and reading online reviews and awards is their most popular next step (83%). 61% consider positive reviews on an independent site essential to trust, and 50% want to read reviews before they even reach out. Yet the 2025 Investment Adviser Industry Snapshot shows only about 9.3% of advisors use testimonials or reviews in their marketing, so publishing compliant reviews is one of the highest-leverage ways to stand out and become a prospect’s first call.

Templates & checklists

Start with the free Online Reviews Playbook and the SEC Marketing Rule Education Series, or grab the One-Page Quick Start Checklist (PDF).

Amplify the reach of your firm’s online reviews

Every review your team earns can work harder. Multi-advisor firms have three flexible ways to display client reviews across firm and advisor profiles, so your stars show up wherever prospects search, for your firm and for each advisor by name.

Firm → all advisors

Review Sync™

Reviews collected on your firm profile also appear on every advisor profile.

Advisors → firm

Review Rollup™

Reviews collected on individual advisor profiles also appear on your firm profile.

Firm → selected advisors

Review Allocate™

Choose which advisor profiles display each review, review by review.

Many firms combine them. Running Review Sync and Review Rollup together is common, so reviews flow in both directions and every profile reflects the full strength of the firm. Disclosures are added once and travel with each review to every profile where it appears.

Go deeper

Compare all three firm review amplification features

Side-by-side comparison, live firm examples, eligibility, and answers to the questions firm leaders ask most.

How Wealthtender compares

Lower cost, more benefits, and the only option with a high-authority consumer website behind it.

| Wealthtender | Indyfin | Amplify | FMG | |

|---|---|---|---|---|

| InvestmentNews 5-Star Technology Award (2025) | ✓ | ✕ | ✕ | ✕ |

| Inbound lead-gen benefits | ||||

| Consumer website | wealthtender.com | indyfin.com | ✕ | ✕ |

| Monthly consumer traffic | 63,700 | 967 | ✕ | ✕ |

| Domain Authority (SEO strength) | 42 | 18 | ✕ | ✕ |

| Advisor profile with client reviews (SEO/AEO schema) | ✓ | ✓ | ✕ | ✕ |

| Advisory firm profile with client reviews (SEO/AEO schema) | ✓ | ✓ | ✕ | ✕ |

| Gold stars appear in Google search results | ✓ | ✓ | ✕ | ✕ |

| Firm review amplification (Sync, Rollup, Allocate) | ✓ | ? | ✕ | ✕ |

| Testimonial marketing tools | ||||

| Embed / display SEC-compliant testimonials on advisor website | ✓ | ✓ | ✓ | ✓ |

| Easily create social media content from client testimonials | ✓ | ? | ? | ✓ |

| Award recognition | ||||

| Wealthtender Voice of the Client™ Awards | ✓ | ✕ | ✕ | ✕ |

| Administration features | ||||

| Dashboard to manage reviews | ✓ | ✓ | ✓ | ✓ |

| Convert Google Reviews to SEC-compliant testimonials | ✓ | ✕ | ✕ | ✕ |

| Additional digital marketing benefits | ||||

| Get quoted in the media | ✓ | ✕ | ✕ | ✕ |

| Get featured in local guides | ✓ | ✓ | ✕ | ✕ |

| Gain recognition for areas of specialization | ✓ | ✕ | ✕ | ✕ |

| Pricing | ||||

| Lowest monthly cost (1 advisor) | $59/mo | $99/mo | $99/mo | $79/mo |

| Multi-advisor discounts | Yes (5+ advisors) | Unknown | Yes | Yes |

Domain Authority as of February 2026. Year-over-year trend: Wealthtender rose from 40 (Jan 2025) to 42 (Feb 2026); Indyfin declined from 19 to 18 (Source: Moz). Estimated monthly consumer traffic as of February 2026: Wealthtender rose from 50,000 (Jan 2025) to 63,700 (Feb 2026); Indyfin declined from 4,000 to 967 (Source: Ahrefs).

Competitor pricing and features are shown as published at the time of review. Tools that let consumers submit Google Reviews can introduce regulatory risk, since in FINRA Regulatory Notice 17-18, FINRA treats only unsolicited third-party comments as outside Rule 2210, meaning the act of solicitation can trigger disclosure requirements that the Google Reviews platform does not support.

Success story

How United Financial Planning Group grows with testimonial marketing

A whole firm builds a testimonial marketing strategy, powered by Wealthtender, into every stage of the client funnel.

Built with securities counsel, for the SEC Marketing Rule and FINRA 2210

The SEC Marketing Rule served as the blueprint for the platform. Here is how certification, disclosures, removals, and oversight work, in one place.

Developed with securities counsel

Wealthtender developed Certified Advisor Reviews™ with the guidance of securities attorney Leila Shaver, founder of My RIA Lawyer and Shaver Law Group, LLC. With experience as General Counsel, Chief Compliance Officer, and serving hundreds of financial advisors, Leila’s guidance and ongoing counsel help advisors grow confidently and compliantly. Wealthtender also monitors the SEC Marketing Compliance FAQ page daily and acts promptly when new guidance warrants.

Yes. Certified Advisor Reviews™ are designed to be fully compliant with the SEC Investment Adviser Marketing Rule, developed with the guidance of securities attorney Leila Shaver and maintained against the SEC Marketing Compliance FAQ page, which Wealthtender monitors daily.

Yes. In addition to the SEC Marketing Rule, Certified Advisor Reviews™ are designed to be fully compliant with FINRA Rule 2210 and Regulatory Notice 17-18. Wealthtender believes the SEC Marketing Rule generally sets a higher disclosure bar than current FINRA regulations, so all reviews align to the SEC requirements. That gives a consistent experience across Investment Adviser Representatives, Registered Representatives, Dually Registered professionals, and state-registered advisers in states that have conformed, and gives consumers a consistent basis to weigh reviews.

To earn the mark, a review publicly displays information known to the advisor that a consumer writing a review usually would not provide. At a minimum, the advisor must disclose:

- Whether compensation in any form was provided for the review

- Whether conflicts of interest may have influenced the review

- Whether the review was written by a client or another acquaintance of the advisor

These are displayed clearly and prominently alongside the review, along with any supplemental disclosures the advisor provides to meet federal or state requirements. Per the SEC, a written agreement must be in place between advisor and reviewer unless the reviewer receives less than $1,000 (in cash or otherwise) within a 12-month period, and these requirements apply even to short posts such as a tweet.

Editing: if a review contains language not permissible by the SEC or another regulator, Wealthtender works with the advisor and, or their compliance officer to redact the disallowed language, or to remove it when doing so does not affect the integrity of the review.

Anonymity: all reviewers must provide a valid email address, shared only with the reviewed advisor to confirm identity. A reviewer may be displayed with their full name, an abbreviated name, or anonymously.

Advisors may request a review be removed or not published if it is disallowed by the SEC or another regulator. For example, if the reviewer meets the SEC definition of a “bad actor,” the advisor can submit a form attesting to the disqualification and Wealthtender will promptly remove the review.

Wealthtender also abides by the FTC Consumer Review Fairness Act and may, alone or in coordination with advisors and their compliance officers, prohibit or remove reviews deemed inappropriate or irrelevant. Spam is deleted automatically, and profane or indiscernible reviews lacking substance may be removed.

Optional: reviews are never required. Advisors may turn them on or off at any time and keep every other platform benefit. Federal or state regulations may also restrict or prevent an advisor from collecting reviews.

Republishing: under the FTC Consumer Review Fairness Act, review sites cannot claim copyright over consumer reviews, so reviews posted anywhere may be republished elsewhere with permission from the review writer. Advisors can display Certified Advisor Reviews™ on their own website via a compliant carousel or an embeddable widget.

Reviews on Google and Yelp lack the disclosures required for them to be used as advertisements under the SEC Marketing Rule, so advisors cannot direct prospects to them. The bigger risk is solicitation. In FINRA Regulatory Notice 17-18, FINRA treats only unsolicited third-party comments as outside Rule 2210, which means the act of asking for a review can trigger disclosure requirements those platforms do not support. Securities attorney Max Schatzow has noted that asking clients to leave a Google review may be deemed an advertisement by the SEC.

We also continue to hear from firm leaders who invited clients to review them on Google and later realized their Google Business Profiles had become toxic, containing promissory language and content prohibited by the Marketing Rule. Add to that: Google prohibits compensating reviewers (the SEC permits it with disclosure), Yelp penalizes businesses that ask for reviews, and removing a bad actor on Google requires a formal legal filing.

Wealthtender designed its platform for full compliance with the SEC Marketing Rule. We could enable Google submissions tomorrow; that is not the point. We are not in the business of doing it anyway and asking forgiveness later. Learn more about Google Business Profiles and Google Reviews for advisors, or how to import Google Reviews to Wealthtender.

Have compliance questions?

Email yourfriends@wealthtender.com or schedule a 1:1 with Wealthtender Founder & CEO Brian Thorp, an NSCP SEC Marketing Rule Working Group member.

The industry-first story, the facts, and an SME to quote

Wealthtender built the first financial advisor review platform designed for SEC Marketing Rule compliance. Here is the quick-reference for reporters covering advisor marketing and compliance.

Fast facts

- First financial advisor review platform designed for SEC Marketing Rule compliance (launched 2021).

- InvestmentNews 5-Star Technology Award (2025) and ThinkAdvisor Luminaries Award (2025).

- Top-rated in the T3 Advisor Software Survey (2023 and 2024).

- Reviews are certified with required disclosures (client or non-client, compensated or not, conflicts).

- Founder & CEO Brian Thorp is an NSCP member and sits on its SEC Marketing Rule Working Group.

Press inquiries or an interview with Brian: yourfriends@wealthtender.com · Brian on LinkedIn · schedule a Zoom.

Selected coverage

Michael Kitces, Nerd’s Eye View called client testimonials “such a powerful marketing tool” and their return to advisor marketing “inevitable.”

WealthManagement.com covered the industry debate over reliance on Google Reviews and the call for SEC vigilance (Feb 2024).

NSCP Currents published Brian Thorp on compliant testimonial marketing (Feb 2022, reprint PDF).

Original research, free to cite

Wealthtender publishes original consumer research. You are welcome to cite it with attribution and a link.

2025 Study: How Americans Find and Hire Financial Advisors. A survey of 500 U.S. adults earning $100K+ found 96% research an advisor online even after a referral, 83% read online reviews and awards, and 25% use AI tools like ChatGPT to start their search.

2025 Voice of the Client Study. An analysis of client reviews finds nearly 90% focus on relationship quality, planning, and emotional factors, while only about 1 in 10 center on investment performance.

What a Certified Advisor Review™ means, and why reviews matter

When your life savings could be at stake, you deserve transparency. A Certified Advisor Review™ gives you more than a star rating.

Unlike a typical online review, every Certified Advisor Review™ is published with clear, prominent disclosures: whether the reviewer is a client or another acquaintance, whether they were compensated, and whether any conflicts of interest exist. That context helps you weigh each review honestly. You can read every review for an advisor on their Wealthtender profile, and search a nationwide map of advisors who have earned reviews.

View the map of highly-rated advisors

Why reviews matter when choosing a financial advisor

Reviews have become central to how people choose local businesses and professionals. In a BrightLocal survey, 87% of consumers read online reviews for local businesses, up from 67% a decade earlier. In a Podium survey of 1,543 consumers, 88% said reviews played a role in discovering a local business and 41% ranked reviews among the three most important factors when choosing one. Other findings advisors should note:

- 58% would travel farther to a business with better reviews.

- 47% are willing to pay more at a business with higher reviews.

- Over 60% are likely to leave a review after a good experience when the business follows up with a link by email.

As technology writer David Pogue observed in Scientific American, the era of one-way marketing is over now that the masses are conversing with one another.

It depends. In Wealthtender’s 2025 study of 500 U.S. adults earning $100K+, 17% consider “no online reviews” a red flag and 33% are concerned about negative reviews. Newer advisors, or those who recently moved from a large firm, may simply have fewer reviews so far, and some advisors are prohibited by their state from asking clients to write reviews through no fault of their own. That said, if an advisor has practiced for several years and has no online presence or reviews at all, it may signal less focus on client satisfaction or digital sophistication.

A great deal, and increasingly so. In Wealthtender’s 2025 study of adults earning $100K+ who plan to hire an advisor, researching an advisor’s reputation by reading online reviews and awards was the single most popular next step after a referral (83%). Even when an advisor came highly recommended, 96% said they would still research that advisor online, 61% consider positive reviews on an independent website essential to judging reputation, and 50% want to read reviews before they even make contact.

Most people think so. In the same study, 61% consider positive reviews on an independent website essential to evaluating an advisor, while only 36% place similar weight on testimonials shown on the advisor’s own site, since businesses tend to display only their most flattering ones. Independent reviews offer unfiltered perspectives, and on a platform like Wealthtender every review also carries the SEC-required disclosures (client or non-client, compensated or not, any conflicts), so you can judge how much weight to give each one.

Mostly the human side of the relationship. Wealthtender’s 2025 Voice of the Client Study found that nearly 90% of client reviews focus on relationship quality, planning advice, and emotional factors like reduced stress and peace of mind, while only about 1 in 10 center on investment or portfolio performance. Reviews reveal how an advisor communicates, follows through, and supports clients through life’s transitions, the kind of insight you cannot get from marketing materials alone.

A helpful review gives future clients real insight into what it’s like to work with an advisor. Here are our tips for writing one:

Additional resources & FAQs

The SEC Marketing Rule, in plain language

Background and answers for advisors, compliance teams, and reporters getting up to speed.

In 1961, the SEC issued a rule prohibiting advisors from using client testimonials, concluding such an advertisement would “constitute a fraudulent, deceptive, or manipulative act.” The prohibition guarded against cherry-picking five-star reviews, but for six decades it also silenced satisfied clients while reviews of doctors, lawyers, and other professionals flourished online.

In 2019 the SEC acknowledged the aging rule did consumers a disservice by denying them a way to evaluate advisors the way they research other professionals. The modernized Investment Adviser Marketing Rule followed.

The SEC Marketing Rule lets advisors give investors useful information to evaluate advisers and advisory services, subject to conditions designed to prevent fraud. Announcing it on December 22, 2020, the SEC acknowledged that technology and consumer expectations had changed dramatically. SEC Chairman Jay Clayton said the rule would improve the quality of information available to investors.

It removed the severe limits on advisor reviews while preserving disclosure and fairness conditions.

The rule became effective May 4, 2021, with a compliance deadline of November 4, 2022. Advisors including client reviews in advertising must work with their compliance officers to meet the SEC’s disclosure and oversight requirements, including clear and prominent disclosure of:

- Whether a review is from a client or non-client

- Whether the reviewer was compensated, and how (cash or otherwise)

- Any conflicts of interest, including a description

- A written agreement between advisor and reviewer, unless the reviewer receives less than $1,000 (cash or otherwise) within 12 months

These requirements apply even to a short post such as a tweet.

Because Yelp’s terms prohibit businesses from soliciting reviews, advisors cannot ask clients to review them there. On Google, many advisors have unsolicited reviews, which is fine and can bring SEO benefits, but because Google and Yelp reviews lack the SEC-required disclosures to be used as advertisements, advisors cannot direct prospects to them.

Advisors may advertise ratings from third-party firms, subject to disclosures and conditions. The SEC anticipates roughly 50% of advisors will use third-party ratings. Key expectations include clearly and prominently disclosing the rating’s date, the period it covers, the identity of the third party that produced it, and any compensation involved. The advisor must reasonably believe the survey made it equally easy to give favorable and unfavorable responses, and the rating firm must be unaffiliated and in the business of preparing ratings.

Working with reviews: practical compliance questions

Educational only, not legal advice. Wealthtender encourages advisors to confirm their firm’s approach with their compliance team and counsel.

The three required disclosures (whether the reviewer is a client or non-client, whether compensation was paid, and any material conflicts) must be clear and prominent. The SEC expects them in the same font size as the review and visible alongside it, effectively part of the review itself, not hidden or accessible only through a link. The SEC also acknowledges the character limits of some platforms and notes that succinctly providing disclosures promotes their salience. Crafting your disclosures.

Review each new review through a regulatory lens. The SEC prohibits promoting reviews that:

- Include an untrue statement of material fact, or omit a fact needed to keep the statement from misleading

- Include a material statement you cannot reasonably substantiate on demand by the Commission

- Would likely create an untrue or misleading implication about a material fact

- Discuss benefits without fair and balanced treatment of material risks or limitations

- Reference specific investment advice that is not presented in a fair and balanced way

- Include, exclude, or frame performance results in a way that is not fair and balanced

- Are otherwise materially misleading

Most reviews simply reflect a client’s perception of your character and experience, which is straightforward to address with a disclosure unique to that reviewer. If a prohibition is triggered, discuss options with your compliance team, such as redacting the prohibited language with an explanatory disclosure, or not publishing the review. For a material statement of fact (for example, a claim about how a portfolio is invested), consider documenting your substantiation. Reviews on Google or Yelp that contain prohibited content cannot be promoted, and linking to them could be viewed by the SEC as fraudulent or deceptive.

Not necessarily. The SEC would not attribute a third-party review to you if you edit it based on preestablished, objective criteria documented in your policies and procedures (for example, removing profanity, defamatory or offensive statements, spam, unlawful or infringing content, or correcting a factual error) that are not designed to favor or disfavor you. This mirrors the FTC Consumer Review Fairness Act.

Firms may also consider a policy that excludes all endorsements (non-client reviews), not only unfavorable ones, from their marketing, provided the policy is not designed to favor or disfavor the adviser and, presumably, requires publication of all client testimonials. See preparing your policies and procedures. Wealthtender clients can archive a review that falls outside their policy (see the next answer).

If you receive an unsolicited review that falls outside your firm’s policy, or that you believe is inappropriate under the SEC Marketing Rule or FTC Consumer Review Fairness Act, you can archive it:

- Sign in to your Wealthtender account

- In the right sidebar, click Dashboard

- Click My Reviews in the left sidebar

- Locate the review and click Options in the Archive column

- Provide the rationale for archiving and click Submit

Yes. Beyond testimonials from current clients, the SEC permits endorsements from past clients and non-clients when accompanied by disclosures that clearly indicate the reviewer is not a client. Non-client reviews can highlight your expertise and character, for example from experts in your niche or leaders of nonprofits where you volunteer. They can be especially valuable for advisors who recently changed industries, younger advisors with strong references, or advisers whose former clients could not transition due to a non-solicitation clause.

Yes, with disclosure. Any review from a compensated reviewer must clearly disclose the arrangement, including non-cash compensation such as gift cards or an advisory-fee reduction, and a written agreement is required if you provide more than $1,000 in value within a 12-month period.

- Cash: disclose the amount paid, including any reimbursed expenses.

- Non-cash: for a fee reduction, disclose the time period and discount percentage; otherwise disclose the dollar value.

Be mindful of timing: an incidental dinner, gift, or other consideration near the time a review is written could be viewed by the SEC as compensation for the review, so many firms disclose any such value provided around that time. Also check the platform’s own rules, since Google prohibits compensating reviewers.

Beyond a review from a family member, common examples include:

- A client who is a close personal friend. A short disclosure such as “John and I have been friends since high school” adds helpful context.

- A non-client friend writing about your character in general.

- Someone with a referral arrangement with you, such as an accountant who benefits from praising you.

As reviews arrive, do a quick check for anything beyond a typical client relationship worth disclosing. Framing it as helpful context rather than boilerplate builds trust with prospects and keeps you transparent with regulators.

Realistically, existing clients are far more likely to write favorable or neutral reviews, and a non-client you invite is very unlikely to write something negative. If a negative review does arrive, take a breath. Then take another. (Seriously. And if your first three-star-or-lower review lands on your Wealthtender profile, email yourfriends@wealthtender.com and we’ll send you a one-year premium subscription to the Calm meditation app. Also seriously. We’ll get through this together.) Once your emotions settle, consider the reviewer’s perspective and whether there is a practical remedy you can offer, ideally by phone to keep it human. You can also use the additional-disclosures field to add your own measured perspective, taking the high ground. The best antidote to one negative review is many positive ones.

Consumers own the content they write and may edit or delete it, but the SEC could frown on encouraging a reviewer to revisit a review, so consult your compliance team first, and be prepared to discuss the circumstances with the SEC even if a review is later deleted.

Establish your policy upfront. The consensus among securities attorneys familiar with the Marketing Rule is to never reply to reviews on platforms like Google and Yelp, since doing so heightens your risk of entanglement and adoption, subjecting you to the rule’s prohibitions and disclosure requirements those platforms cannot support. Whether thanking a reviewer or addressing a concern, handle it individually offline by phone or email. A few neutral or negative reviews are healthy, since consumers tend to be skeptical of professionals with only perfect reviews.

Yes. Beyond the SEC’s requirements, hybrid or dually registered advisors should also satisfy FINRA Rule 2210(d)(6), which fits neatly within the SEC framework. If a review discusses your investment advice or performance, it must prominently disclose that the testimonial may not represent other clients’ experience, that it is no guarantee of future performance or success, and, if more than $100 in value was paid, that it is a paid testimonial. If a review discusses a technical aspect of investing, the reviewer must have the knowledge and experience to form a valid opinion. FINRA disclosures can sit alongside the SEC disclosures, or be reached through a clearly marked link such as “important testimonial information.”

The SEC has issued a number of Risk Alerts and, more recently, press releases announcing enforcement actions. You can review past Risk Alerts and enforcement actions via this list of SEC Marketing Rule links.

SEC Marketing Rule Education Series

Promoting third-party ratings & awards · Asking for testimonials & endorsements · Promoting your testimonials · Preparing your policies & procedures · Crafting your disclosures

Online reviews: Wealthtender vs. advisor websites vs. Google & Yelp

How Certified Advisor Reviews™ compare with other places advisors and consumers encounter reviews.

| Wealthtender | Advisor website | Google Reviews | Yelp | |

|---|---|---|---|---|

| Designed for SEC Marketing Rule compliance? | Yes | Maybe | No | No |

| Profile pages exclusive to each advisor? | Yes | N/A | No | No |

| Can I solicit reviews? | Yes | Yes | Yes | No |

| Potential SEO/AEO benefits? | Yes | Yes | Yes | Yes |

| Add the SEC’s “clear and prominent” disclosures? | Yes | Yes | No | No |

| Can reviews be displayed anonymously? | Yes | Yes | No | No |

| Easily request removal of SEC “bad actors”? | Yes | Yes | No | No |

| Platform reviewed by an experienced securities attorney? | Yes | Maybe | No | No |

| Import and display reviews collected elsewhere? | Yes | Yes | No | No |

| Turn reviews off and keep all other benefits? | Yes | N/A | No | No |

| Cancel your account and remove all reviews? | Yes | N/A | No | No |

“Financial advisors embracing online reviews will lead the industry in attracting new clients throughout the historic transfer of wealth from Baby Boomers to Millennials over the next decade.”

Brian Thorp, Wealthtender Founder & CEO

Ready to grow with compliant client reviews?

Join 900+ advisors and firms using Certified Advisor Reviews™ to strengthen their reputation, build authority in their specialties, and attract their ideal clients.

Free playbook and education series included. Reviews are always optional.

Wealthtender, Inc. · 1401 Lavaca St. #893 · Austin, TX 78701

Certified Advisor Reviews™, Review Sync™, Review Rollup™, and Review Allocate™ are trademarks of Wealthtender, Inc. Wealthtender does not provide investment or legal advice; information here is educational. Third-party links are provided for convenience and are not endorsements. Wealthtender is a trusted, independent financial directory and educational resource governed by our Editorial Policy, Integrity Standards, and Terms of Use. While we receive compensation from featured professionals (a natural conflict of interest), we operate with integrity and transparency to earn your trust. Wealthtender is not a client of the advisors or firms featured. Testimonials may not be representative of other clients’ experiences and do not guarantee future performance or success.