Discover financial advisors trusted by residents of Key West, Florida in the only local directory featuring 5-Star Certified Advisor Review™ recipients and Wealthtender Voice of the Client Award™ winners—recognition earned for exceptional client feedback. Compare fiduciary, fee-only advisors, CFP® professionals, and specialists to find the right fit for your unique financial needs.

Whether you have lived in Key West for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Key West featured on Wealthtender you may want to add to your shortlist.

Featured Key West Financial Advisors

As you prepare to interview financial advisors in Key West who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Key West

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Key West.

The Benefits of Hiring a Financial Advisor in Key West

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Key West, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Key West? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Key West Financial Advisor

Before hiring a financial advisor in Key West, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Discover financial advisors trusted by residents of Wilkesboro, North Carolina in the only local directory featuring 5-Star Certified Advisor Review™ recipients and Wealthtender Voice of the Client Award™ winners—recognition earned for exceptional client feedback. Compare fiduciary, fee-only advisors, CFP® professionals, and specialists to find the right fit for your unique financial needs.

Whether you have lived in Wilkesboro for years or recently moved to town, you may need help finding the right financial advisor in the community best suited for your individual needs.

It’s important to first consider your own financial planning priorities before choosing an advisor. Here are a few quick tips to help you get started along with financial advisors in Wilkesboro featured on Wealthtender you may want to add to your shortlist.

Featured Wilkesboro Financial Advisors

As you prepare to interview financial advisors in Wilkesboro who may be right for you, get to know local financial advisors featured on Wealthtender.

📍 Map: Financial Advisors with their Primary Office Location in Wilkesboro

Double-click (or pinch the map on mobile devices) to zoom in and expand the details for financial advisors whose primary office location is in Wilkesboro.

The Benefits of Hiring a Financial Advisor in Wilkesboro

Hiring a financial advisor can be a great move to help you build a long-term investing strategy. Advisors can help you build an investment portfolio to meet your financial goals and help you plan appropriately for retirement.

As a resident living in Wilkesboro, hiring a financial advisor who lives nearby and understands the local economy, cost of living, and regional employers can be quite valuable, especially if your individual circumstances are deeply tied to such factors.

Do you work for one of the largest employers in Wilkesboro? If so, there’s a good chance the local financial advisor you hire will also have other clients who work there. This knowledge could prove valuable if they are already familiar with your employee benefits, such as a 401(k) plan, Health Savings Accounts, and other components of your total compensation package.

When you reach out to financial advisors you’re considering hiring, let them know where you work and ask if they are familiar with your employer’s unique benefits and compensation structure.

Quick Tips For Hiring an Wilkesboro Financial Advisor

Before hiring a financial advisor in Wilkesboro, here are a few quick tips to help you find the best advisor for you.

1. Decide Which Services You Need

Before hiring an advisor, determine what services you need from them. Whether it’s full-service investment management or a plan focused on a specific area of your finances, put together a list of what you’d like help with before contacting an advisor.

Though most people use a financial planner simply to invest for retirement, this is only a small part of what many advisors offer. Here’s a quick rundown of potential services a financial advisor may offer you:

Budgeting and money management

Debt management

Insurance planning

Retirement planning

Other investment planning

Inheritance planning

Estate planning

Tax planning

As you can see, financial advisors can help you with your entire financial picture, not just investing. As you start to plan for life’s bigger milestones, you should consider finding a financial advisor that specializes in those areas.

Finding the right advisor can help you minimize risk, maximize gains and take advantage of tax breaks while investing for your future. They can also help you protect your assets with the right kinds of insurance and help you pass on your financial legacy with a proper estate plan.

2. Consider Your Budget and Payment Preferences

Once you have a list of services you would like, review the fee structures financial advisors offer. Finding a balance between the services you need and the cost of those services will help narrow down the field of advisors you may want to work with.

If you are looking for a full-service advisor to manage all of your investments, consider searching among fee-based financial advisors. If you want to manage your money yourself, consider the flat fee and monthly subscription advisors for ongoing support.

3. Interview Multiple Financial Advisors

Once you have chosen the services and fee structure you prefer, it’s time to contact a few advisors and interview them. Here are questions to ask financial advisors:

What services do you provide?

What are all the ways you get paid? (fee transparency)

What is your investment strategy?

How do you measure investment performance?

How do we communicate about my plan?

Interview multiple advisors to get a feel for who you want to work with. A combination of fees, services, and customer service will help you determine the best fit for your financial advice.

4. Review Financial Advisor Credentials

Once you find an advisor (or two) you feel comfortable with, it’s always a good practice to check their credentials and the firm’s details. You can do this at the Investment Adviser Public Disclosure (IAPD) website.

You can check both the individual and the firm to view their background and experience details, as well as any disciplinary action taken against them or their firm.

As licensed financial professionals, there is oversight into how financial advisors conduct business, so running a quick (free) check on them is recommended.

For additional information about advisor credentials, read our article to learn the most popular designations held by financial advisors, as well as specialized credentials which may be important to consider if you have unique financial planning needs.

Frequently Asked Questions & Additional Resources

How do I know if I’m ready to hire a financial advisor?

You should strongly consider hiring a financial advisor if you have a significant amount of money available for saving or investing. This could occur after years of making annual contributions to a retirement plan like a 401(k) through your employer or suddenly if you receive a large inheritance or sell your house for a large profit.

But even if you don’t have a lot of money saved, many financial advisors and planners provide reasonable pricing options and valuable services you should consider, especially if you’re facing a significant life event. For example, if you’re starting a new job, getting married, starting a family, getting divorced, lost your job, starting or selling a business, or approaching retirement age, working with a trusted financial advisor or planner may prove worthwhile.

Before I hire a new financial advisor, should I fire my current advisor?

You don’t need to fire your current advisor before beginning your search for a new financial advisor. In fact, your new advisor can help coordinate the transition of your assets from your previous financial advisor.

Where can I read reviews about financial advisors written by their clients to help me decide if I should hire them?

After 60 years of regulatory prohibition of financial advisor reviews in the US, a rule issued by the Securities and Exchange Commission (SEC) became effective on May 4, 2021 that means both financial advisors and directory websites that help consumers search for a financial advisor can collect and display financial advisor reviews, an important factor worth considering when choosing who you’ll hire to manage your investments and life savings.

Wealthtender is the first independent advisor review platform designed to be fully compliant with the new SEC rule, and we look forward to helping you evaluate financial advisors based on reviews written by their clients.

I’m a local financial advisor interested in being featured in this guide. How do I get started?

Thanks for your interest. We look forward to learning more about your practice and helping you attract your ideal clients where you may be a good fit based on their individual needs and circumstances. Please click here to learn how you can join local financial advisors featured on Wealthtender.

Brian is CEO and founder of Wealthtender and Editor-in-Chief. He and his wife live in Austin, Texas. With over 25 years in the financial services industry, Brian is applying his experience and passion at Wealthtender to help more people enjoy life with less money stress. Learn More about Brian

Do you work at Home Depot?

Get expert insights from financial advisors who specialize in helping Home Depot employees and executives make the most of their compensation package and benefits.

Looking for a financial advisor who specializes in working with Home Depot employees? You’re in the right place. Below, you’ll find advisors who understand Home Depot benefits and compensation — along with their answers to common financial questions from Home Depot employees and executives.

Whether you recently joined Home Depot or you’ve advanced into a management or executive leadership role over a multi-year career, making smart decisions about your income and Home Depot benefits can have a lasting impact on your financial future. For example:

✅ Do you know the right moves to get the greatest value from the Home Depot benefits available to you?

✅ If you’re thinking about leaving Home Depot for another job or planning to retire in a few years, are you taking the right steps today to receive all the compensation and benefits you’ve earned?

Key Takeaways

1

Home Depot’s PCRA Brokerage Within the FutureBuilder 401(k) Is Widely Overlooked but Highly Valuable

The PCRA Trust Brokerage account available inside the FutureBuilder 401(k) is not widely known or utilized by Home Depot employees. When used correctly, it can significantly expand investment options beyond the standard fund lineup and allow for more tailored portfolio management.

2

Concentrated Home Depot Stock Exposure Is One of the Biggest Hidden Risks for Executives

Many Home Depot executives accumulate a large pile of vested HD shares that sit idle for years, on top of ongoing grants of stock options, RSUs, and PSUs. Advisors working with these employees frequently prioritize tax-efficient diversification strategies early in the relationship to reduce that concentration risk.

3

Tenure and Age at Departure Can Determine Whether Unvested Equity Is Lost or Preserved

At Home Depot, the combination of years of service and retirement age can affect whether stock options continue to vest after an employee leaves. Understanding the full value of compensation that would be forfeited upon resignation also gives executives a stronger negotiating position with a prospective new employer.

Why Home Depot Employees Work with a Specialist Financial Advisor

Throughout the year, Home Depot provides its employees and executives with updates about their benefits, ranging from health insurance and health savings accounts to retirement plans like a 401(k) and deferred compensation, along with equity compensation such as restricted stock units (RSUs), stock options, and an employee stock purchase plan. While the company offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Home Depot who specialize in helping Home Depot employees make the most of their income and benefits.

Whether you work at one of Home Depot’s offices, from a regional hub, or remotely from home, you may have questions about your compensation package and benefits better suited for a financial professional who can offer unbiased advice and guidance.

Sensitive topics — like the steps you should take before quitting your job at Home Depot to work elsewhere, protecting yourself in advance of a corporate layoff, or deciding when you should plan to retire — are all conversations that may be more comfortable with a trusted financial advisor.

Should You Hire a Home Depot Specialist or a Local Financial Advisor?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it can be harder to find a financial advisor who specializes in serving Home Depot employees. Fortunately, many financial advisors offer virtual services, so you can meet online no matter where you (or they) live — which means you can hire a specialist financial advisor who lives hundreds of miles away if their knowledge and experience working with Home Depot employees is the better fit for your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Home Depot employees to help them make smart decisions, get the most value from their compensation and benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Have a question not yet answered? Use the form below to submit your question. You can also contact financial advisors directly to set up an introductory call or contact them with your questions.

Q&A: Financial Planning Tips for Home Depot Employees & Executives

In this section, you’ll learn how you can make the most of your Home Depot employee benefits and gain valuable tips from financial advisors who specialize in working with Home Depot employees and executives.

Patrick Lawson is a financial advisor based in Athens, GA who specializes in offering financial planning services to Home Depot employees. Patrick helps clients understand and make informed decisions regarding their Home Depot benefits and compensation package so they can enjoy life and feel confident about their financial future.

QAs a financial advisor with experience helping Home Depot employees save for their retirement, how do you help them make the most of their employee benefits?

First and foremost, every person has different values and personal objectives, so we work with them to help build on their unique plan, and a large piece of that is incorporating their benefits into the mix.

We comb through the robust benefits offered to Home Depot executives to provide a bespoke solution tailored to each client’s individual needs and objectives. Not only does this include helping clients understand their medical and life benefits for them and their families but also utilizing and managing the PCRA brokerage piece to their 401k plans while seeking to maximize the generous company match, making sense out of their stock options, RSUs, PSUs and Restorations Plan and developing implementation strategies designed to support their personal financial planning objectives.

Overall, there is a lot that goes into being an executive at the Home Depot, and many executives may find it valuable to work with a professional to help evaluate these decisions. A “thought partner” to holistically bring it all together in a clear manner is what we do at Branch Partners. Our goal is to make sense of their benefits and incorporate them into a clear, actionable plan.

QWhen you first speak with a Home Depot employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

– What is it that is important to you? Financial and non-financial.

– Are you fulfilled in what you do? Tell me about it.

– How long have you been with the Company and what is your vision for how much longer you will stay?

– Do you feel like you have a good handle on your executive compensation, how it ties into accomplishing your personal financial objectives?

– Do you have an idea for how your stock compensation impacts your tax picture?

– Have you worked with an advisor before? What worked well, what didn’t?

– What are you looking for out of a financial partner?

QIs there a particular benefit available to Home Depot employees you feel isn’t as well utilized or understood by employees as it should be?

In my experience, the PCRA Trust Brokerage account offered through the FutureBuilder 401(k) is often underutilized or misunderstood by employees. If used appropriately, this can significantly expand the investment options available beyond the core plan menu and provide additional flexibility in portfolio implementation.

QBeyond Home Depot employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients (e.g. stock, education savings, health savings)?

Life and disability benefits. It is important to understand how much life and disability coverage is provided and paid for by the Company. This is great starter coverage, but depending on your family, lifestyle and goals, it is possible that it may not be enough. A full analysis is an appropriate step we take with all of our clients to determine if their family and assets are properly covered.

QFor Home Depot employees thinking about leaving the company to accept a job elsewhere, what actions do you recommend they take before resigning and shortly thereafter?

At many companies, Home Depot included, there is significance around tenure with the Company and age at which you are retiring. This could mean the difference between continued vesting of options or not. This is important to understand.

Additionally, it is equally important to understand what you may be “leaving on the table” if you were to leave the Company. We help executives understand what that amount is that can be beneficial in negotiating tactics for future employers.

QFor Home Depot employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

You spent your career living off a paycheck — someone else’s promise to pay you, on time, every time. Retirement means living off something you built yourself. That’s a different relationship with money, and it can feel unsettling at first.

But here’s what I want clients to remember: a well-built portfolio isn’t a pile of money you’re slowly spending down. It’s a living, working asset — more like a farm than a savings account. It produces things. It grows things. And when you need income, we harvest thoughtfully — never taking more than the farm can sustainably give, always leaving enough to keep growing.

The paycheck was someone else’s farm. This one is yours. We help clients grow, nurture and harvest what they have responsibly planted.

QFor Home Depot employees who have managed their finances on their own to this point, what would you suggest they consider to help them decide if they should begin working with a financial advisor at this stage in their lives?

The further you grow in the Company, the more is demanded and expected of you. With those expectations come reward — bigger stock option, RSU and PSU grants. This is all great, but it creates complexity – complexity that you may not have time to handle on your own. One thing I tell my executive clients often is that “you wake up every morning thinking about what you have to do to polish the Home Depot brand and you are great at it. You should go do that and not have to think about your own personal finances.”

Much like you do in many other aspects of your life, delegate this work to a professional who knows your financial life inside and out.

QWhat are some of the unique financial planning challenges you commonly see among your clients who are Home Depot employees and how do you help them overcome these obstacles?

Understanding their executive compensation. That entails understanding what they have, when it is accessible to them, following Company regulations such as trading windows, what the tax impacts are of transacting and then ultimately what to do with the proceeds! How much should we allocate to college savings, HSA, tax withholding, brokerage, etc.?

QWhat questions do you recommend Home Depot employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

What value do you receive for the price you pay?

How do you incorporate these various forms of compensation into my overall financial picture?

How do you charge clients?

QIs there anything that comes up frequently in your initial meeting with Home Depot employees that surprises you?

It always surprises me how much exposure they have to Home Depot stock. Not only does the Company sign their paychecks and support their family’s healthcare needs, but they also have a pile of vested HD shares that have been sitting there idle for years. Not to mention the hundreds of shares that will vest in the coming year! The stock price has done incredibly well, but I believe proper diversification is key to any successful financial plan. One of the early common conversation topics we have is around diversification and tactics on how to diversify in a tax efficient manner.

QIs there a particularly memorable experience or a moment you recall with a client who worked at Home Depot when you realized they have unique opportunities and circumstances when it comes to their financial planning needs?

In many situations, I find employees and executives may not fully understand all of the benefits and planning opportunities available to them. And it is not their fault. There is just so much to learn and understand that they don’t have the time to learn it themselves.

Considering a financial advisor who specializes in working with Home Depot employees?

Are you a financial advisor who specializes in working with employees at Home Depot or another large company?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with employees at Home Depot or another large company. (Subject to availability and terms.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender

Ask a Financial Advisor Your Home Depot Benefits & Career Questions

Get answers from the Wealthtender network of financial professionals and educators.

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

Brian Thorp is the founder and CEO of Wealthtender and serves as Editor-in-Chief. With over 25 years in the financial services industry — including nearly 22 years at Invesco, where he led strategic partnerships with wealth management firms representing more than $100 billion in assets — Brian founded Wealthtender to help people find financial advisors they can trust and make more informed money decisions.

A member of the National Society of Compliance Professionals and its SEC Marketing Rule Working Group, Brian was recognized by WealthManagement.com as one of its “Ten to Watch in 2024” for his work reshaping how financial advisors market their services. He holds a B.B.A. in Finance from The University of Texas at Austin.

Get expert insights from financial advisors who specialize in helping Anthropic employees and executives make the most of their compensation package and benefits.

Looking for a financial advisor who specializes in working with Anthropic employees? You’re in the right place. Below, you’ll find advisors who understand Anthropic benefits and compensation, along with their answers to common financial questions from Anthropic employees and executives.

Whether you recently joined Anthropic or you’ve advanced into a management or executive leadership role over a multi-year career, making smart decisions about your income and Anthropic benefits can have a lasting impact on your financial future. For example:

✅ Do you know the right moves to get the greatest value from the Anthropic benefits available to you?

✅ If you’re thinking about leaving Anthropic for another job or planning to retire in a few years, are you taking the right steps today to receive all the compensation and benefits you’ve earned?

Key Takeaways

1

Equity Is the Most Valuable and Most Misunderstood Part of Anthropic Pay

For many Anthropic employees, equity compensation (including ISOs, NSOs, and RSUs) is the largest piece of their net worth, yet it’s often the least understood. A specialist advisor can help you work through vesting schedules, exercise windows, and the tax treatment that determines how much of that value you actually keep.

2

Concentrated Stock Is the Top Financial Risk for Anthropic Employees

When Anthropic equity makes up more than roughly 20% of your investable assets, a single adverse event at the company could erase a large share of your net worth. Calculating your concentration and building a diversification and tax plan around it is a common first step, and an especially timely one now that Anthropic has confidentially filed for an IPO.

3

Map Your Vesting and Option Exercise Windows Before You Leave Anthropic

If you’re weighing a job change, understand exactly how much unvested equity you’d forfeit and how long you have to exercise vested ISOs or NSOs after you depart. The same analysis can help you quantify what you’d be walking away from and negotiate a stronger offer with a new employer.

Why Anthropic Employees Work with a Specialist Financial Advisor

Throughout the year, Anthropic provides its employees and executives with updates about their benefits, ranging from health insurance and health savings accounts to retirement savings like a 401(k), along with equity compensation such as stock options and restricted stock units (RSUs). While the company offers many useful resources and access to knowledgeable staff who can assist with questions, you’ll also find financial professionals not affiliated with Anthropic who specialize in helping Anthropic employees make the most of their income and benefits.

Whether you work at Anthropic’s San Francisco headquarters, an office in Seattle, New York, or Washington, D.C., one of its international locations, or remotely from home, you may have questions about your compensation package and benefits better suited for a financial professional who can offer unbiased advice and guidance.

Sensitive topics, like the steps you should take before quitting your job at Anthropic to work elsewhere, protecting yourself in advance of a corporate layoff, or deciding when you should plan to retire, are all conversations that may be more comfortable with a trusted financial advisor.

Should You Hire an Anthropic Specialist or a Local Financial Advisor?

You’ll likely find dozens of nearby financial advisors well-suited to help you reach your money goals with a personalized plan. But it can be harder to find a financial advisor who specializes in serving Anthropic employees. Fortunately, many financial advisors offer virtual services, so you can meet online no matter where you (or they) live, which means you can hire a specialist financial advisor who lives hundreds of miles away if their knowledge and experience working with Anthropic employees is the better fit for your unique needs.

💡 In the Q&A below, you’ll gain insights from financial advisors who work with Anthropic employees to help them make smart decisions, get the most value from their compensation and benefits, reduce their money stress, and prepare for a comfortable retirement.

🙋♀️ Have a question not yet answered? Use the form below to submit it anonymously and watch this article for updates with answers to your questions. You can also reach out to the financial advisors below to set up an introductory call or contact them with your questions by email.

Q&A: Financial Planning Tips for Anthropic Employees & Executives

In this section, you’ll learn how you can make the most of your Anthropic employee benefits and gain valuable tips from financial advisors who specialize in working with Anthropic employees and executives.

Jump to a Financial Advisor for Anthropic Employees

Jackie Lewis is a financial advisor based in San Diego, California who specializes in offering financial planning services to Anthropic employees. Jackie helps her clients get the most value from their Anthropic benefits and compensation package so they can enjoy life and feel confident about their financial future.

QAs a financial advisor with experience helping Anthropic employees save for their retirement, how do you help them make the most of their employee benefits?

Anthropic has some great benefits and we make sure that you are taking advantage of all that they offer. This includes helping you with equity compensation, retirement account, health insurance and family benefits within their overall corporate benefits package.

QWhen you first speak with an Anthropic employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

Anthropic provides robust equity compensation packages so we help you to strategize around the best way to tax efficiently liquidate your RSUs based on your unique situation and needs. This leads to questions such as What are your goals in life? How long do you hope to stay with Anthropic? What would you like to do for your family? How well do you feel you understand your equity compensation? Do you have an idea of what taxes you will owe with your total compensation package?

QIs there a particular benefit available to Anthropic employees you feel isn’t as well utilized or understood by employees as it should be?

We help you to understand your equity compensation and put together a strategic plan to find the most tax efficient way to liquidate this compensation so that you can use this to fund your goals whether they be financial freedom, a home purchase, travel plans, etc.

QBeyond Anthropic employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients?

Anthropic provides a significant portion of your compensation through their equity compensation so we guide you through how best to leverage them during an open window so that you pay the lowest tax possible and have a multi-year plan at your finger tips.

QFor Anthropic employees thinking about leaving the company to accept a job elsewhere, what actions do you recommend they take before resigning and shortly thereafter?

If you’re thinking of leaving Anthropic, you should consider the impact on your equity compensation as you have a window to take advantage of them. In addition, any first-year bonus that may need to be repaid, and whether they are prepared with enough emergency savings if making a move to a smaller tech company.

Another consideration is health insurance. Health insurance will end at month-end of your employment. Knowing you have another job starting in a few weeks vs. a few days may leave you open to a medical emergency if coverage is not continuous. Finally, 401(k) employee contributions and HSA contributions are a sum game across employers. If you contribute the maximum to the Anthropic 401k and then move to a new employer, you will need to wait until the next year to start contributing to the new 401(k).

QFor Anthropic employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

Many of our tech professional clients look to make work optional around age 50 to age 55. This means a time of needing taxable investments and medical coverage. We work with our clients to understand COBRA and health exchange options years in advance, so we have a good year of emergency savings ready for the first big moment of this next phase in life. Then, it’s really about seeing how you can lean into your values and passions while keeping the finances in mind.

Some of our clients go on to create their own startups or decide on consulting or volunteer work, etc. ‘Retiring’ isn’t about sitting around. These different adventures may require cash needs to get going, so we make sure we understand what will be going out the door for this as well. We help them structure their cash flow needs so they can see how they are doing spending-wise compared to what we planned for.

QFor Anthropic employees who have managed their finances on their own to this point, what would you suggest they consider to help them decide if they should begin working with a financial advisor at this stage in their lives?

An advisor can help with short-term decision-making such as equity compensation decisions, tax advantaged guidance, etc. and also with bigger-picture thinking (i.e. creating a framework so you can see the direction all your hard work is taking you, and make sure your money behaviors are aligning with your life goals). A client is often already doing many of the right things and the value of the planning process is to put things in a broader framework to allow for proactive/intentional decisions to be made as well as being a sounding board and accountability coach for the client.

We encourage DIY investors to consider the cost of NOT getting a second opinion. Investment management is one thing, but retirement planning has incredible nuance to it that many people overlook such as:

How will my investments be taxed? Can I minimize my lifetime taxation? Am I taking too much (or not enough) risk in the markets?

What is my plan to turn my assets into income? What are the tax implications of doing that?

Am I going to run out of money? How should I deal with Inflation? What about long-term care?

Are my beneficiary designations up to date? Do I understand what’s going to happen to my assets when I pass?

Do I need life insurance? Do I have enough or too much? Should I keep these old policies?

There are a number of different areas that a Certified Financial Planner (CFP) can provide incredible value to a recent retiree, even if they choose to continue to manage their own investments.

QWhat are some of the unique financial planning challenges you commonly see among your clients who are Anthropic employees and how do you help them overcome these obstacles?

A good, high-paying job in tech can feel a bit like golden handcuffs sometimes and it can be hard to imagine walking away. But, if you want to prepare for an exit or a shift to a different industry, we can create a pathway to ease the transition. In a role with equity compensation, a challenge can be to define how much to rely on that compensation in the plan. It’s variable and can be hard to quantify, but can be significant. So, having a firm structure based on a client’s comfort with the exposure and how it’s treated in the plan is important.

QWhat questions do you recommend Anthropic employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

Are you a fiduciary? Do you have to act in my best interest? Will you be providing comprehensive financial planning or just investment management? What will I pay in fees? Are there any hidden fees in the products you’re recommending?

Considering a financial advisor who specializes in working with Anthropic employees?

Investment advisory services are offered through Mariner Platform Solutions (“MPS”), an SEC registered investment adviser. Wealth With Options is a separate business entity used for marketing purposes. The separate business entity is not owned, controlled by, or affiliated with MPS and is not registered with the SEC. For additional information about MPS, including fees and services, please contact MPS or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you invest.

Tom Lo is a financial advisor based in San Carlos, CA who specializes in offering financial planning services to Anthropic employees. Tom helps clients get the most value from their Anthropic benefits and compensation package so they can enjoy life and feel confident about their financial future.

QAs a financial advisor with experience helping Anthropic employees save for their retirement, how do you help them make the most of their employee benefits?

For Anthropic employees who want to get to financial independence, I help you make the most of your employee equity including ISOs, NSOs, and RSUs. I help you diversify risk, minimize taxes, and make the most of your Anthropic equity so you can achieve financial independence.

QWhen you first speak with an Anthropic employee, what questions do you like to ask to better understand their unique circumstances and determine how you can best help them achieve their goals?

What are your big life goals? When do you want to get to financial independence? What financial goals do you have for yourself and your partner e.g., buy house? What financial goals do you have for your children e.g. pay for college? What financial goals do you have for your lifestyle e.g., travel? What vested and unvested Anthropic equity do you have?

QIs there a particular benefit available to Anthropic employees you feel isn’t as well utilized or understood by employees as it should be?

Anthropic employees don’t understand your Anthropic equity including ISOs, NSOs, and RSUs as well as it should be because this is by far your most important employee benefit. I can help you understand how to diversify risk, minimize taxes, and use your Anthropic equity to reach your goals including financial independence.

QBeyond Anthropic employee benefits for retirement savings, are there other types of benefits offered by the company that you find valuable to discuss with your clients (e.g. stock, education savings, health savings)?

I find it valuable to discuss your Anthropic equity including ISOs, NSOs, and RSUs to help you so you can diversify risk, minimize taxes, and maximize the value to achieve your other financial goals.

QFor Anthropic employees thinking about leaving the company to accept a job elsewhere, what actions do you recommend they take before resigning and shortly thereafter?

For Anthropic employees thinking about leaving Anthropic, I can help you negotiate your compensation package with your new employer by quantifying the financial value of your Anthropic equity that you’re leaving on the table. I can help you understand the details of your vesting schedule including timing so you can maximize the vesting of your equity. I can help you understand how long you have to exercise ISOs and/or NSOs that you have vested but not exercised yet after you leave Anthropic and the exercise cost and taxes if you do that.

QFor Anthropic employees approaching retirement age, how do you recommend they prepare to make the transition from living off their salary to relying upon other sources of income?

I help Anthropic employees approaching financial independence understand how you can use your Anthropic equity and other assets to generate enough income to support your financial independence and with what type of lifestyle.

QFor Anthropic employees who have managed their finances on their own to this point, what would you suggest they consider to help them decide if they should begin working with a financial advisor at this stage in their lives?

For Anthropic employees who don’t have the time, energy, interest, or expertise to understand how to diversify risk, minimize taxes, and maximize value of your Anthropic equity including ISOs, NSOs, and RSUs, you should consider working with a financial planner that specializes in working with tech professionals with equity. If a financial planner can help you get 10% more value out of your Anthropic equity that you would on your own, how much would that be worth?

QWhat are some of the unique financial planning challenges you commonly see among your clients who are Anthropic employees and how do you help them overcome these obstacles?

The primary financial planning challenge among Anthropic employees is helping you understand how you can diversify risk, minimize taxes, and maximize the value of your Anthropic equity including ISOs, NSOs, and RSUs so that you can achieve your goals. I help you overcome these obstacles by helping you identify your goals and using selling and tax strategies to maximize the value of your Anthropic equity to help you reach your goals.

QWhat questions do you recommend Anthropic employees ask financial advisors they’re considering hiring to help them decide if they’re a good fit?

What percentage and number of your clients are tech professionals with equity? How many clients in total do you work with? Are you fee-only which means the client is the only one who pays the advisor? Are you a fiduciary which means the advisor is legally obligated to work in the clients’ best interest? Are you independent which means the advisor isn’t connected to a bank or broker? Do you have the Certified Financial Planner (CFP) designation which is the highest standard for financial planners?

QIs there anything that comes up frequently in your initial meeting with Anthropic employees that surprises you?

Anthropic employees not understanding the importance of the concept of concentrated stock, holding too much of a single company stock, is what surprises me. Anthropic employees are typically taking a ton of risk because Anthropic equity makes up too much of your investable assets. The risk is that something happens to Anthropic and most of your net worth vanishes.

QFor highly compensated Anthropic employees and executives, are there any special benefits you believe it’s important to take into consideration when preparing their financial plan?

The primary benefit to take into consideration when preparing your financial plan for highly compensated Anthropic employees and executives is your Anthropic equity including ISOs, NSOs, and RSUs. I want to help you diversify risk, minimize taxes, and maximize value of your equity. For executives and select employees, I want to be aware if you are subject to corporate insider rules and if so, I would look at using a 10b5-1 plan when selling Anthropic equity.

QIs there a particularly memorable experience or a moment you recall with a client who worked at Anthropic when you realized they have unique opportunities and circumstances when it comes to their financial planning needs?

I met with an Anthropic employee to talk about working together and then met a second time about eight months later. In that relatively short time, the value of his Anthropic equity increased ~600%. The skyrocketing value helped me realize that Anthropic employees have a unique opportunity to use your Anthropic equity to reach your goals likely faster than any tech employees in history.

QWhat should Anthropic employee do first since Anthropic filed for an IPO?

Anthropic employees should first calculate how concentrated you are in your Anthropic equity. Take the value of your total vested Anthropic equity and divide by the total value of your investable assets including savings, investments, retirement, and 401ks to get your concentration. If you are more than 20% concentrated in Anthropic, you need to figure out a plan for your Anthropic equity because it makes up lots of your net worth.

Considering a financial advisor who specializes in working with Anthropic employees?

The information contained within this article is provided for informational purposes only and is not intended to substitute for obtaining accounting, tax, or financial advice from a professional. Information provided in this article is not all inclusive and such information should not be relied upon as being all inclusive. In no way should this information be construed or interpreted to be advice for your specific situation. Before making any financial decision you should consider all factors and consult with a professional. This article provides general information only, and is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation and the particular needs of any specific person. In addition, investments in the stock market are subject to fluctuation, and that the price or value of any securities and investments may rise or fall and you may lose part or all of your investment. In addition, any information relating to the tax status of financial instruments discussed in this article is not intended to provide tax advice or to be used by anyone to provide tax advice. You are urged to seek tax advice based on your particular circumstances from an independent tax professional.

Are you a financial advisor who specializes in working with employees at Anthropic or another large company?

✅ Join Wealthtender and get featured as a specialist financial advisor based on your knowledge and experience working with employees at Anthropic or another large company. (Subject to availability and terms.) ✅ Sign up today and join financial advisors attracting their ideal clients on Wealthtender

Ask a Financial Advisor Your Anthropic Benefits & Career Questions

Get answers from the Wealthtender network of financial professionals and educators.

Are you ready to enjoy life more with less money stress?

Sign up to receive weekly insights from Wealthtender with useful money tips and fresh ideas to help you achieve your financial goals.

Brian Thorp is the founder and CEO of Wealthtender and serves as Editor-in-Chief. With over 25 years in the financial services industry — including nearly 22 years at Invesco, where he led strategic partnerships with wealth management firms representing more than $100 billion in assets — Brian founded Wealthtender to help people find financial advisors they can trust and make more informed money decisions.

A member of the National Society of Compliance Professionals and its SEC Marketing Rule Working Group, Brian was recognized by WealthManagement.com as one of its “Ten to Watch in 2024” for his work reshaping how financial advisors market their services. He holds a B.B.A. in Finance from The University of Texas at Austin.

The recent Ultimus 2026 Client Summit provided an informative industry event designed to offer an insightful update on the state of the asset management Industry for both registered and private asset managers and RIA clients. The Summit’s carefully crafted agenda addressed major industry issues and challenges by inviting financial industry experts to share insights and perspectives, along with numerous breakout sessions to allow for a substantial sharing of ideas, experiences, best practices, and the exploration of innovative strategies.

As a leading independent, tech-enabled provider of full-service fund administration, accounting, and middle office services for fund sponsors and investment advisers, Ultimus Fund Solutions (Ultimus) has grown considerably over the years through organic growth in new clients and a series of acquisitions. The firm’s growth has strengthened its administrative capabilities and consultative approach across the full registered and private fund spectrum.

It also positions them with a unique vantage point to keep a finger on the pulse of the rapidly changing operating environment, accelerating investment product innovation, distribution re-engineering, and technological transformation happening across the asset management industry in its registered and private fund space.

The 2026 Summit agenda reflected more than a roster of timely topics – it captured a broader strategic reality facing the industry: asset management firms are no longer preparing for gradual change, but for simultaneous transformation across product innovation, distribution, operations, regulation, and technology, and the confluence between registered and private funds.

Key 2026 Summit topics included distribution strategies, regulatory and compliance matters, middle office solutions, optimizing operations, fund governance, registered alternatives structures, ETFs, and cybersecurity. They also organized several excursions and networking opportunities with peers in the fund advisory community, industry experts, and Ultimus professionals from its registered, private fund, and middle office teams.

Overviews and takeaways from some of the sessions are highlighted below:

Ultimus Update: A View from the Top

To kick off the summit, Gary Tenkman, CEO, and John Lehner, President of Public Funds Solutions, shared their vision of Ultimus’ future.

Gary opened the 10th Ultimus Client Summit by discussing his tenure, the company’s growth, and outlining Ultimus’s strategy that focuses on best-in-class service, talent, and technology across a wide range of product wrappers. Ultimus has grown to be the only independent, tech-enabled fund administration firm with scale across all product wrappers, including mutual funds, ETFs, private equity, retail alternatives, and middle office services – a unique competitive position compared to large global custody banks.

As evidence of the firm’s investment in people, he noted the company’s growth from 350 employees in 2019 to nearly 1,300 today, with over 100 hired in the current year alone. Firm growth has led to Ultimus currently supporting over 450 investment advisers, 2,500 funds, four million shareholder accounts, and $775B in assets under administration (AUA).

He also highlighted a key priority of expanding capabilities in Europe and other jurisdictions to better serve clients wanting to distribute funds globally. Announcing a clear vision of expansion signaled the company’s international growth ambitions.

John Lehner followed, reinforcing the company’s core ethos of “service, service, service,” which he framed as “service at scale” – meaning the combination of its client-centric culture with a robust, scalable technology and data infrastructure.

The Summit theme of the “Power of Partnerships” was characterized as a testament to how partnerships amplify possibilities and enable the seizing of new opportunities together by harnessing the collective strength of the community to shape a brighter, more successful future. At the heart of the power in partnership lies the ability to drive progress and achieve extraordinary outcomes through collaboration. He especially thanked clients for their presence and participation at the Summit, making the event even more special and meaningful as everyone can dive into the future of administration, technology, and innovation side by side.

He also discussed the goals of the conference to foster connection, provide education, and listen to client feedback; introduced his public funds team; and emphasized how the company’s focus on scalable technology, seamless data integration, and the responsible adoption of emerging technologies like AI, positions Ultimus as a forward-thinking partner for their asset management clients that is prepared for the future of the financial services industry.

Washington Watch: What’s Ahead for the Industry

This panel of seasoned Washington observers from the ICI, Thompson Hine, and DLA Piper shared practical observations on evolving policy discussions and what policy changes mean for the industry – delivering timely intelligence for investment advisers, trustees, and other industry professionals navigating a rapidly changing environment. Insights into enforcement dynamics were provided to help inform compliance strategies.

Main discussion points revolved around three key areas: tokenization, the use of Artificial Intelligence (AI) in the industry, and the Department of Labor’s proposed rule on alternative investments in 401(k) plans. Speakers explored the implications of tokenization for asset distribution, investor experience, and regulatory frameworks. They also delved into the increasing adoption of AI by investment advisers, the regulatory challenges it presents, and the potential for AI to transform prospectuses and investor interactions. The SEC has already acknowledged the current state of e-delivery as a “crazy quilt,” indicating its archaic nature and the need for re-evaluation and improvement.

Finally, the discussion touched upon the Department of Labor’s efforts to allow alternative investments in 401(k)s, with skepticism surrounding its clarity for litigation avoidance, and the broader impact of regulatory changes and enforcement on the industry.

With the consensus that the industry will be very different from what it is today in five years – not 10 or 15 years, mind you – the most interesting projection made was on tokenization, where in five years most products will be tokenized and most people will be investing through a wallet. It was cited that Schwab reported that their mutual funds have already been tokenized in Europe by third parties, demonstrating that tokenization is occurring independently of direct issuer action.

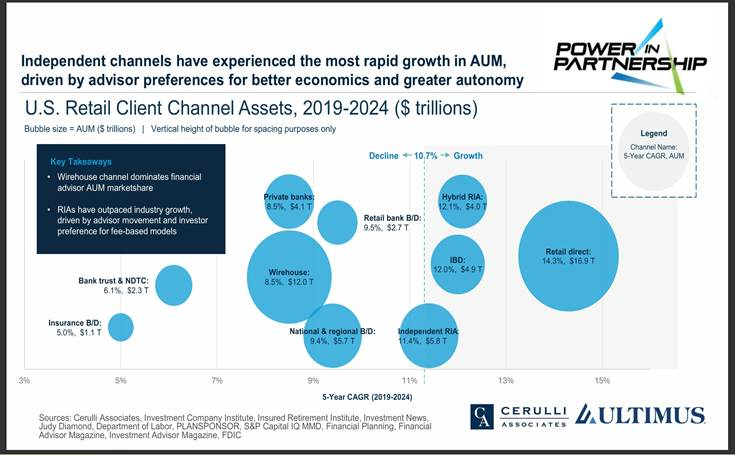

Today’s Market Pulse: Product Trends and Capital Movements

This data-driven session examined the latest investment product trends and how asset management firms are adapting to a rapidly evolving investment landscape, particularly the shift towards retail distribution and the increasing complexity of investment products. The breakout was led by Nickolaus Darsch, Chief Commercial Officer, Ultimus with Brendan Powers, Director, Product Development, Cerulli Associates, and Kerri Heidemann, Director, Asset & Wealth Management Consulting – North America, Alpha FMC.

The data presented on channel growth (see Cerulli chart below), product adoption, and operational challenges informed asset managers about critical industry shifts that can guide strategic decision-making. The insights into evolving financial adviser needs and the complexities of new product structures like ETFs and alternatives were offered to help firms prioritize investments in technology, talent, and distribution strategies. The discussion on AI specifically highlighted a forward-looking trend that firms need to consider for future operational efficiency and innovation, like exception detection, reconciliation, and onboarding.

Key points:

Retail client channels are growing significantly faster than institutional channels.

Firms are adapting their business models to offer advanced financial planning services.

Asset managers are making strategies more accessible through new vehicles like ETFs and SMAs, and by expanding into different investment options such as direct indexing.

Asset managers are increasingly providing support to wealth managers in areas like customization, personalization, and model portfolios.

ETFs have become commonplace for financial advisers, with increasing comfort in active ETFs.

Operational hurdles for ETFs include managing daily portfolio changes, daily disclosures, and establishing capital markets teams.

The dual share class for ETFs presents regulatory and economic challenges.

Alternatives are moving into the private wealth channel, with a shift towards semi-liquid funds like interval funds and evergreen funds.

Managed accounts are evolving beyond equity to include fixed income and options, with a trend towards model-delivered SMAs.

Model portfolios are a key way for asset managers to provide scale to wealth managers, offering investment strategies, client communication tools, and implementation support.

Image Credit: Institute for Innovation Development

From Niche to Mainstream: The Rise of Retail Alternative Fund Structures

As retail access to alternative assets continues to expand, fund structures are evolving to meet growing demand. This session unpacked the operational, regulatory, and structural considerations behind interval funds, tender-offer funds, BDCs, and ’34 Act private funds, highlighting the key considerations advisers need to evaluate when looking to launch retail alternative fund structures.

The panel, led by Nicholas Ablahani, Managing Director, Head of Retail Alternative Administration Product, Ultimus, brought together legal and operations specialists to examine how interval funds, tender offer funds, and business development companies (BDCs) are reshaping the way retail investors access private markets. The discussion also touched on fund structures gaining popularity, including ‘34 Act funds, registered 3(c)(7) funds, and outlined the factors advisers should consider when evaluating these structures.

Panelists worked through the structural distinctions that matter most to advisors. Interval funds offer continuous daily subscriptions paired with mandatory periodic repurchase offers, while tender offer funds give boards greater discretion over both the timing and frequency of repurchases as well as net asset value (NAV) striking cadence. That added flexibility, the panel observed, has meaningful downstream operational effects on shareholder servicing, distribution platforms, and the role of the transfer agent. BDCs were positioned with much different considerations: subject to SEC diversification requirements, focused largely on lending to private US companies, and reporting on a 10-Q and 10-K cadence rather than the N-CSR, N-PORT, and N-CEN regime that governs registered investment companies. Across all three structures, the panel identified a consistent set of pre-launch questions that sponsors should be wrestling with early, including seed capital sizing, target asset under management (AUM) thresholds, NAV frequency, liquidity management, and the valuation framework for Level 3 assets.

Operational readiness emerged as the through line. Panelists walked through legal formation, board and chief compliance officer appointments, and the assembly of service providers spanning legal, audit, fund accounting, fund administration, transfer agency, tax, and compliance administration. On the distribution side, the conversation turned practical: how the NSCC Fund/SERV and DTCC pipes interact with daily versus periodic NAV products, the data hurdles advisers routinely encounter at onboarding, and the recordkeeping nuances of private BDCs and 1934 Act private funds that rely on capital commitments and closings rather than traditional subscriptions.

The session closed on regulatory and market context, with commentary on redemption pressure in private credit and the proration mechanics that interval and tender offer funds rely on when repurchase requests exceed the offered amount, alongside heightened SEC scrutiny of valuation policies for hard-to-value assets sitting inside daily NAV vehicles. The takeaway for readers: retail alternatives have crossed into the mainstream, and the operational, governance, and valuation infrastructure behind them is now where the real competitive differentiation lies.

Solving the Unstructured Data Problem

This panel led by Mel Van Cleave, SVP, Technology and Jason Stevens, EVP, Chief Technology Officer, Ultimus with Jack Lupica, Senior Sales Engineer and Strath Lanyon, Chief Client Success Officer, Xceptor, addressed how asset managers are inundated with unstructured data – from PDFs and emails to tax documents and research reports.

The session explored how cutting-edge technologies like Generative AI and Natural Language Processing (NLP) can transform this data into actionable insights, empowering more informed decision-making, and uncovering tradeable opportunities. The discussion on the need for AI security and data governance served as a crucial guide for organizations navigating the complexities of implementing these new technologies responsibly.

A key observation was made that many people assume the pain points show up at the back end of operations, whether it is during reconciliation, or when operations teams are dealing with the data already in the system. The reality is that the problem needs to be solved upfront, at the ingestion stage where governance and normalization are established. That front-end work is where about 90% of the friction lies, when it comes to getting the data into the systems cleanly and consistently.

Further discussions around SEC announcements regarding AI records suggest regulatory bodies are actively considering and preparing for the impact of AI. The concept of an “operational control tower” – integrated platforms that provide real-time monitoring, root cause analysis, and guided response for data incidents – offered a vision for future operational efficiency and risk management.

From Back Office to Powerhouse: Scaling Investment Operations Data for Growth

This session explored how investment operations teams are strengthening their data using modern technology and smarter processes to specifically support growth.

Keith Totten, Founding Partner, Aliter Investment Solutions and Paul Wahmann, SVP, Head of Middle Office Services, Ultimus, along with client testimonials, discussed what is working, what has changed along the way, and how new tools are helping turn investment operations data into an advantage.

Key topics included:

Prioritizing which data and operational challenges to modernize first.

Turning previously siloed operational data into actionable insights.

Experiencing a clear connection between stronger data practices and business growth opportunities.

New data capabilities – like lineage, cataloging, or real‑time access – delivering big improvements.

Measuring ROI data quality improvements.

Evaluating technology partners or platforms.

Emerging technologies that have the biggest impact on investment operations in the next 3–5 years.

Scaling Excellence: Future-Proofing Operations, Technology, and Tax for the Private Credit & Multi-Asset Era

As the private funds landscape shifts toward yield-driven private credit strategies and retail-accessible structures, the “back office” has become a critical driver of institutional credibility. This panel explored how fund managers are navigating a new era of complexity, where specialized credit data hooks, process automation, and integrated audit and tax strategies are essential for survival in 2026.

The panel led by Chris Cullison, Managing Director, Head of Private Funds Product, Ultimus, analyzed the shift from siloed workflows to digital-first models capable of handling the unique valuation and reporting demands of private debt alongside traditional assets to meet heightened LP expectations for transparency.

Cyber Crisis in Action: An Incident Response Walkthrough

Of particular value was a two-part interactive breakout session and engaging tabletop exercise led by Shawn Waldman, CEO and Founder, SecureCyber in simulating a real-world cyber incident. Attendees were asked to openly participate and consider “What would you do?”

The panel walked through initial responses and key decision points in managing a cyber crisis and demonstrated effective response strategies. Attendees gained deeper insights into mitigating risks, improving preparedness, and safeguarding organizational integrity during a cyber attack.

Meet the ETF Market Participants

This session focused on the critical roles that key ETF ecosystem participants play in the success of an ETF launch and long-term growth strategy. The discussion featured Trammel Robinson, Director, ETF Issuer Relations, ETF Global, Paul Weisbruch, Head of ETF Issuer Services,GTS, Greg Schmidt, Director of ETF Listings,CBOE, and Michael Prendergast, SVP, Senior ETF Product Specialist, Ultimus.

While innovation and product development are accelerating, the panel emphasized that successful ETFs are ultimately supported by a strong ecosystem of partners across trading, listings, operations, servicing, and distribution.

A major theme throughout the discussion was the importance of understanding how ETF liquidity is created and supported. Paul Weisbruch discussed the role of lead market makers from pre-launch through ongoing trading support, emphasizing that liquidity is often driven more by the underlying securities and ecosystem support than simply by trading volume on screen. Greg Schmidt highlighted how exchanges have evolved beyond simply being listing venues and now play a strategic role in supporting issuer visibility, education, branding, and capital markets connectivity. Michael Prendergast discussed how issuers are increasingly evaluating differentiated product structures, including ETF share classes and alternative investment strategies, while also stressing that many new entrants underestimate the importance of operational planning and distribution strategy early in the process.

The panel also explored the continued rise in ETF launches and whether capacity constraints are beginning to emerge across the ecosystem. Panelists noted that service providers are becoming increasingly selective in the products they support, with greater emphasis being placed on differentiation, distribution readiness, and long-term viability. One of the key takeaways from the session was that launching an ETF has become more accessible than ever before, but achieving scale and gathering assets remains highly competitive. Successful issuers today are those that not only bring innovative ideas to market, but also understand the importance of liquidity support, operational infrastructure, strategic partnerships, and thoughtful distribution planning from day one.

The Intermediary Landscape in a Shifting Distribution Environment

Led by Kevin Guerette, SVP OF Distribution, Ultimus and manager of the Ultimus Distribution Advantage Program, a panel of leading industry intermediaries from Fidelity, LPL, Charles Schwab, and Osaic Wealth shared their approach to engaging with diverse product structures, meeting platform inclusion requirements, and building strong manager firm relationships.

Besides explaining the basic elements of gaining access to these firms and their platforms, they also spent time discussing product usage, investment product trends they are seeing, and directionally where they think flows are heading into the balance of 2026 and beyond. This session offered practical strategies to position investment offerings for success in today’s competitive landscape.

Executing a Distribution Plan in a Multi-product Environment

Also led by Kevin Guerette, SVP of Distribution, Ultimus, this session brought together experienced client partners to share their expertise in distribution strategies. Focus was placed on the successful path each has been on, how they have deliberated to arrive where they are today, and how they are assessing where they need to be in the future.

Topics included product development decisions, leveraging technology, maximizing conference exposure, and implementing wholesaling, national accounts, and marketing best practices. A special focus was placed on distributing multiple product structures, such as mutual funds, ETFs, separate accounts, model delivery, and alternative funds. It provided practical and insightful guidance for dealing with the complexities of a multi-product environment.

Transforming the Future with AI

As the closing keynote, Henry Lindemann, Co-Founder and Chief Growth Officer, BlueFlameAI shared how to build a robust framework for innovation risk and effectively plan for constant change in the rapidly evolving AI era. The session provided strategies to stay ahead of the curve and harness AI’s transformative potential in a fast-paced landscape.

After starting with explanations regarding the basics of LLMs and AI Assistants, along with the two types of AI – Generative and Agentic AI – and their different purposes, he explained that the AI Feature Arms Race is a dead end as AI capabilities are commoditizing. True institutional advantage comes from architecture.

What actually differentiates is: workflow integration embedded in how you actually work; data connectivity to your systems of record; institutional governance of security, compliance, audit trails; and continuous model optimization where you are always using the best AI for each task. No single model wins every task: the answer is multi-model routing.

He offered how Agentic AI is delivering a clear ROI and leading to increasing adoption:

Customer service – 25% shorter call times, 60% fewer transfers.

Sales agents – 10–30% conversion increases.

Supply chain – 40% delay reduction via multi-agent workflows.

Commerce – Visa, Mastercard, and PayPal launched agent-capable systems.

Projected $5Trillion in AI-mediated global commerce by 2030.

40% of enterprise apps to embed agents by the end of 2026.

Conclusion

The Ultimus 2026 Client Summit provided an informative and insightful conference program that helped reinforce the massive nature and scope of the transformations occurring in the asset management industry. The Summit gave attendees a valuable perspective on the forces reshaping the industry, while also making clear that the lines between the registered and private fund spaces are increasingly converging, creating new opportunities, operational demands, and strategic considerations for asset managers moving forward.

More than a recap of trending topics, the Summit underscored a key takeaway: competitive differentiation will increasingly depend on how well firms align strategic vision with operational readiness, governance, and technology execution. Adaptation is no longer a response to change, but an ongoing business discipline.

With its every 18-month month cadence and breadth of issues addressed, the Ultimus Client Summit continues to establish itself as a meaningful industry gathering for asset managers and industry partners alike. Combining education, partnership, and practical insights, it is a worthwhile event for those who want to stay informed about the innovation and evolution in asset management.

For full disclosure, Ultimus is an Institute Founding Member, and I have always attended their events to stay informed and be in an optimal position to report on the evolution and innovation happening in the asset management industry.